One of the most notable turnarounds in recent IT services history has been the remarkable increase in revenue and profit performance of Wipro since Thierry Delaporte took the helm 18 months ago just as the Pandemic was in full throttle. Over the past few quarters, the firm has posted close to double-digital revenue growth and will surpass the $10 billion revenue level. Thierry moved swiftly to make restructure the firm around geographic regions while simplifying its management structure, and he also brought in some new faces from the outside to add fresh ideas, energy and focus to implement his plans.Read More

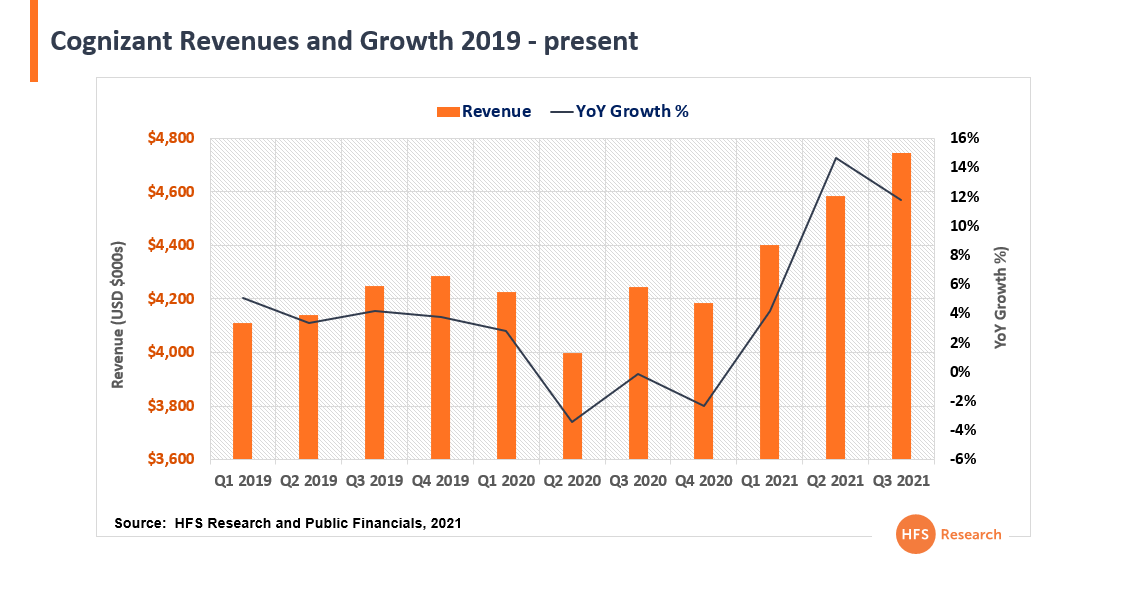

One of the most over-criticized service providers of the past couple of years has been Cognizant. The company which rocketed from $1bn-$15bn in 15 years took full advantage of the pre and post-Great Recession offshore boom, the directionless years of Wipro and Infosys, and a lovable arrogance… which even scared the hell out of Accenture. And all this was achieved with very few changes to its leadership team and an entrepreneurial spirit which was the envy of the IT services industry.Read More

We’re excited to unveil our eagerly-awaited Top Ten report covering Native Automation Services (click here for your copy). In short, Native Automation services leverage a range of emerging technologies to create intelligent and automated workflows in the cloud enabling new “native” standards for consistent cross-functional enterprise operations. Let’s remind ourselves that automation is not your strategy. It is the necessary native discipline to ensure your processes provide the data – at speed – to achieve your business outcomes. Hence you have to approach all future automation in the cloud if you want your processes to run effectively end-to-end.Read More

Almost two decades after its landmark acquisition of PwC Consulting, IBM Global Business Services (GBS) is now IBM Consulting. Just another industry rebrand, you say? Botox for GBS? Not so fast. .Read More

“Freedom” appears to be the current central theme of individuals who refuse to be vaccinated against COVID-19m as one of many reasons for refusing to be protected against the deadliest pandemic in over a hundred years. It is essential to recognize that many reasons for not getting vaccinated can be overcome by the enormous data we now have, with over 45% of the world’s population vaccinated with over 6 billion doses.

The data shows that the vaccine effectively prevents deaths and serious illness, the side effects are marginal compared to the effects of COVID-19, and it is the only way to get back to the normal we are desperately seeking to experience again. That translates into supporting all those on the front lines as well as evangelizing vaccinations.

Healthcare workers and teachers are not the villains here

Healthcare workers have gone from being heroes that we cheered at the Pandemic’s peak to being threatened, ridiculed, and harassed in recent months. A school association (NSBA), representing locally-elected school board officials that oversee more than 50 million US public school students, has requested the FBI and President Biden to provide them with protection due to the increased threat levels to officials and teachers.

These threats are in response to healthcare workers and teachers encouraging vaccination or enforcing mask mandates, both intended to help protect individuals from contracting COVID-19. In a civil society, threats are a non-starter in any facet. To harass those who protect and cure us of diseases, to threaten those that educate our young minds is unacceptable and unfathomable.

Such behaviors could have profound implications when there is already a high turnover of healthcare workers, sometimes 100% attrition in a typical year, which could very quickly translate into a critical shortage. Our kids are performing below average compared to other OECD countries, and lacking teachers will make the US even less competitive than we are already headed.

We must balance vaccine mandates: If those who are providing services are vaccinated, then those receiving those services must also be vaccinated

The federal government has mandated vaccines to all its employees, as have many states and cities. Corporate America has taken its cue from that mandate to issue its corporate mandates for vaccinations. Many enterprises, including hospitals systems, are issuing ultimatums to their employees to be vaccinated or lose their employment.

The holistic effort to vaccinate vast populations either through free access or mandates appears to be effective with about 66% of the US population over the age of 12 being fully vaccinated and the delta variant on the retreat.

Freedom is a fair concept and must be equally dispensed. If those who are providing services are vaccinated, then those getting those services must also be vaccinated. That would be reasonable to ensure that everybody has a level of protection.

Protect our people to return to business as usual

The airline business has been returning to a level of normality given the strict protocols in place for testing and vaccination. Restaurants in certain cities are experiencing some “normal” due to protocols in place for vaccine evidence. Such examples are beginning to expand across the US and globally.

A critical driver of that return to normal has been the vaccine, which has been highly effective and will likely continue to improve on its efficacy with the boosters. This data is important to support the need for a wider proliferation of vaccines. For example, recent data from the US shows that 50,000 “breakthrough” cases from the delta variant with vaccinated citizens only resulted in 59 actual hospitalizations.

Consequently, corporations and small businesses must have the freedom to do what they need to protect their people. Keeping their employees safe is paramount, and if that means mandating vaccines or refusing services to those who are not vaccinated, so be it. This is the path to going back to being in business as usual and enjoying the fruits of freedom.

The bottom line: Freedom must be an equal opportunity right; if individuals choose not to get vaccinated or refuse to mask up because they do not want to surrender their freedom to a mandate, then they must accept not getting healthcare or education, or other services from establishments that have a vaccine or mask policy.

Nurses and teachers are two of our most trusted professions. If we vilify and threaten them how will the rest of the society fair? So, we are calling upon corporations, small businesses, and individuals to help enable healthcare workers and teachers to refuse services to individuals who are not vaccinated and refuse to do so. Healthcare workers must be allowed to refuse treatment in non-emergency conditions as should teachers be allowed to refuse to teach kids who will not be vaccinated or wear a mask in a public setting. In these unparalleled times, we must protect each other to return to the lives we cherish. That is the only way forward.

The banking and financial services sector remains the largest market for IT and business process services and is generally regarded as one of the most aggressive in terms of emerging tech adoption. However, do not confuse the spend and the adoption with digital transformation. So much of what gets done in established banks and capital markets firms is all about care and feeding of some of the largest and most complex tech stacks and business processes in the world. As with the rest of the planet, the pandemic exposed the lack of digital transformation achieved by established financial services firms.

Many subsegments of the financial services sector were 100% certain they were digitally transformed pre-pandemic. It took a global crisis to lay bare the precise lack of connectivity between glossy front-end customer engagement interfaces and the myriad of aging back-office systems that actually run financial services firms. The post-pandemic imperative is rapid modernization across all BFS subsectors, with implicit cloudification and digital optimization to connect the front to back. This is only achievable with a collaborative ecosystem approach. This is where service provider partners came up big during the pandemic.

Our BFS practice lead, Elena Christopher, weighs in to share the results of our 2021 Banking and Financial Services research on the leading service providers specialized in supporting BFS customers.

Well, aside from a searing validation of the myth of digital transformation in BFS markets, the pandemic served as the ultimate reality check of what happens when digital CX is not linked to the back office and employee and partner enablement. This pursuit of the OneOffice yielded three core study themes around context, collaboration, and creativity.

Context. The pandemic ultimately helped BFS firms and their service partners prioritize their transformation needs with leading priorities centering around payments modernization, core banking transformation, and enhanced digital experiences for its customers. In all cases, the cloudification of legacy or migrating applications to platform solutions increasingly offered as managed services enabled the transformation. Digital enablers such as Triple-A Trifecta tech (automation, AI, and analytics) are increasingly embedded in engagements as native enablers rather than as engagements in their own right. This is transformation contextualized for BFS.

Collaboration. You can’t achieve contextual transformation alone—at least not at pace or with guaranteed success. IT and business process service providers are critical partners to help BFS firms on their change journeys. Part of their value is their ability to help curate partnerships and form collaborative ecosystems of services expertise, technologies, hyperscale cloud capabilities, and industry expertise. It is this collaboration across partnerships and ecosystems that fosters exponential speed and value.

Creativity. Driving differentiation as a provider of IT and business process services to the BFS sector is hard work. It’s a highly competitive, crowded market, often ruled by incumbents. Its strong sourcing culture is perhaps over-focused on the best deal rather than the best outcomes. Aside from table stakes investments in offerings, talent, and tech, providers are getting creative with commercial and engagement models such as modernized managed services offerings. They are also finding digital whitespace in neglected corners of the BFS market, such as wealth management, retirement, commercial banking, and capital market front-office capabilities.

Which service providers are really helping BFS enterprises make an impact?

For the BFS study, we assessed 18 service providers who specialize in industry-specific services across banking and financial services value chain. We opted to break the results into two reports:

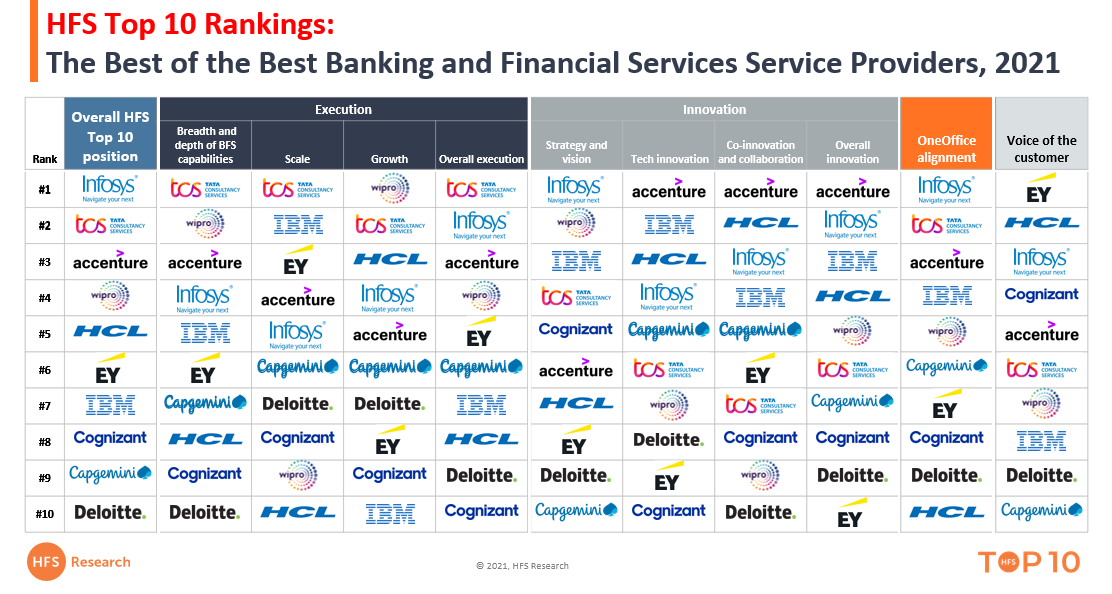

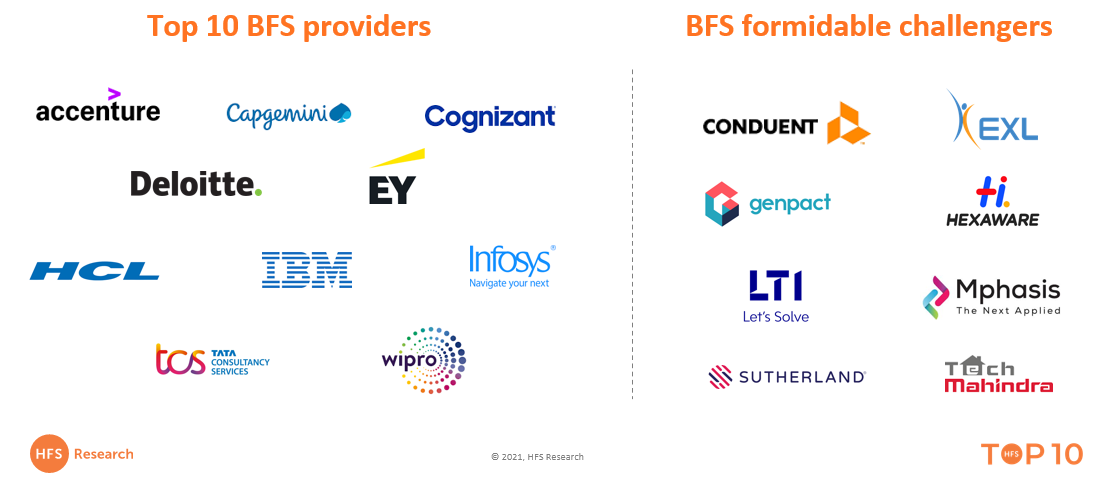

The 2021 HFS Top 10: Banking and Financial Services—The Best of the Best Service Providers report examines the capabilities of the ten largest service providers to BFS clients. These providers have full value chain coverage across banking and capital markets, revenue of $1.5B+ and 20,000+ BFS-dedicated headcount. Enterprises assessing providers should think of this lot as your end-to-end transformation partners.

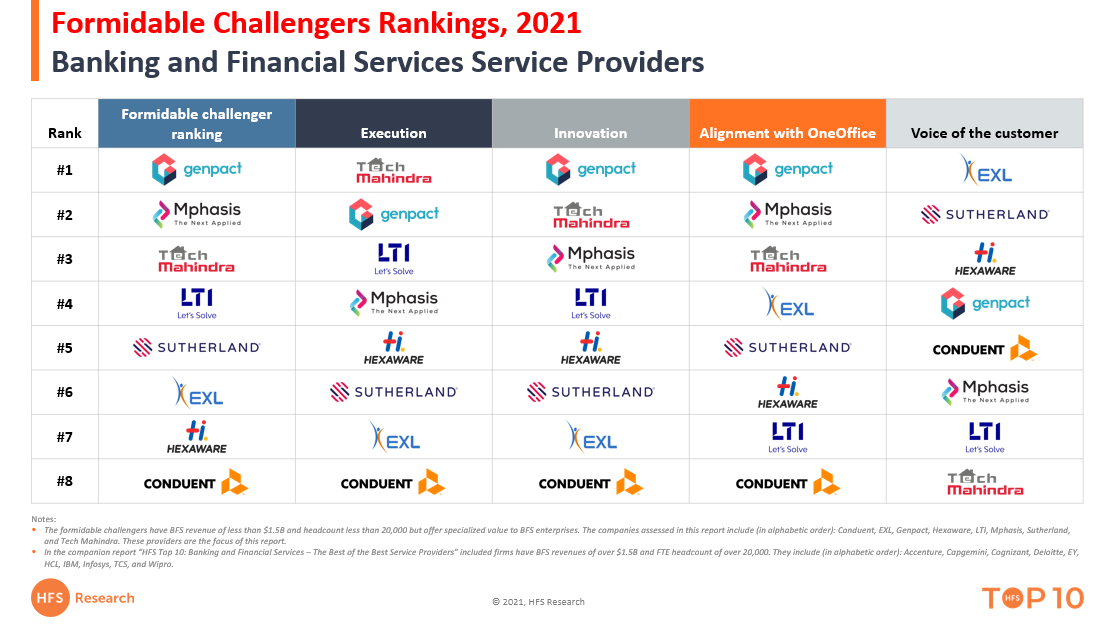

The 2021 HFS Market Analysis: Banking and Financial Services Formidable Challengers report features eight IT and business process service providers offering differentiated approaches to meeting the industry-specific needs of banking and financial services clients. They may not be as large as the firms featured in the BFS Top 10, but they routinely punch above their weight delivering contextual transformation enabled by deep subdomain process expertise and enviable applied technology capabilities. Enterprises assessing providers should think of this group as specialists.

For the Top 10, we assessed 10 service providers across execution, innovation, OneOffice alignment, and voice of the customer criteria. The top five leaders are 1. Infosys, 2. TCS, 3. Accenture, 4. Wipro, and 5. HCL. These leaders’ shared characteristics include deep industry expertise across BFS subsegments combined with strong consulting, design, and IT and business process expertise, continued identifiable investments and growth in their BFS businesses, strong cultures of innovation, deep and ever-evolving third-party partnerships, internal OneOffice alignment enabling a comprehensive external approach with clients, the ability to deliver business outcomes, and exceptional customer experience.

Some specific call-outs on the BFS Top 10 leaderboard:

Infosys secured the #1 position overall, successfully defending its title from 2019. What helped Infosys prevail across our four evaluation pillars was essentially continued investment and refinement of its capabilities leading to notable new client wins, deal expansion, and ultimately customers reaping the benefits of business outcomes. We specifically took note of its growth throughout the pandemic, ongoing investment in onshore and nearshore regional operations, big deal wins – most notable of which is Vanguard retirement, but complemented by wins with regional and mid-tier banks like Indiana-based Old National.

TCS grabbed the #2 spot overall, driven by a commanding performance in Execution and OneOffice alignment. We took note of its sustained growth during the pandemic, regional investment like its roll-out of Pace Port innovation centers, and its continued focus on selling beyond the CIOs’ office.

Accenture nabbed the #3 spot overall led by its top innovation performance and top three performance in Execution and OneOffice. What stood out for us was its strong investment in IP, notably its myIndustry offerings for BFS, clear connective tissue between its big investments in cloud and how that helps BFS clients, and one of the best partner ecosystems.

Wipro’s continued investment in its BFS capabilities, including its recent mega-acquisition of Capco, helped it secure the #1 position in growth, #2 spot in strategy and vision, and the #2 spot in depth and breadth of capabilities.

Cognizant secured the #5 position in strategy and vision, buoyed by strong investments in leadership and enhanced capabilities. Its customers also came through, recognizing its progress moving from IT provider to strategic partner, scoring it the #4 slot.

IBM scored the #2 spot for scale, driven by its global footprint and capabilities. Its ongoing investments in innovation helped it score well across the board, ranking it no lower than #4 in any innovation categories and #3 overall. It Banking and Financial Markets group formalized an array of powerful services capabilities around core banking, payments, digital banking transformation, capital markets, intelligent security, risk, and compliance. Oh yeah and cloud.

HCL secured the #2 position in co-innovation and collaboration, driven by its continued commitment to partnership beyond the contract. The firm also landed the #3 spot in growth.

EY, a new addition to this year’s study, fared well across the board, securing a top-five position in execution and leading VOC.

For the Formidable Challengers report, we assessed eight service providers across execution, innovation, OneOffice alignment, and voice of the customer criteria. The top three leaders are:

Details on notable performances from our BFS Formidable Challengers include:

Genpact was our #1 Formidable Challenger for BFS services. The firm shored up its BFS leadership in its consumer banking segment with strong hires from within the industry. This is driving renewed focus and growth, including geographic expansion with some recent UK and Europe wins under its belt. The acquisition of Rightpoint and consolidation of design and experience assets under the Rightpoint brand are driving effective tip of the spear transformation engagements. HFS notes the continued investment in new and improved CORA for banking assets and its cloud transformation capabilities that contemplate process reinvention. It also has notable strength in financial crimes compliance.

Mphasis earned the #2 spot for Formidable Challengers driven by its unbroken growth streak despite the pandemic, putting up 13% growth year over year. About 80% of new deals are sourced proactively, and its average big deal size has more than doubled. Its new pandemic-driven offering is NextOps, a framework for reimagining digital operations. Mphasis recently opened a nearshore center in the UK to expand its footprint in the local region for its BFS business.

Tech Mahindra secured the #3 slot for Formidable Challengers. While TechM is a $5B company, its BFS business is smaller than its TWITCH competitors’, allowing it to retain a certain nimbleness. Strategic M&A has been a strong growth lever for TechM, with several design-focused acquisitions boosting digital CX and design capabilities and a payments business to bolster its platform capabilities. It launched new offerings spurred by the pandemic, such as video-KYC and mobile customer on-boarding. TechM’s BFS growth is largely through expansion within existing accounts, often supported by co-innovation initiatives and funds.

EXL and Sutherland secured the #1 and #2 spots in Voice of the Customer, underscoring the close ties these BPO-led firms have cultivated with their clients.

LTI made it into the top three for Execution led by its supercharged growth and strong depth and breadth of capabilities across the BFS value chain.

We always go deep on Voice of the Customer to round out our research. Any notable take-aways here, Elena?

In a nutshell, BFS firms pick their service partners based on execution criteria, not innovation potential. This needs to change.

We did deep-dive interviews with over 50 BFS firms as part of our VOC research for this study. We observed that BFS firms select their providers based on execution-oriented criteria such as delivery quality, array of services, and industry and domain expertise rather than leading with innovation criteria such as advisory, digital expertise, automation, or partnership ecosystem. Downstream in the relationship, when assessing satisfaction, BFS firms have the highest levels of satisfaction with execution, while innovation capabilities leave something to be desired. If BFS firms want to get real about transformation and results, they need to prioritize innovation as part of the perfect partner capabilities mix.

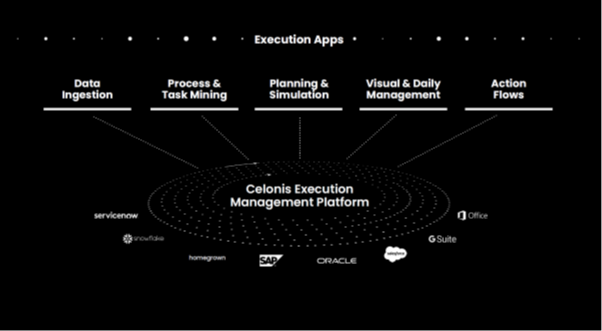

The new Celonis–ServiceNow partnership blends operationalizing data science with the capability to design workflows in the cloud. We are witnessing a determined partnership between the leading IT Service Management vendor and the leading process execution platform. This is a true first in combining an IT-centric workflow mindset with an operations one. This is where we combine IT orchestration with process modeling, mining, discovery and execution. And even RPA. The likes of SAP, Pega, Appian and UiPath will be feeling very nervous right now and surely have to make massive investments to keep pace with what we’ve just witnessed.

This is the boldest move yet to automate complex data with process intelligence

Against this background, Celonis’ strategic partnership with ServiceNow is a bold step that could reshape many IT and business operations discussions across major enterprises. The announcement spans initially a reseller agreement, a deeper integration of both platforms as well as a joint go-to-market.

Notably, ServiceNow is making a strategic investment into Celonis, and partners are expected to launch joint products as early as the first half of 2022. The strategic intent is to link Celonis’ data platform with ServiceNow’s workflow ecosystem to advance toward the broad execution and ultimately automation of complex data ingestion and process intelligence.

From a Celonis perspective, it is the logical evolution of its ambition to offer a powerful execution management system. Or in plain English to position itself more as an automation rather than a data company. Figure 1 outlines the strategic intent as well as the integration into the leading cloud platforms.

The Celonis EMS ecosystem straddles data, automation, and intelligence to deliver more value from core ERPs

Source: Celonis 2021

Celonis’ product investments are seeing it double down on big, hairy data and automation problems (process mining who?)

The other big announcement during the ‘Celonis World Tour’ digital event was the acquisition of DataOps provider, Lenses.io. This addition brings streaming data from any Apache Kafka project into the Celonis EMS platform. This enhances the platform’s data ingestion capability to most data types and crucially provides the basis for real-time operational intelligence.

The approach that Lenses takes to dataops is almost as important as the streaming data technology itself. The vendor allows solutions to be built by analysts and engineers without necessarily needing them to be experts in Apache Kafka and stream processing through a low code, UI-based interface while allowing monitoring and governance to ensure performance.

Operating with real time data is an aspirational goal for many enterprises as they become more and more data-driven. As a supply chain executive shared in our recent process intelligence Top 10 research, “I want to jump on digital supply chain management, but I can only do this if I have access to real-time data.”

At the same time Celonis positions itself to advance with convergence topics as Lenses can also integrate data such as the telemetry provided by AIOPs and Observability tools that shape the IT Operations discussions.

Celonis must also keep investing to help clients at the bottom of the tech maturity curve

While it designs the bright and shiny new future of enterprise operations with EMS and ServiceNow, Celonis must also meet struggling enterprises where they are and invest to bring them along for the ride. Automation, data, and process intelligence technologies are seeing significant investments from the Global 2000. But from our research, including conversations with enterprise clients, global SIs, and consulting partners, the ground challenges of implementation are substantial. For many, data integration is the big element that is a roadblock to the adoption of products like Celonis. While the vendor invests in streaming data, process simulation, and execution graphs that get into more and more sophisticated uses of emerging technologies for business processes, it must make it easier for the average company to get the basics in place.

To this end, we do see Celonis releasing new features, such as new connectors and data sources. The ServiceNow partnership will also go a long way in easing integration challenges and delivering value to clients using both technologies across business and IT. Ultimately, to drive mass adoption, these tools need to enable faster and less painful ways to deploy across the organization. As one of the enterprises in our research shared, “These newer offerings [in the process intelligence market] are completely new to us. As a company, we are far behind. We can’t fully grasp technologies like AI/ML – they are almost too innovative.”

ServiceNow doubles down on foothold in business operations

Even though 40% of its revenues come from non-IT workflows, with the Celonis partnership, ServiceNow opens a completely new buying center. Most of its business-centric deployments are in customer and employee services. Yet, the potential for the collaboration is indicated by the fact that ServiceNow’s most innovative clients such as Japan Tobacco are managing GBS operations with ServiceNow end-to-end. Clients are attracted by ServiceNow’s holistic data model and by cross-functional workflows capabilities. Thus, ServiceNow is central to the notion of operationalizing the OneOffice (For more details of the dynamic of the ServiceNow ecosystem, see our blog.) Lastly, by partnering with Celonis, ServiceNow is also building a buffer against Salesforce encroaching on its established ITSM patch.

Bottom line: The Celonis-SNOW partnership centers on operationalizing the OneOffice, furthering Celonis’ strategy of expanding data capabilities to design workflows in the cloud

If both partners can execute against the strategic intent, the announcement could herald a new phase in the battle for dominance in the back-office. Blending operationalizing data science with the ability to design workflows in the cloud, would put both organizations beyond the often myopic RPA-centric discussions. And if both partners get comfortable with each other despite contrasting organizational cultures, the future could move from courtship to a financially secured relationship.

The market dynamics in business operations are at a tipping point. RPA providers that used to dominate the discussions are moving toward ISV ecosystems to provide extensions to legacy applications as part of a much broader value proposition. Salesforce acquiring Servicetrace and ServiceNow picking up Intellibot were the most recent examples. But perhaps the most telling event was that the poster child of RPA, Blue Prism, put itself up for sale to be consequently acquired by private equity just to be merged with Tibco. Tibco a data-centric provider has lost much of its relevance. Yet, operationalizing data science in particular in the guise of process intelligence is taking center stage of the operation discussions.

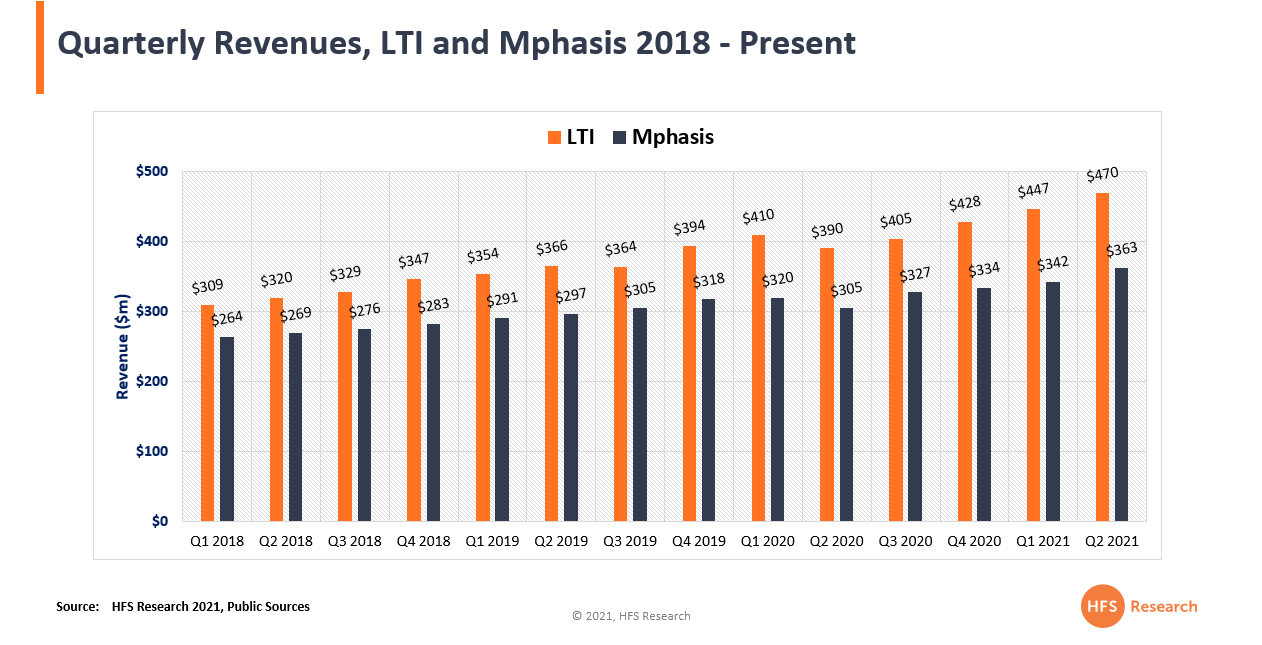

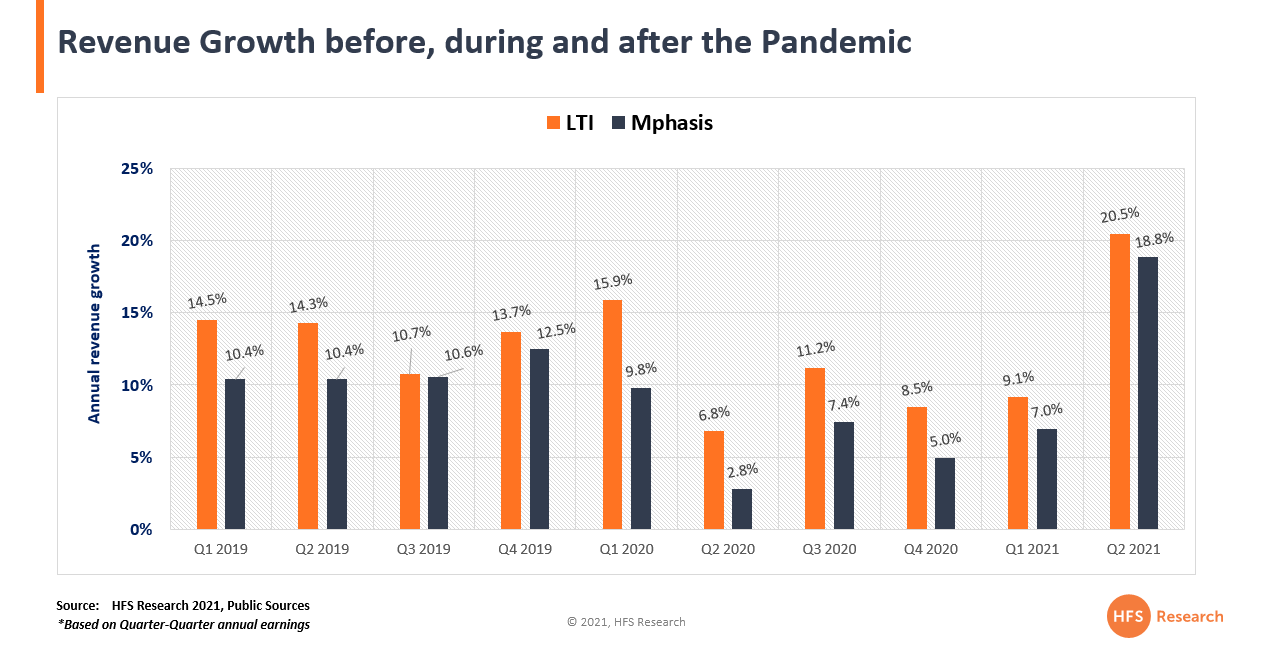

While most folks are obsessing with the performance of the IT mainstays over the past 18 months, spare a thought for two IT services businesses that not only entered Covid on a long growth cycle, they also readjusted quickly and carried on their growth stories even during the worst of 2020. Just check out the quarterly revenue growth paths of LTI and Mphasis respectively:

Click graphs to Enlarge

Why have LTI and Mphasis carried on their growth unphased?

Big enough to get to the table, small enough to keep client intimacy. It’s the oldest quote on the book for the mid-tier service providers, but couldn’t be more true in today’s market. Enterprise clients want to feel they have the personal attention of the CEO and the leadership team when it comes to signing over their technology control. Rewind 10-15 years, most enterprise CxOs had a direct line to Chandra (TCS), Shibu (Infosys), Jeya (Patni), Pramod (Genpact) or Frank (Cognizant). Client leaders wanted to feel the personal touch from their services partner leaders, and they were usually personally involved in the scope and negotiations. Today those same executives are most likely stuck with a client partner, who is literally horsetrading the rate card with them. Enter the likes of Sanjay and Nitin, who spend most their time talking to their clients, reassuring them, convincing them, but most importantly are available to them.

Flatter structures and visibility to leadership motivate staff. Staff want more from their companies these days than a good stock plan and competitive salary – they want to know what their leadership stands for, and want to learn from them. With less bureaucracy and promotion cycles based on merit, not purely tenure, it motivates staff to see how to get ahead, and and having more access to their leadership. Nothing demotivates staff more than seeing weak managers stay in their positions year in, year out, while the rockstars leave, or are sacrificed. I have even seen hierarchies in some services providers so rigid, you are instructed not to interact with people in the level beneath you. Yes really…

Sustained profitability helps high performers to be financially rewarded and retained. In a market where attrition is running at an all-time high, the smart players are identifying their talent engaging with clients and helping them execute and making salary increases to keep them. Providers like LTI and MPhasis have kept their profit margins in the high-teens consistently over the Pandemic and are in good stead to reinvest in retaining key talent and attracting new blood from start-ups and larger service providers suffering from low morale.

Savvy tuck-in investments and market moves. Mphasis continued to bolster its depth in largest industry, banking and financial services, with its Front2Back transformation methodology and NextOPs framework really bearing fruit during the Pandemic, while also venturing effectively into other industries, such as logistics. The firm also added delivery depth in the UK, notably acquired Seattle-based digital design house Blink and significantly de-emphasized its reliance on DXC as a client. LTI merged most of its cloud transformation under its Infinity umbrella mimicking Accenture’s Cloud First and Infosys’ Cobalt offerings, but at a lower price with a focus on outcome or risk-based pricing models. This bought their customer an extra ~20% of possible savings while the downturn driven by the Pandemic was underway. LTI also ramped up its CSP/Hyperscaler partnerships (mainly with AWS) at the right time and added some customers to their book through acquisition.

CEOs who can inspire and motivate their people. Simply-put, making themselves highly accessible to customers and staff has been huge in driving their respective businesses. Moreover, showing longevity and loyalty to their brands has been a key factor with Nitin recently signing on for a further 5 years at the helm with majority investor Blackstone.

Bottom-line: Big is no longer brand-beautiful

The days where you never got fired for hiring IBM, or ensuring high performance being delivered with Accenture, are not as vogue as they used to be as service delivery levels off across providers and speed/execution take center stage. Moreover, the top tier of service providers simply cannot afford to focus their A teams on smaller-scale deals that will not fit their high-pressured revenue models. The amount of new business becoming available to the likes of the LTI, Mphasis, Virtusa, Hexaware, Zensar et al is larger than ever and most of the Global 2000 opt for one to two primary global service providers and a couple of these nimble, energized mid-tier firms to keep everyone honest.

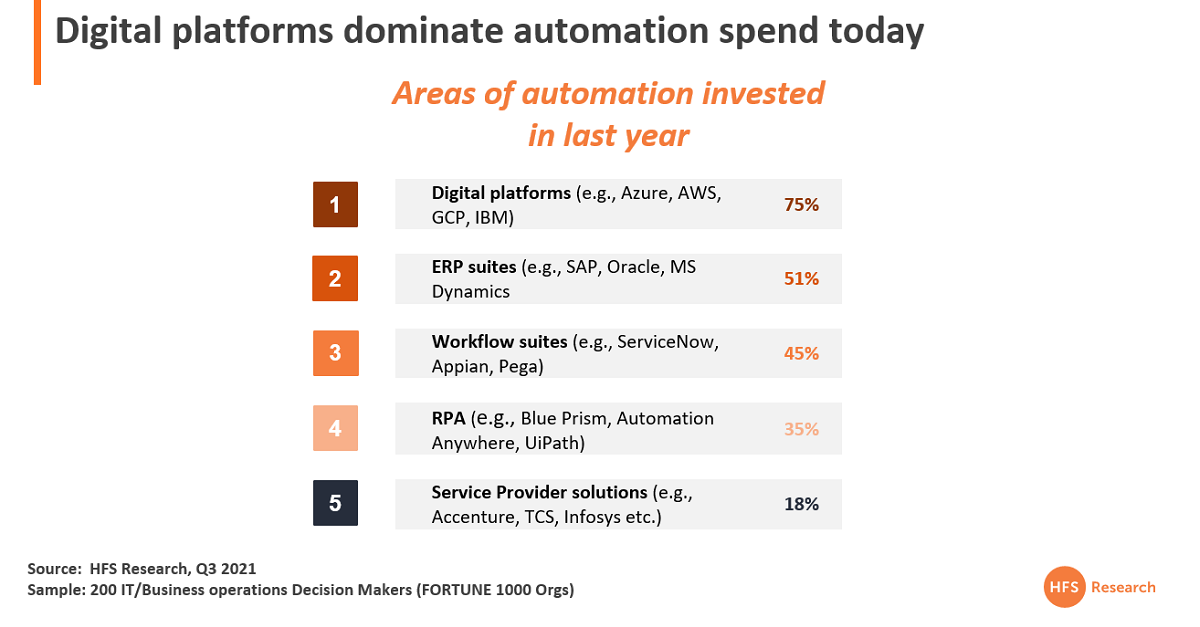

New insights by HFS Research from FORTUNE 1000 leaders provide the context of how we have to reimagine the automation narrative. It is not about the myopic view of one bot for every employee or bold claims of progressing toward the autonomous enterprise. It’s about delivering immediate outcomes by designing workflows that take the RPA value out of the back office, where most RPA has been buried, and aligns its capabilities with helping the immediate commercial needs for the enterprise. The need to create immediate solutions with the digital hyperscaler platforms is now far greater than ERP suites, as that is where the hyperconnected business environment operates, as opposed to the traditional back office.

RPA impacts when it helps enterprises function effectively in new virtual customer and supplier environments

Over half of organizations are realizing that it requires rapid investments in process innovation to be effective in virtual environments. Before and during the pandemic, organizations that deployed RPA as a band-aid on badly designed or even broken processes were found badly wanting. Firstly, scaling fragile processes with RPA fixes is a huge challenge – they are brittle, and usually results in perpetuating a legacy environment. Secondly, RPA can have much more impact when it is deployed to bridge existing commercial systems with digital platforms that are essential for survival.

The RPA fraternity has reacted to this by accelerating tie ups with the Hyperscalers. The most recent example is Blue Prism (see news) who significantly expanded capabilities across the AWS ecosystem. However, what is urgently needed are proof points of how we are managing the new complexity of cloud native deployments. If applications or processes are running on containers, the interdependencies and consequently the reasons for failure increase exponentially.

As our current in-progress study of the automation focus of the FORTUNE 1000 is already revealing, the majority of automation investments enterprises are making are with the digital platform giants (75%). Only half of them still keep faith in ERP, while even less are focused on workflow suites and the RPA platforms themselves. Hence, hooking up with AWS is a masterstroke as it dominates so much of the commercial supply chain in the virtual economy:

The onus shifts from fluffy “strategy” to immediate need fulfillment

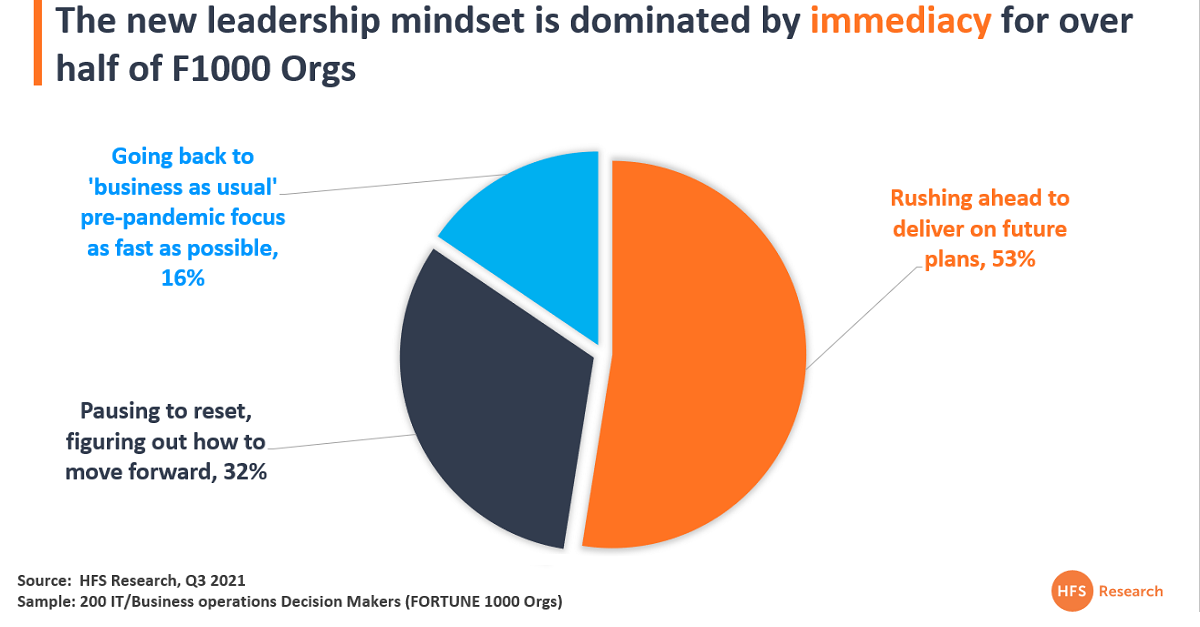

Addressing immediate critical needs at the business and supply chain end is happening… when you get into the whole commerce space the needs are immediate. Like how does a consumer products firm take data from legacy supply chain systems into an AWS environment… not the sort of thing you can solve overnight. You literally can’t operate seamlessly in the virtual economy if you don’t have the tools to link the old with the new, and RPA must be part of the toolbox to make immediate impact with the suppliers and customers which are the lifeblood for survival in a world where supply chains are falling apart at the seams, customer needs are immediate and stitching together processes from the front to the back office is the only way to function in today’s hyperconnected markets. As this new data shows us, more than half of today’s F1000 organizations are under intense pressure to implement new capabilities to take them into the future, as opposed to clinging on to the past:

Bottom-line: Automation is not a strategy it’s the native discipline to keep the wheels on as you rush to the future

Organizations are gearing up to drive fundamental operational change. To stay relevant in the virtual world, application and processes must be designed in and run on the cloud. This requires not only a broader ecosystem of cloud native capabilities but a new mindset and culture of running operations. It is literally about operationalizing the OneOffice by driving change that finally delivers on overcoming the organizational silos and experience-led outcomes. Yet, we can only get there by converging IT and business operations and by leveraging IT and business automation

So what’s our new cloud guru Joel Martin, saying about the frantic rush to the cloud these past few months? Let’s just hear it from the horse’s mouth…

Phil Fersht, CEO and Chief Analyst, HFS Research: Hey, Joel. So how should we be thinking about cloud today? What do you think has changed in the last couple of years, and how should we think about the market as it starts to evolve?

Joel Martin,Research Leader, Cloud Strategies, HFS Research: The cloud is the architecture people are building their businesses on. As we move to these virtualized economies, virtualized businesses, and virtualized experiences, inside and outside the organization, the cloud is the only way companies can scale up and scale down their ability to reach those customers and deliver services. They can’t do that within their private data centers. And that’s the biggest differentiation of using hybrid or public cloud, is that scale versus continuing to invest in in-house IT talent, resources, and tools.

The thing that has changed Phil, is the speed of the network. With fiber, 5G, and gigabit speeds working in the cloud feels like you are working on a device on a local network. The pure speed at which we can create, collaborate, and innovate with others, with systems, and with a growing number of AI solutions is truly mind-blowing. And it’s become so simple to use. People don’t have to be technology literate to create solutions others can benefit from ease-of-use at scale is really what we are benefiting from these days.

Phil: Okay. So tell me about the flow of workloads in the cloud. We hear about private cloud, we hear about public cloud, and then we hear about hybrid cloud. What do you think is going to be the ultimate outcome with these workflows, and how are people going to engage with the cloud in the future?

Joel: There are two things I’ll focus on. First, looking at HFS’s recent Pulse survey data, and which workloads are moving to those different cloud models paints a very interesting picture. As you look at that data, and it looks like a black hole. There’s no clear direction of how firms are preferring to deploy, develop, or adopt workloads. Instead, companies are moving their workloads to the Cloud because they have to move; remaining complacent is not an option. Honestly, we see less of a clear strategy and more of a tactical plan to get things into the cloud because their executives, employees, and customers demand it. What I see is rapid tactical execution without a long-term, conscious strategy for sustaining the current momentum. This is true across private, public, and hybrid cloud initiatives in many cases.

Second, as we move to native cloud workloads, what we’re going to see is a much more real-time access to the data across those workloads, for people to make decisions – and by people, I mean people at the executive level, and all the way down in the field level, those closest to the customer. The challenge is these, often like the applications they are moving, are the existing workloads. Too often, the drivers for these are cost-related rather than outcome or value-driven. Shortly companies are going to realize many of these workloads don’t reflect how people work now and how people engage with the markets and customers they deal with.

Regardless of cloud type, we need to change the discussion from applications and workloads to data and architecture. Once we understand the data we need to run our business, where it comes from, where it resides, and how people want to use it, then real innovation can happen. I feel we’ll realize the value of domain-centric, hybrid clouds with a whole lot of AI, and tools like Low Code will let teams and individuals create the next generation of workloads. As such, the two things CIOs and CEOs need to be focused on are data and governance. The “what and how” of composing, consuming, and curating digital experiences driven by data securely to their teams and customers.

Phil: Right. So how do you see the competition between Google, AWS, Microsoft Azure, as we look at that battle for who’s managing the datacenters in the cloud, Joel? What is driving adoption, and who do you think is winning the medium-term battle here?

Joel: Who’s won the medium-term battle out of the gates? You know, Microsoft’s done a great job at catching up to AWS, but I continue to talk to the services providers and the enterprises, and AWS is still the one they think of first. While it might not be the one they choose, AWS is still extremely strong with their ecosystem, the different solutions they’re offering for everything, from customer experience, with Amazon Connect all the way through to their big data tools and their Fargate solutions. So, you know, Amazon is still the big guy in the room, and how they’ve invested in talent across the ecosystem, at the customer level, and at the integration level, that’s what’s keeping them there right now. Meanwhile, Google is going to be a dark horse, and I think, at the end of the day, the vast majority of customers will have an Azure cloud, and then one other, and this is where Google and AWS, to me, will continue to battle for customer mindshare.

Phil: Interesting. You mentioned earlier, Joel, that we’ve now got to get our shit in the cloud, but our data’s still crap. Can you build on that a bit? I mean, how much of that is genuinely true, versus are companies now adopting a realization that they need to transform their data before they make the shift? How is that evolving?

Joel: Right now, data is moving with the applications, rather than people figuring out their data and then realizing what applications are critical to get to their data. Again, people have moved their applications quickly to the cloud because that’s been their mandate, driven by executives, and the market factors. But if you look at where we’re going with cloud-native architectures and solutions, how data is going to need to be managed, organized, and delivered is very different from the way applications or the pure database vendors built their solutions. Whether you take microservices, which requires a direct call to data to manage it, so parsing your data and securing that data is delivered completely different than a large open database, you’re also seeing a lot of native cloud database solutions, whether it’s Mongo or PostgreSQL, those things are also becoming very popular with companies, typically in smaller workloads, or smaller solutions, but they’re going to grow, and that’s going to be the data repository. And, honestly, that scares the hell out of most of the application vendors, because the application vendors are really differentiated on how they manage data and then how they integrate that data with other databases, which is really a bane for CIOs.

I’ll give you an example, I was talking to the Chief Technical Officer at a global food company, he was talking about how the marketing team will come to him and want to buy a new SaaS application because they can’t get the data they need out of SAP. Not a big surprise there. And he looks to a low-code provider that can help him extract the information out of SAP more effectively and deliver it, without using a packaged app at all; they’re able to quickly customize and build things that have strong survivability with their core systems. That’s less an application play, and more a mining the data and then presenting the data.

To me, the second half of this decade is going to be all about fixing your data. And that’ll also be driven by the amount of IoT data that’s coming into the marketplace. And this is, again, where companies are really struggling right now. I mean, you take all the IoT, say, in a manufacturing facility, where you have sensors collecting data on a device’s noise, visualization, thermodynamics, and all this data can help them prioritize how they service, replace, and maintain very expensive physical assets. That’s all important data, but it lives outside the traditional data domain. So all that needs to come together because it’ll be critical for their hyperconnected supply chains, their partners that do the servicing, and also how they manage inventory and replace the machines.

Phil: So the final question I have, Joel, is how is the role of the technical architect, the senior-level IT manager, going to change, as a result of this, and the way they interact with the rest of the business? When this becomes more and more about data, is this really less about technology, at some point, and more about just getting clean about the data we need? How do we access it? How do we get it? How do we make it ubiquitously available? How do you think this is going to change the roles of business and IT executives?

Joel: Companies will struggle to keep up with change, Phil. They are going to need to work with partners who can bring automation tools, data modernization practices, and domain-centric planning and governance. A lot of our conversation has been about moving to the cloud. Those companies that feel they can go straight to the cloud vendors (Microsoft, AWS, Google, etc.) may struggle with building and sustaining these core elements of the Cloud.

We expect to see technical people with a lot more domain expertise, so you’re not going to have business owning the domain expertise and technology owning the platform and technology acumen; we’re going to see a much more digitally fluent company that people understand, fundamentally, what their customers are paying them to do.

And, you know, at the end of the day, that’s what I look for. It’s like, what are you doing… what are you investing in that brings value to that customer engagement? Because they don’t pay you for your ERP solution. You know? They don’t pay you to have Salesforce or CRM; they pay you to answer questions and deliver services. And, you know, those are the applications that we’ll see the IT organization and the business work closer on, on developing, and all the things that take care of traditional back-office are going to be the ones they’re going to be either partnering or looking to simplify as much as possible.

Phil: So what can we expect to see, just briefly, from you, coming up in the next few months, in terms of the research that you’re driving?

Joel: The three biggest things you’re going to see from us coming out in the next few months, Phil… we have a big study on app modernization, outlining what are the opportunities to refactor, renew, replace, recode traditional on-premise software solutions and data solutions into the cloud. That’s coming out in October. We’re also going to be talking a lot more about low-code, and really drilling into how low-code and Agile methodologies are coming together to do something that we haven’t been able to do before, which is to see co-innovation between the business and the end-users, where they collaborate. They can build and sustain the momentum of being able to react to changes in the market faster than before. Another thing that you’re going to see us talking about is that mix of domain and data expertise; this will come to market as a Data Modernization research study. We’ll delve into the kind of data needed in banking and financials versus manufacturing versus healthcare and life sciences. I’m going to be working with our team that focuses on those domain areas and really drawing that out. I think that’s going to allow us to start that data conversation that will become more and more important to our customers over the coming years.

Phil: Excellent. Thanks, Joel. It’s been great seeing your research over the last few months; look forward to what’s coming up in the future. Awesome Joel!