After our dramatic fake announcement that we had entered the sourcing advisory business on 1st April, our phones have been ringing off the hook from service providers desperate to get included in our deal pipeline (no joke).

While, in hindsight, HfS& would likely have been a roaring success disrupting the legacy sourcing advisory business, we fundamentally have no desire to be an advisor shop. Sorry. Back to the research grindstone…

And for all of you who sent congratulatory notes, please do read beyond the first paragraph next time we announce something. Especially on April 1st =)

HfS Research, the leading analyst firm covering outsourcing strategies, today launched HfS Advisory (abbreviated to “HfS&”) and announced its exit from the research analyst business. The firm, once lauded for disrupting the research industry by giving its research away for free, finally conceded there is actually no money to me made from a business model where there the core product does not have an associated price tag.

As part of its relaunch as HfS&, the firm announced the following new advisory service lines, designed to disrupt today’s outsourcing advisory marketplace:

1) FTE-Lite . HfS& will disrupt the traditional outsourcing transaction marketplace by offering a series of unique advisory services designed to broker the lowest-priced FTE-based outsourcing deals for enterprise clients. HfS has contracted with a SWAT team of professional negotiators whose fees are paid by the winning service provider, allowing HfS to undercut other advisors by up to 75% on advisor fees.

2) Business Outcomes Definition Creation. HfS& has also recognized a dire need in the sourcing industry to help clients define business outcomes, so that they can be executed on, and ultimately achieved. HfS& intends to use the latest techniques in Design Thinking to make this all happen.

3) Digital Transformation On-demand. HfS& is also getting ahead of the curve with digital transformation, by offering leading edge digital transformation expertise to clients – again at much lower fees to clients as the providers will pay HfS& directly to get invited to the shortlist.

Charles “Hank” Sutherland, preparing to take the reins at HfS&, is spotted trading in his Prius for an F250

4) Robotic Process Automation Starter Kit. HfS& will also move the disruptive advisory needle by offering up real, transformative solutions to help early phase clients take their first baby steps into robotic process automation in one, complete, off-the-shelf do-it-yourself RPA toolkit. Like other advisors, HfS& has actually no clue what it is doing in RPA, but acknowledges it needs to have some semblance of a practice to appear relevant in the market.

As of today, HfS& will no longer produce research and be a fully-fledged outsourcing advisor, and has even made the steps to relocate its headquarters to Dallas, Texas under the watchful eye of Charles “Hank” Sutherland, who today was spotted trading in his Toyota Prius for an Ford F250, equipped with gun rack and complimentary enrollment to the NRA FIRST Steps Shotgun Orientation course.

Commenting on the strategic move, HfS& CEO, Phil Fersht added, “We were getting increasingly fed up giving away all our research for free and getting little appreciation for it from industry. While we did a great job putting our competitors out of business, we found it hard to develop any for ourselves either. So all we really achieved was putting the whole research business out of business. Hopefully, now, we can still glean a few bucks feeding off the stagnant remains of the legacy outsourcing advisory market before that also winds up on the scrap heap of putrid old-world business models.”

Photos of Mr Fersht and Mr Sutherland will be available once you register here.

And of course… this was an:

Please, please don’t tell me you fell for this again! (Even though the business model might kinda work…)

And while we’re reminiscing about falling for April Fools’ gags, here is 2014’s classic:

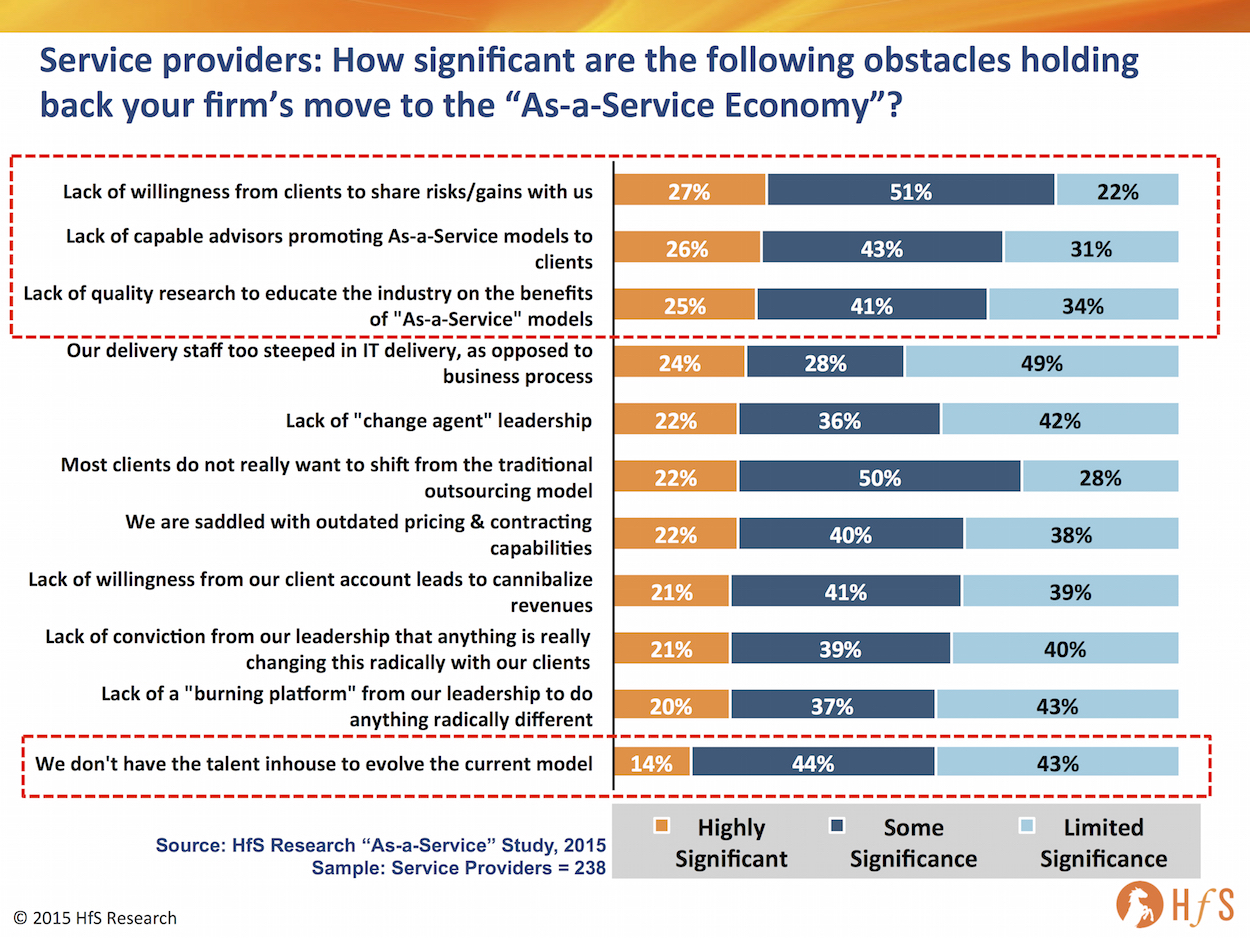

We couldn’t resist sharing a quick snippet from our new “Eight Ideas of the As-a-Service Economy” study that reveals some rather alarming news: service providers are blaming everyone bar themselves for obstructing their progress towards As-a-Service.

Click to Enlarge

At fault number 1 – the Clients. Top of the lists are their clients themselves, with 78% of service provider executives (from a pool of 238) citing their unwillingness to venture into risk/gainshare models with them. Considering most enterprise clients we talk to complain that their provider refuses to budge from their predictable, profitable FTE delivery model, baffles me here.

At fault number 2 – the Advisors. Next up are sourcing advisors – those lovely folk who bring them to the table and horsetrade to get deals done. Apparently, they are not selling the evolving model to enterprise clients and are just not very capable. We are starting to see more As-a-Service traits in some mid-tier deals, where there is less wiggle-room to make huge profits on wage arbitrage, and these frequently are too small to warrant several hundred grand being spent on an advisor. The advisor model is still built for the old world of big scale deals, not the new world where analytical and creative skills, technology enablement and automation are the watchwords.

At fault number 3 – the Analysts. And third on the list appears to be a pot shot at analysts, where providers claim a “Lack of quality research to educate the industry on the benefits of As-a-Service models”. We apologise and promise to write more coherently… and this time make sure you read it, Mr and Mrs provider executive, because we know how much time you spend trawling your way through analyst reports these days….

Least at fault – the Providers themselves. And very last on the list (no sh*t) is the fact that they are struggling with their own inhouse talent to shift the model to As-a-Service. Well that’s great news, as I thought it might be a bit of a struggle for providers to retrain their developers and project managers to think analytically, help clients with design thinking, laying out an automation roadmap etc. Now we can all rest easy with the knowledge that the providers will save the day, while the rest of us clients, advisors and analysts can all go away and die somewhere on the scrap heap of legacy labor models, SLAs and dull irrelevant research.

Bottom-line: We’re all pretty much at fault for perpetuating the old models. This is a collective learning effort across all stakeholders to adopt the ideals of As-a-Service

As we reach the end of the runway with the legacy model (which still has a way to go for many enterprises) there needs to be a much better effort collectively to discuss the actual measures enterprises need to adopt to take better advantage of the technology enablers and hone our skills accordingly. Many advisors are clearly still making a good living advising on the old model, otherwise many would cease to exist, while analysts clearly do a poor educating the market on real world examples of how to make the shift (and persist on an old world model themselves to engage with clients). Meanwhile, if service providers are as good as they think they are, they need to find better ways to convince their clients to trust them more, to work with the on joint projects of discovery etc. Lee rhetoric, more dialog among the key stakeholders and better real-world education is the only real formula for success here.

One growing talent issue I have increasingly become concerned about, is observing people whose career development quickly nosedives when they isolate themselves in a work-at-home model.

I personally believe being able to work effectively within a virtual environment warrants a completely different skillset and attitude, if you want to advance your career and keep developing your potential.

So here’s my guide to being an effective virtual worker in six easy steps:

1. Use voice and video as much as you can. Staring into a computer relentlessly typing emails for 16 hours a day with little voice contact with your clients/co-workers makes anyone miserable – and anti-social over time. Make considerable effort to talk to people as much as you can. Use video for conference calls too – it forces everyone to pay attention (and get dressed) and have a much more personal series of dialogs.

2. Sort out your voice technology. There’s nothing worse than communicating with people who have a crappy wifi connection, with whom you can never get a clear skype/google conversation without the echos, constant disconnections etc. If your wifi’s garbage, you can get great quality Skype (for example) over 4g LTE these days on your iPad or iPhone. Oh, and while we’re at it, stop slurping coffee and eating into your microphone on calls, it’s disgusting…

3. Stop using email for every bloody communication. Email is a tool for passing along information and instructions. Learn how to be cordial, get your message across and use voice as much as possible to communicate. Never use email for heated conversations that have emotion (especially negative emotion).

4. Buy an exercise machine and work out everyday. Without fail. You’re sitting on your bum most the day burning zero calories and likely visiting the fridge on an hourly basis. You have to exercise, or you will balloon and die. Buy yourself an elliptical trainer, exercise bike or treadmill, use it everyday, and after a while you’ll get so fit you can even take calls while you get even fitter. I would recommend going to a gym, but who has two hours to carve out when you’re an overworked virtual nutcase glued to your machine all day and night?

5. Invest more time getting out to see your clients, your peers and do more networking. When you see noone bar your family, pets and the plumber on a daily basis, the only way to stay motivated and continue to develop yourself is to go to more conferences, make more effort to visit your clients / peers etc. You learn the most from your collective discussions with others, from having discreet conversations. Everyone’s fed up with social-media – meeting people and being social is back in vogue. Really – get out of the house!

6. Stop complaining about how stressed and overworked you are. Boohoo – just suck it up, we’re all over-bloody-worked. It’s all in the mind – so get healthy, get social again, start enjoying your work and you’ll forget about stress and go with the flow. Just go with the flow, it’s the only way to survive these days.

There endeth my lesson for the day. Go back to your weekend…

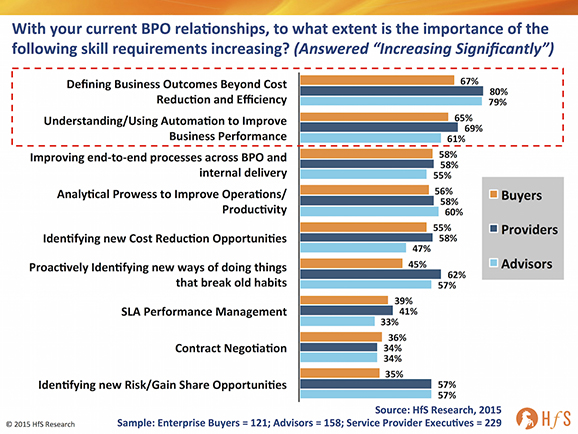

We’re shortly going to release the results of our new study delving into BPO talent, which probes into whether there is a genuine career path to follow for BPO and operations professionals, or whether we’re terminally stuck in the “accidental career” we never intended to venture into. In anycase, I wanted to share one set of data points that show which skills have been increasing in significance.

RPA has arrived as a core part of BPO’s future

Over the past year, the skill where demand and expectations has become the most elevated, more than any other, is automation. 65% of service buyers and 69% of provider professionals cite the need to understand and deploy automation is significantly increasing as a skill requirement – and even 61% of advisors are feeling the pressure to knowledge-up.

Essentially, as the room for additional cost savings diminishes for BPO buyers, the logical next step is to reduce manual tasks (and ultimately unnecessary labor costs). With the heavy marketing coming from service providers and technology firms offering robotic process automation (RPA) solutions, the awareness from the buy side – and pressure on operations managers – to have a more defined, measurable automation strategy, has never been as intense as it is today, and is likely to crescendo for some time to come yet. At HfS, we are getting calls every week from buyers wanting support developing an RPA plan for their business – it’s becoming the new efficiency drive for many experienced BPO buyers. Whatever actions buyers eventually take with RPA, they at least need to have some sort of strategy developing to placate the higher-ups questioning where their next 20% of productivity benefits are going to to come from.

The Bottom-line: RPA provides transformation baby steps for buyers wanting away from overdependence on labor arbitrage

RPA provides that logical first step for buyers and service providers to reduce their reliance on throwing lower cost human labor at problems. It provides the building blocks to develop more streamlined end-to-end processes, to perform more meaningful analytics, to create more of a digital infrastructure across the business. Essentially, RPA is the new arbitrage for many, but is unlikely to yield massive cost-savings in the near to medium terms – it is more about helping enterprises deploy their talent on higher value activities. In short, RPA is about working smarter, not cheaper.

Would you believe it? That quirky little research firm that started as a blog, at which many people snickered as a flash in the pan… reached 5 years old this week.

But we actually had a plan – and it was a five year one to break into the analyst mainstream and influence our services markets as much as any of the establishment analysts who’ve been around for years. Have we succeeded in doing that? I’ll leave that to you to decide…

I would personally like to recognize several characters who have played a part in helping HfS get off the ground and developing our reputation in the market as the destination for unvarnished insight, collaborative debate and plenty of entertainment: Esteban Herrera, Tom Ivory, Tony Filippone and Jamie Snowdon for having pride and faith in our mission and playing their part. Reetika Joshi, Charles Sutherland, Ned May, Mark Reed-Edwards, Tricia Bolger, Ned May, Pareekh Jain and Khalda de Souza for their ongoing support of the business and preaching the gospel – and putting up with me.

Fred McClimans, Bram Weerts, Hema Santosh and Barbra McGann for throwing their lot in with us recently to take us to a whole new level. And several friends (and family) who have been active in their support; Deb Kops, Lee Coulter, John Haworth, Sir Alan Fersht, David Poole, Jay Desai and many others. Also our early clients who have stayed loyal; Sarah Thomas, Shari Wenker, Mike Salvino, Ian Maher, Frank D’Souza, Stan Lepeak, Cliff Justice, Tiger Tyagarajan, Frank Cannata and many, many others. If I forgot to mention you, please forgive me as so many of you have been amazing with your support.

Now for our second 5 year plan…. what fun and games are in store for us next?

Happy Springtime all =)

Phil

Some fresh faced healthy looking chap in March, 2010…

Is your enterprise ready for what the future has in store for us?

This emergence of “As-a-Service” represents the most disruptive series of impacts to the traditional IT and business services industry that we have seen.

The globalization wave is peaking, and many maturing enterprise service buyers are struggling to find incremental value from the traditional outsourcing model, such as accessing more meaningful data, achieving better automation of processes, deploying end-to-end process delivery and accessing talent with creative business thinking skills. At the same time, service buyers need to keep driving down their operating costs to a minimum, with globally accessible technology platforms, based on common standards enabled by the cloud.

Looking at this next evolution of value, it is coming from technology-driven “As-a-Service” advancements that directly enhance employee, partner and customer effectiveness.

In short, the way service buyers receive services, and the way service providers sell and deliver them, is going to be very, very different in a few short years, and already some process areas where the technology is already available are being impacted.

At HfS, we have developed Eight Ideals of As–a–Service, that provide a guide for us all to follow as we look to achieving maximum value from our services in the future:

1. Design Thinking

2. Business Cloud

3. Intelligent Automation

4. Proactive Intelligence

5. Intelligent Data

6. Write off Legacy

7. Brokers of Capability

8. Intelligent Engagement

So how is your organization shaping up against these Ideals – and what is most important to you?

Whether you buy, provide or advise on business and IT services, your opinions and intentions are critical for our research, so please spend some time completing our study and you could win an Apple Watch.

Please note that your contact details will only be used for the purposes of sending you the optional executive report and entering you into the prize draw for the Apple Watch.

So please take our survey to air your views and experiences.

One of the main purposes of NASSCOM is to showcase the strength and direction of the Indian IT and BPO services economy. However, it’s not only about the heritage Indian firms promoting their strengths, it’s also a great venue for leading traditional Western-HQed service providers to brand themselves in India, to help them compete for the top talent.

One such service provider that’s made considerable strides in developing a major brand in India is Capgemini, whose staffing base has rocketed to 55,000 and made sure it had a very strong presence at the Mumbai showpiece this year. We managed to grab a side-bar with their dynamic CEO, Aruna Jayanthi, recently voted India’s third most powerful business woman by Fortune magazine, to talk a bit more about herself, her firm and her views on talent the future for India’s services economy…

Phil Fersht (CEO, HfS): Good afternoon, Aruna. Thanks for spending a bit of time with us today. Would you start by introducing yourself and how you got into this business?

Aruna Jayanthi (CEO, Capgemini India): I started with Capgemini 15 years ago. I now run Capgemini India, and before that I ran global delivery for our outsourcing business. I was part of the core team that setup India, and when I joined there were 80 people in India. Today, we are a little over 55,000 (couldn’t say this then due to impending results announcements – will be good to mention the new headcount number as this is current view).

Phil: 55,000. That’s a large number!

Aruna: It is a large number. But in the end, it’s not only numbers that matter; what matters is the value you deliver to your customers.

Phil: Right… so would you talk a bit about your career progression and how you ended up leading the India business for Capgemini?

Aruna: It’s a strange story, because twice in my life I was tempted to get out of the industry and do something else, but somehow I got back in. I started my career with TCS, fresh out business school. I got trained in programming and project management, did account management, the works. Then I thought, that’s enough, let me go try something else. And even though I did something completely different, I ended up in software for another in six years.

Then I decided to get into consulting. So I joined Ernst & Young in India, and within three months it was acquired by Capgemini. At that time, Capgemini didn’t have a presence in India, and the ex-Ernst & Young management consulting team became the core team that set it up and grew our offshore presence.

Phil: Traditionally, Capgemini has had a very strong reputation in Europe and in parts of Asia. And more recently, it’s been investing more in the U.S. and in India. And 55,000 is a big number, even though it’s not about the numbers. Would you talk about that operation and you know how it’s running? And, what do you think is making it successful?

Aruna: 70-percent of our business here is apps-oriented, and the rest is BPO and infrastructure-related services. And more than 90 percent of it is the traditional offshoring model. We do a little bit of work here for local Indian customers, but the bulk of the business is from customers in Europe, North America, and a little bit in Asia Pac.

What differentiates us in terms of value? We’ve managed to blend the India advantage and the local onshore advantage. That local touch is sensitive, it’s important, and we’re very strong with it in Europe and increasingly in North America.

Phil: Aruna, we spoke with several hundred services buyers for a study we’re producing. And the number one issue right now is talent and how to get more access to creative analytical capabilities, that sort of thing. How are you addressing that in India for Capgemini? What sort of people are you trying to hire? What’s the training strategy? What are you doing to try and stay ahead of the talent game?

Aruna: We’ve shifted our talent strategy in the past year and a half. Originally, we focused on lateral recruitment, meaning recruiting experienced hires from the industry. But in the last 18 months, we’ve started hiring far more fresh graduates.

The reason for it is twofold. First, there really aren’t many people already in industry that have experience in the new technology areas we want to build on. They just don’t exist. But I visit university campuses regularly, and look at the stuff they are doing in their labs. They have access to almost all the new technologies, as they get all the licenses at almost no cost. And the students are playing around with cool stuff, which is what we want. Of course, we continue with lateral recruitment when it’s appropriate.

That’s our shift in terms of where we get our recruits. The second shift is in terms of the skills we’re looking for. The Internet of Things, embedded systems, wearables, big data…now we’re focusing on analytics plus business skills. So while engineers were formerly our typical recruits, I think math graduates who have done a bit of business school are actually better.

Phil: So the theme of this year’s NASSCOM was “digital”, at a very high level. And an early takeaway of ours was that probably half of the service providers here get it. They know what’s happening, and they are figuring out what they need to do to get ahead of the curve. The other half they are like deer in headlights. How do you think India is going to make the shift, and do you think there is going to be some collateral damage on the way here?

Aruna: Phil – there is bound to be. My view is that when you look at digital, it’s not about technology. The role of the provider itself is changing. The question is, who understands the shifting role of the provider and how do they see it? Are we strong enough to understand the emerging digital agency, and the fact that if you are going to work on the customer side of it you better understand that side of the business? Is my role to write a program or code a system for somebody? Or is my role to provide a solution for a problem that they have?

So if I take the latter approach of it’s my job is to provide a solution that gives the customer value, then I start to look at building different sets of skills altogether, right? I would start to look at building more consulting skills, more domain skills. My job then becomes an aggregator or an integrator role, as opposed to a software developer role. And I think for me that’s far more important. Providers that understand that shift will do well.

Phil: So, if you were to look out five years to 2020, what do you think we will be talking about?

Aruna: I think we’ll still have a large digital element, but we won’t be talking software or applications anymore. The content will be far more business-focused than IT-focused. Also, I think the definition of the service provider will change. To me, the start-ups will become far more important, and it could be an aggregation of much smaller companies. We may even see a completely different set of providers.

Phil: One final question, Aruna. If you were crowned the Empress of the Indian services industry for one week, what would you change?

Aruna: I would change our positioning. Let’s use cars designed in Germany as an analogy. We talk about German engineering and how great it is, but we never talk about where the cars are manufactured (which I think is most often Mexico.) We just say it’s German engineering. What I would really aim for is that we say, “It’s Indian designed software” or Indian whatever. That’s the value that we need to rebrand ourselves to. It could be delivered from anywhere in the world. But the branding that we need to get to is that this is Indian IT. It is a solution conceptualized in India.

Phil: Precise and to the point, Aruna! Thanks for sharing your insights with our readers – it’s been great to meet you.

Aruna Jayanthi (pictured) is the CEO, Capgemini India. You can view her bio here.

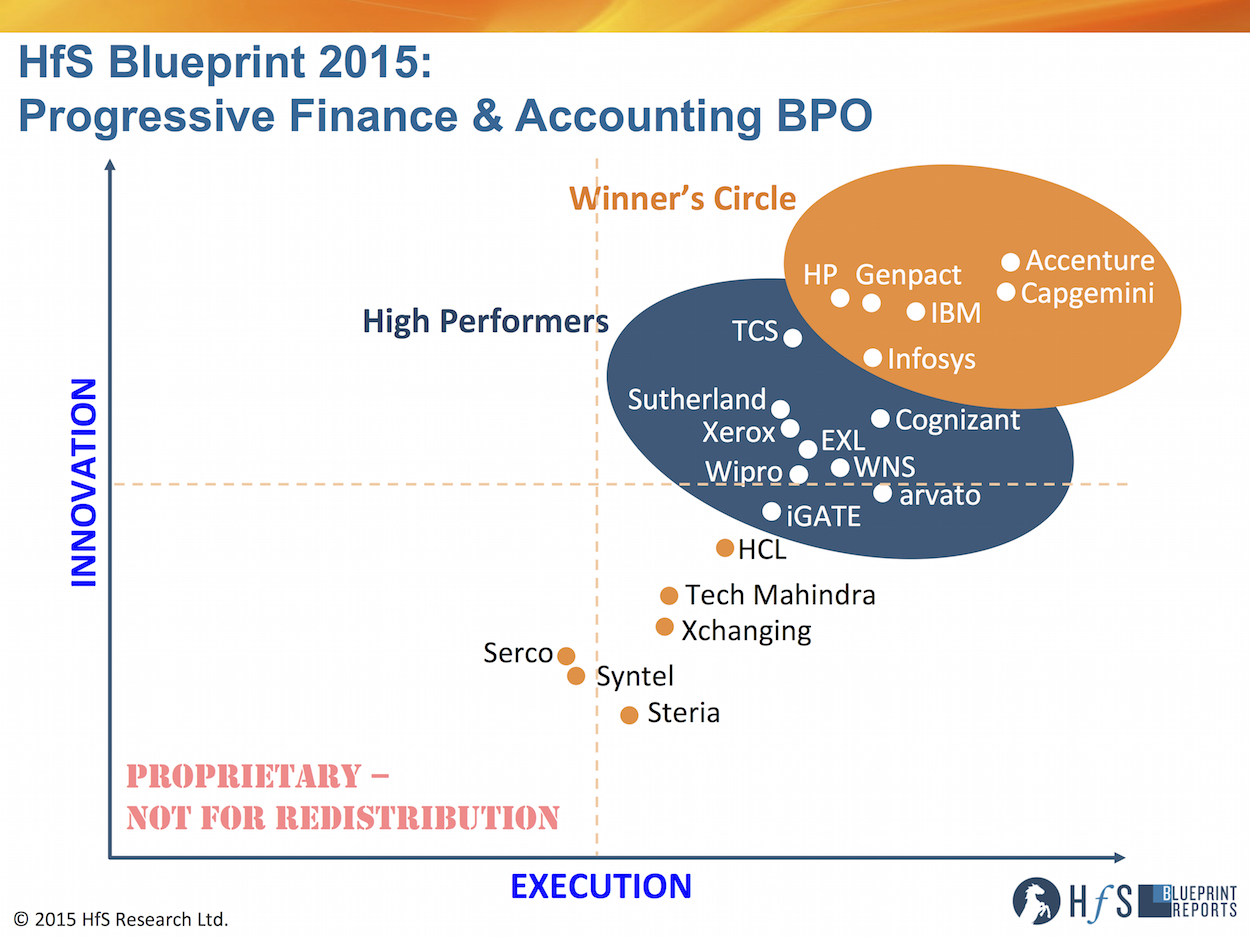

Almost two years to the day since we launched our first Blueprint Report, we finally circle back to the core horizontal services function providing the fulcrum for BPO and shared services: finance and accounting. For our 20th Blueprint, authored by analysts Phil Fersht and Hema Santosh, we deliberately focused on the proven “progressive” skills, investments, domain acumen and as-a-service potential of the leading providers in finance and accounting service delivery.

In order to pull together the most comprehensive view of this market, we created importance weightings for the key categories of services innovation and execution, that were based on the opinions of 1109 services buyers, advisors and provider executions in our 2014 State of Outsourcing Study, conducted in conjunction with KPMG. In addition, we conducted exhaustive interviews with more than 100 F&A service buyers, many of whom are members of the HfS Sourcing Executive Council. We didn’t rely 100% on reference clients ponied up from the service providers themselves – this is the genuine, unvarnished view of how providers are performing today from the people experiencing their services:

Click to Enlarge

So, Phil, what’s happening in the F&A space these days? Is the market slowing down as BPO services commodotize?

Not at all, one of the reasons why people hear about F&A “slowing down” is the diminishing role of sourcing advisors on F&A deals (only 30% of competitive F&A deals in 2013-14 were advisor-led, and 17% of sole-sourced used a advisor). A third of the deals were also sole-sourced, and very, very few were publicly announced. So the lack of “noise” causes people to incorrectly assume that activity in F&A is slowing down. In addition, we saw a lot more mid-sized businesses take the plunge for the first time, with 55% of F&A deals being signed up companies under $5Bn in revenues in 2013-14 – there have been many non-advisor-led sub-$15m engagements that pretty much flew under the radar in the last couple of years.

Net-net, total F&A BPO surpassed $25B in 2014, at a growth rate of 5%, with multi-process F&A BPO reaching $5B for the first time. Multi-process F&A BPO is expected to increase at 9% in expenditure in 2015.

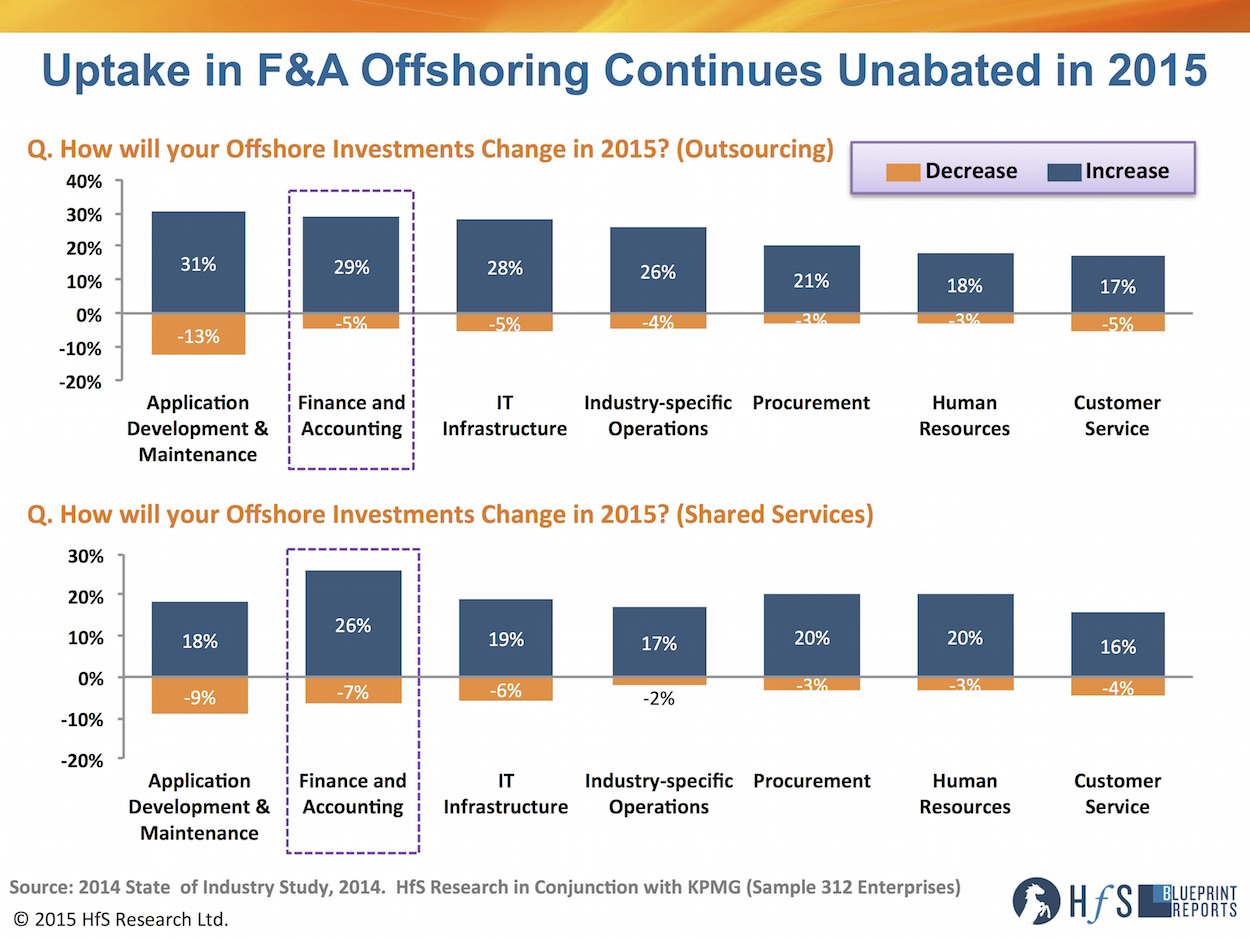

But isn’t offshoring slowing down? Surely buyers are pulling back from moving F&A delivery into offshore locations?

Stories of the demise of offshoring are not only premature, but wildly inaccurate. Our 2014 State of Outsourcing Study asked 312 major buyers of services their 2015 intentions to increase/decreasing offshoring, and close to one in three enterprises will increase their F&A offshore delivery for both outsourcing and (notably) shared services.

Click to Enlarge

This is indicative of buyers using their offshore in-house centers to house more controllership / high risk services they do not feel ready to outsource, but want to reduce overhead. Additionally, the increased scope in services that experienced buyers are outsourcing, such as F&A analytics, is increasingly markedly amongst some enterprise clients.

However which way you look at it, the offshore component of F&A is almost as popular as IT – and there is no slowdown in sight. While use of robotic process automation is being piloted by several F&A buyers, we’re still years away from firms being able to make significant reductions in labor as a results. F&A is a function which has, is and will be – for a very long time to come – dependent on people and talent. While buyers and sellers all want to leverage better tools and tech to streamline delivery and improve digital workflows, the change is more in the nature of work the delivery staff is doing than simply offloading them altogether. The game today is more about working smarter than simply cheaper..

Who’s winning the progressive game with the service buyers?

The most eye-opening shift has been the steady improvement of both HP and InfosysBPO to join the “Big 4” of Accenture, Capgemini, Genpact and IBM in the Winner’s Circle. We also saw real momentum, in terms of innovative delivery, from TCS, Cognizant and Sutherland and steady gains from both EXL and WNS.

I hope you all find the time to read our report that profiles each of the service providers, but there have been a few standout performances worth highlighting:

Accenture leads on partnerships with clients (Winner’s Circle)

Accenture breaks new ground with a formal joint venture with its long-standing client, Marriott, to go to market with BPO services to hospitality industry, where F&A outsourcing is a prominent offering. The firm increased its share of the market even further to 30% with its highly successful strategy of expanding its based of large enterprise (diamond) clients. The blending of F&A operations, infrastructure and close alignment with its shared services consulting has the firm leading the market in a time when clients need real consultative support.

Capgemini’s Global Enterprise Model is a world-class delivery platform for F&A services (Winner’s Circle)

Capgemini’s flexible, platform-based GEM methodology has all the aspects of progressive delivery covered from the right mix of FTEs, location mix, competency, technology, analytics, and governance. All key Capgemini clients attest real value from the GEM methodology. Capgemini has now emerged as one of the global market leaders with its laser focus and dedication to its F&A business.

Infosys wins big on account management attention and responsiveness (Winner’s Circle)

Infosys scores highly when it comes to the “listening” capabilities of their account management and delivery teams for clients. The firm are frequently cited as being easy to work with and highly responsive to the short- and long-term needs of clients of all sizes. Infy has shown a real hunger to grow their F&A business with multiple recent mid-sized deals that can be scaled in the future and a CEO who clearly sees the value of investing in his BPO business. The recent acquisition of automation tech firm Panaya (see link) could have major impact for clients struggling with ERP strangleholds in F&A.

HP leads with F&A Process Automation Tools and strong SAP-enablement capabilities (Winner’s Circle)

HP has been actively been driving the benefits of deploying robotic process automation for high volume, repetitive, rules-based work, and its AutoFlow tool for workflow meets the needs for clients tired of relying on legacy systems. Its recent number one rating in the 2015 Robotic Premier League is testament to HP’s strong automation focus in F&A. The recent restructuring of HP has been a positive for its F&A business, which has been better exposed to upper management as a genuine area of growth for the firm.

Smart Design and CFO focus from Genpact (Winner’s Circle)

Its dynamic ‘Smart’ foundation of Smart Strategy, Delivery, and Design are compelling and transformative, and Genpact’s tools have been backed by several customer F&A success stories. Moreover, Genpact is making investments in areas of F&A value to meet the needs of the CFO through its CFO Suite offering, under the leadership of Shantanu Ghosh, which could prove to become a major differentiator for the firm.

IBM drives innovative partnerships with clients (Winner’s Circle)

IBM continues to win over ambitious clients by hosting innovation discovery jams and workshops with its clients to understand pressing needs and create required solutions. There is strong future potential with its analytics and cloud offerings in F&A BPO. Its recent merging of GBS with GPS (BPO) delivery, could well craft a compelling proposition to the market, under the impressive leadership of Jesus Mantas, who is adopting the term “consult-to-operate services.” Mantas, a transformational consultative leader, understands the value of delivering the entire lifecycle of F&A services to clients – from process design through to managed steady-state.

Cognizant succeeding in moving from FTE-pricing to outcomes (High Performer)

Despite a smaller footprint in F&A BPO, Cognizant’s clients all cite the firm’s desire to move as aggressively as possible to outcome-based delivery of F&A, which is already working very effectively. Well positioned for the As-a-Service Economy and clearly one of the more forward-thinking innovative service providers in business services today.

WNS’ flexibility positions it well in today’s F&A market

WNS has firmly established itself as a strong “pure play” alternative to some of its larger competitors, winning against the top tier on several occasions. The firm is big enough to deliver and small enough to respond. Has received many positive accolades from many market clients for its hard-work and client focus. Also developing a strong reputation for it’s F&A analytics focus.

TCS’s vertical focus a strong potential differentiator for “As-a-Service” F&A in the future (High Performer)

Continues to believe – and invest – in strengthening industry knowledge, and investing in key leaders within industry segments who provide domain intensive guidance. Proprietary TRAPEZE Tools – available both in web-based and mobile versions provide compelling governance support in F&A. Its innovative approach to Robotic Process Automation in F&A has been lauded by some clients and impressed the HfS analyst team (see link).

EXL a strong all-round performer with a consistent transition and process improvement performance (High Performer)

The no-surprise transitions and managing change strategy works well with EXL’s clients. When operations are stabilized over the 12-18 month period, EXL shifts focus with its EXLerator process improvement methodology and collaborates effectively with clients for overall process optimization, target operating model, platform changes, business impact value drivers, and scope shifts. The recent appointment of Henry Schweppe is will help EXL compete for larger, more transformative engagements.

So, Phil, what is your prediction for what this market will look like in three years’ time?

F&A represents the perfect blend of “traditional” labor arbitrage and evolving “As-a-Service” delivery. Nowhere is more ripe for advancements in robotic process automation, analytics and outcomes models than F&A. The winners will be those which can maintain effectively their global delivery scale, but combine it effectively with the As-a-Service ideals, where clients can “plug-in” to the service provider experience, where cloud and automation are at the core of the offerings and designed with these in mind, as opposed to being retrofitted as an after-thought. However, people are still the key ingredient in F&A, and the market leaders are all differentiated not only by the scale – but the skill – of their delivery talent.

This market will continue to grow at an annual clip of 5-10% for several year to come – remember, it took the world of finance a decade just to make the jump from Lotus 1-2-3 to Excel. It’s going to take a while to get ahead of the As-a-Service curve!

HfS readers can click here to view highlights of all our recent 20 HfS Blueprint reports.

HfS subscribers click here to access the new HfS Blueprint Report, “HfS Blueprint Report 2015: Progressive F&A BPO Services“

Each year, most of the service providers like to bring together their multifarious assortment of “influencers” to pitch their capabilities, reinforce their strategies and make sure their key executives have some sort of relationship with the key people in their space who talk to their clients.

Having been in and around the analyst and consultant community for the last 20 years, these gatherings were typically 90% attended by industry analysts, namely Gartner, Forrester, IDC et al and a few small boutiques, independents, bloggers etc who mattered to them. Then, about five years ago, most the service providers had the bright idea of tacking on a handful of sourcing advisors who could also benefit from the same experience of being influenced. All of a sudden, these events have become about 60% advisor, 40% analysts. I think only Accenture and IBM are the only service providers left which actually separate the analysts from the advisors these days.

As a recent example of this, I had the privilege of attending Capgemini’s influencer day in an arctic Chicago last week. And I was impressed at the line up of legends attending from the sourcing advisory world – characters like Peter Allen (Alvarez & Marsal), Harvey Gluckman (ISG), Kevin Parikh (Avasant), Chip Wagner (Alsbridge), Peter Bendor-Samuel (Everest), Tom Torlone (PwC) – all accompanied by teams from their advisory firms. I have to hand it to Capgemini’s advisor relations team – no-one has ever assembled a gaggle of advisors together in one place quite like they managed. I then popped into WNS’ influencer day in New York and a similar line up ensued there… with additional SWAT teams from KPMG and Deloitte adding to the festivities.

This change in dynamics is having the following impact on the way these service providers interact with their influencers:

Pros

Much better questioning from advisors. It’s almost a relief to hear sensible, real-world questions from advisors during these sessions. Long gone are those days when you’d get analysts piping in with their drawn-out abstract thought-patterns, which actually were never really supposed to be questions, more statements of how clever they were.

Advisors are much more social. Most the advisors like to network – even with their competitors. Always good to exchange views with (some) them over a glass of wine. Most analysts just disappear to their hotel rooms at 8.30pm, never to resurface.

Advisors have more energy and passion. Most of the advisors enjoy what they do – they are passionate about services and are hungry to learn more. Most of the analysts have been doing this for decades, are clearly jaded and exhausted by these dog n’ pony shows, and are just going through the motions these days.

Cons

Advisors have become quasi-competitive with most service providers. As the outsourcing service providers look to move further up the value-chain with their client engagements, they are essentially offering the same services as most the advisors. All I hear from the leading advisory firms, today, are how they are running consulting practises in digital transformation, robotic process automation, CFO services, GBS etc. These ambitious advisors want service providers who are only really focused on the efficiency-driven services further down the value stack, so they can profit from the consultative and governance-driven services they can layer on to their clients’ outsourcing engagements. However, the more complex clients’ needs are becoming, the blurrier the line is becoming between what service providers and advisors deliver.

Advisor “influence” is much harder to track. With analysts, the goal for service providers is simple: dazzle them and hope they will write about them to their readerships and social followings. Tracking their influence is easier when there is a tangible outcome, such as a piece of research or a blog post. Most advisors won’t write anything – even with a gun to their heads. The service providers simply hope the advisors are moving them up their evaluation curves and pushing more deals their way.

Most advisors with deep client engagements do not have time for service provider days. Having been on the advisor side myself, I can tell you that I never had the time to take entire days out to hobnob with service providers, unless I had a lucky week of break-time in between client engagements. Most of the advisors who do have the time for these service provider influencer days are clearly the executive-level leaders not so ensconced with the day-to-day execution of advisory services. Hence, the service providers are hoping this bedazzling of the advisor leaders is somehow translating its way to the advisor deal teams doing the site visits, service provider selection sessions etc.

The Bottom-line: The influencer model is clearly broken in the services industry – a new breed clearly needs to emerge that advises, analyzes AND influences

In short, the evolving confusion over advisor and analyst roles is a result of the lack of real influencers in the industry – experts who not only talk to buyers on a daily basis, but also share real insights and leverage data for them. In today’s world, advisors and analysts are very different animals – and the winners will ultimately be the ones which can fuse together the two worlds.

One growing talent issue I have increasingly become concerned about, is observing people whose career development quickly nosedives when they isolate themselves in a work-at-home model.

One growing talent issue I have increasingly become concerned about, is observing people whose career development quickly nosedives when they isolate themselves in a work-at-home model.

Phil: So, if you were to look out five years to 2020, what do you think we will be talking about?

Phil: So, if you were to look out five years to 2020, what do you think we will be talking about?