Anyone failing to escape the swirl of intense hype threatening to destroy everything great about RPA is probably thinking that these cute products are going to solve all their artificial intelligence needs and deliver them with a “digital workforce” that will go way beyond scraping screens, producing scripts and running unattended recorded process loops.

Now, don’t get me wrong – I LOVE RPA… jeez, I bloody helped create the space when I first wrote about it in 2012. I don’t want to toot my own horn, but this space probably never have would have got off the ground if we hadn’t been curious enough to get deep into it and articulate its value to the world. And no one’s paid me a billion dollars (well not yet, anyway).

RPA creates a genuine experience, where the underlying fabric of decades-old processes can finally be altered

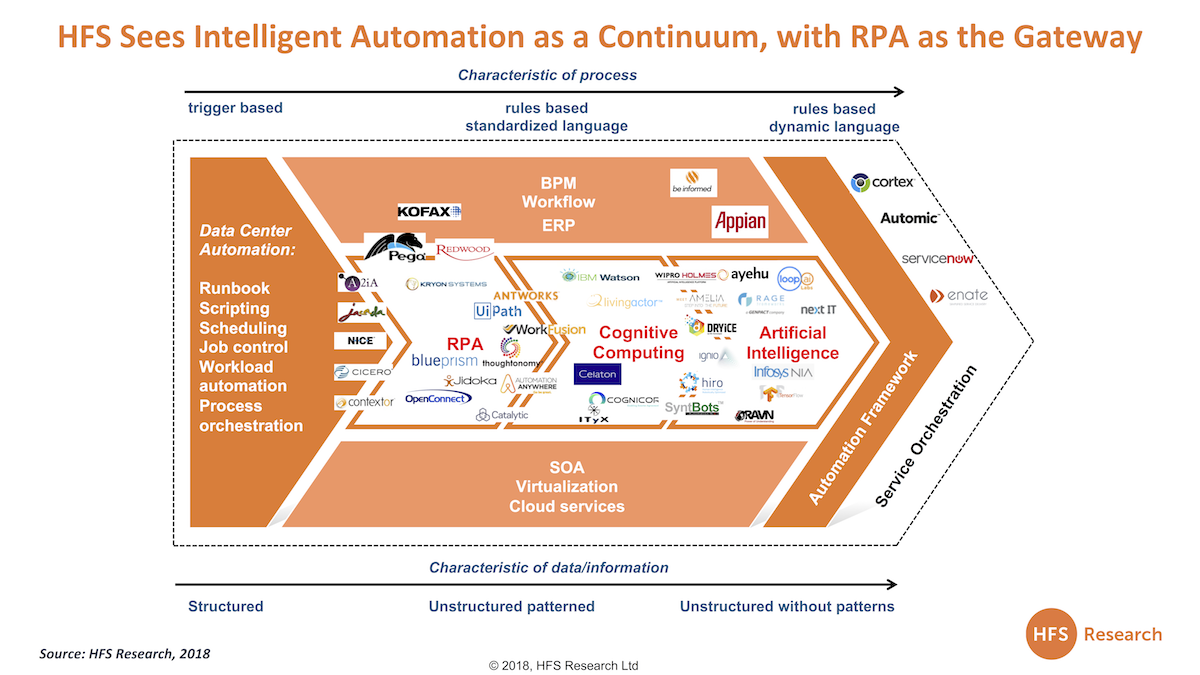

When we released the first “Intelligent Automation Continuum” in 2015, we made it very clear that RPA was clearly the first step in a much broader roadmap to achieve beautifully-automated intelligence across your enterprise. And today, this gateway philosophy has never been closer to reality. RPA, when executed well, delivers a digitally-transformative experience to business operations executives, where they can – for the first time – fundamentally change how a process is designed to process data much, much faster. Suddenly, firms have the chance to make fundamental changes to how they design workflows, instead of persisting with doing things the same old way, but with lower cost people and more efficient delivery models. Isn’t that enough for now? Why does the hype take it to a place where it’s only going to disappoint? If IBM’s leadership already thinks these firms are massively overpriced, are there really others out there which will take the plunge?

When I see executives who previously stared at excel sheets all day (while beating up BPO providers for overcharging for insurance clerks in Delhi) actually getting trained to redesign workflows using scripts and GUIs, it warms the soul. We are actually trying to do thing better... not just cheaper! So why can’t we be content with making this actually work before we get too carried away?

Time for a reality check: RPA is firmly on the radar, but let’s see it become properly industrialized and scaled before we get too carried away

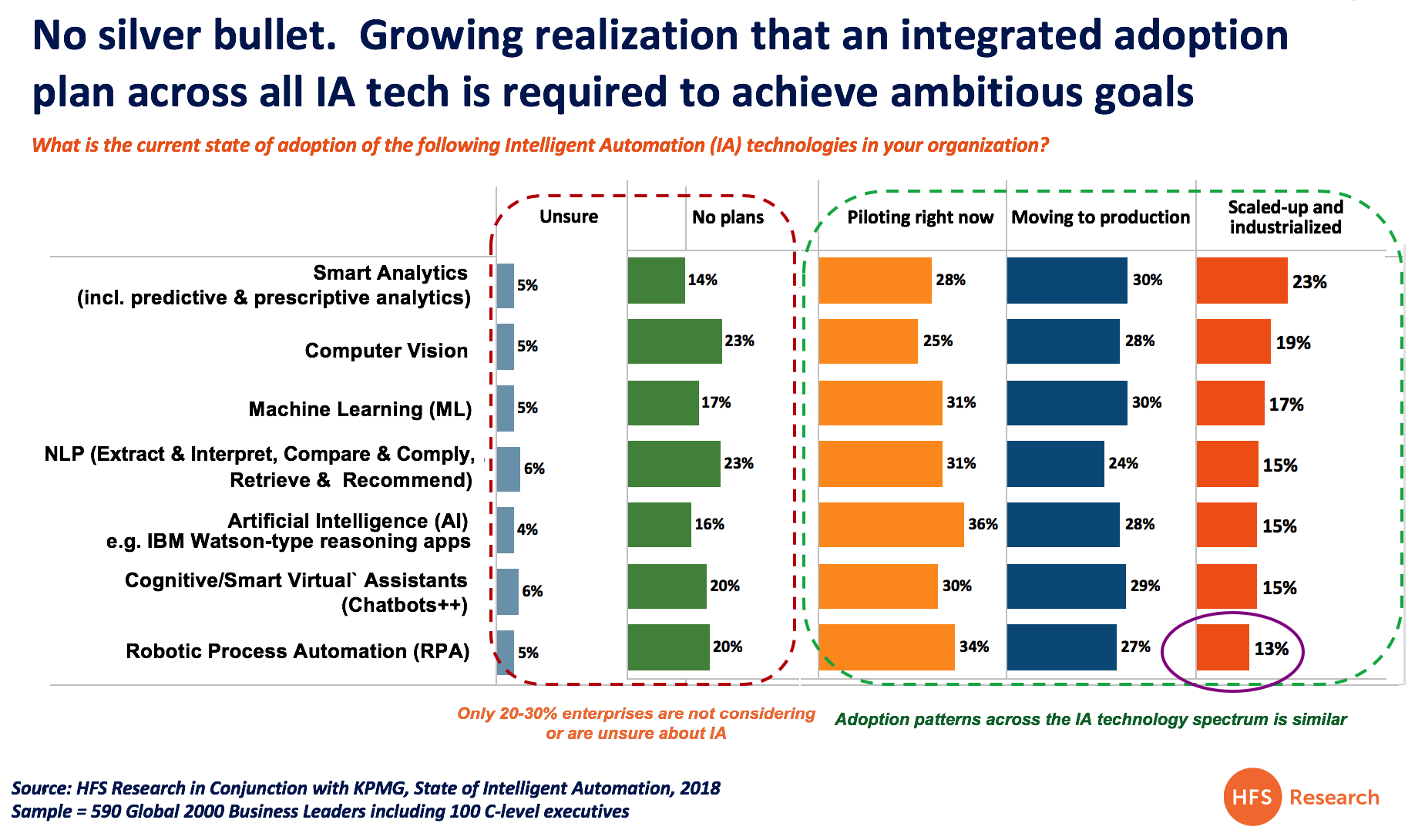

The vast majority of these initiatives are project-based, not scaled – only 13% of RPA adopters are currently scaled up and industrialized, according to new data from 590 enterprises worldwide. Most RPA adopters are still tinkering with projects and not rushing towards enterprise scale adoption:

Suddenly, the whole RPA value proposition, which has carefully matured from the “Oh my God, a robot’s going to take my job” to “OK, I get it now, RPA actually frees up time and fixes process breakages and staves off costly investments” has been injected with some serious hype-steroids, where suddenly these firms are worth billions of dollars, some are actually declaring they are going to deliver their own consulting services (really) and quickly move up the continuum to offer real cognitive and AI capabilities. I’m sorry, but when were the RPA firms going to compete with Google and Microsoft? Am I missing something here?

The Bottom-Line: Enjoy that RPA high a bit longer before you graduate onto the harder stuff…

The real data shows just how not-ready we are to declare some kind of robo-victory – executives must evaluate how all intelligent automation technologies can work together to take us to the promised land. RPA provides a terrific first stop for executives to make real underlying changes to their processes. Once processes are digitized, there is so much more we can do with the data being produced, which is where other automation and AI tech comes into play, such as Machine Learning and predictive analytics and sophisticated cognitive computing.

Now it’s always critical to focus on the “what next”, and in the case of RPA the possibilities are limitless, but only when you have mastered how to digitize your underlying mess that has plagued your organization since before the days COBOL was the next big thing. Then it’s about how you reel in the analytics and AI possibilities that truly take your business to a new level of data heaven. But let’s get past the gateway first… let’s not get ahead of reality and mess this one up, folks.

One firm that’s kept driving consistent growth above the industry average, despite the cries of “commodotization” and “cannibalization” in the business process management arena, is Genpact. This firm blitzed the offshore-centric BPO industry in the mid 2000’s, with its focus on the “virtual captive”, its obsession with process excellence (emanating from its GE roots) and the willingness of enterprise operations leaders to invest in its energetic culture.

As times evolved and other aggressive outsourcers rolled up their sleeves, Genpact has increased investments in higher-end process and operations management expertise to maintain its early tranche of enterprise customers, while focusing on the next wave. Making a concerted focus on building a Design Thinking competency out of its LEAN roots, while adding skills in AI-enabling and digitizing processes, Genpact has not been afraid to stay ahead of industry disruption. In fact, its process roots have often bolstered the firm’s credibility when driving industry narrative, as it understands the real changes enterprise need to make at the process and cultural level, if they are genuinely serious about a OneOffice Framework.

The one major constant behind these phases of change has been CEO Tiger Tyaragarajan, who’ve I’ve personally known for more than 15 years, when he was the North American market-maker for the firm, before becoming CEO in 2011. Today, Tiger talks a lot about the Instinctive Enterprise, which is very similar to our view of the OneOffice Framework, so I thought it time to reconnect before he joins us at our December FORA Summit in New York…

Phil Fersht, CEO and Chief Analyst, HFS Research: It’s great catching up again, Tiger. We’re looking at a lot of serious tinkering and experimentation with new technologies in the business process management (BPM) space. How has a company like Genpact evolved over the last 18 months, and where do you think things are going in the next couple of years?

Tiger Tyagarajan, President and CEO, Genpact: Phil, thank you for the opportunity to spend some time talking with you.

I like the word you used—evolution—and the period that you applied it to—18 months. In the world we are in, evolution is the way to think about things. I distinguish that from revolution, which is to drop everything that you’re doing and go after something new.

In our business, we think about many of our journeys as evolutions. We’ve always had depth and process; we understand how to bring the science of process to problems and how to generate value. We’ve always looked at process outcomes as important metrics to improve, and we’ve used methodologies like Lean and Six Sigma enough that we’re effective with them.

We’ve added new capabilities that didn’t exist six years, four years, and 18 months ago. Six years ago, we had nothing on digital; four years ago, we started building out our capabilities; 18 months ago we started scaling those capabilities and continue to scale them.

In the last three years, we’ve made nine acquisitions. Of the nine acquisitions, seven were in consulting and digital, and two were in deep domain areas, such as supply chain and insurance. We continue to add domain, but the ratio includes much more digital, analytics, and consulting. That piece of the puzzle is growing at 25% per annum; it’s now 20% of our business. The other 80%, which is operations and managed services and the run side of our business, is now growing at 7% or 8%. The combination is growing at 13% to 15%, outside of our GE (General Electric) business.

We never thought of customer experience in the past; we think a lot about customer experience and user experience now. That’s new language for us, and we’ve added it to our lexicon.

Phil: Market expectations are moving faster and becoming demanding more than ever, but at the same time, the pace of change within many enterprises is slow and painful. That seems to have been creating several pressure points. How is that impacting your business, though, Tiger? How do you find your traditional clients, where finance is still finance and procurement is still procurement, reacting to the pace of change? How are you viewing that whole paradigm?

Tiger: That’s a great question, and the answer has many parts. First of all, we have two kinds of clients and two kinds of engagements. We have managed services and what we call transformation services, which is digital analytics consulting. Managed service contracts are still for about five years, but in many cases, we’re entering into seven-year and ten-year contracts, which is amazing. I think that’s happening because some of those journeys are becoming high profile. Our clients are investing up front in building new technologies – these are not ERP solutions, and therefore don’t cost a billion dollars, but they do cost millions of dollars. We have to recover the costs jointly over a longer period of seven to ten years, and longer contracts work very well.

At the other end of the spectrum, we have quick consulting engagements that typically last four-to-six-weeks. These are “Hey, can you come in, and in six weeks, take a look at my consumer products business,” or, “My pharma business,” or, “My credit card business, and come back and tell me the top five areas that you would pick, to apply AI and machine learning to. Tell me how you came to that conclusion, tell me the pros and cons of your choices, the prioritisation metrics, that then allows me to choose the top two AI/machine learning opportunities that I want to go after.” That’s a four to six week engagement, it’s classic consulting engagements and, strategic assessments that clients sometimes extend, but often not longer than 12 months.

The third example includes digital, RPA, AI, machine learning, and so on. Often these engagements end up being a proof of concept (POC). No customer is going to turn over their entire operation to a machine, so they pick a subset of products, contracts, or retailers, for example, for a POC. If the POC delivers great results, the customer might gradually expand it across wider geographies. I think the most important thing here is to be flexible and not get married to one contract or commercial construct. That would be a dangerous thing to do. We have to be agile enough to construct a contract for each particular case.

Phil: So, how do you become agile enough, Tiger? In the old days, it was all cookie-cutter. You could train 10,000 people to do 10 things, 10 ways, and then multiply those capabilities across as many clients as you could. Now clients ask for so many things in so many different ways and push for more experimentation. This creates huge pressure to acquire skills. Everyone wants the A-team. It’s harder and harder to find people with algorithm capabilities, Python capabilities, and things like that. How do you win, in this market?

Tiger: There are a few things to do. One trick here is to make sharp choices, then drive the organization to buy into those choices. So, no one starts talking to a potential telecom client, for example, because we don’t do telecom. We tell our ecosystem where we operate and where we are strong, and then we stay disciplined about it. The second trick is a combination of building, partnering, and buying. I don’t think any one of those is going to be good enough alone. Historically, this industry, including Genpact, has thrived on building scale for the long term. Those days are over. If you assume that everything that you do has to be built by you, you’re going to miss staying ahead of many key developments.

The last thing is that culture becomes incredibly important. At my team level, I think about culture as a combination of three groups of people. The first group is made of people who have been in the company a long, long time. Another group includes people who have grown through the system and who don’t have that much experience, but bring new thinking because they’ve grown from doing much smaller jobs in the company. The third group includes people who have joined the company from the outside and bring very different thinking. My job is to allow those three groups to work together to create value. I think CEOs across all businesses and industries are challenged with that problem.

Phil: Do you think, Tiger, as we look at the change we’re going through, that this is becoming much more about people, purpose, and planning and less about the next shiny new gadget that’s the flavor of the month? I think we all got a bit obsessed with the gadgets, but it’s really the people, the purpose, and the planning that give us forward momentum, right?

Tiger: You nailed it, as usual, Phil. I’ll start with purpose. I think people underestimate the importance of purpose in an organization. We are approaching purpose at two levels. One is the purpose that can charge up, motivate, and create passion for 80,000 people in our company.

That purpose has to be anchored on three things. First of all, themselves. “What is the value for me?” That value proposition, for us, is all about learning. Genpact is actually a university. You continuously learn, we will provide you with the weapons, the curriculum, the opportunity to learn, but you have to self-learn and self-skill. You have to be curious, which is why curiosity is a big value driver for us. Curiosity is one of our values, and it’s one that I love a lot.

Second, you’ve got to drive business motivation, and business motivation for 80,000 people has to be around value for clients. You can’t make 80,000 people say, “I’m trying to create value for Genpact.” That’s wrong; it won’t work.

Third, you have to find a way to connect value for yourself, for clients, and what you do to a purpose in society. I think millennials want that. They want to be able to go home and say, “The work I do saves patients’ lives. The work I do makes an aircraft run more safely. The work I do allows a customer to quickly get their insurance claim after a major fire.” I think if you don’t have that, you are missing something important in today’s environment.

Phil: We’re starting to see some weird consolidation happening; some of these dinosaur-type businesses are coming together, while others are making more strategic bets – both big and small. And then we have all the insane valuations making M&A almost impossible. How do you see this unfolding? Do you think we are going to have an increase in consolidation in the next 12 months? Do you think that things are markedly different now, and we’re ready for more M&A movements with the market at a peak? Or do you think things are still going to be slow and uncertain for some time to come?

Tiger: I would say both, and they play into each other. I think uncertainty and change are givens. Does that drive consolidation? Yes. Does that drive consolidation driven by commoditization? Yes. Does that drive commoditization that drives a search for scale, because the only way you win in commoditization is scale? Yes. Is that unique to our industry? No.

I think it’s happening in every industry. One part of the journey of change and disruption is that some things are going to become commoditized in every industry. The only way to win is scale. Some people will go after that scale.

Now, there is also a reverse game. Some people are going to say, “Okay. If that’s commoditizing, I want to get out of it. I want to carve this out, and give it to the person who wants to get scale.” In the consumer goods industries, so many companies have split along a very simple dimension. This is a commoditized, high-cash generation, “I want to extract margin” business. Scale is important, and they want to run low-cost operations.

Cisco is an example of a third trend—acquiring for capability. Around 20 years ago, Cisco’s performance was amazing, and it became an acquisition machine. Every one of those acquisitions—100% of them—were capability acquisitions. Some of our much larger peers are going down that path. When we acquire seven or eight digital companies, all of them have about $5 million to $50 million in revenue. We’re continuously bringing in new capabilities and taking them back to our clients.

Phil: Things are changing—10 to 20 years ago, businesses wanted fresh new ideas on how to change business models. Now I think most enterprises understand their digital needs very well and understand where the competition is coming from. They want someone to come and translate what they need into a solution. They don’t need the next crazy new idea. If the client understands what they need now, they need somebody who can understand automation, applications, and processes. If anything, the strategy piece is dissipating into more of a “bringing it together.”

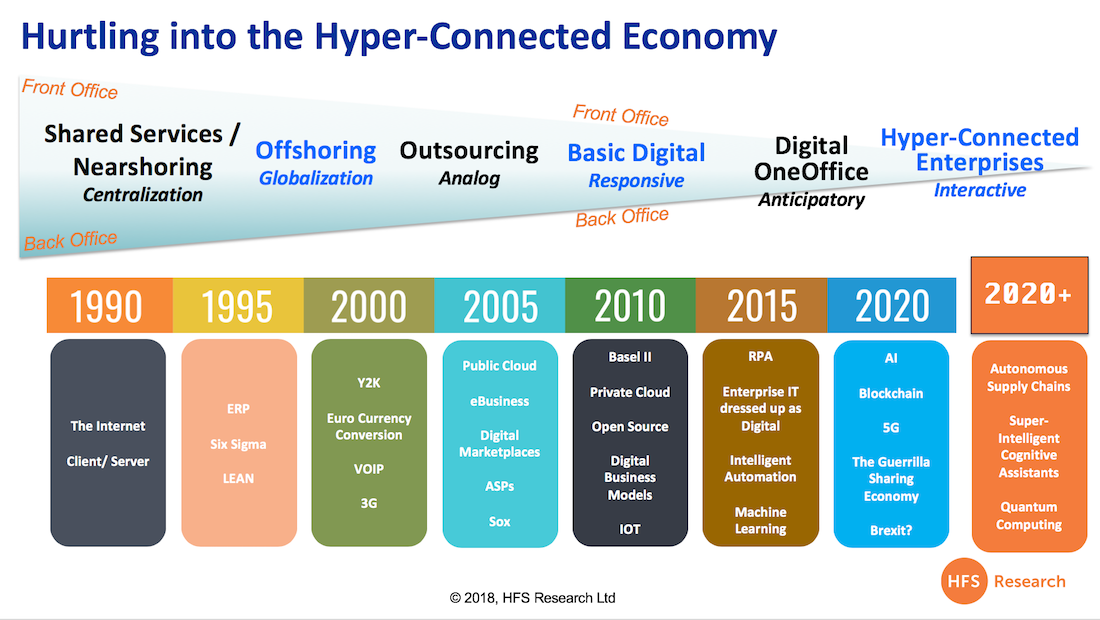

If we look at the last 30 years of industry, we can see two parts of the business that digital connectivity has transformed. First, the back office transitioned from nearshoring and shared services to outsourcing and offshoring and then to basic digital. The front office transitioned from e-commerce models and e-digital marketplaces to where we are today. But, how do you bring those two together?

It’s not just responding to needs as they happen; you have to anticipate your clients’ needs before they happen. That’s why it’s so important to understand your supply chains and those in related industries. How do you understand how to leverage intelligent cognitive assistants better? How do you know how to take in macroeconomic information, predictive market data—all these external inputs—and bring them into the company? I think where this is challenging companies now… This dramatic convergence of business, ideas, and forward thinking, and I think we need a bit more patience and pragmatism as we take things forward.

Something else I’ve seen that is dramatically different is this desire to embrace millennials and Gen Z-ers—these kids behind millennials that are about 14 to 22 years old—because they’re bringing a whole different mindset into the game. They’ve only ever lived in this digital world that we’re in today.

I heard something interesting the other day: there’s a big drop-off in Gen Z-ers learning to drive – they just use Uber and Lyft, and that’s why Uber is going crazy trying to figure out the self-driving car. What’s going to happen to the automotive industry, if the young generation doesn’t want to drive cars anymore, as they’re just too expensive to own. I think the habits of the younger generation—the big spending generation of the future—are changing dramatically, and that’s going to impact some industries beyond recognition.

Tiger: That’s a great example, Phil. My son is 25. He has been working as a consultant for three years since he graduated from college. He doesn’t have a driver’s license, and he never wanted one. He doesn’t know how to drive. Can you imagine life as a consultant in the US without knowing how to drive?

He said, “Why do I need to know? I can hail an Uber any time!” He produced an Excel spreadsheet that convinced my wife and me that it’s a wiser decision financially. He proved to us that car depreciation plus gas, insurance, and maintenance was higher than him having to use Uber everywhere he went every day. He has a bunch of friends that also don’t know how to drive and don’t have driver’s licenses.

To get us back to how the front and back offices are changing, I think the piece we are missing is the middle – it just hasn’t received as much attention. One good example is finance. On the front end, finance organizations partner with businesses to understand their problems. Then finance brings all the analytics and insights from the back office and helps businesses understand what kind of predictive analytics will be useful—then makes sure the back office creates them. The toughest jobs today in finance are the business partner finance groups.

You can find that scenario in many similar functions—where the middle isn’t strong enough.

They should run as end-to-end processes—you call it a OneOffice process, we call it an end-to-end process—and these processes must have owners. Businesses also must map customer and user journeys so that they can improve experiences. I think that’s finally playing out with digital.

Phil: Well, I think in the interest of time, Tiger, I’ll ask you just one more question. You’ve been running Genpact for many years now, and you were one of their top salesmen back in the day, I seem to remember. So, what keeps you going, and what do you think you’ll be doing in five years’ time?

Tiger: I think what keeps me going, Phil, is everything that we just talked about. It’s all so new. I often feel as though I am in the first year of my job. I’m not talking about 2011, when I took over as the CEO. I’m talking about 1999, when we first set up this business.

I’m learning new things after 20 years in the business. I look at them and think, “Wow. What a great opportunity!”

After being in the same business for 20 years—in the last 24 months, I know what R and Python is and how it works. I know how in-memory databases work now, and I didn’t know the meaning of in-memory databases two years ago. I’ve learned how you scale a cloud-based workflow platform.

Our acquisition (in Tel Aviv) of PNMsoft, which we now call SeQuence, has taught me a lot. We had to scale it from being able to manage 300,000 transactions in every instance per year to 9 billion transactions per year for a client. “I’m learning, and I’m going back, actually, to my engineering days—it’s very interesting.

At the same time, I am transforming our culture. I thought I’d done enough cultural transformation in the company over the last 20 years. I now realize I’m in one more cultural wave, and it never really stops. All of a sudden, after 20 years thinking I’ll be working with the same people, I’m dealing with a whole set of new people. So, what keeps me going? Just the fact that I can learn so much every day. I also try and keep myself fit so that I have the energy to learn and run at 100 miles per hour.

Phil: Well, that’s fantastic, Tiger. So good to hear about all the new developments at Genpact and how much you’re enjoying it! We look forward to hosting you at the HFS FORA Summit in New York this December.

It’s not been possible to escape the wild world of RPA valuations these past few months, culminating in the recent claim from UiPath and its investors that the firm is worth $3 billion, despite the reality that AA’s annual revenues this past year are ~$100m, Blue Prism’s ~$55m and UiPath’s ~$65m (HFS estimates).

As much as I would love to celebrate my friends Daniel Dines’, Mihir Shukla’s and Alastair Bathgate’s untold wealth, I have done my homework with my analyst colleague Elena Christopher and, while these three gentlemen and their teams will undoubtedly become exceedingly wealthy from locking up the RPA market, valuations as high as $3 billion are, sadly, pure science fiction. I welcome any of these three dudes to save a copy of this post and proclaim to me “I told you so” in a couple of years – and I will gladly accept a glass of their champagne – but we hate to burst this bubble with seven misnomers why RPA is not your typical Silicon Valley software fantasy:

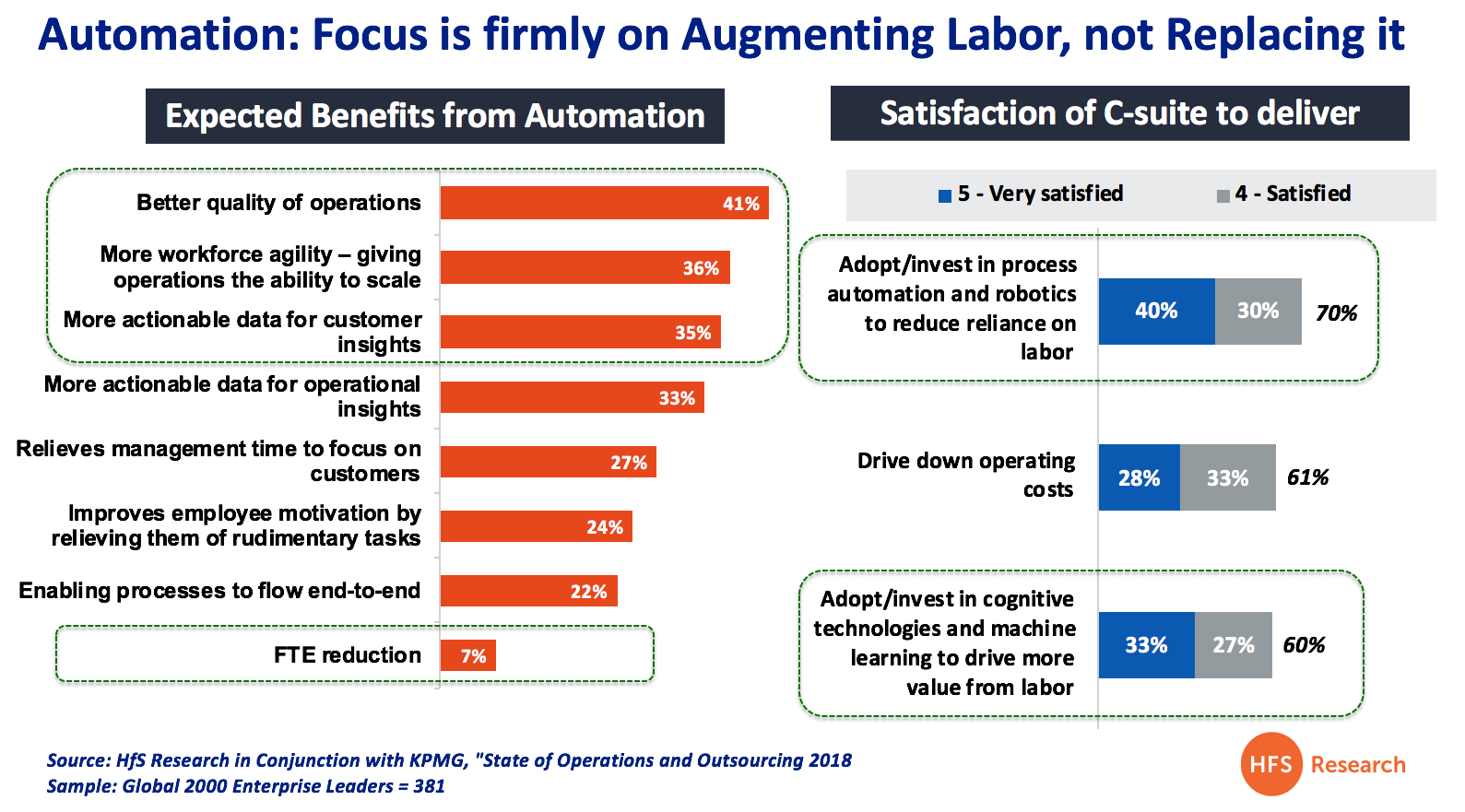

1. RPA directly replaces people.This is incorrect, its all about augmenting processes and the improving the quality of the workforce, not eliminating actual employees with bots. As our recent State of Operations Study with KPMG, across 381 Global 2000 operations leaders, illustrates, only 7% go into automation expecting direct FTE reduction. Consequently, the C-Suites from 70% of these organizations are happy with the ability of RPA to reduce reliance on labor. Hence RPA augments labor, it doesn’t replace it.

2. RPA can scale rapidly to have a dramatic impact on enterprises in months. Incorrect. The vast majority of these initiatives are project-based, not scaled – only 13% of RPA adopters are currently scaled up and industrialized, according to new data from 590 enterprises worldwide. Most RPA adopters are still tinkering with projects and not rushing towards enterprise scale adoption.

3. RPA tools can achieve amazing benefits all by their lonesome.Incorrect. RPA has to be driven by a motivated business line, and supported by capable IT.This isn’t the typical software sales model where licenses are sold en masse and distributed willy-nilly across the business.Without a genuine buy-in and partnership between business units and IT, RPA fails.There has to be a balance.

4. RPA delivers intelligence.Incorrect.RPA is a gateway drug to digitize low-value processes and free up human-time to focus on higher value activities.RPA is a catalyst to drive a more intelligent enterprise operations but is not intelligent itself.

5. RPA will be a unique game-changing product in the market for years to come.Incorrect.Most organizations take a couple of years to learn and understand how to incorporate the benefits of RPA, but after that it’s merely a tool in the enterprise toolbox.

6.We will still be talking about “Robotic Process Automation” in two years time.Very unlikely. The narrative is already shifting to a broader Intelligent Automation roadmap.RPA is very good at breathing new life into legacy processes and technologies but isn’t driving genuine digital business model transformation. RPA helps digitize the underbelly that supports the ultimate digital business outcomes by digitizing manual processes and fixes system integration points. It is a gateway to achieving front to back office workflows that are critical for digital business to service the needs of their customers in real-time. However. once RPA has performed these tasks, the real challenge for enterprises in going beyond simple RPA to drive real intelligence into the processes. Hence, RPA is a gateway to creating basic digital infrastructure across the organization, but other AI tools are needed in the future to help organizations anticipate their customer actions before they happen.

The more intelligent your business operations, the more you can stay ahead of the game, but none of this is possible if your processes are not automated effectively to create this knowledge for your business operators:

Once the digital baseline is created, enterprises need to create more intelligent bots to perform more sophisticated tasks than repetitive data and process loops. This means having unattended and attended interactions with data sources both inside and outside of the enterprise.

7.Valuations of $2/3 billion per firm are realistic.Incorrect.While software vendors such as Mulesoft and Marketo have recently fetched insane multiples of $5bn-$6bn, these are very established IT applications that augment multi-billion dollar industries.RPA tools are supporting backend automations that require a very unique combination of business/IT aligned delivery, as opposed to being front-end apps that can be sold to IT budgets en masse.RPA is a BandAid, not your new enterprise platform. These are not the typical products an SAP or Oracle can easy ingest into their apps portfolios – the needs are too process heavy, too consultant dependent to fit their sales models.

The Bottom-Line: Let’s love RPA for what is it, not what some people, who do not understand it, pretend it to be

RPA has dramatically altered the narrative among middle/back office process owners. We predict a market approaching $2 billion this year alone and growing fast as traditional process outsourcing models are hugely impacted. We’ve even gone as far as declaring RPA the “new outsourcing”. RPA has been a major game changer in the world of operations and outsourcing…. but $3 billion valuations of software firms barely hitting $50m in revenues? We don’t think so… let’s learn to keep nurturing this great business and not squeeze it until it breaks.

While the industry is busily adding fancy new words to their résumés and job titles, we have to remember that our technological journey is gradual. Change comes slowly and incrementally and you can’t just rip off the proverbial Band-Aid, hire a bunch of Millennials and Gen-Z kids… and it’s mission accomplished. As the Hyper-Connected journey illustrates, it took 30 years to get where we are today – and that’s because both front and back offices needed to go through major, secular changes to become efficient and digitized.

But the next phase is not a trade-secret – this “Future of Work” is merely a phased transformation of the present. Dumb robots evolving into intelligent assistants… ineffective supply chains plagued with manual breakpoints becoming fluid, autonomous and intelligent – with the ability to interact with other supply chains. Quantum computing and blockchain emerging to challenge the very logic of TCP/IP and computing architectures. But to get there, we need to be experimenting, tinkering, exploring and disrupting with the kit that available today to get our organizations in a place where all these far-flung innovations can have some real possibilities.

So let’s have less talk about the future of work and focus on the present… we know where we are and what we need to do. So let’s do it!

it’s easy to overlook our digital underbelly during these times of AI hype and “let’s make a few billion based purely on investor hype” fantasies. But who’s providing the tools and grunt to make all this possible? HFS analyst Ollie O’Donoghue has pooled our study data from the Global 2000, conducted countless enterprise interviews and driven the providers potty to deliver the perfect poignant viewpoint of this industry:

Ollie, what are the major trends in the infrastructure market?

Over the last few years, the infrastructure market has taken a bit of a battering with the kings of hyperscale eroding market share, and enterprises looking for more exciting things to spend their money on than traditional “lift and shift” engagements. However, that’s all changing, and the market is evolving. The big providers are partnering up with the hyperscale cloud players and making them a valuable tool in their toolbox. Moreover, “digital” has fueled enterprises’ appetite for technology. Which means getting their infrastructure and digital foundations in order. After all, these overhyped technologies like AI and blockchain have to run off something!

The challenge for us as analysts covering the space is rethinking how we assess and evaluate providers. In essence, partnerships have become a much more critical part of this market – if a firm isn’t befriending the big cloud leviathans, then they’re likely to struggle to build offerings that resonate with evolving enterprise appetite. The challenge is that as all providers follow this path, there’s a degree of equilibrium, so the assessment needs to evolve further and evaluate how these providers are leveraging partnerships, and building value-add offerings. We also need to scrutinize how providers are developing automation capabilities to design and build more resilient, scalable and cost-effective infrastructure solutions for clients. So while this is a mature market, it’s one that’s changing all the time – and one that certainly keeps us, analysts, busy.

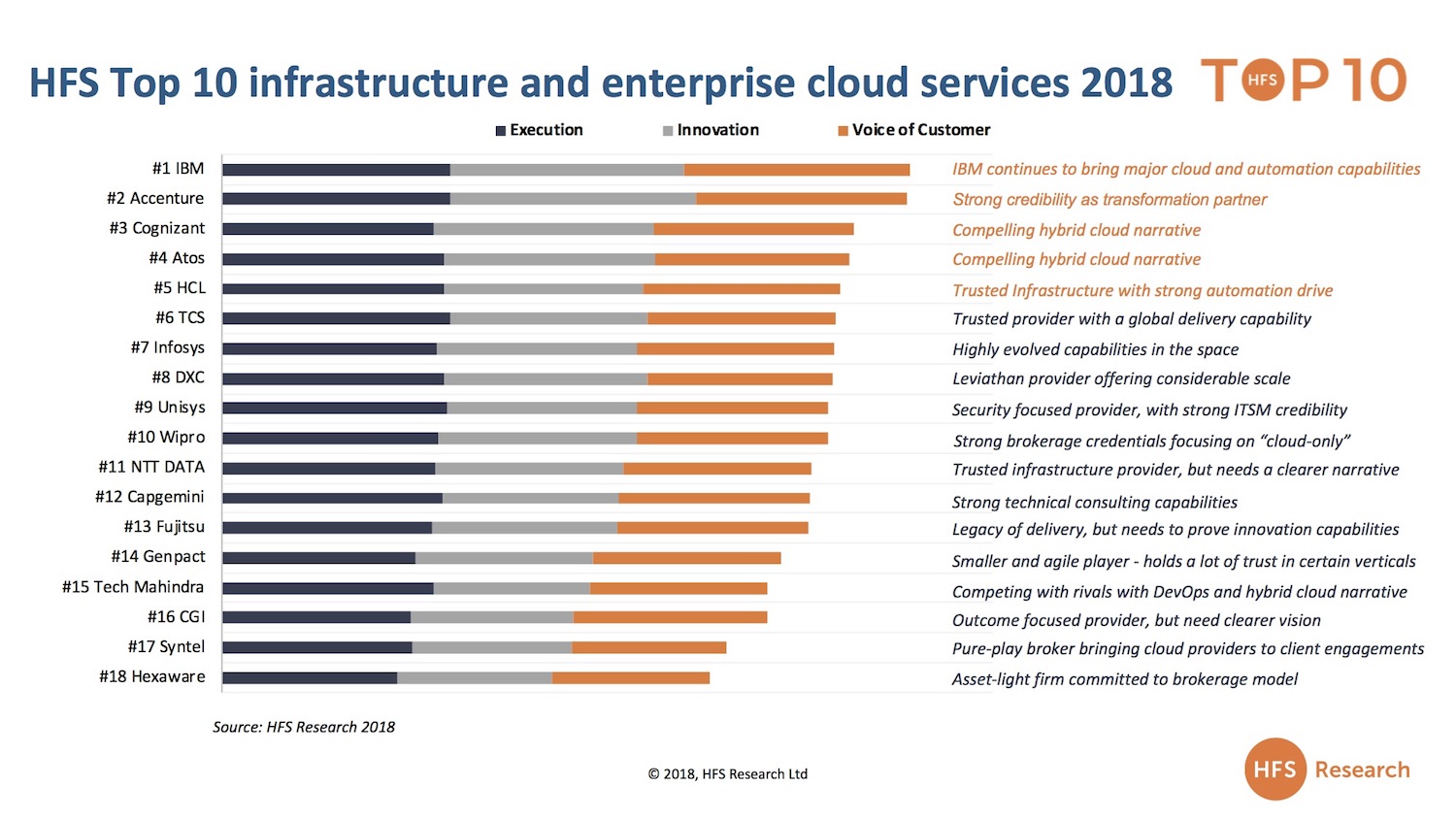

So who’s winning this infrastructure and cloud war?

IBM’s still the undisputed champion of the infrastructure and cloud market – Big Blue brings with it unrivalled enterprise trust, and is the only IT Services major that truly has the cloud capability and resources to fight alongside the hyperscale leviathans AWS, Google, and Microsoft. It also has true scale and ability to manage the largest most complex engagements in this space. That being said, Accenture has an uncompromised reputation for delivering quality and bringing best in class capabilities to engagements. From an enterprise perspective, the fact that this comes at a premium count against the firm to some extent. And while Accenture executives assure us they’re building commercial models to make pricing more attractive, the reputation for being expensive is relatively well set in, and any changes might be like trying to get toothpaste back into the tube. Although let’s be honest, there are worse problems to have than being known for delivering quality at a price.

And the main movers and shakers in the Top 5?

A couple of firms are worth mentioning – Atos performed well because of a concerted effort from the firm to broaden and deepen partnerships with major cloud players. It’s now shaken hands with all of the big hyperscale players and is doing some exciting work around analytics with Google. Atos has also pulled some fresh thinking out of the bag and built a compelling vision for hybrid cloud. HCL has excelled at large scale transformation, is also doing interesting work in the space and comes with strong client references – the consensus is, HCL will keep working to get the job done, bringing in automation capabilities to get the most out of assets. And then we have Cognizant, another firm that is striving to deliver innovation through all its infrastructure services is producing offerings that focus on specific client’s needs. Ensuring business value is delivered, whilst pushing hard down the hybrid cloud path – in recognition that the future of cloud will be leveraging multiple providers to deliver the best results.

So what about the Top 10 overall, any surprises there, Ollie?

The big heavy lifters hold a competitive position, TCS brings a lot to the party and has an enviable track-record of delivery in some industries and loyal clients that leverage the firms considerable global delivery network. Similarly, Infosys is positioned competitively, reflecting the investment the firm is making in building out nearshore delivery centers and redeveloping talent into higher value areas of work. However, the firm does struggle to get its message out there which is holding it back a tad. And then we have DXC – the leviathan firm can bring considerable brains and brawn to engagements, but its path is still unclear to some clients and all eyes are on its financial reports looking for stability at a time when providers sinking can drag clients down with it. Unisys relies on its strong legacy in the Infrastructure space – and innate trust from some industries, particularly financial services. Supplemented by respectable security credentials and offerings. Finally, Wipro is driving a competitive approach to writing off legacy through a cloud-only approach, a strategy which could see the firm drive further up the top 10 list in the future.

So what does the future look like for the market?

We’ve been charting the major trends impacting the infrastructure space for some time now and it’s a quickly moving market. Partnerships are no longer a nice-to-have, they are mandatory if providers are going to have a chance of survival. Finally, the big providers are warming to the potential value they can leverage from the cloud giants, rather than shaking hands through gritted teeth as their revenues eroded. This is an important step as the market matures. But the biggest shift is the rosier tint the market now has after years of revenue freefall. Shifts to cloud and as-a-service hammered traditional revenues – which often made up a sizeable chunk of vendor revenues. But with some compute-heavy applications and technologies on the cards, spending on infrastructure is very much back in vogue. The smart enterprises are investing in their digital underbelly now, in preparation for their future digital needs.

Bottom line: Our partners who got us here may not be the ones to take us where we’re going – the future’s all about smart partnering as the need for savvy IT talent reaches critical levels

If we take a look at revenue projections for the market, it’s not the good news providers are looking for. With As-a-Service and cloud continuing to batter traditional revenues, the market is unlikely to grow from a revenue perspective. But it’s not going to shrink either – we see this market is bouncing back in other ways as enterprises urgently seek help digitizing their operations and scaling their digital businesses: technology is at the heard of C-Suite strategy these days, and partnerships which provide scarce talent to keep these increasingly data-driven environments agile, scalable and secure are critical for enterprises.

Reputationally, IT infrastructure has always had a hard time – security breaches, server crashes, and integration challenges. But all of that’s changing now as automation drives service quality up, and costs down. And partnerships are supporting providers in offering clients best-in-class cloud capabilities at a time when the contents of their digital shopping list needs to be running on the best.

There is a massive opportunity to lead in the world of IT services, provided you can plug these skills gaps. The challenge is breaking out of the traditional sourcing model to access niche talent across the globe in areas such as crypto-technology, Python development, Lisp, Prolog, Go and C++. While most traditional firms still rely heavily on bread and butter IT services delivered at scale from regions such as India, the emergence of talent in Central and Eastern Europe, China and parts of South America also need to be brought into play. The IT services world will be a very different place in a couple of years as boutique firms offering niche skills come into the fore. Not to mention the emergence of crowdsourcing for IT talent. Having really savvy IT leaders who can cobble together crack teams on-tap to solve their IT headaches is already becoming a huge differentiator for many firms. The will also be a role for the super services integrator, who can pull together teams for clients to work with them on complex projects.

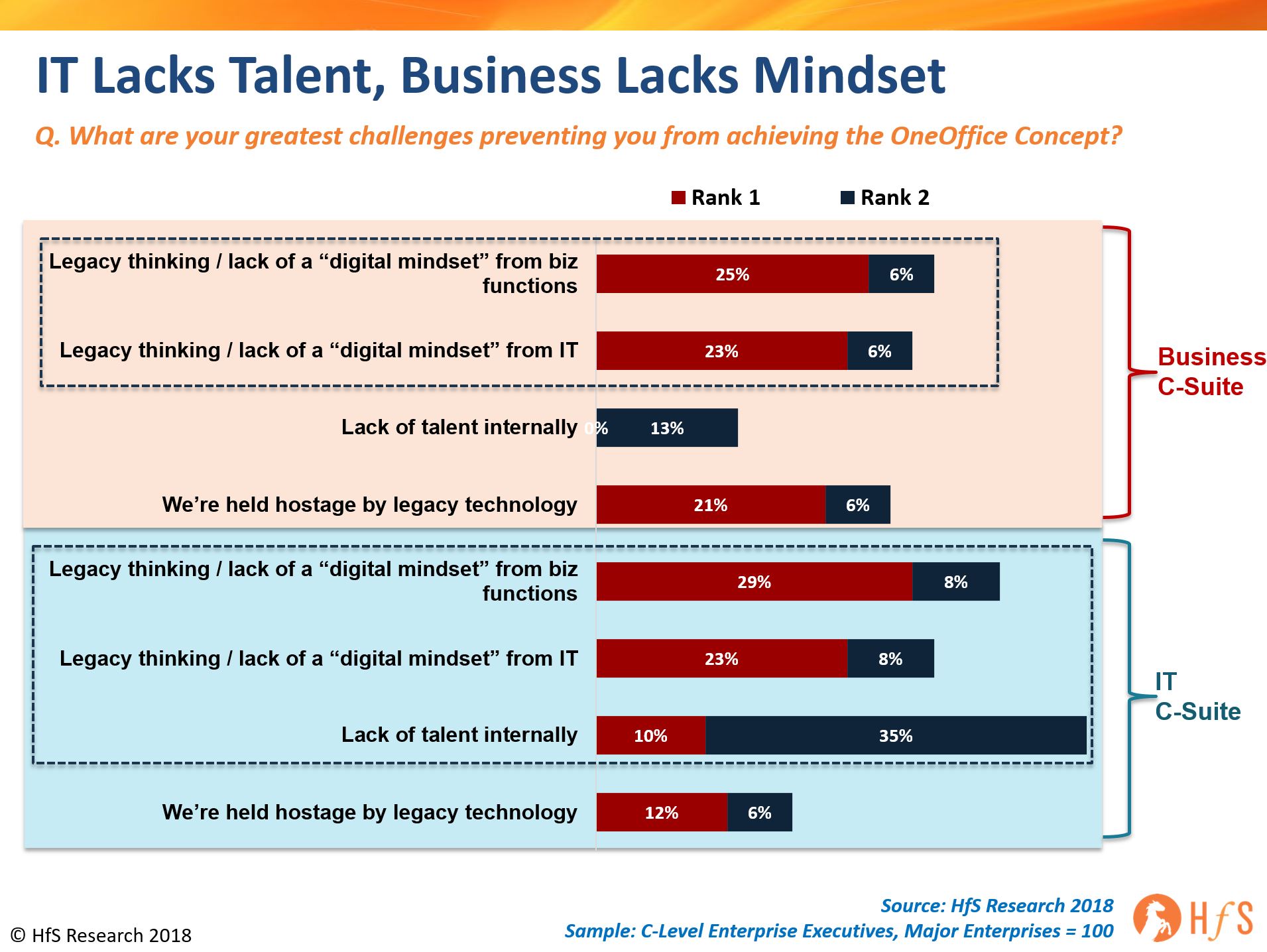

To this end, we recently presented the Digital OneOffice Concept to 100 C-Suite executives to understand what is holding back both business and IT leaders from reaching the promised land of perfect real-time symmetry of their business operations staying ahead of their customers’ needs. While the business leaders grapple with changing their mindsets, the IT leaders were quick to call out their skills deficiencies to enable their businesses to achieve a digital OneOffice.

Hence, those providers which can pull together the resources and talent can still profit from this disruptive market – the digital engine can only purr when it’s aligned with all the core components of the business, right from the front to back office. Today’s market is all about taking bigger bets on bigger risks… and only the smartest and boldest will make it.

The rise of RPA is nothing short of spectacular as the market closes in on $2bn this year. It has captivated the attention of the digital operations executives with the promise of cost-savings beyond labor arbitrage, cost avoidance by extending the life of legacy IT, quicker implementation than traditional IT projects, business-user friendliness, auditability and compliance, straight through processing, and let’s be honest – terrific marketing!

However, confusion around RPA deployments is also rife. There are growing questions whether RPA can deliver on the promised ROI and outcomes. Most RPA initiatives continue to be small and piecemeal. Truly scaled RPA deployments are rare. The industry is still struggling to solve challenges around the process, change, talent, training, infrastructure, security, and governance.

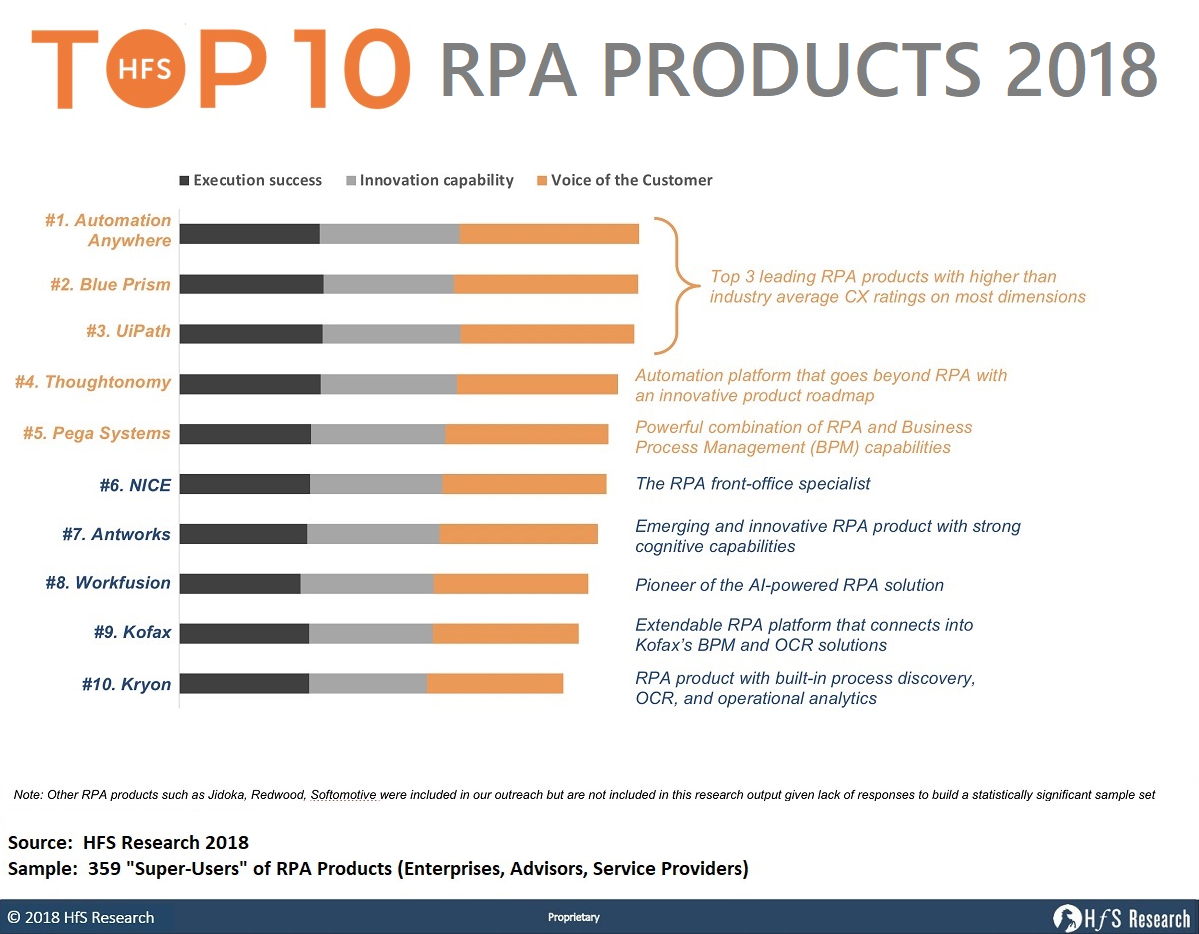

With the mission to demystify this confusion and uncover the truth to successful RPA deployment, we conducted a first of its kind RPA CX research to develop the list of “HFS Top 10 RPA Products” (See Exhibit 1). The research is based on interviews over 350 clients and product partners across the ten leading RPA products across:

Ability to execute based on product functionality (Ease of integration with legacy IT, Unassisted automation functionality, OCR functionality, Scheduling functionality, Development tools, Exception handling, Required set-up coding, Ease of product configuration); integration and support (Service extensions and connectors, Documentation, Certification program, Training and customer support, Experience in serving multiple geographies, Adoption across multiple industries, Required IT skill-sets), and security and governance (Uptime and SLA commitments, Version control and upgrade management, Centralized controls, Regulatory compliance, Enterprise security, Disaster Recovery (DR) and Business Continuity Planning (BCP))

Innovation capability based on flexibility and scalability (Accommodating process / environment changes, Licensing model flexibility, Ability to handle multiple processes, Workflow templates and library of processes, Handling multiple inputs) and embedding intelligence (Processing structured, semi-structured, and unstructured data, Operational Analytics, Dashboards, and Artificial Intelligence (AI) capabilities)

Voice of the customer based on the RPA products ability to drive business outcomes (Realizing cost savings, Speed-to-market, Overall satisfaction, and Client reference ability)

Key highlights from the HFS Top 10 RPA Provider assessment

Overall RPA Client Experience has been ‘Good.’ The aggregated average CX scores across all assessment dimensions is three on a scale of 4 implying a good overall experience. For most clients, RPA has created value in addition to reducing costs (just not as much and as fast as they heard in the first sales pitch!). For almost all the RPA products assessed, security, controls, accuracy, integration, and out-of-the-box functionality performs as promised. Basically, RPA works!

Getting RPA “production ready” is not as easy as promised. The client experience with the amount of coding/configuration required is rated amongst the lowest. Management of version control and upgrades as well the training and support offered by RPA providers was also sub-par. The primary reason behind this is a classic expectation mismatch – the RPA providers oversold and overpromised, raising the client expectations beyond normal, that then resulted in less than required client investments towards process and change management. The disappointment associated with RPA is not about the technology itself.

RPA is not very smart (at least as of today). The dimension around embedding intelligence in RPA was rated amongst the lowest by clients. There is considerable confidence in RPA’s ability to process structured data but drops down significantly when asked about unstructured or even semi-structured data. Clients are not convinced about the Artificial Intelligence (AI) capabilities of their RPA products. The good news is that most RPA providers recognize this and are investing in building out capabilities especially around Machine Learning (ML). At HfS, we believe that the holy grail of service delivery will be at the intersection of the Triple-A Trifecta – Automation, AI, and Analytics

Bottomline. RPA works but is not a magic wand. Best practices are emerging

Based on our in-depth conversations with the RPA clients, we developed a set of best practices that you need to keep in mind when implementing any of the RPA products:

RPA is not a silver bullet. Keep expectations realistic

RPA cannot automate everything. Choose the use-case wisely

RPA success is not about technology. Treat it as a change agent

Automated processes are still processes. Invest in documentation, especially as for complex automations

RPA vendors are product companies. Do not expect them to behave like service providers

Do not side-step your IT folks. RPA success requires IT-business collaboration

RPA products are still nascent. Do not short-change security and testing

RPA is not a one-time exercise. Change management and ongoing governance and the keys to continued success

RPA is not the holy grail. Business outcomes driven by integrated solutions are

RPA does not solve your data issues. Data-centric mindset is the key

RPA offers more than cost savings. Think beyond cost-reduction and figure out how to measure success

We’ve been talking about the legacy model of butts-on-seats “mess for less” outsourcing fizzling out for years, but somehow the same old candidates have clung on grimly to the same old model, relying on clients that still find a modicum of comfort negotiating rate cards down to the lowest common denominator, content to hobble along with average service delivery that just about keeps everyone paid… and somehow relevant.

As we’ve bemoaned the decreasing growth rates across almost all traditional areas of business and IT services, no one’s pressed the panic button to do anything wildly different. In fact, many have used the recent stagnant times to merge with each other to eke out a bit more revenue growth and rationalize costs wherever possible.

Meanwhile, all the providers have slapped the lovely “digital” tag on pretty much ever new client dollar that wasn’t obviously a help desk deal or some server consolidation. Yes, people, even good old app testing today has managed to be magically reformulated as a “digital” service by some.

The balance of power sits firmly with the enterprise clients, and many have no choice but to jump ship from the old model

Being realistic, the IT and business services business is no different than it was five years ago, except there is a lot more cloud… and a lot more window dressing. But that is all changing, and our new research reveals a new services economy is upon us.

But, finally, many enterprise clients are wising up to the reality they now wield a lot more power over service providers as the market flattens to a state of hyper-commoditization and negligible-to-pathetic growth. Many are, finally, awakening to a new dawn that service providers can (and most are) able to takeout delivery cost through better deployment of cloud, less costly SaaS apps, and applying robotic process automation to reduce manual workarounds and augment people delivery.

Simply put, if your long-time service provider is failing to deliver you any of these benefits to your business, or at least is making some strides to incorporate pricing that is tied to successful service execution and not only people effort, then it’s time to cut bait before you get fired yourself for perpetuating a legacy model that is depriving your firm from finding new thresholds of value your smarter competitors are already enjoying.

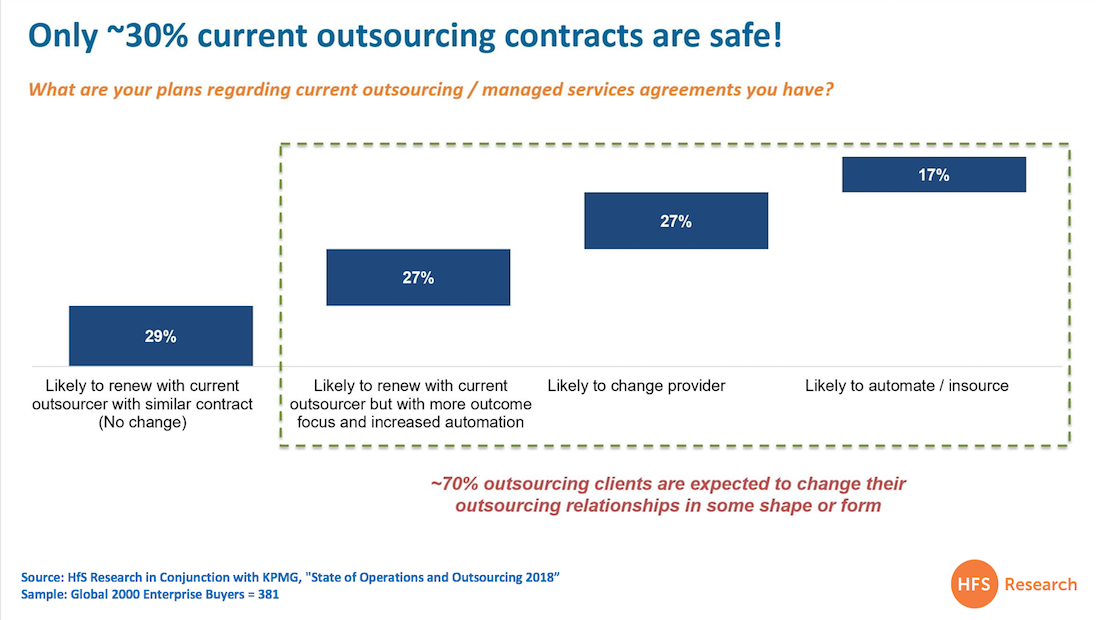

As this year’s State of Operations and Outsourcing study of 381 enterprise operations leaders across the Global 2000 reveals, only 30% of these relationships will continue to operate in the old model, while a similar number will stick with their service provider if they can have a shift towards business outcome pricing and a degree of automation applied. 27% have already given up on shifting the model with their current provider and have declared their attention to switch, while 17% want to end the misery and focus on bringing the work back inhouse, and look to simply automate it:

The Bottom-line: Outsourcing is finally entering the uncomfortable phase of change that’s threatened for several years, and it’s going to get ugly.

Judgement day is now upon the industry once known as outsourcing and this one will get pretty ugly before it eventually finds a new groove, where enterprises and service providers find real value in each other again.

History has told us time and time again that nothing in this business changes until deals are lost and the C-Suite is forced to address why this is really happening… and actually act on it. This is the fine balance in which we find ourselves today, where actions will change dramatically when 2% growth spirals into a 5-10% decline because that is what will happen to many service providers if they truly cannot pivot to deliver value beyond cheap labor.

Those providers which have the capability to make the necessary investments and adjustments will take a few hits, but rebuild for a new phase… those which think they can keep papering over the cracks, repeating to same old spin, but never fundamentally changing how they invest in solutions, talent and their clients, will quickly start moving backward (and fast) in the new services market that’s emerging.

The word “Chatbot” is officially banned: they treat conversations like they’re a game of tennis: talk, reply, talk, reply. There is little to no context and zero intelligence, just pre-programmed responses only set up to deal with a pre-set finite number of frequently asked questions. It’s a legacy customer experience that most of us go out of our way to avoid. To be blunt, it’s easier to be redirected to an FAQ page, or even some online Q&A forum than try and engage in a dumb one-dimensional conversation. I’ve had more intelligent conversations down my local pub after a 3.00am “lock-in”… So let’s shift the entire conversation towards chatbots with some form of intelligence…cognitive assistants.

HFS Research sees cognitive assistants as the combination of conversational interaction and process execution capabilities; they combine characteristics of smart analytics and artificial intelligence. These services can include front-office facing elements (e.g., conversations with end customers) and internal employee use cases (e.g., help desk, HR onboarding, assisting contact center agents).These cognitive assistants can self-learn, self-remediate, and execute business processes. They can also often understand structured and unstructured data and then use natural language processing to learn, comprehend, and recommend next steps. Advanced cognitive assistants can also enable predictive decision making using real-time analytics. This distinction is significant as many people use the terms “cognitive agents” and “chatbots” synonymously. While cognitive agents are a less mature capability, interest and adoption are growing rapidly—and their impacts are far greater than traditional automated tools.

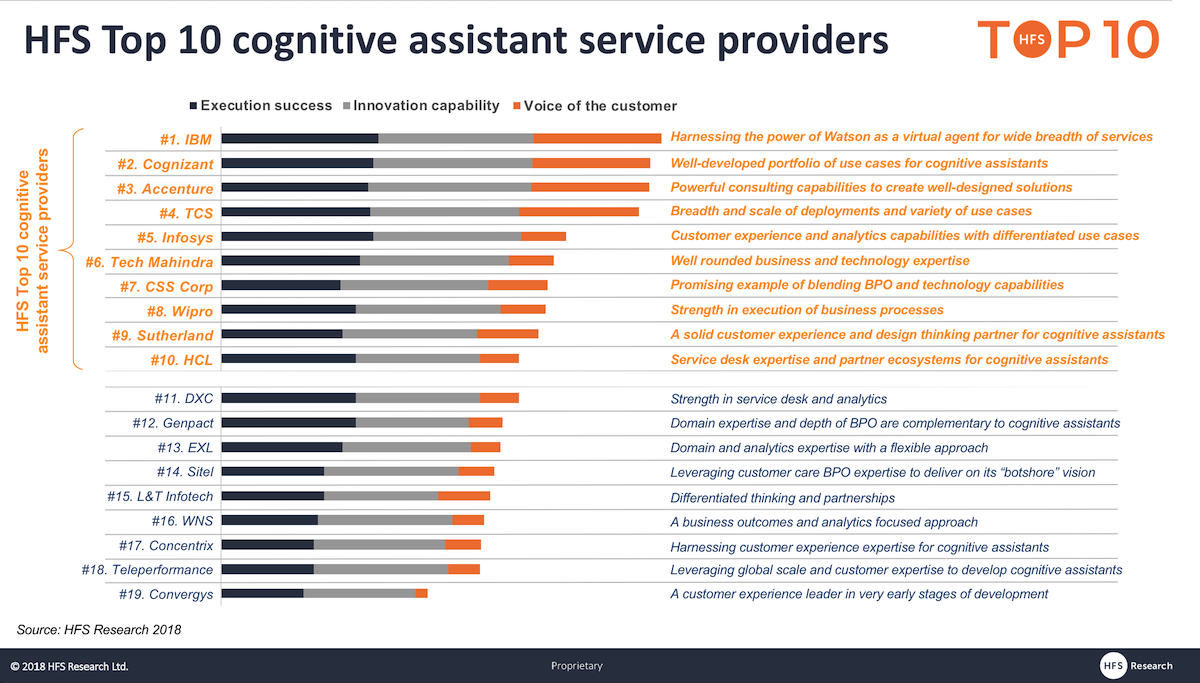

So who’s delivering these services most effectively today? Well, who better to consult that HFS customer experience connoisseur Melissa O’Brien, who’s just launched the industry’s first deep-dive report on the services market for these cognitive assistants:

We based this research on interviews with 300 enterprise clients of IT and business services from the Global 2000 in which we asked specific questions about innovation and execution performance of service providers assessed. We augmented the research with information collected in Q1 and Q2 2018 through provider RFIs, structured briefings, client reference interviews, and from publicly available information sources.

Melissa: Which service providers are the early front-runners?

The most notable players in this study demonstrated the most sophisticated and well-developed cognitive assistants. These providers’ services had solid examples of use cases with capabilities above and beyond the traditional rules-based chatbots and IVR style communications. These intelligent bots have the capability to learn, handle unstructured data, solve business problems and use natural language processing to analyze sentiment and understand context, and are deployed across the enterprise in a variety of ways.

IBM, which topped the list of providers demonstrated the greatest volume and depth of cognitive assistant use cases across industry verticals and enterprise processes, and has the power of Watson as a brand and a tool to leverage for these services. Cognizant, the runner up, also has a wide variety of deployments and some unique examples outside of traditional channels, like its cognitive assistant in a kiosk of a quick serve restaurant. Accenture had some very strong virtualized deployments and the most sophisticated consulting and design capabilities for cognitive assistants.

Which other providers are also showing potential?

One service provider with a unique focus is CSS Corp, which has doubled down on its “Yodaa” cognitive assistant capability. While it risks getting pigeonholed by going to market with the one persona, its actual use cases are broad and the sales and marketing outcomes achieved in particular have been significant. TCS demonstrated broad applicability for its cognitive assistants services, with significant depth and scale of deployments and compelling and differentiated use cases in particular for travel and the NYC Marathon (check out “Pacey Miles”. Many of the service providers, including TCS, Accenture, Infosys, Tech Mahindra, Concentrix, Sutherland, and Convergys, have developed cognitive assistants for their internal processes—using them within their own HR and IT processes or to assist their customer service agents — which is demonstrative of their faith in the solutions they’ve developed. Wipro, DXC and HCL have each demonstrated strength in deploying cognitive assistants within clients’ IT service desk environments— automating ticketing and issue resolution in a more intelligent way.

Is the focus of cognitive assistants is more about augmentation of employee work rather than replacing them?

Automation tools can often replace a human interaction—we see this a lot in self-service, especially in the case of straightforward, focused inquiries. Tools can typically free the employee to do something less transactional, more valuable to the customer, and more “human.” However, with cognitive assistants, the capabilities are more powerful and therefore more nuanced. Generally, the use cases we’ve seen are about making employees, whether contact center representatives, IT service desk staff, or human resources officers more efficient and effective; often that means that the bot is working side-by-side with the employee as an assistant, synthesizing and presenting data, aimed at making their lives easier and processes more intelligent and agile.

Which processes are more commonly being used for cognitive assistant deployment?

Front-office deployments are common, but their AI implementations are not as mature as examples often found in HR, finance and accounting, and help desks. The majority of case studies we saw in this research involved the front office, particularly in sales and customer service. These are often the starting points or the low hanging fruits where enterprises will decide to test the use of cognitive assistants. But the capabilities for cognitive assistants go well beyond the front office, assisting in various elements of the enterprise such as HR, finance and accounting, and the help desk. While the front-office examples are ubiquitous, more mature use cases are often found in other areas where cognitive assistants can execute on processes such as ordering equipment for an employee during onboarding or creating and resolving a help desk ticket autonomously.

Will this all boil down to smart partnering, or a best-of-breed approach?

Partnerships are essential building blocks for cognitive assistants. Many of the service providers in this study cited a “unique” approach with “best-in-breed” technology providers. The reality is that the technology is advancing so rapidly that there’s really no such thing as best-in-breed, and having a partner ecosystem is hardly unique. Those leading in this market will develop strong relationships with well-known players (e.g., IBM Watson, IPsoft’s Amelia, Nuance for NLP), which is essential to have a flexible client-friendly environment—but will keep a keen eye on up-and-comers. Integration with other systems (e.g., ServiceNow for ticketing, HCM platforms for recruitment and onboarding, or CRM systems for customer data) is also important. Almost all of the service providers we spoke to have a technology-agnostic platform (perhaps with the exception of IBM, which partners but leverages the Watson platform heavily), which enables them to leverage their clients’ existing investments and be flexible to clients’ needs and modular with building the tools.

If this market is so focused on the front office, Melissa, why aren’t the contact center providers leading the pack?

Pure-play contact center BPO companies are less mature but have tremendous potential to move up the value chain. The contact center BPO companies (Convergys, Sitel, and Teleperformance) we profiled had less mature capabilities and fewer actual client case studies; two reasons are that contact center BPO companies are finding that it is difficult to fit cognitive assistants into their bread-and-butter business and that automating customer interactions brings with it revenue cannibalization. However, for front office use cases there is a tremendous opportunity for these players to take the lead given their wealth of customer data and customer experience expertise. By embracing cognitive assistants, these service providers have the opportunity to carve out a differentiated capability for a blended bot and human model, providing seamless transitions to human agents and harnessing the power of their core capability—while potentially breaking out of the legacy FTE models that have dampened innovation and profitability for years. Two ripe areas for further developing cognitive assistants for contact center companies are in use cases that employ bots internally for recruiting and hiring and those that augment agents. Companies that use these tools internally to their best advantage will create differentiation in their service delivery.

The Bottom-Line: The disruptive potential of cognitive assistants is only just unravelling for service providers and enterprises

Today, the cognitive discussion is about augmenting peoples’ performances. Being able to engage in a semi-intelligent manner with a bot has huge ramifications for everyone in the business environment: for consumers who want to engage digitally, for employees who can spend less time having routine interactions, for supply chain staff who can move products and services around at digital speed, and so on. The common nuance here is that all these entities are being assisted – they aren’t being replaced.

Tomorrow’s discussion is about scaling businesses with less reliance on people addition, and these cognitive assistants will be a significant factor. However, the evolution of technology isn’t finite, and while these social tech tools today add value and efficiency and add to the customer engagement experience, the more these tools can be refined to self-learn and self-remediate, the more judgement-based human tasks they will be able to support. Ultimately, this means both service providers and enterprises will not need to keep adding so many new staff in the future to deal with larger business volumes. Cognitive technologies, when smartly managed, will allow business to scale without the linear addition of staff to deliver scale. This creates a huge opportunity for service providers to compete, as those which can provide volume services and lower rates, based on their acumen to deploy cognitive assistants to support their clients. Of course, enterprises will have the choice of deploying cognitive assistance themselves inhouse, or whether to engage with external service partners which can deliver high volume/ low-cost cognitive services for them. Much depends on the skills needed to develop ongoing algorithms based on an intimate understanding of the business and its institutional processes. This has much more far-reaching potential than merely deploying an RPA bot to crank some basic process loops… This means having unattended and attended interactions with people, processes and data sources both inside and outside of the enterprise, such as macroeconomic data, compliance issues, competitive intel, geopolitcal issues, supply chain issues etc.

Net-net, the more intelligent we become at deploying these cognitive assistant tools, the more we will focus on technology-driven solutions that reduce the numbers of butts-on-seats needed to support the business. Those service providers which fail to deploy cognitive assistants to scale their services competitively will fall away, and for those which have not yet developed this emerging capability, it may already be too late. I doubt we’ll even call these solutions “cognitive assistants” in a couple more years… they’ll simply become part of the fabric of operations, and how we engage and interact digitally to get things done. Rather like offshoring became so normalized we stopped defining and noticing it, the same will happen with many of these emerging technology solutions as they become part of how we conduct business.

When you do something to change the status quo, you usually expect those who love the status quo to resist. So why on earth would Accenture’s global leader for analyst relations, Allen Valahu, laud the emergence of the HFS TOP 10, when his firm is already hitting top right corners of all the analyst quadrants on a (seemingly) daily basis? Well, Allen publicly submitted to us his viewpoint:

“Good news. I believe the TOP 10 will allow us to have more regular and meaningful interactions with your team throughout the year. It will put less pressure on our clients as they will have more lead time to talk to the analysts. Finally, the ability to update HFS through timely structured briefings, demos, and reference customers as the opportunities arise throughout the year, is a much more targeted and strategic approach. Look forward to interacting with HFS in a more strategic way going forward.”

In short, Allen is seeing the HFS TOP 10 as not only presenting the voice of the customer in a more meaningful way to customers, but it also enables analysts and vendor executives to engage in a less stressful – and political – manner. Where quadrants force a “lobbying” situation, where the outcomes of the matrix dots are entirely dependent on the analyst getting served up their vendor references within tight deadlines, dictated by the analyst firm, the TOP TEN frees up all parties from these stressful processes and interactions, as the analyst firm isn’t 100% reliant on those vendor reference calls. This also refocuses the analyst/vendor relationship more around valuable conversation and strategy, and less around the “he said, she said” tactical bake-off, which the legacy quadrant model forces.

Bottom-line: Goodbye quadrants… it was nice while it lasted, but the industry has moved on

I have been overwhelmed with messages of relief and encouragement from many people right across the industry who are delighted to see a change to a practice that is tainted, tired and viewed negative by all and sundry. Only one vendor executive voiced objections, based more on the fact that their job is tied to quadrant management, and the HFS TOP 10 threatens to impact their cosy existence.

Full credit to Allen, who runs a tight ship of analyst relations executives to communicate their performance effectively. While the current system works for Accenture, it clearly impacts the quality of relationships with analysts, their own clients and their under-pressure executives. It’s too stressful, drives far too many negative, defensive conversations, and, quite frankly, degenerates the whole balance and value of analyst/vendor relationships. While am sure it will take time for many people to fully get used to the more strategic methodology the TOP 10 brings to the table, having the market leaders immediately voice their support (and relief) is heartening.

Yes, folks – the rumors are true. HFS is officially out of the quadrant business.

We’re done, the whole quadrant craze is starting to smell pretty bad and we know the industry is fed up with it. Increasingly, many of these 2×2 matrices are missing several of the market leaders (who refuse to participate) and having them all stacked in the top right just smacks of pay-for-play (even if the analyst has fair intentions). Let’s be honest, noone trusts these matrices and they are harming the entire credibility of the analyst industry. Sure, there are many honest, quality analysts with integrity, but their craft is being soiled by several quacks who are basing their vendor placements purely on vendor briefings, whether they like a particular vendor, and whether some vendors pony up for their research services. There are many “analysts” out there who do not bother to do sufficient customer research and we all suspect who these characters (and their employers) are…

If we don’t change, we all – as analysts – might as well admit we’re no longer in the research business: we’re in the vendor PR business. Yes, it’s that bad… and let’s stop sugar coating it.

Enterprise executives tell us all the time they get zero value from these grids – they are purely for vendor marketing sales decks (and I talk to a helluva lot of these enterprise folks). However, enterprises desperately need to be informed on vendor performance – they just need a direct ranking that’s relevant for their needs, where a credible analyst puts a stake in the ground. That’s what everyone has told me, so that is what we are delivering: The HFS TOP 10.

Quadrants, Peaks, NEATS and Waves – and sadly Blueprints – are all sales tools for vendors as opposed to decision support tools for enterprise customers. At HFS, we are not in that business – we are in the research business to support informed enterprise decisions. At HFS, we are not ending our involvement in covering the hottest markets in the industry and producing the best competitive analyses, we are merely making our research more relevant, more timely and more impactful with the HFS TOP 10 and much more simplified to support the enterprise customer. What’s more, when some firms take six to nine months to get a quadrant to market, that market has often already moved on, and the data, despite its credibility, may already be stale. We are in a world that doesn’t stand still, where enterprise customers are thirsty for timely, credible data that clearly shows the winners, contenders and laggards in a given market.

Customers want rankings where the analyst took a stand, not merely a fuzzy matrix where everyone looks like a winner. Here is an example of how the HFS TOP 10 ranking looks (the RPA Products in 2018), and here you can download a full report example to see for yourself how we get to the point, how we inform decisions and we clearly profile where vendors are strong – and where they face challenges.

HFS TOP 10 reports remove the unhealthy involvement of vendors from the analyst evaluation process and are much more timely, relevant and less cumbersome to produce

The main difference with the HFS TOP 10 is the fact we’re running them purely on desk research, support from our research academy and from our vast repository of current user data. We are eliminating the whole laborious vendor lobbying and briefing processes so we can get these reports out the door faster than ever before, without being tied to vendors schedules and relying on references they provide. This does not mean analysts cannot do vendor briefings to support their research (if the analyst deems it necessary, or if the vendor requests a timely briefing), it just means we do the research in a timeframe that can’t be moved. It means vendors cannot complain that we “did not do reference calls with their customers” or give them a chance to be adequately represented in the market. Because HFS already has the data! We have reams of data on service vendor performances, or vertical markets, on RPA products, on blockchain platforms, on analytics firms, on FinTechs etc. And where we may occasionally not have sufficient customer data in a niche market, we will invest in gathering it using the HFS network. Yes, we actually set aside funds for user surveys where most of our competitors only perform custom research when their customers are funding it.

Here are some FAQs you probably want answering:

1. How is the methodology of the HFS Top 10 different from the Blueprint? There are several key differences in methodology:

a. We are Ranking vendors, not Gridding them. The HFS Top 10 is presented as a simple and clear ranking of assessed products / service vendors versus the 2X2 Blueprint grid

b. Voice of the Customer, execution success, and innovation capability. The HFS TOP 10 methodology is driven by customer experience with products / services (voice of the customer) in addition to vendor’s ability to execute and innovate.

c. Powered by HFS G2000 network. The primary source of data for the HFS TOP 10 reports is HFS’ extensive network of G2000 enterprise customers. HFS will gather information via surveys, analyst interviews, and ongoing dialog with customers versus relying on data inputs from service vendors. HFS conducts over 5,000 interviews a year with enterprise customers right across the six change agent areas of our research coverage: RPA, AI, Smart Analytics, Global Sourcing, Blockchain and Digital Business Models.

d. Not reliant on vendor RFI responses. The Top HFS TOP 10 report methodology does not rely on the use of old-school traditional approaches of collecting data through vendor RFIs. We welcome vendors to augment our analysts’ knowledge base through structured briefings, demos, and reference customers, but this not a necessary component in the process. We will not allow vendors to slow-down our research processes.

e. No opt-out. There is no opt-out for leading vendors given HFS is relying 100% on its own network and data sets. We never produce vendor landscapes where half the leading players are absent.

2. Will there still be fact checks with the vendors?

Yes, vendor profiles, including strengths and development opportunities will be sent for fact-checks. However, rankings will not be shared in these fact-checks. An embargoed HFS TOP 10 will be released one-day prior to the actual release of the report, intended to be an FYI versus any negotiation on ranking etc. We are not in the lobbying business, we are in the research business.

3. What data will populate the HFS TOP 10 reports?

The data will be populated from multiple sources of information:

– The primary source of data for the HFS TOP 10 reports is HFS’ extensive network of G2000 enterprise customers. HFS gathers this information via surveys, analyst interviews, HFS roundtables and summits, and ongoing dialog with enterprise customers, versus relying on data inputs purely from service vendors.

– Providers can augment our analysts’ knowledge base through structured briefings, demos, and reference customers.

– Note that we will minimize the use of old-school traditional approaches of collecting data through vendor RFIs (unless covering a nascent / emerging market where most of the solutions are still in beta mode).

4. What is the minimum customer data-set needed to be able to guarantee a voice of the customer? What happens, if for whatever reason, there is not enough customer data?

A statistically significant sample set is 30 datapoints for a report across reference checks, our existing data sources, and our own customer conversations. While most of our current research has a significantly higher sample set than 30 there is rarely a lack of available data to use to source the rankings. Where a lack of customer data does occur, it may result in delays of the research publication as we make extra efforts to source customer data.

5. What can vendors do to maximize customer data access?

Real value usually comes through engaging with HFS analysts throughout the year by providing HFS analysts the opportunity to speak with more of their customers, sharing and collaborating on customer stories. As mentioned, we make it our business to do our own customer research – that is our purpose in the industry, but those vendors who can persuade many of their customers to showcase their experiences will benefit.