Without a doubt, the impact of automation on the IT Services industry is a topic of much debate and contention. The challenge is that speculation drives much of the discussion, rather than quality data and analysis.

While the subject of automation has been discussed a few times on the blog, I feel compelled to add my experiences and those of the IT professionals I met on my travels to the discussion.

Not long before joining HfS, I spent several months presenting research on automation at events and conferences across the UK. While the research covered a broad range of topics, automation in IT services was by far the most popular. After a few presentations discussing the increased adoption of automation and the growing capability of the tooling, it became apparent where the popularity of the topic originated – fear. After each session, a small gathering of IT professionals would question me on job security, headcount decreases and how automation augered a bleak future for the industry.

It’s not difficult to see why the audience felt this way. The mainstream media and even some analyst firms have been stoking the climate of fear with considerable vigor.

So I went back to the drawing board and changed my presentation. I took a fresh look at the data to examine what was happening in the industry – did we genuinely need to worry? Beginning with an impactful quote most media outlets were running with – something along the lines of “be terrified, the robots are coming” – I started to dismantle these theories with my research data on employment trends, headcount increases, and industry perception.

While many argued that automation would lead to job cuts, my data showed the opposite. Organizations recognized the importance of technology to their businesses and were investing in the services needed to support it. The data revealed that in organizations with higher levels of automation, workers were not disappearing, they were moving to higher value areas of the support structure – taking on strategic projects or developing services.

At the end of the presentation, I concluded that the reality of automation’s impact on modern IT services was far from the bleak picture painted by other analysts and consultants.

Nevertheless, a few minutes after the session ended the same horror stories started to emerge: IT leaders facing a backlash from staff as automation projects ramp up and professionals working themselves into a frenzy over their job security if projects continued. It was frightening stuff.

Crucially, my research revealed that the cause of this panic doesn’t come directly from the automation itself – there were almost no real-life examples of automation leading to sweeping changes in any of the organizations I was working with. Without a doubt, much of the fear was generated by analysts and media outlets whipping up this distorted perception, but surely there must have been another force at work.

After a bit of digging around the real cause of the hysteria became clear. In organizations with little or no perception issues, it was clear that the leadership team had taken the time to communicate with their teams. Conversely, those with stressed and worried staff had not.

When I questioned an executive who sought advice on soothing fears in his team if he had clearly explained his vision, and what the outcome of the project would be, he replied that it was obvious what he was trying to achieve. If that were true, the perception crisis in his organization would not be there.

Successful automation projects have an engaged team working behind them. The most effective I have seen understand what will be automated and why. They know what impact it will have and, for the most part, agree it was an area of manual work they found repetitive, boring and unfulfilling anyway. They eagerly anticipated a time when they could dedicate their efforts to more meaningful and valuable work.

Under different circumstances, this committed group would be dealing with the same fear and stress as their peers in organizations with less effective communication.

In the noisy information age we now live in, it’s easy to get caught up in the hype. Business leaders have an obligation to provide clear, effective communication that outlines the vision and journey of automation projects. Without the context and understanding they provide, an engaged team can quickly turn into a stressed one. And a stressed team will undoubtedly hold your project back. It’s not hard to understand why an individual afraid of becoming obsolete may not be working towards your goals with total enthusiasm.

Bottom Line: Effective communication strengthens the fine line between a successful automation project and one held back by a nervous and stressed team.

A few weeks ago, I was fortunate enough to spend some time talking with the head of IT of a large transportation company – and we talked about the future of his job and the most important things impacting his role. When I asked him what was the main issue getting in the way of him adding value to his business, he said it was a cloying inertia brought about by a thick soup of negative thinking.

The number of people in his organization that focus on the way things have been done in the past and the reasons why things can’t change, were a source of incredible frustration to him. Incremental change was possible, colleagues understand how processes evolve, so innovation could be staged, but it was very hard to implement anything totally new. We joked that original thinking was being pecked to death by negativity, like a flock of miserable seagulls.

As an analyst, this is something really close to my heart – if we are to produce anything that approaches original thinking, we need an environment where ideas are cherished and even the craziest thought is welcome – although it will ultimately need to stand up to scrutiny, the original thought can’t be wrong. It’s only when you make cerebral room to nurture some crazy, orthogonal thinking do you create inspirational work like the Digital OneOffice.

So what needs to happen, how can this change? How can we get people to take leaps of thought rather than increments?

Phil’s recent blog “Is your current job the end of the line?” delivered seven action points directly to the chief “peckers” of the world. Distilling that, the most important thing organizations can do to encourage this behaviour and become more open is to move away from traditional hierarchical relationships, look at the idea itself and any data that supports the idea. It is the addition of data and more evidence that helps to shift thinking from more traditional decision making.

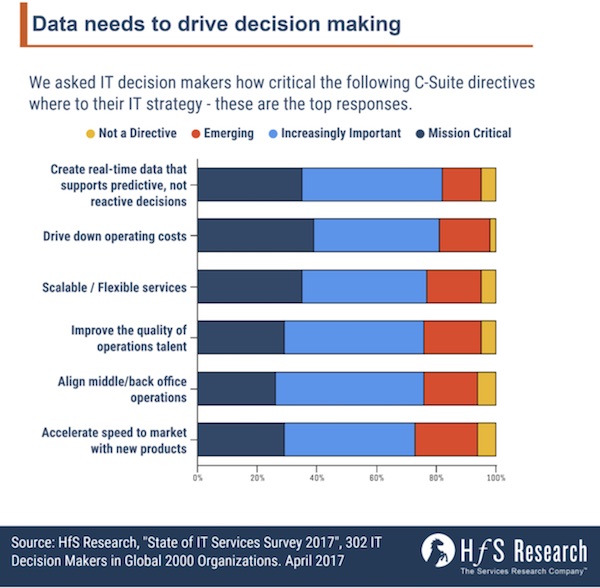

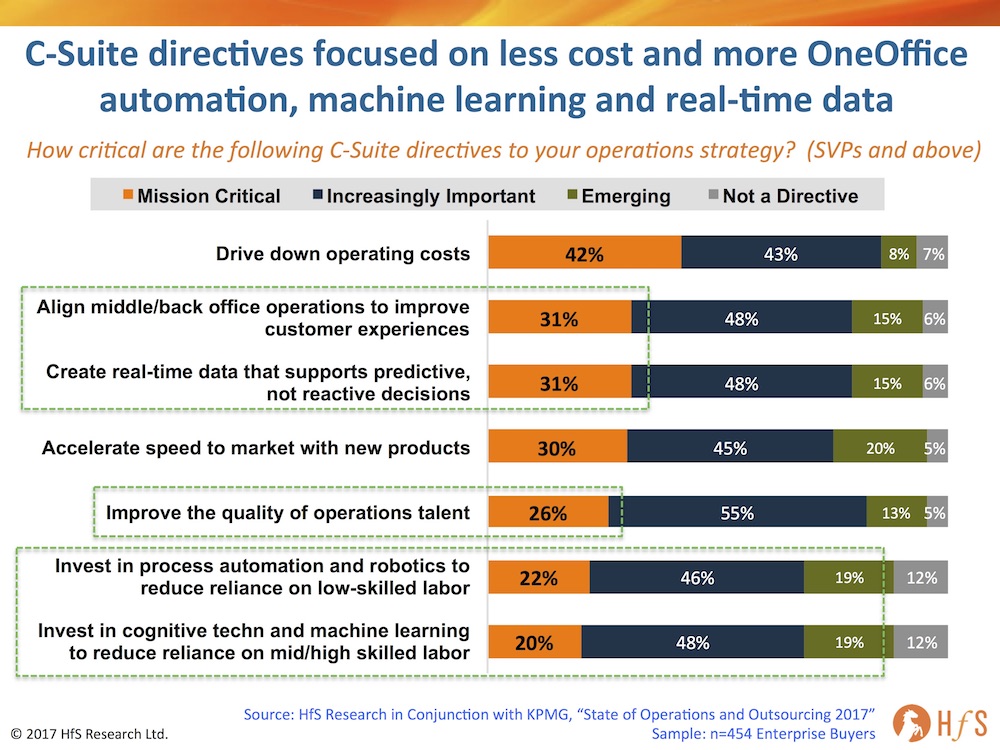

It’s interesting that the message, at least in terms of its overall importance, seems to be getting out at last. In a recent survey of 300 major Global 2000 enterprises, we asked IT leaders about the importance of some c-suite directives to their IT strategy.

This graphic shows that IT decision makers realise the best way that they can increase the relevance of IT within the organization is by supporting more predictive decision making. This is a crucial change in mindset, taking IT away from its most recent manifestation which has almost been as a custodian of IT, or a gatekeeper, focused on reigning IT in and keeping the costs down.

Bottom Line – data gives crazy thoughts wings

We suspect that part of the embracing of data by IT departments goes back to my friend and his battle with the naysayers. Data levels the playing field and gives more people a voice. It gives more power to the elbow of anyone seeking to make a change. An IT department that delivers insight will be listened to, as opposed to being largely ignored as a legacy function tasked with keeping the lights on. Let’s stopped being pecked to death.

A new trend is developing in the tech and business world and the speed at which it is happening is alarming. The need for people is waning as companies seek to scale themselves profitably on a digital backbone – and it’s having a serious impact on our career paths.

When companies historically did layoffs, it was because they were in financial peril and had no choice but to saw off costs to stay solvent on the balance sheet. It was always painful, because you needed people to grow your business. Sacking people was not a good thing to do.

Suddenly it’s in vogue to shed people

However, if you were unfortunate enough to get caught in a layoff, you dusted off your CV, went out on the job market and (usually) found yourself something pretty quickly. Companies needed people – whether they were superstars, or solid foot soldiers; when you needed an employer, you would always find something.

Now something different is happening in the mindsets of business leaders – companies which are doing really well are in the process of proactively removing staff – both at junior and senior levels. You really don’t want to get caught up in one of today’s layoffs if you’re eager to stay in a similar job in future, because the modern business is adopting a new mentality – cut costs and scale profitably with a digital backbone. Adding armies of people is no longer the order of the day when you peer into an uncertain future, and many savvy businesses are eagerly looking to get ahead of making savage future labor reductions by making them now, in a more incremental fashion.

Case in point, Cognizant has been the golden child of IT services growth over the past decade, the firm ballooning from $2bn in 2007 to $13.5bn exactly a decade later, and yesterday announced 11% year-on-year revenue growth and a 26% increase in year-on-year net profits to $557m. The company continues to outperform the market with relentless growth. Meanwhile, the same firm has recently (reportedly) laid off ~6,000 staff in India and has just offered voluntary redundancy to 1,000 director-and-above US staff – a sizeable chunk of its US workforce.

Meanwhile, we witness firms merging together, such as CSC and HP, with the prime goal to rationalise their armies of people, while IBM’s US marketing employees were recently instructed that they must report to and work at one of these main offices in America: New York, San Francisco, Austin, Cambridge, Atlanta, or Raleigh – and offering redundancy options to those unwilling to make the move (who have renamed their firm “I’ve Been Moved”). And expect similar activities involving many of today’s IT juggernauts, such as Accenture, Capgemini, Deloitte, Infosys, TCS, Wipro, etc – all these firms are looking to deliver more “digital” services for clients with less people, as part of their “digital automation” drives. We’ve also been hearing about leading BPO providers bragging about delivering their traditional services on 10-20% less people, because they have figured out how to automate their services using RPA software and are making progress adopting machine learning techniques to speed up data driven work.

This isn’t just about corporate greed anymore – firms just don’t need people like they used to

One constant between now and the Great Recession of almost a decade ago is the insatiable greed of corporations and their shareholders to maximize quarterly profits at whatever cost to society and long-term planning. However, the rapidly emerging trend that is really causing alarm, is this determination to grow businesses while reducing their workforces, because the majority of people are now very replaceable with technology. We’ve never seen a situation where firms are growing their revenues, maintaining (and often growing) fat profit margins, but eagerly looking to trim whatever “fat” they can find.

New data from our 2017 State of Operations and Outsourcing Study, covering the dynamics of 454 global enterprises, highlights the emerging dynamics of C-Suites seeking both to slash costs (85%) but also to digitize their operations by breaking down the barriers between front and back offices and driving real-time data to support decisions (four-fifths see this as mission critical / increasingly important). Most alarmingly, only 26% of C-Suites now view developing talent quality as mission critical, while only 12% have not yet embarked on investments in automation and machine learning to reduce reliance on both low-end and mid/high-level labor:

The skills that were in demand, even 5 years ago, are now almost defunct, as marketing, programming, accounting, administration skills that were reliant on people, now being significantly enhanced by software, analytics and algorithms. What required 50 programmers, analysts or accountants 5 years ago, can be done by a handful of smart thinkers and much smarter systems. If you are in a profession like HR or procurement, the chances are your firm gave up on scaling up your division a decade+ ago and the emergence of affordable technology suites that do the job has already left these functions operating with as lot less people. Now this is happening right across the board, as the value or programming is diminishing (the future of IT is about smart logic and smart algorithmic thinking, not programming), the need for data analysts is shifting to simplicity as opposed to complexity, marketing is more about data science than content creation and finance is more about predicting data than archiving it.

So how do we survive? Here are seven tips to seriously save you

Before we embark on steps we can take to save ourselves, I would love to recommend a host of courses you can take to sustain your relevance in the modern workplace. However, there really isn’t a defined curriculum for this stuff – you need to develop a strong “unlearning” appetite to develop yourself on the job to get better at communicating and articulating your ideas, understanding how to manage data sets with greater logic and focus, and become a better collaborator, team player and driver of initiatives, with really visible impact on the business.

Firstly, you need to Unlearn – and fast. The first thing we all need to do is unlearn the work habits we picked up over the last decade or two. What was considered sufficient to check the boxes 5 years ago is now already in the legacy box (or, as I hate to call it, the “voluntary redundancy” box). The good news if your company probably still turns in a lovely fat profit, so they can still afford you. The bad news if you need to adopt a mindset of helping them grow profitably if you want to keep your job long term.

Secondly, crank up the urgency. You must focus on speed and urgency with short-terms plans to realize your long-term vision. Really look to deliver results in weeks not months and keep delivering robust outcomes as you go to enhance your credibility . Think of each individual project as a milestone achieved on a longer journey.

Thirdly, you must leave your comfort zone. Everyone in our industry needs to get out of our comfort zones, being bold, and smart about trying new ways of thinking, interacting, collaborating and driving positive energy. You have to venture outside of your comfort zone and take your colleagues and partners with you. You have to believe in what you’re doing and make smart, pragmatic – and sometimes bold decisions along the way.

Fourthly, focus on “quick wins”. Get stakeholders onside by demonstrating meaningful, impactful outcomes without major resource investments. Find a broken process that you can quickly fix with RPA or a SaaS/mobile app, or simply by converging data. Then find another… self-contained projects where you can prove your value quickly are the way forward, not hiding behind big projects that are hard to prove the ROI and seemigly never-ending.

Fifthly, focus on much more dynamic reporting relationships. The need for dynamic management is desperate in so many firms today: managers and staff must constantly interact to fine-tune performance against evolving outcomes. You need to manage up and down in the same constant manner, where relationships are fluid and dynamic – where you are constantly challenging each other with new ideas and ways of doing things . The days of the old “weekly box checking meeting” is over..

Sixthly, be smart about data and how it drives value to your job. Whether you like it or not, data is at the core of every modern enterprise – and you need to get with the program. If you can’t automate and digitize your rudimentary processes, you will quickly run out or value to any organization in today’s era. Being smart about data is no longer geeky, its career-critical.

Seventhly, put your ego aside and get used to flatter org structures. Companies need to kill the hierarchies and most emerging digital business have already adopted a flat structured approach to team building. People naturally collaborate in cross-functional teams motivated by shared outcomes. So put aside your old mentality of climbing the greasy corporate pole and get used to a whole new wave of politics – that of collaborating in flatter, autonomous teams where egos are driven by collective success, not just individual achievement.

This week we crossed the Atlantic to meet the cream of the crop of the utility industry in Miami for the International Utilities and Energy Conference, hosted by Accenture. A packed agenda entertained the brightest minds in the utility space from around the globe.

We were in for a surprise: from the first session to the closing key-note it was one big future-oriented gig, focusing on business value instead of enabling technology. No sales pitches from the provider (many providers can learn from this), zero bad jokes… and a highly engaged audience (yes, we are still talking about utility executives here) that wanted to smell, touch and work towards a better future with more and better client interaction. They all want to be more profitable but more important (for real) greener! Their customers demand it; the infrastructure is ripe for an upgrade, and so the question is, why not make it happen?

Fossil is the new uncool, and renewable energy (with loads of digital components for their clients) the new hipsters, the future of utilities!

Let us explain with a couple of fantastic examples that had a high impact on your peers at this week’s event. Over to you Derk!

Thanks, Bram. We had an interesting time for sure. Let me give you some quick pointers on the new, the unexpected and the future that headlined IUEC 2017.

A dizzying barrage of industry shattering disruptions thrown at attendants

As one Utility executive put it; the first day of the event was a succession of shock and awe, fear and nausea. Florida Power & Light CEO Eric Silagy set the stage immediately; the unstoppable force of renewables and how being clean is good business. It is a vision that not everyone dares to execute on as radically as Florida Power & Light, but they are doing it without hesitation. CEO Silagy provided an excellent example of lowering his customer’s bills by taking the most polluting oil and coal plants offline.

In this picture, you see a perfectly well-operating oil based power facility Florida Power & Light just blew up (after many people try to stop them) to build a far cleaner and more profitable (not only for them but also their clients) and this is just one of many examples. Don’t wait, just do it. There are always excuses, but just doing it will pay off in the end.

Further, he explained his strategy for relationship building with the regulators, being proactive and ahead of the curve and highlighted Florida Power & Light’s investments to build a more resilient infrastructure to deal with (the ever increasing) hurricanes’ ravaging effects in his service area.

Salim Ismail of ExO Works and Singularity University, talked about Exponential Organizations, and the drastic competitive forces these present in many markets. As electricity shifts from a scarce resource to an abundant resource, the dynamic of the market changes. Exponential organizations find business models to leverage abundance. Ismail explored Airbnb, GE and Ford’s journeys. One key takeaway that resonated with the audience is how innovation in large organizations is almost impossible. Innovation needs to be positioned at the edge, insulated from the internal organization. Large organizations have immune systems that attack any threats to the status quo, i.e. innovation. This is particularly relevant to utilities; being large, engineering-oriented and traditionally conservative organizations.

Accenture’s Digital guru Mark Sherwin brought his analogue chicken Penny to illustrate digital business models (his chickens and eggs turn out to be some of the world’s most expensive when factoring in the services he gets offered through digital channels to make his and the chicken’s life easier, from predictive food delivery to chicken hotels).

MIT professor George Westermann implored the audience to challenge pre-digital assumptions, as those hamper real transformation, reinforce the status quo and limit the ability to think outside the current frame of reference. Unintentionally providing great input for Design Thinking exercises.

Accenture’s Chief Strategy Officer Omar Abbosh shed light on disruptive forces over the last decades, from mainframes to IoT, AI, and Quantum Computing. He provided a great comparison of how he and Accenture’s leadership reinvented the strategy five years ago to rotate to “the new,” completely overhauling the organizational structure to change the culture, and how utilities are on a similar trajectory.

Vlogger and, more importantly, former monk Jay Shetty reflected on the Millennial mind, demystifying and busting myths. It turns out; millennials are not as scary as you might think. Jay called on the audience to incorporate four ‘Millennial mindsets’ (which are great for anyone by the way): the leadership of a coach, the fresh eyes of a child, community thinking and the mindset of a coder.

Missy Cummings, one of the first ever female US Navy’s fighter pilots and currently Duke professor of the Humans and Autonomy Laboratory Duke Robotics, talked about the highly relevant topic of drones and other unmanned vehicles and robotics’ potential in the utility industry. One of the key points she made addressing the fear robots will destroy jobs, is robotics and automation will likely create more jobs than destroying them, albeit different jobs requiring different skills, providing examples of people and robots working side by side in aviation.

It was time to evaluate all this and time to hit the Miami’s South Beach and more specifically Nikki Beach. The first feedback trickled in, and people had a lot to think about. Clearly, the platform that is IUEC worked.

Day two focused on more practical, “how to” examples and some great new research findings from Accenture and Bloomberg New Energy Finance about the industrialization of renewables, and Accenture’s global lead for Smart Grids Stephanie Jamison presented fascinating findings from a study of distributed generation (DG), focusing on business disruption of DG and the lack of clear forecasts utilities have around the impact of DG integration.

What stood out

At previous editions of IUEC, there were still reservations amongst executives about how fast digital and renewable energy would force change upon them. Those reservations are completely gone. Overall, utility executives have a positive outlook. Solid examples and cases are providing proof points and inspire the way forward, but there still a lot of work to be done.

A terrific event was wrapped up by living legend Clay Christensen, the godfather of disruptive innovation and Silicon Valley’s favorite guru. He gave the audience an excellent perspective and frame of reference of disruptive innovation and clues to shift capital investments to disruptive innovations to prevent becoming the next Blockbuster.

The Bottom Line

It is all about disruption and making a play instead of being played. Harvard Business School professor Christensen expressed his desperation for his industry – higher education – being disrupted with lightning speed by online learning and corporate universities. He did not worry too much about Harvard itself, but many universities are not that well funded and will be disrupted by new forms of learning leveraging technology. His response, without any hesitation, to a question about disruption in the utility industry was: “If you all pray for me, I will pray for you.”

From Derk and Bram; Godspeed, safe travels back home and until next time.

Just about 90% of CEOs who participated in a KPMG survey are concerned with the issue of changing customer loyalty, and the majority believe current their company’s products and services won’t be relevant to current customers in 3 years. That means they need innovation – now. They see technology (often referred to as “digital”) as an opportunity to move, but 85% of the surveyed CEOs feel they don’t have time to think about disruption and how to respond to it with innovation. This sets the scene for KPMG’s Analyst day recently in Boston. KPMG looks to bring purpose and passion for helping clients be successful in making innovation a part of the core of their businesses – through a diverse workforce, solutions, and collaboration.

With this backdrop, four themes stood out to us during the day about how KPMG is working with its clients:

A vision for “OneOffice” – work designed to address customer needs using “digital labor” and systems. Digital transformation is (finally) moving from the front office (customer touchpoints) to include the middle and back office (business functions and transactions) – and talk is moving from “how do we use ‘digital’” to “what problem do we want to solve for our customers and how do we use the possibilities of talent and technology to do it.” At HfS, we refer to this concept as “OneOfficeTM” – the need for businesses to break down silos in their organizations to create a more effective data and workflow for business outcomes, so this theme resonated with us.

As we are focused on “ making it real” and providing examples of where it is happening, we appreciated the story that KPMG told about a client they worked with to map out the customer experience. They registered a number of customers on an app and these customers recorded their experience in real-time, as did employees. KPMG captured the data in the Pathfinder tool and used it as input during a journey mapping session with employees from across the organization, front and back office, including a finance director, a customer service manager, and a valet. They talked through the points in time when the customers and employees had a poor experience and came up with ideas that were then prioritized for addressing through the client’s own innovation management approach. What stands out here is the breadth of people included in capturing the experience (customers and employees from different business units and IT) and the way the experience was captured (an app in real-time), which led to in-person workshops to map out various customer journeys and an action plan.

Additionally, staying true to the “ embedding innovation” theme, KPMG trained a number of the employees in departments throughout the client on the design thinking principles and methods used in the initiative. These people are networked as a COE. The team also has access to an analytics tool to continue to capture and analyze data on their journey.

2. A focus on defining and enabling the evolving role of workers and work. “Even in a digital world, humans are still the most important investment, the secret element of our brands, and the magic asset in the company,” said Robert Bolton, capturing the tone of the recent day. One example of a workforce transformation in progress was launched when a client started a discussion about the size and shape of the workforce of the future. This has led to questions such as “How do you know you have the right size?” “How does it have to change because of the advent of RPA and artificial intelligence?” “What are the impact on entry level jobs and the way those jobs provide a launching pad for careers?” “How does it impact learning, training, career paths?”

KPMG is not just working with clients to address these questions but shared its own experience in a changing workforce through the use of digital labor. For example, instead of having new hires who are eager, smart MBAs do mundane and repetitive audit work while they “pay their dues,” KPMG is able to automate much of that work and provide a more stimulating and challenging role for the talent they’re bringing on board. It’s changing the culture and employee work allocation models.

This area of “ digital labor” is one that the shared services and outsourcing group at KPMG is hearing a lot of questions about as well, according to the group’s global head, Dave Brown. Digital labor and cognitive are on the forefront of activity in evolving operating models and defining who (or what) does what. “Digital labor, simply put, is another form of outsourcing,” said Dave Brown.

4. Innovation starts with culture. Innovation needs to be a way of working in companies – it can’t just be siloed in one department or area. Key features of a culture that embrace innovation include diversity – of workforce and partner ecosystem; collaboration; and experimentation (these are also principles of design thinking). Having a culture and environment where it’s “OK to fail” is also a lynchpin of innovation. To provide a “space” and showcase for innovation, KPMG has broken ground for a new facility in Orlando to provide its clients and train its workforce with a multidisciplinary, hands-on, collaborative, high-tech experiential approach. And it’s partnering with the academic community to help develop (via technology, data sets, and case studies) the future workforce during the university years – for example, combining soft skills like teaming, collaboration, and critical thinking with critical technology skills for analytics and the subject matter expertise of accounting.

5. Deep investments in software to improve and automate complex processes. KPMG’s Spectrum unit created several “business intelligence engines” to automate and analyze several complex corporate processes like third party risk, contracts, and regulatory compliance like Automatic Exchange of Information (AEOI.) Beyond Spectrum, other tools KPMG discussed at the event include its KPMG Digital Responder, for security threat discovery and analysis and its KPMG FIRE regulatory reporting automation tool. While the KPMG teams mentioned a number of tools and IP throughout the day, and showcased a handful, a little of it felt “mysterious” – they were referenced by name and not explained or shown. These days when everyone is still exploring what digital really can do for them, showcasing case studies and tools can be really impactful in getting the message across.

What does this mean to you?

Digital transformation and innovation continue to dominate corporate boardrooms as buzzwords. But actually implementing requires a lot of complex detailed decisions that spur significant changes to the ways companies operate every day. What’s impressive about KPMG’s message is the firm’s ability to talk at the 100,000-foot strategy level but then dig into the last mile delivery details.

For clients that already work with KPMG, if you’re not seeing the kinds of messages the firm presented at the analyst day, then it’s time for a meeting with your account team. Talk about how some of KPMG’s new (and even not so new) techniques are being or could be, applied to your engagement. Don’t take it for granted that your account team will automatically propose new ideas so be proactive in asking for innovation.

For non-clients, take a look at Spectrum and other KPMG tools as stand-alone solutions. The Spectrum team told us they do sell the tools separately – they don’t just get embedded into larger services deals. This gives you the opportunity to get access to KPMG IP and operational expertise without having to exit any existing services engagements you have in place.

For an organization that candidly admits it was on the slower end of developing a stake in front office, its recent investments and acquisitions (a whopping 51 in the last 3 years) show that it’s quickly catching up, and also tying together the concepts of front, middle and back office nicely and in a forward-thinking way. Using their own interpretation of OneOffice, KPMG is forging ahead to help clients (and itself) break down the legacy barriers to become more intelligent and responsive client-centric enterprises.

A client asked me recently what happens to attempted transactions that are unsuccessful and do not go through. Does a blockchain implementation capture that data anywhere? The answer, barring the potential of some apps I’m not aware of, is no. Blockchains record completed transactions but attempted transactions that get rejected just go back out into the ether.

From a technology and business operations perspective, this isn’t a big deal. The system works just like it’s supposed to work. But if you’re interested in capturing data on failed transactions so you can monitor for fraud threats or do a forensic investigation if someone manages to execute a fraudulent transaction, then you’ll need a way to capture, store, and analyze the failed attempts.

Also, we need to distinguish a couple of points about blockchain security: 1) In this blog we’re writing about failed transaction attempts, not hacking attempts. Managed security services provider SecureWorks told me, “Hacking attempts are not the same as failed transaction attempts. Security systems don’t often monitor failed transactions in blockchain just as they don’t track failed attempts to use credit cards. The credit card systems capture that data about failed attempts.” 2) We’re writing about individual failed transactions that one particular company would care about. For example, Ethereum has penalties for trying to load bad blocks onto the network that dissuades bad behavior by participants. Also, at the network level, there isn’t a need for a system to capture failed attempts across all the participants, only the ones that pertain to one participant. Because a company wants to track how many times another party has attempted a fraudulent transaction specifically with it, not with all participants.

In essence, a failed transaction in this context is when someone uses stolen or fake credentials to try and create a transaction. This is the same as, for example, someone who uses stolen credit cards – sometimes successfully and sometimes unsuccessfully. It’s not a hacking attempt in the way security professionals think of them. But for those transactions that fail, companies might want to keep track and determine if any further action is needed, depending on the nature and criticality of the process. Actions could include suing the person or company attempting the fraudulent transaction(s) or changing some of the smart contract business logic to prevent such attempts in the future.

This leads us to the crux of the matter: you can’t expect your security team to protect you from threats they’re not able to detect. Instead, detection and monitoring of failed attempts need to be built into the application or integrated at the application level. Then your action plan should follow similar action plans that you follow with other applications regarding attempted transactions.

Bottom Line: As you experiment with blockchain and do some proofs of concept, make sure to ask your application vendor AND your blockchain services provider about blockchain security around failed attempts.

Here are some questions you can ask:

What’s your perspective on security considerations regarding failed transaction attempts?

Do you have any capability to detect and analyze failed transaction attempts? If not, why not?

What recommendations do you have to reduce fraud in your blockchain-based implementations and how are they different from recommendations for other kinds of applications?

The SAP SuccessFactors Influencer Summit, held in California recently, was an opportunity to see up-close-and-personal how the major HR Tech vendor views the concept of transparency, as not all players in this space view it the same way. It was, in a word, refreshing. Mike Ettling, company president, set the tone early by reminding participants what the company committed to the year before so they can be held accountable. Presentations were also ”open kimono” about execution areas they want to be better at in the next year, sharing many plans in detail – not just product plans and strategies (staples at such events) but spending hours on areas like delivery, support and even data centers (partly under NDA due to being within the earnings quiet period).

Throughout the event, speakers offered bold and somewhat surprising statements, and not always ones that blanketly served the software vendor’s interests. Ettling, for example, stated, “no one will be logging into HR Systems in five years time”. Other executives highlighted some subtle aspects of digital disruption; e.g., “it’s all about cloud adoption” (implication: not product adoption), and “trust is central to everything we do” (a great word for a company you’re taking a major journey with, and one which conveys product quality without saying those words).

As to Ettling’s proclamation about what is essentially the “no platform HR Tech platform” in five years, it led to a discussion of one of the company’s product strategy pillars, “Conversational HR.” The concept is to enable your employees to use interaction channels and platforms such as Slack, plus HR bots and “intelligent services” that connect and predict application actions and are embedded into daily work. Intelligent services are designed to transform HR operations through targeted analytics and machine learning, and cutting across relevant business processes. They were announced in August 2015 and there are 40 predefined intelligent services today; e.g., change of manager, employee department or job. This results in delivering a user experience that’s outside the traditional walls of both system modules and singular HR processes, and also involves linking HR and non-HR data. Also of note, SAP SF is now integrating Slack with its Continuous Performance Management functionality so employees and managers interact around, versus execute a process.

Improving the customer experience

The emphasis on usability and the customer experience was evident throughout; e.g., it’s fairly unusual to hear targets like this from an HR Tech vendor: Unlimited scalability, 99.9% availability and 80% of support cases resolved within 2 days. And the company has learned more about “attention to detail” in the mobile experience from its collaboration with Apple. I was also impressed with seeing plans to bring the customer support function into the digital era and make it a more engaging, tailored experience; e.g., by using such mechanisms as guided answers and even a tool for customers to easily schedule 1-to-1 “expert sessions” at a mouse click.

A “Peer Match” capability is now also being leveraged by the base. This is the company’s direct, peer-to-peer connection tool that allows SAP SuccessFactors’ customers to connect and share experiences with their counterparts within other SAP SF customers, from implementation to best practices to thought leadership. More than 227 “advisors” have self-registered and have made 200 connections in short order. Frankly, actively participating in a customer community (and sharing lessons learned for example) is one of the major benefits enjoyed by HR Tech customers of the cloud model, as you are on the same software instance and version. One other example of the customer experience focus is the new Digital Boardroom soon to be in production. It is touch-(boardroom) screen, dynamic, visual, based on multi-sourced data, and SAP SF’s HR Department was the design partner.

Fast take-up of newer capabilities

Continuing the theme of transparency, we learned that 260+ SAP SF customers have enabled or are using Continuous Performance Management: real-time coaching, feedback and learning even though it was more vision than seamless product capability when it was launched just two years ago. That is changing.

And beyond the vendor’s continuing product emphasis on candidate relationship management, internal mobility, better mid-market penetration and removing gender bias in decision making, two other interesting takeaways:

The “marketplace” concept is catching on in the HR Tech space, as now another vendor is making it easier to find and inter-operate with 3rd party apps that are innovative or focus on a specific area of HCM functionality. It’s a great marketing / PR tactic, as current/future competing products probably won’t find their way to the marketplace. 157 apps are available today.

Diversity really does matter to SAP SF, as highlighted in the anecdote shared about a developer asking: “How come in the org chart a blank image (for a vacant position) is always a man?”, thus bringing about a change in the vendor’s org chart.

Outstanding questions

While the presentations and sessions with experts and customers provided considerable information and insights, I’m left with a few additional questions:

Shouldn’t HR Tech vendors also be transparent about their product roadmap prioritization process, not just the roadmap itself?

How can change management be done effectively when you’re so focused on reducing deployment times?

Will SAP SF’s support of more flexible organizational structures cause similar issues that Workday customers experience when interfacing HCM with 3rd party Financial Systems?

Bottom Line:For more than 10 years, SuccessFactors has emphasized cool, innovative features, an engaging, consumer-like user experience – and in more recent years, rolling out a Core HR System and additional Talent Management components (e.g., recruiting and learning). Now, by also addressing issues like diversity and biased decision making, and by embracing and executing on the Conversational HR vision, SAP SuccessFactors is poised to weather uncertain times in general, and maintain its top-tier market position.

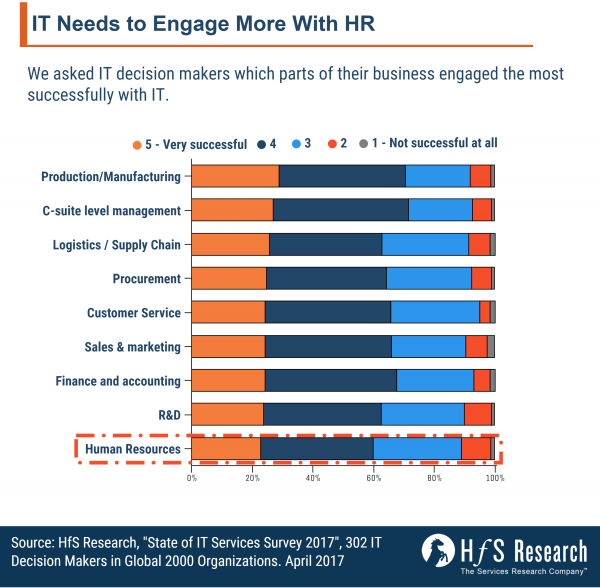

And here’s another core finding from our “State of IT Services Survey 2017”, where we spoke to 302 IT service decision makers from the Global 2000 to find out what they think of their IT services and digital consulting providers.

We asked IT decision makers to rate how successful different business units were at engaging with IT. The chart shows the top level results for all the business units.

The good thing is that the majority of business units have a broadly successful relationship with IT, with 66% of responses being successful or very successful – which is encouraging. Although that means 34% of business units don’t have successful relationships with their IT departments – which for Global 2000 organizations in such an increasingly digital age is worrying. Although we are likely seeing the tension of business units’ desire to use IT to operate more dynamically being tempered by their IT departments’ conservative nature to act in a safe operating environment.

HR departments have the worst relationships on average, with 40% of IT managers questioning whether the engagement is successful. This is concerning as IT departments need to demonstrate how technology can be applied in an HR setting – it is not just about buying the latest SaaS product like Workday. Looking at how data can help fuel better decision making for HR leaders, use predictive analytics to identify employee needs and use IT tools to assess potential employees more objectively. HR also has a key role to play in data protection and instilling the right culture of data protection within the organization. Given that employees pose one of the biggest data protection threats, IT should get HR onside.

Bottom Line – good IT fosters good relationships, poor IT fosters poor relationships

What has not detected in our surveys is an inflection point in IT and business unit relationships – whether the reliance from one to the other is increasing or decreasing as when we compare with similar survey work the change is only small on average. However, it does appear that the better relationships seem to be getting better and the worse relationships seem to be getting worse. Given that the choice to use external IT is easier (if not necessarily cheaper) than it has been – the fact that the worse relationships are getting worse is a worrying sign for IT departments. With the growing increase in the functionality and the breadth of SaaS and cloud services, it is not mad to envision a time when a large organization could move beyond the internal IT department toward a matrix of cloud procured products and services. So it is vital that IT continues to foster these relationships – get better or get bumped.

The intersection of Artificial Intelligence (AI) and personalization in HR / HCM offers the opportunity to significantly elevate service delivery, and therefore employee and manager satisfaction and engagement. It also highlights the looming challenge of getting the mix right between human and machine or “bot”-based HR. These critical topics were discussed during our recent Digital HR webcast.

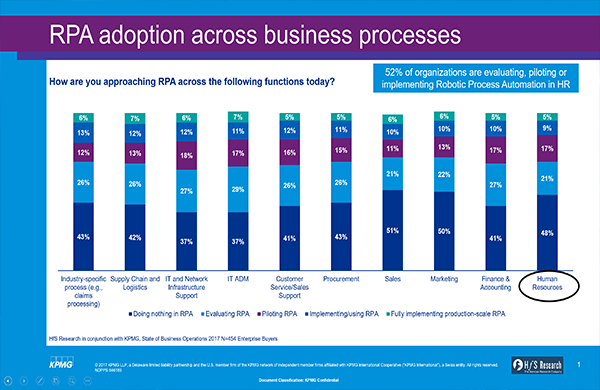

The evidence? Our annual “State of Operations and Outsourcing” study of 454 major global enterprises, conducted with KPMG, just revealed that 52% of enterprises are already evaluating, piloting or implementing robotic process automation (“RPA”) solutions for HR processes. HR executives: Like it or not, the new world of HR Tech automation has arrived, and you need a definitive strategy to deal with it.

How are enterprises approaching RPA in the HR domain today?

We already know that “science” has for years been leveraged in the recruiting domain in the form of assessments that predict the best talent, culture fit, leadership potential, retention likelihood, etc. And with the initial wave of HR chatbots or digital HR assistants converging with many new personalization capabilities to further enhance the user experience, the range of potential use cases linking these two themes for enterprise benefit is only limited by one’s creativity and understanding of operational HR.

Here is a small sampling of what HR Tech buyers will likely see from their vendor partners, and in many cases, sooner than one might expect. HfS Research just published a detailed POV (point of view) with more examples under the categories listed below. It can be accessed here.

HR Tech vendor Beta / early release capabilities

Slackbots: SAP SuccessFactors is now testing “Slackbots.” These chatbots use their new technology partner Slack’s messaging tool within a performance review module to manage various process-related communications and tasks. HR Tech vendors like Zenefits and BambooHR, popular with smaller and medium-sized businesses, also integrate with Slack.

Sourcing bots: Crowded Inc. is a startup sourcing technology provider with a bot that asks questions of software developers applying for a job, and uses their responses to complete an application vs. making them type in the information themselves. TextRecruit is a California startup with a recruiting chatbot named Ari that organizations can use to field questions from job seekers. This allows recruiters to prioritize questions from actual candidates. Finally, Fama, founded in 2015, uses natural-language processing to scan news stories, social media and deeper web content for indications of a higher-than-acceptable risk profile in candidates.

Heavy usage bots: And multiple new chatbots from global ERP and HCM platform company Ramco Systems, and one from Boston startup Talla, are designed to respond to various, typically predictable and common employee HR questions and issues in real time. And if appropriate, the new (digital) HR staff initiates an approval or notification process. Bot-driven PTO-related interactions seem popular with both software vendors.

Right around the corner

HR admin chatbots: Extending the heavy usage bots theme, this category refers to Q&A capabilities using text messages and messaging applications (e.g., Slack), in concert with AI (e.g., natural language processing and machine learning), to manage many of the routine questions that come into HR, Payroll and Benefits departments every day. These include “I joined last week, when is my first check?”, “Our baby is due next week, how can I adjust my Benefits coverage?”, and “How do I know if a planned leave of absence is eligible for FMLA (Family Medical Leave Act) coverage?” These chatbots accept and answer questions in a flow of natural language and provide links to appropriate forms, workflows or content.

Highly personalized onboarding experiences: Given that mentors and courses don’t address much of the social side of getting acclimated, the convergence of personalization and AI will soon lead to having particular colleagues being alerted to welcome the newbie because they have a college or town of residence in common, or the same former company, or similar interests or career goals. This capability should be right around the corner given that all the relevant data is available between the corporate HRMS and tapping into pretty standard social media.

Likely a bit further out (2018/2019)

Reporting line and team member matching: HR Tech platforms can also be expected to make recommendations about who someone should report to, or which team they should join, based on analyzing where that employee tended to be most successful in the past, specifically from a behavioral, personality type or cultural compatibility perspective. Anyone who’s been in the workforce for some time knows there are certain types of bosses – and teams — that bring out the best in them, and others that do not.

Further out still? We shall see

Span of control alerts: An “HR” or organizational design issue that occasionally surfaces for C-suite residents is the span of control of their direct reports and one level below that, as it can get unwieldy at times. Compounding this, what if there was higher than average employee retention risk in the particular department where a manager’s span of control (number of direct reports) was already way above average? If the HR bot could let the senior manager or C-level executive know all this, it would be an example of the Bot leveraging two things: KPI info on desirable span of control for different roles, and as above, one of the humans on the HR staff for complementary consultative support around viable options.

Bottom line

Continuing advances and the obvious momentum building within the Digital HR (including AI in HR) arena highlight three important calls to action: (1) the need for a very symbiotic relationship between human and bot HR staff; (2) the need for crafting a vision for this relationship “asap” and (3) the need to bring together HR Tech customers, vendors and representative end-users, along with HR practitioner and corporate culture experts (and ultimately, perhaps legal advisors) to start developing best practices for this new and exciting frontier.

The time a person has the most interest and insight into an activity is when they’re doing it. Did you just finish helping someone or facilitating a meeting and wish you could quickly get feedback on what the person or attendee is thinking?

What did they like? What did they wish you did differently, more of, eliminate, change, or add? What bright ideas do they have that you just wouldn’t think of yourself? Sometimes people’s quick thoughts and reactions can be the most valuable feedback. In the moment, you are also likely to tap into the “gut reaction” and how they are feeling.

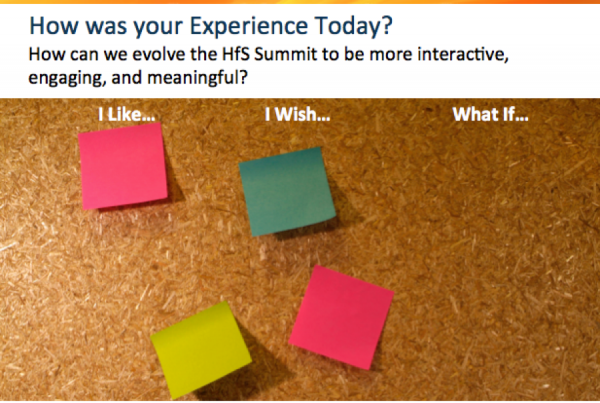

To get feedback in the moment, we’ve been using a design thinking exercise in our HfS Summits. The exercise we use is based on the simple and useful questions in the Stanford d.School toolbox (link).

Here’s how we use it: We put pens and sticky pads on all tables, plus a flip chart or whiteboard somewhere in the room. (When you start to do more design thinking you’ll realize that sticky notes and design thinking go together like water and ducks.) Then towards the end of the day we do this exercise to get feedback to confirm, challenge, and share on our objective.

Our question: How can we evolve the HfS Summit to be more interactive, engaging, and meaningful? In the next 5 minutes, write down what comes to mind to finish the following:

I liked…

I wish…

What if…

Then we encourage attendees to get up and put their sticky notes on the flip chart pad under the phrase that starts the same way. Soon, we have people up and milling around, colorful walls, and energy flowing.

Almost everyone writes something – either because they have something to say or perhaps because they feel peer pressure to perform. By asking these questions, we get specific feedback on sessions, logistics, and content – the good, the bad, and the ugly. The insights, ideas, and feedback also show us themes among what on the minds and in the interests of our attendees, and we see where there are really strong feelings.

This feedback is an addition to the formal surveys. The design thinking exercise engages attendees in a way that the formal survey doesn’t. For example, any event organizer will tell you their frustration with attendees who leave the “what else would you like to see?” or “anything else you want to tell us?” sections blank. But in the moment, when everyone is still engaged in the event, they easily share ideas and commentary.

I often get asked how to get started with Design Thinking. Although the tendency is to attach design thinking to a workshop – and there are proven benefits to taking a day or more out of your regular schedule to do this – you can also incorporate design thinking principles and activities into the way you work on a regular basis. This is one example of an activity that is so easy and simple, that you can immediately start to use it in meetings, in conversations, with sticky notes or even electronic questions in text messaging.

Bottom Line: If you want to understand someone’s experience and get feedback that you can wrap into a future interaction, meeting, activity, or event, ask: What did you like? What do you wish for? What if?