Our latest research into intelligent operations reveals a customer first strategy is the biggest driver for C-Suite leaders today, so where more important to focus than what’s going on at the call center? Has there ever been a more compelling time for call center service providers to step up and prove to their clients they can do a whole lot more than execute basic customer services?

Call center services have matured significantly in recent years, where you can find a plethora of providers doing a masterful job managing resources all over the world to deliver affordable voice services – but choosing between them has often never been so difficult. However, with the need for so many enterprises to focus on the omnichannel customer experience to differentiate themselves, we’re now in a critical bake-off between those call center providers delivering real customer value versus those still walking the treadmill of proving legacy voice services at ever-cheaper rates. Plus, we still have many enterprise buyers who squeeze the life out of their providers on cost, and then expect the provider’s A team to show up. Hence, there is a fine balance between the value clients need, the investments they are prepared to make to achieve this value, and the ability of smart providers to invest in As-a-Service models that take advantage of talent, digital technology and automation to deliver high value, without huge increases in headcount investments. Sounds easy, right?

In this vein, we’re excited to announce the release of our first Contact Center Operations Blueprint, authored by HfS Research Director and contact center veteran, Melissa O’Brien, the only contact center analyst who’s actually lived in the Philippines running a call center operation herself. Melissa’s been exploring the cluttered competitive landscape, talking to a huge number of clients and leading providers, to help shed some light on the competitive landscape and where this market is truly heading:

(Click to enlarge)

Melissa, please give us a flavor for the current state of the contact center operations market

This is a market undergoing a pretty dramatic transformation, in part due to increasing end-customer expectations – ambitious service providers are looking for ways to continue delivering operational excellence, while adding value and innovating to meet the expectations of their clients’ increasingly digital end-consumers.

In the past, contact center service providers were valued for providing basic interaction services at a lower cost. As enterprises are more often now looking at the contact center in a much more strategic way, they are putting greater scrutiny and expectations on their service providers, looking to them to add value to their customers’ experiences. Forward-thinking contact center service providers are not only aiming to help clients support customers using newer channels, but also to provide thought leadership and platforms that facilitate an “omnichannel” view of the customer, which includes consulting capabilities to design the customer experience, and actionable analytics that support predictive and proactive decisions with customer interactions.

These providers are embracing the opportunity to deliver value beyond cost reduction, by transforming the contact center to an engagement and profit center with sales through service, increased levels of CSAT and customer loyalty. This has a profound impact on the needs for contact center talent, generating a major shift in the mentality and approach to recruitment and retention in contact centers.

Melissa O’Brien is Research Director, Contact Center and Omnichannel Operations, HfS (Click for Bio)

Despite these new dynamics, scale, flexibility and vertical expertise are also still key buyer requirements in the contact center space. Buyers commented, “it is their job to know the industry and help me figure things out”, and “we view contact center staffing like Uber when we need a ride.” Service providers are addressing these needs with flexible workforce solutions such as work-at-home agents, and with workforce management and optimization tools. Robust and holistic security measures are also incredibly important, especially considering some of the contact center security disasters that have been very public in the last few years.

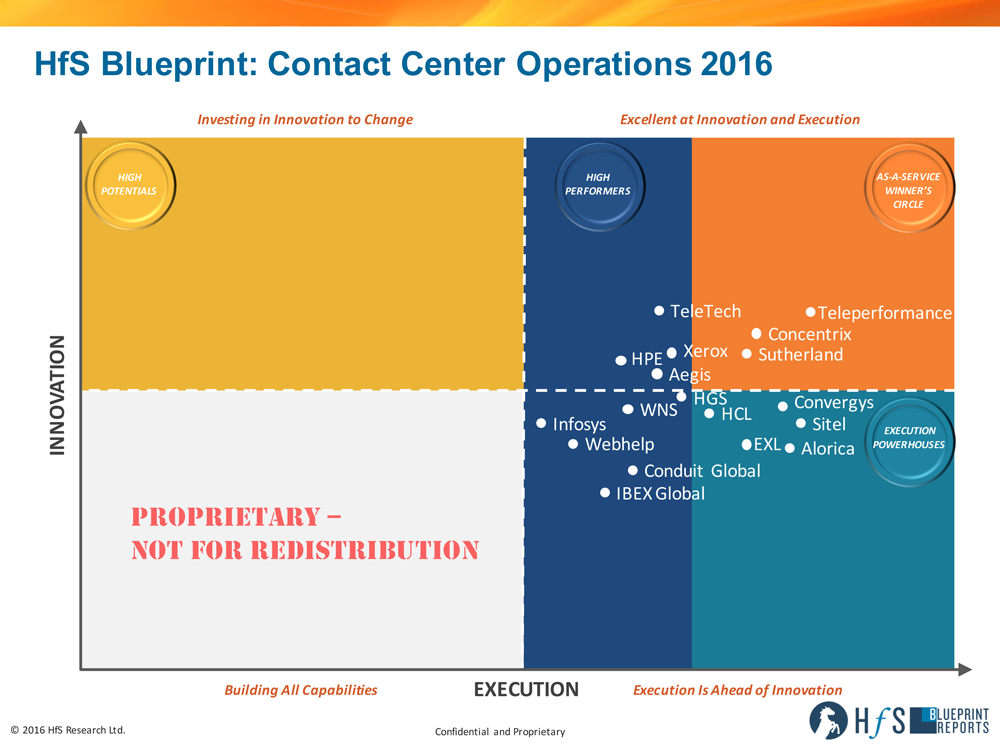

We covered 18 service providers in this Blueprint and interviewed many of their customers. One thing that struck us was that almost all of the buyers we spoke with were very pleased with account management and the execution of ongoing operations, but, on the whole, buyers found innovation and proactivity lacking, even in the leading service providers.

There was a frequent disconnect between the service provider stories of innovation and the unvarnished client feedback from many of the reference calls. Despite many of the provider-offered case studies, most of the reference call discussions with buyers were examples of FTE-based engagements, heavily focused on traditional channel interactions. Clearly, this is a very mature market for servicing basic interactions on traditional channels, however, real life examples of omnichannel capabilities are few and far between. We are going to be doing a deeper dive on the Blueprint participants that are really implementing new channels, embracing automation and more advanced analytics in our upcoming “Digitally Enabled Contact Center” Blueprint.

Who are the leading service providers in this market today?

Teleperformance, Concentrix and Sutherland landed in our As-a-Service Winner’s Circle. Teleperformance is, by far, the largest provider in this space in both headcount and revenue, growing at an above industry average rate, and continues to invest in research and thought leadership to stay ahead of the game. Both Concentrix and Sutherland stood out for their endeavors to embrace the As-a-Service ideals, with Concentrix attempting to help clients write off legacy with technology partnerships and Sutherland demonstrating a real focus and vision for omnichannel customer engagement. One other common theme for the As-a-Service Winners Circle leaders was an effort to embed Design Thinking in client relationships.

Each of the High Performers are approaching the market in innovative ways as well. Aegis, HGS, HPE, TeleTech, and Xerox are all working toward an omnichannel vision with clients. Conduit Global and IBEX Global both have solid execution and approaches to talent. Infosys, WNS and Webhelp are all broaching automation in unique ways.

The Execution Powerhouses demonstrate strength in delivery execution, with Alorica, Convergys and Sitel boasting excellent talent strategies, and HCL and EXL performing well with solid account management and a focus on moving up the value chain.

Moving forward, Melissa, what recommendations do you have for ambitious contact center service providers?

Contact center service providers must have their thought leadership and innovative ideas front and center of everything they do. Even many clients of our As-a-Service Winners complained of a dearth of innovation and proactivity. Buyers are no longer expecting providers merely to meet service levels—they are expecting insight and leadership as well, not just for process improvements, but also ideas around the bigger picture of improving customer experience. This can lead to better, and ultimately, expanded relationships.

We also think there is real potential for Design Thinking to have a profound and positive impact on relationships in the contact center operations space, especially as it relates to the customer experience design needs, such customer journey mapping. Almost all the clients we spoke to scored their providers well in collaborative engagement, but Design Thinking presents an opportunity to take that collaboration to another level—and it just fits so well with the present needs of omnichannel design and customer journey mapping. Embedding Design Thinking into client/provider relationships can help facilitate ongoing discussions between (formerly) siloed groups to re-imagine business models that embrace digitally-enabled contact center operations. The leading service providers are starting to step up and embrace Design Thinking, but we need to see more focus on outcomes that have an impact on clients’ business. We also need to see Design Thinking embedded in the way call centers engage with clients from the outset, as opposed to a project-based billable consulting service. You don’t buy Design Thinking – it is a mindset change that focuses everyone on defining, prioritizing and achieving desired outcomes.

Most importantly, and something that the leading service providers understand well, is to continue to invest in and evolve a robust talent strategy. With all the movement toward self-service and all this talk about automation, people will still remain the most important part of the contact center, whether by designing customer experiences, analyzing customer behavior and demands, or having higher value real conversations. Contact center service providers need to work toward writing off the industry legacy brand, both as providers and employers. In order to do this, service providers need to change the perception of the industry, offering enticing career paths and focusing on analytical talent, and continue to increase strategic importance to clients. The service providers that can help their clients find the right balance of talent and technology in an omnichannel vision will be the future leaders in this market.

Soon there will be nowhere left to hide. Everyone’s value is under the microscope from colleagues and management alike. Whether you turn widgets, manage a process, a set of processes, lead teams or manage team leaders leading teams… or run a whole division… or even an entire organization, you are under constant scrutiny in today’s open workplace.

Everyone has to prove they are useful, add real value and are worth their salaries… or they are toast. But most importantly, people need to prove they can be trusted. Employee trust in today’s workplace is about proving you are doing more than just enoughnot to get fired.

Loyalty is legacy

Most heritage enterprises no longer want to give out gold watches for your turning up everyday for last 30 years… I mean, “thanks for showing up and coasting here for 30 bloody years and making it really hard to fire you”. I don’t think so… Loyalty means little, but value means everything. The more legacy work we automate/digitize, outsource, replace with software, or just write-off, the more we have to focus on our human skills to justify our existence in today’s workplace.

Tomorrow’s successful workers are those who use their initiative to perform activities, on their own volition, to find new value for their enterprises. You can’t get any progress or value from methods like Design Thinking if your staff are only checking the boxes to perform their rudimentary employment functions. Design Thinking is about going beyond the norm to challenge the status quo, to think outside the boxes, not just checking them.

You are who you are – your reputation is everything, your ability to forge relationships with colleagues, peers, industry influencers and company leaders who appreciate your value, your perspective and your personality is, really, all you have. The days when you could get away with hopping from job to job because you were great at bullshitting your way through interviews are dying – any employer with half a brain isn’t recruiting through traditional channels any more. It’s all about people engaging with people who have established a reputation for adding value, going beyond the basics, and being great to work with.

You need to find new problems, not just solve old ones

But adding value is not just about solving known existing problems, it’s about finding new ones to solve in the future. You can always find a contractor or an outsourcer to fix a broken set of processes, or correct lines of badly written code. But finding people which can challenge whether those processes or lines of code are even still relevant to meeting your desired outcomes… people who care enough about their jobs and their company’s success to go beyond performing “just adequately enough not to get fired” is the secret sauce for future value. And that is what new workforce trust is all about – initiative, attitude, personality and trust.

The Bottom-line: There is no secret sauce to staying relevant – it’s about putting our egos aside and becoming students again

Frankly, I’m sick and tired hearing about “Digital Skills” and “Creative Capabilities” being some far-flung capabilities which you need to go to Millennial school to develop (whatever that is). Digital skills are about understanding your customers’ current experiences and intelligently leveraging every traditional, social and mobile channel touching your business to make them richer. Creative capabilities come from collaborating and challenging yourself with your colleagues and partners.

So correct me if I am wrong, but being successful today is about using capabilities we already have. It’s simply making ourselves students again, finding that hunger to learn about what’s out there and engaging with everyone around us to prove and challenge our theories. We must ditch this sense of entitlement that dictates we don’t need to go back to basics and force ourselves to think, collaborate and learn all over again – or we’re going to be done before we know it.

Enterprises need to behave like start-ups, where their people group together for the common cause of making their collective group successful – only willing collaborators with a desire to learn and challenge need apply. We’re all part of the Digital Generation – we just need put our egos to one side and own up to the fact we’re all students rediscovering what we’re all about and what we’re capable of…

Growth in offshore-dominated services may be slowing for traditional IT support services, but for multi-process Finance and Accounting (F&A) services engagements, 2015 saw the market continue to grow at a 10% clip.

Why? Because F&A outsourcing is about 10 years behind IT outsourcing – in terms of adoption – and is a market that can quickly take advantage of more experienced governance executives, capable service providers that have ironed out many of their past mistakes, and notable advances in analytics, robotic process automation (RPA) and digital technologies.

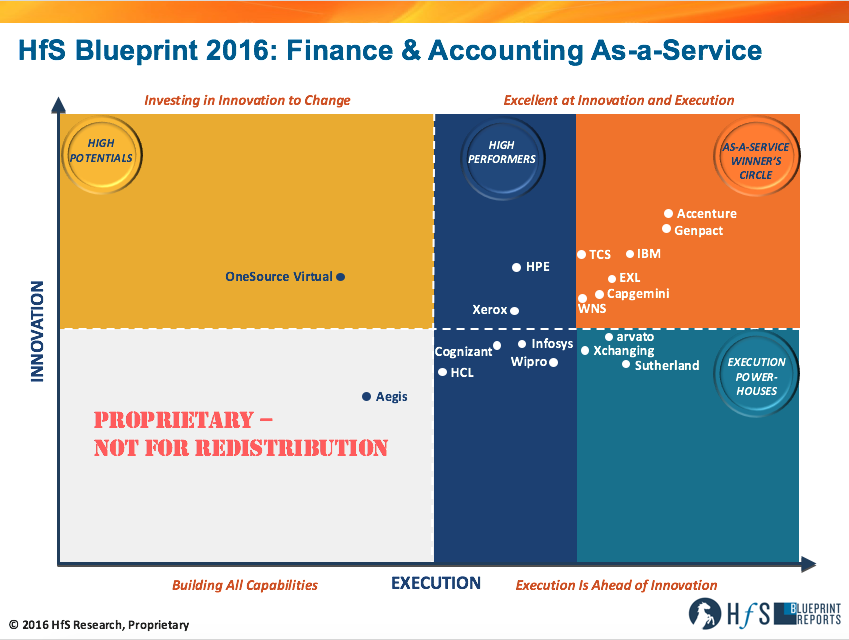

In short, the shift from enterprise clients approaching F&A engagements largely as a labor-obsessed cost-driven solutions towards outcomes-centric value-obsessed solutions, is now really happening. Yes, we’re finally starting to talk about F&A being delivered “As-a-Service”. To this end, for 2016’s F&A Blueprint, which covers over 1500 multi-process F&A relationships, we’ve reoriented the performance innovation and execution scores to reflect each service provider’s alignment with the HfS As-a-Service Ideals:

Click to Enlarge

So, what’s new about this year’s F&A Blueprint?

We’ve gone deeper than ever before in really getting to the essence of buyer/provider F&A relationships. In the past, we were as guilty as the rest of the industry of focusing too much on engagements being operationally effective, when we should have placed even greater emphasis on the measures being taken by both service providers and buyers to evolve beyond meeting the decimal points in service levels, the obsession with legacy methods like Six Sigma, and the fact that achieving adequate delivery and meeting cost budgets, were considered the only desired outcomes.

“Innovation” has previously been focused more on future plans and investments (as, let’s face it, there really hasn’t been a lot of genuine innovation in F&A BPO). We’ve grown tired of people describing future models of what great looks like, and, instead, are focusing on the current willingness and commitment from service providers to work with their clients to break from the legacy mindset of preserving obsolete processes and technologies to meet prehistoric metrics that were agreed in a bygone era when cost-savings from offshoring of labor were the watchword.

In this vein, we conducted exhaustive interviews with F&A service buyers to align their current service provider relationships with the Eight Ideals of Being As-a-Service; we really put the emphasis on buyers and providers changing how they behave with each other, their appetite and mindset to start writing off their legacy processes and technologies:

Click to Enlarge

Why are some service providers being more “As-a-Service” with their F&A clients?

When you talk with most the service providers today, they are all claiming they are:

a) Willing to cannibalize existing revenues to invest in the As-a-Service delivery model;

b) Willing to share risks and gains with clients;

c) Willing to shift away from FTE pricing and move to consumption-based models with built-in outcome pricing.

The reality is that these claims are only really happening with a small handful of service providers – and only with some specific clients which are willing to have a deeper, more collaborative and trusting relationship. The most common claim from clients is that many have been stuck managing a certain number of FTEs for several years, and their service provider has no incentive to reduce that number, as that is how they get paid. There are instances where service providers are very willing to invest in robotic process automation on their own delivery staff resources, but are unwilling to pass on these productivity gains to their clients.

Essentially, F&A outsourcing is caught in two worlds – preserving legacy and embracing As-a-Service:

1- Preserving legacy. Most service providers are far too comfortable maintaining margins with legacy engagements. The sad reality of legacy F&A BPO is there are hundreds of engagements, signed over the last decade, based purely on an FTE cost model, where the service provider is paid for managing a set number of people; reduce the headcount, and its profit margins go down. What’s happening here, is when these deals come up for renewal, many clients are pushing for new productivity gains, only to find their service providers unwilling to take margin hits, unless there is a true competitive situation. Unfortunately, for most clients, it’s hugely costly and complex to swap out an incumbent F&A service provider – and finding a willing competitor to invest in their business can be enormously challenging. It’s much harder to develop a competitive mix of providers in F&A than it is in IT, where we’re dealing with complex people and processes issues, not commodity application support. We’re going to need to see some truly disruptive offerings from ambitious service providers to change the model here, such as Robotics-led BPO, however, this also means service buyers must entrust their providers with more intimate data access.

2- Embracing As-a-Service. Ambitious service providers going after greenfield F&A opportunities with automation and analytics front and center. Many of the new deals being negotiated are where the As-a-Service action is much more prominent. Service providers are much more willing to invest in new opportunities, than make sacrifices in existing engagements. We are now witnessing the emergence of automation-led human augmentation solutions, where some deals are partially funded by the expected headcount reduction and productivity improvements over the course of a multi-year engagement. We believe this will be especially relevant in F&A contracts, which form the baseline of the BPO market today. However, buyers need to be much more willing to enter into deep collaborative relationships with their service providers, where they stop forcing their providers to only access their systems using Citrix, which limits the effectiveness of RPA overall and encourages an “us versus them” mindset between buyer and provider. Both parties cannot enjoy the full benefits of RPA and Intelligent Automation, without genuine collaborative engagements and a holistic security model that aligns the capabilities more effectively. In addition, greedy buyers need to stop treating RPA like legacy offshore BPO and demanding all the productivity savings up-front, before the RPA benefits have been formalized – and without realizing that RPA often drives up service provider costs in the short term for increased testing and QA.

Who are the standout performers for F&A As-a-Service?

The outstanding two service providers are Accenture and Genpact. Accenture leads the market in terms of sheer size and scale (we estimate its annual F&A BPO revenues now exceed $1 billion), and has made considerable investments in its analytics and RPA capabilities. Most impressive are its on-demand FP&A apps that really create an As-a-Service mindset for its delivery staff and clients. We would like to see a mid-market approach to emerge from Accenture in this space, considering its As-a-Service approach and ability to plug new clients into its massive global delivery model.

Genpact has really re-emerged in the market over the past 18 months, winning a host of new deals which have deep commitments for future productivity improvements through RPA built in. The firm has also made good progress evolving relationships with existing clients which were originally signed up in the legacy lift-and-shift model. Its focus on LeanDigital and CFO consulting has helped the firm move up the value chain with a proven reputation for consultative process capabilities. We do hope, however, that Genpact can stay more consistent with its offerings in the future, as it does have a habit of confusing the market with too many product launches, using too much jargon.

IBM‘s Global Business Services team has convinced the industry it is still very committed to F&A, and is aggressively looking to embed Design Thinking and Intelligent Automation into its engagements. It’s commitment to RPA and cognitive could be huge differentiators for the firm as it embeds these into its engagements – and Watson’s “Buying Assistant” tool signals the potential of further expansive cognitive capabilities for F&A. We would, however, like IBM to embed its technology portfolio better with its F&A offerings – too often they come across as standalone tools.

EXL makes winners circle in F&A for the first time with a genuine top-down determination from its CEO to embrace the ideals of As-a-Service. The firm is a real example why some mid-size service providers are adapting much better to As-a-Service than some of the monolithic Tier 1’s – it can scale down to pick up mid-market engagements and is big enough to play at the big table. EXL also has a genuinely collaborative client centric approach which really helps it deepen relationships in areas like process improvement and analytics – and has stayed true and consistent to its product offerings over the years, with EXLerator, for example, effectively supporting process improvement for several clients. We would like to see it build on its nascent RPA capability with its recent partnership with Automation Anywhere.

TCS also makes its first F&A winners circle, with a determined focus on RPA in O2C and P2P processes. TCS is proving highly determined to prove the RPA model to its clients by taking risks and making revenue sacrifices. Moreover, its diverse portfolio and vertical depth in BFSI, manufacturing and utilities are starting to bear fruit in F&A. We would like to see the firm clearly articulate its overall focus and mission moving forwards, as TCS currently has so many initiatives in areas such as automation, cognitive, digital etc., that it sometimes comes across as a confederation of multiple businesses than one integrated enterprise.

Capgemini continues to be a leading F&A provider with its renowned global process model and real focus on operational excellence in finance delivery. Moreover, its acquisition of IGATE could deliver real potential for the firm’s “As-a-Stack” approach to F&A by marrying IGATE’s ITOPS platform and bringing much-needed vertical industry depth. We would like to see greater urgency and focus on integrating the BPO components of IGATE and the firm would also benefit from increased focus on analytics.

WNS makes up the winners circle – also a first-time entrant – with a very effective outcome-based pricing approach and CFO framework, popular with many clients. Not unlike EXL, being a mid-sized provider is playing to WNS’ advantage, with its aggressive sales approach and client-first mentality. We would like to see WNS expand its footprint further – both geographically and vertically – as the company continues to grow and perform well in the As-a-Service era.

Other standout As-a-Service performers include: Sutherland, which has quietly won some impressive new deals and has been an early mover with RPA; HPE‘s well articulated approach to RPA; arvarto‘s order-to-cash focus; OneSource Virtual‘s entry into the market with it’s Workday model and RPA-native development environment; Infosys‘ unique focus on Design Thinking; Wipro‘s deployment of it’s Holmes platform in processes such as AP and fraud detection.

And finally, what developments can we expect to see in this market over the next year?

Two Ideals are dominating the F&A As-a-Service space – Intelligent Automation and Actionable and Accessible Data, and I expect these to continue to differentiate the service providers. While I see capabilities around RPA becoming fairly commonplace in the coming months, the ability to support the data underbelly for the finance function will come to the fore – and clients will need to let their service providers into their intimate systems and data repositories for them to be truly effective together.

With all this pressure coming from the front office to embrace digital business models, the onus is moving to the middle/back offices to keep pace with the changes happening at the business end of organizations, with the finance function being the fulcrum for future agility and responsiveness to market conditions. I also believe we will start to see Design Thinking start to emerge as a methodology for buyers and providers to make the shift to As-a-Service, and the finance function is a place where many organizations need some serious re-imagination if they are ever going to break from legacy habits.

This market has a long way to go, and the real work of making the shift to As-a-Service is still in its very early days.

HfS readers can click here to view highlights of all our 37 HfS Blueprint reports. See our plans for 2016 Blueprints here.

HfS subscribers click here to access the new HfS Blueprint Report: F&A As-a-Service 2016

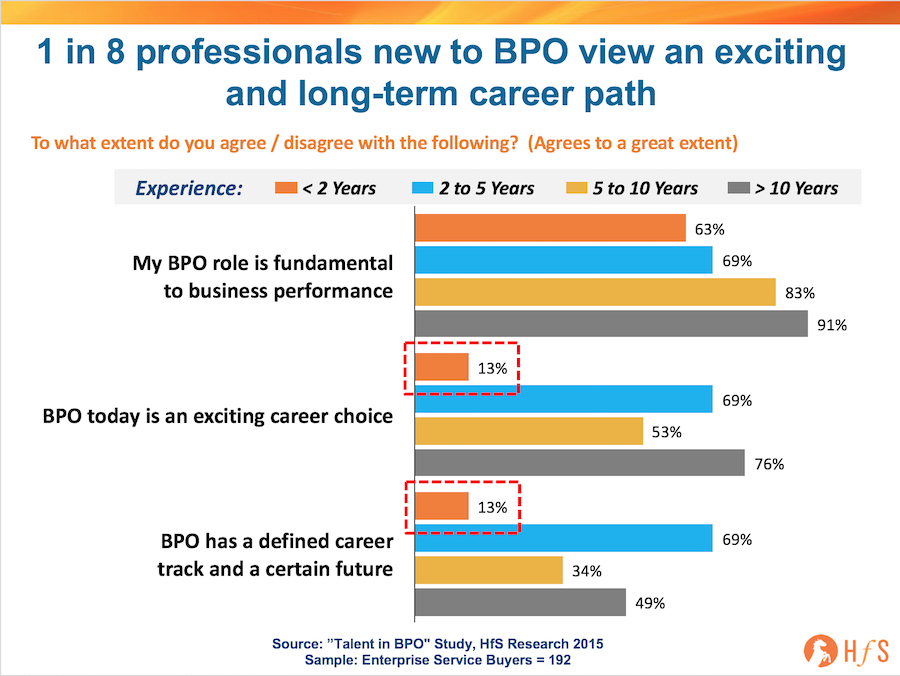

When your enterprise is increasingly dependent on hiring “Millennials” with digital skills and lower wage needs, you’d better figure out a plan for creating exciting, challenging career paths, or you’re pretty much already doomed.

Sadly, our Talent in BPO study from last year tells a very depressing tale when you ask BPO delivery executives what they think of their BPO career:

Click to Enlarge

What’s alarming is the failure of enterprises to create and communicate a viable BPO career path for seven-out-of-eight professionals with under two years’ experience. And – while 63% of newbies strongly agree their job is vital to business performance, a depressing one-in-eight are actually excited by their career choice. When people get past the first couple of years, their experience clearly improves, but the concern here is how can we attract top (or even middling) talent into BPO careers, when there is such a negative perception of the potential of the job. If we can’t attract the talent, the industry will never progress beyond a cost/efficiency play.

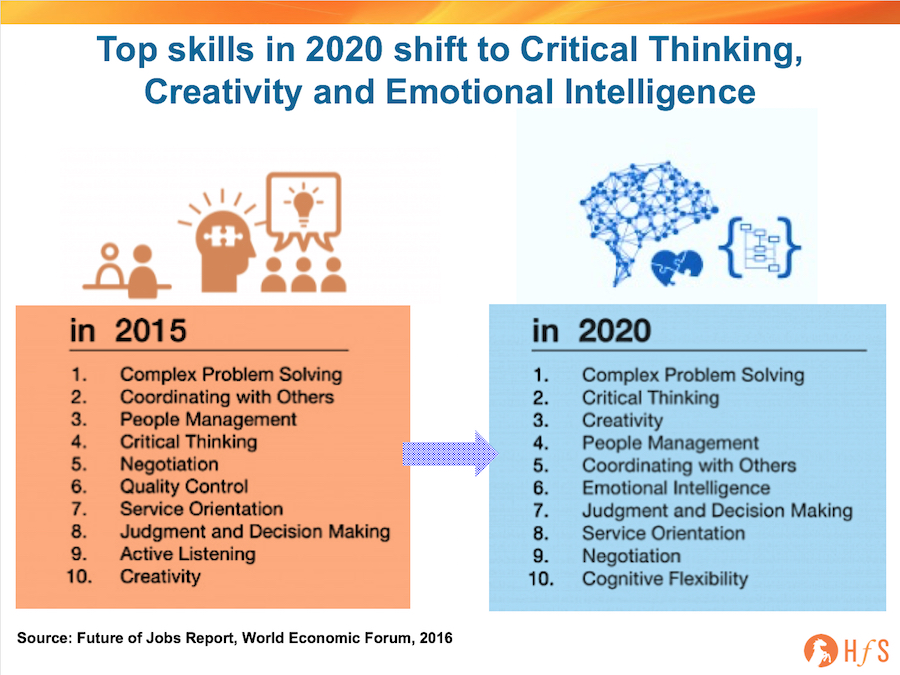

What can we do to attract the “Digital Generation” into the BPO business?

Start new hires on activities that require creativity and critical thinking. Working in BPO has to be about delivering capabilities beyond rote, operational processes. Today’s college graduates are simply not coming out of school willing to perform mundane routine work. Just look at the new WEF jobs report to see how skills requirements are quickly shifting, as business needs evolve – especially the need for creative skills, going from number ten to number three in merely five years:

Click to Enlarge

In the past, for example, an accountant would often earn his/her chops processing accounts and doing routine GL work, before progressing to controllership activities, such as budgeting, quality audits, FP&A, forecasting and risk assessment work. With much better technology and offshoring available, the days of people doing highly-automatable / offshorable processes are fast dying. Everyone knows they will be irrelevant in the future if that is all they do.

Operations staff proactively need to support the fast-shifting needs of the front office. So the focus needs to shift towards creating a work culture where individuals are encouraged to spend more time interpreting data, understanding the needs of the front end of the business and ensuring the back/middle office can keep pace with the front office. This is especially the case in industries that are more dependent than ever on real time data, using multiple channels to reach their customers and being able to think out-of-the-box with disruptive business models. Sure, we all need to make sure we can keep the operations functioning by paying the bills, responding to customers, processing the claims etc, but if we can’t be proactive and look at how we can create a better customer experience using digital channels, or challenging the logic of running a process a certain way, we’ll never create work cultures that will attract the bright minds to take us forward.

Driven managers, multidisciplinary teams and flat structures essential to drive collaboration and Design Thinking. People want to feel a part of something and that their work matters – and the best way to do this is to move away from rigid corporate structures of the past, with too many management layers and departments run siloed like mini-empires. Both buyers and service providers need to invest in driven managers which understand how to motivate and collaborate across business functions. Sales, marketing, customer service, IT, finance, HR and supply chain are functions that all depend on each other to be effective. Smart enterprises are already breaking down the silos and creating multidisciplinary teams, using collaborative tools and Design Thinking methods across delivery centers to help their staff be more motivated, creative and challenge the old way of doing things.

The Bottom-line: Enterprises need to create broader “business manager” roles to challenge the Digital Generation

Beyond just moving up the ranks, there is a certain clout attached to becoming some kind of subject matter expert, taking pride in the ownership of a certain area of expertise. In my viewpoint, there should be two roles for BPO staff in their first two years: associate business manager leading to business manager. This individual needs to oversee a process, or set of processes, with the task of constantly seeking out ways to do things better by interpreting data, collaborating with colleagues and service partners, delighting customers and understanding the business. The onus in on the operations leaders to appoint and train team leaders to inspire junior staff to take ownership of their areas and not feel like “back office” process jockeys.

This blog could have been the start of a very long book about how “Businesses should be Designed for the Digital Generation” but instead is a starting point for how we can rethink operations jobs to attract better talent and deliver much more value beyond merely keeping the lights on. These may be early days, but if today’s business are not already thinking this way, they could already be doomed…

Shantanu Ghosh, SVP CFO Services and Consulting, Genpact (Click for bio)

Digital, digital everywhere, but what about the finance function? It took a decade for accountants to make the seismic shift from Lotus 1-2-3 to MS Excel… so how much focus is our favorite business function putting on today’s advances in analytics tools, interactive and collaborative solutions, mobility and automation?

Can finance executives really embrace digital to break away from some of the legacy mindsets, processes and technologies that have plagued the function for decades?

Not too many people have been driving the digital agenda as aggressively with the CFO’s office than Genpact’s Shantanu Ghosh, with his firm’s own methodology “lean digital,” so we thought it high-time we caught up with him to get his viewpoint on the impact of digital o the finance function.

Phil Fersht, CEO and Industry Analyst, HfS: Shantanu, it’s been a couple of years since we’ve had you on here. Can you tell us a bit about what you’re up to in Genpact today?

Shantanu Ghosh, Senior VP & Business Leader – CFO Services and Consulting, Genpact: Actually, my remit remains pretty similar to what it was two years back. I lead the financial accounting, sourcing and procurement service lines, globally. I also lead consulting across Genpact.

But I’ll tell you, the complexities, the scale and the type of solutions involved in all three have changed pretty dramatically in the last two to three years. So it feels like I’m doing a new job every day, even though broadly the remit remains the same.

Phil: I’ve seen Genpact has been on a real tear, particularly over the last 12 to 18 months. I’ve seen a real uptick, especially in Europe, where you’re winning a lot of deals. What’s going on? What are you doing differently?

Shantanu: I think there are four things at play, Phil. One, I think it’s a result of there or four years of sustained investment in our domain capability and our front-end capability. Obviously, in this business it takes a little bit of time for that to result in winnings in the marketplace, because you have to start engaging with clients at a different level. Then you get into a virtuous cycle, because as you get engaged with more and more clients they see the differentiated value that you’re bringing to the table—and the advisors see that as well. You get involved in more dialog and, as a result, you get in on bigger deals.

Let me share a data point. Our big deals—deals that are worth at least $50,000,000 in total contract value—have gone up five to seven times over the last four or five years. Obviously, the growth, other than GE has been pretty robust.

We have really focused our attention on a few verticals and a subset of clients. So, in terms of mining our existing clients, we have focused on a few and we have gone deep with them. We’re spending far more quality time with them. And, therefore, we’ve been far more proactive in terms of solutions and business opportunities, than just reacting to demand that is coming out from the market.

The last thing is that we’re combining much more technology, analytics, traditional strengths of Lean and Six Sigma into our process solutions. That’s creating a differentiated view in the market, which we’re branding as Lean Digital. Lean Digital wasn’t done over night. The branding is more recent but we have been on this journey for the last three to four years.

Phil: What would you say is the secret sauce that you can share that differentiates Genpact? What do you think makes your culture unique compared to maybe some of your competitors in the market?

Shantanu: That’s an interesting question, Phil. I’m not so sure that it’s a really secret sauce. I think it boils down to three fundamental factors. One is the real focused investment and persistence in building deep domain expertise, in a few chosen verticals and a few chosen service lines. We’ve been extremely insistent and persistent on that for the last three to four years—to the exclusion of everything else. We go very deep, and create differentiated capabilities.

The second thing is the bundling, which we talked about. Our focus on leveraging new digital technologies and what you can do to leverage data and analytics, has gone up 10 times over the last three to four years. That’s obviously resonating very well with clients, because the value equation has changed from just cost to many things outside cost. Third, we come back to the cultural point that you’re making. There are some pieces that have been consistent for the last 15 years, which is the maniacal focus on customers. Our Net Promoter scores have continued to go up. Last year we ended at 67%, which is our highest level ever. So that’s been consistent.

I think what has changed in the culture is the level of experimentation that we’re able to now do, both in terms of solutions as well as commercial constructs—because of the confidence that we have built up in our vertical and service mind domain expertise, and in our capability to try really large fundamentally, transformational programs for our clients. I think it’s about our interest in experimentation, our co-innovation mindset with customers. We go out and put a stake in the ground and continuously push the boundary and commercial constructs in terms of getting paid for results and performance, rather than just for effort. I think that’s been a big change over the last few years. If you look at us five years back and today, I think you’ll see a pretty significant change.

Phil: So we did a recent study that looked at the impact of digital on finance. Were you surprised when we saw that three quarters of the finance professionals fundamentally view digital as changing the way the function operates? Where do you see digital impacting finance in the medium term?

Shantanu: No, Phil, I wasn’t surprised at all. Actually, I am surprised that more people didn’t say that. I would have almost thought 100% would say the same thing, but I’ll give you two different dimensions to this. I think most people think of digital as having a very, very significant impact in cost and cycle time. There are lots of stories on what’s happening on the financial services world with fintech, what’s happening with robotic automation and stuff like that.

I think what is less appreciated today is the level of flexibility or agility, that this is bringing to operating models in finance, one. Two, with a greater level of data leveraging, analytics, predictive modeling, and forecasting means you’re really becoming a better business partner. I think that’s under appreciated and possibly not viewed as a fundamental shift. So no, I’m not surprised. But I think if you dig down, you will find all the dimensions are possibly still to be discovered in their entirety.

Phil: Shantanu, I’m really starting to see a growing, stronger link between automation and digital in the back/middle office. You can’t really develop a strong digital capability without a smart, actionable roadmap. I’d almost go as far as saying we’ll even cease using this term RPA soon because it’s just becoming a core component of digitizing the business. So do you agree with this viewpoint? Are you expecting this robo hype to continue? Or do you think it’s just going to become mainstream in the offerings very quickly?

Shantanu: Two different questions, Phil, so I’ll answer this separately. One is, I 100% agree with your world view. In fact, our entire positioning of our solution structure and the whole lean digital platform that we have taken, is fundamentally based on the premise that a lot of digital disruption and innovation so far has happened in the front office—changing the way customers interact in a B2B environment or a B2C environment. However, one of the biggest learnings from that innovation in the front office is that after the initially hype it causes severe customer dissatisfaction.

And it causes severe business problems if the middle and the back office does not get streamlined, does not get digitized. So we have focused exclusively on making that middle office and back office transformation become real for our customers, ensuring that the front-end transformation that many of them are on is something that they can deliver and they can actually delight the customer. That’s my answer to the first point, which is in 100% agreement with your view.

We’re seeing the customers are getting into that mindset now, they’ve understood that linkage. While many of them started from the front end, now the focus is coming back to the middle and the back end. Obviously, the evolution of the technology and the platforms that are happening, are allowing them to get over the historical impediments of cost and inflexible systems.

To come to your second question on the robotic automation piece: I think the hype will morph from the concept of robo today, which is primarily mimicking of a human task, to the application of bundled digital technologies, which is robotics, plus machine learning, plus cognitive algorithms, plus visualization and stuff like that, that transforms a process very fundamentally. When robotics came in initially, it was really just making an inefficient more efficient. But it’s not a fundamental transformation, but it takes out human beings and just mimics what the human being was doing, even if the process was inefficient.

What we’re seeing is increasing application of purpose-built solutions across the whole value chain of a commercial operation, which has various pieces of bundled digital technology, to really great differentiation. Our entire focus on the digital element and the process solutions that we’re developing, is about bundling rather than focusing exclusively on robotics, which would cater to just the hype. .

Phil: I think that’s a very good point. I’ve had some interesting conversations about the term “digital labor”—so getting away from the term “robotics” because it’s a little toxic. But I take the attitude if you’ve taken a manual process and digitized it using robotics software, it’s no longer labor, it’s a digital enabler. So that’s one of the reasons why I think we’re going to start to get away from that term. It’s like outsourcing was the act of moving services to a third party, RPA is the process of moving certain processes into technology.

I have a final question, Shantanu, about the impact on talent, and this has come out hugely in some of our recent client group sessions. I think some clients are scared today, they’re worried about what’s going on and are they still relevant. How can they stay ahead of the curve and be successful? How is the workplace changing finance professionals? What’s your advice here in terms of how to handle a lot of this disruption, to many of your peers and colleagues and clients?

Shantanu: Phil, this is possibly the most common question I face when I interact with senior finance professionals across our clients and potential clients. So I’m exactly on the same boat as you are. So let me give you some reflections, but I’m not sure it qualifies as advice. I think if you look at traditional finance skill sets, there was a lot of emphasis on the technical aspect of finance, then grounding your experience in the operational delivery of finance. So the traditional management training to senior leadership model was you go through practice, you go through sales offices, you go through profit centers, you go through corporate offices and you learn how operational finance happened in each of those places.

Then you did it in treasury, you did it in this company, you became a CFO–for the people who made it, that’s really how you went through the pyramid. With what is happening in the fundamental finance operating mode of transformation and digitization of operations, three things are becoming more important. The first one is analytical literacy, and that’s different from visual literacy. So how do you use data to be a true business partner? Phil you and I both know, almost every research study done with finance professionals has always shown serious dissatisfaction on the potential to be a business partner and the reality.

I think that has fundamentally changed, given the sheer amount of data that gets spewed out of the systems—and what you can do with that data in terms of modeling, forecasting and stuff like that. So that’s one. Two, with that data comes the whole concept of risk management. Risk management is going from the static view of controlled definitions and one-time control set up, and then auditing to really far more dynamic risk management—and also multivariate risk management across the globe.

The third is really the mindset shifting from cost-to-serve and managing cost-to-serve and cycle time, to creating really agile and flexible operating models—not just in finance, but in the core supply chain and being a partner to that.

So if you think of those dimensions, traditional finance does not cater to that. So it is a very live issue and I don’t think I have a ready made answer. But as we go through a lot of this, the sources of the talent will possibly have to change. So the curriculum will have to change. So I think there are more questions out there than answers.

Phil: That’s has been a very rich discussion, Shantanu, and I look forward to sharing this with our audience and the network on the blog very soon. We really appreciate your time and the thought that you’ve put into this.

If you weren’t able to make our excellent buyers summit at our research partner Cambridge University, we managed to crack the code (finally) on surviving in these disruptive times – in twelve simple steps. Just download our report and all will become crystal clear:

75% of finance executives agree that the new wave of digital technologies is fundamentally changing the way that the finance function operates. So what will the finance function of the future really look like?

Join us on April 21st to be part of this exclusive webinar and find out!

Join these experts from HfS Research, Genpact, Mondelez and KPMG as they discuss the findings from recent research that shows how digital technologies are delivering competitive advantage. They will share their insight on the future of F&A and explore:

What are the key drivers for F&A leaders to embed digital technologies, such as SaaS platforms, analytics, mobility tools, RPA, and machine learning, into their operations?

Where are most F&A organizations in their digital journeys and what lessons have they learnt?

What are the talent requirements and skill sets that finance leaders need in their functions to take advantage of digital technologies?

Where are digital pioneers investing and what challenges are they experiencing?

The BFS industry is completely dependant on data and analytics and the services to provide these analytics are critical. These services enable analytics data preparation and management, routine business intelligence reporting and dashboarding, advanced analytics modeling and ongoing decision-making for industry-specific use cases, including customer and marketing analytics, fraud, risk and compliance, and portfolio analytics.

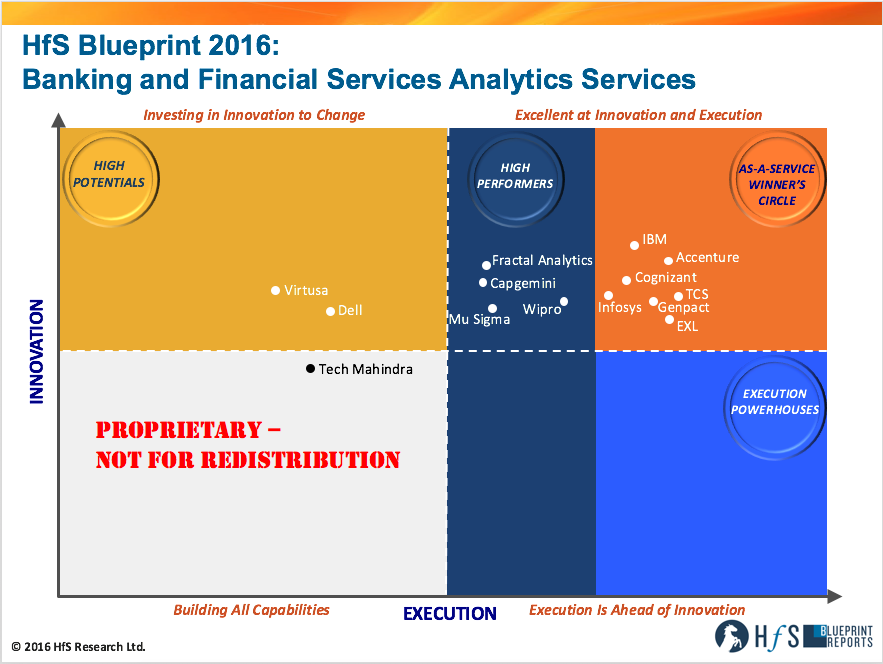

To this end, we’re excited to announce the release of our latest Blueprint Report–this one on BFS Analytics Services, authored by HfS Research Director Reetika Joshi‘s exhaustive research to arrive at this comprehensive view of the market. So let’s get an up-close view from Reetika on the Blueprint Report:

Click to Enlarge

Reetika, why have we undertaken an HfS Blueprint on analytics services specifically in banking and financial services?

The BFS industry is heavily reliant on the use of data, and yet the potential for embedding analytics-driven insights into operations is still far greater than adoption. The last few years have seen their focus on risk analytics intensify as regulatory changes and government scrutiny continue to mount. Along with balancing this growing compliance work, banks have also found a renewed interest in customer analytics to orient their growth initiatives. Most banks are not set up to meet digital consumer needs and are now embarking on digital transformation, powered by customer and marketing analytics.

Major banks and financial institutions are once again focusing on the next generation of analytics models, tools, and skillsets. We see demand from BFS clients across fraud, risk and compliance, AML/KYC, and customer and marketing analytics. Enterprise buyers in this industry are either unable to find the talent they need, for areas like specialized fraud, risk and compliance, or technology platform expertise, or are unable to afford it at the level of scale needed today—leading us to undertake this Blueprint to understand market direction. We see BFS clients trying to balance and complement their internal analytics teams with the global talent access that some service providers can bring them.

Report author Reetika Joshi, HfS Research Director (click for bio).

So how would you describe the current state of BFS analytics services?

For most service providers, big data and analytics services are the fastest-growing businesses in their portfolios, with significant revenues coming from BFS clients. This is due to the growing adoption of data-driven decision making within different parts of the enterprise for BFS buyers, and the need for more analytical support than internal staff can support.

Service providers have doubled down on BFS verticalization in their analytics portfolios, turning initial work with clients for analytics modeling and reporting into portfolios of pre-packaged industry-specific use cases and catalogues. As service buyers consistently stress the need for domain expertise from service providers, we see service providers strengthening industry training programs and hiring professionals from BFS industry backgrounds to increase contextual understanding and allowing for more meaningful analysis. We see the types of BFS analytics solutions changing today, with the next level of analytics use case development. BFS analytics services buyers seek the following:

The application of cross-vertical learnings to banking, especially from other consumer-facing industries that have progressed in customer experience analytics (e.g., from telecom to retail banking)

The incorporation of newer sources of data into existing analytical models to gain new insights into fraud, risk, and marketing (e.g., sensors, geolocation mobile data, and web and social data)

The exploration of modern business intelligence and reporting applications and tools, big data infrastructure, and advanced analytics platforms (e.g., cloud-based data warehousing, the mobile delivery of reports, and insights)

These initiatives are step changes for in-house data and analytics teams that are already struggling just to keep up with the demand from a growing list of internal clients. Service providers are bringing in the skills, technology, and scale to these categories coming from investments in the last few years in this industry vertical. We see this market as gradually transitioning, with service buyers and providers becoming more collaborative and focused on solving business problems to improve the outcomes for different functions within banking and financial services organizations. We view this as a step in the direction of a transition to the As-a-Service Economy, with service buyers leveraging their service providers more strategically for their big data and analytics needs.

Which service providers are leading this market today, Reetika?

The banking and financial services industry vertical has historically been the biggest revenue contributor for most service providers in our evaluation. They have developed meaningful relationships with BFS clients across the globe by taking on outsourced IT services, infrastructure, and BPO services. In the last decade, they expanded services to include data management, reporting, and analytics across industry-specific and horizontal business functions. As a result, today we observe a significantly mature set of service providers that have strategically invested in this vertical, have strong multi-tower relationships with their clients and have both analytics services and technology expertise across different BFS business needs. This is visible in our Blueprint grid results with several As-a-Service Winner’s Circle and High Performer positions from leading service providers in this market:

Accenture is creating an industrialized analytics model using FinTech networks and innovation

Cognizant is fostering specialized talent for BFS analytics and platforms

EXL has been described as an “extension to the advanced analytics team” by its BFS clientsGenpact is augmenting niche BFS talent development with a new IP-led strategy

IBM is introducing its BFS clients to the potential of cognitive risk management with Watson

Infosys is investing in analytics platform specializations to drive new value for its BFS clients

TCS is a BFS domain expert bringing automation to legacy analytics engagements

High Performers in this study include:

Standalone analytics specialists, Mu-Sigma and Fractal analytics that have a loyal client base of BFS clients that see them as business problem solvers.

Capgemini and Wipro that are pivoting from their experience in data management, BI and routine reporting to invest in analytics, with Capgemini driving customer experience analytics and Wipro focusing on cognitive and analytical solutions in risk and compliance.

Due to multi-faceted demand, service providers have evolved their analytics practices in different ways, e.g., EXL and Genpact have more large scale, multi-year BFS engagements, while Accenture and IBM have more experience with projects and consulting services for banking clients. The Winner’s Circle and High Performers are now developing adjacent capabilities on the back of these traditional strengths. So BFS clients are advised to take a new look at their analytics service provider to freshly evaluate their capabilities. In the last few years, service providers have undertaken several acquisitions and other investments in developing critical thinking, data sciences, and analytics technology platforms. Due to past perceptions of capability, we see the pigeonholing of service providers as a key inhibitor to partnering at a strategic level. There is an opportunity here for service buyers to collaborate and influence market direction for strategic partners at this stage of their growth, where they are extremely amenable to making investments in BFS-specific solutions.

Finally, what recommendations do you have for BFS analytics service providers in 2016?

Facilitate Industry Collaboration: Barring a couple of Winner’s Circle leaders, the majority of service providers lack the ability to act as facilitators for sharing ideas across companies in their client base. BFS clients in our research stress that they would really value the opportunity to connect through forums, etc. with other enterprise analytics users, academic communities, and FinTech startups to understand next-generation analytics developments. While it is difficult to orchestrate given confidentiality concerns in the banking industry, clients would also value cross-industry perspectives, especially for consumer-facing verticals that have rapidly advanced their analytics adoption in the last few years.

Find New Ways of Lowering Costs: In the near term, there is still value to be found in leveraging offshore talent for BFS analytics, and this is an area of utmost importance to BFS clients. However, the costs continue to rise year after year for Indian analytics data scientists, PhDs, and analysts. Service providers must continue to explore cost controlling levers, including hiring in Tier III locations, and building in more automation to eliminate work (and pass on savings to clients).

Above Everything, Have an Iron-proof Global Talent Strategy: We see a few service providers like Accenture, Genpact, Infosys, and EXL focus on expanding the talent pool and contributing to curriculum development with university tie-ups across global talent locations. As the data sciences field continues to grow, BFS-specific specializations in risk and compliance will command greater attention from clients.

Initial Printing of Groundbreaking New Magazine to be Mailed to 200,000 Subscribers

The firm that coined the As-a-Service Economy is now disrupting the analyst industry even further. HfS Research, The Services Research Company, today announced it has launched its most disruptive research offering so far: HfS unDigital Magazine.

This revolutionary publication will challenge the rhetoric and hype currently being stirred up in the IT and BPO services industry, building on the success of the radical blog “Horses for Sources,” which will soon be replaced by this cutting-edge print publication. HfS is now taking disruption to an entirely new level…by revitalizing the hallowed glossy magazine. The firm believes people are so tired of relentless social media that bringing back printed words and pictures will change the research game once more.

In announcing the latest development, Phil Fersht, HfS Founder and Industry Analyst, noted that this is not the first time the firm has shaken up the marketplace.

“In 2007, when I created the Horses for Sources blog, people thought I was crazy,” said Fersht. “Who would read that? Then, when I started HfS Research a few years later, people became truly concerned for my sanity. Soon after, we created the industry’s best summits. Now, with well over a million hits on our sites every year, we have decided to shake things up once again. How can people still doubt us now?”

HfS unDigital Magazine will be available on newsstands around the globe and via subscription to 200,000 existing clients and community members:

The first issue of the magazine is printed by Heidelberger Druckmaschinen AG, in Heidelberg (Baden-Württemberg), Germany, on 80lb glossy paper stock, features the following stories:

Phil Fersht tells all with his Undisrupted Undigital Experience

Dumb and Bummer: Why Artificial Intelligence is all hype

Hot News from December 2015Outcome-based pricing is worth the paper it is written on

A Labor Arbitrage love-fest with Agony Uncle Charles

Design Stinking: HfS sifts through the cheese to get to the real deal

De-automating your Back Office the Reuner way

“This is a huge undertaking,” Fersht added. “But we know that a lot of our community has grown tired of staring at pixels and yearn for the feel of the printed page once again. Disruption has moved full circle and now we’re disrupting back in print. Our clients tell us they miss being able to sit on the loo and flick through pages of their favorite analysts waxing lyrical. Those days are now back… so take your seat and enjoy!”

And of course… this was an:

Please, please don’t tell me you fell for this again! (Even though the business model might kinda work…)

And while we’re reminiscing about falling for April Fools’ gags, here is 2015’s classic:

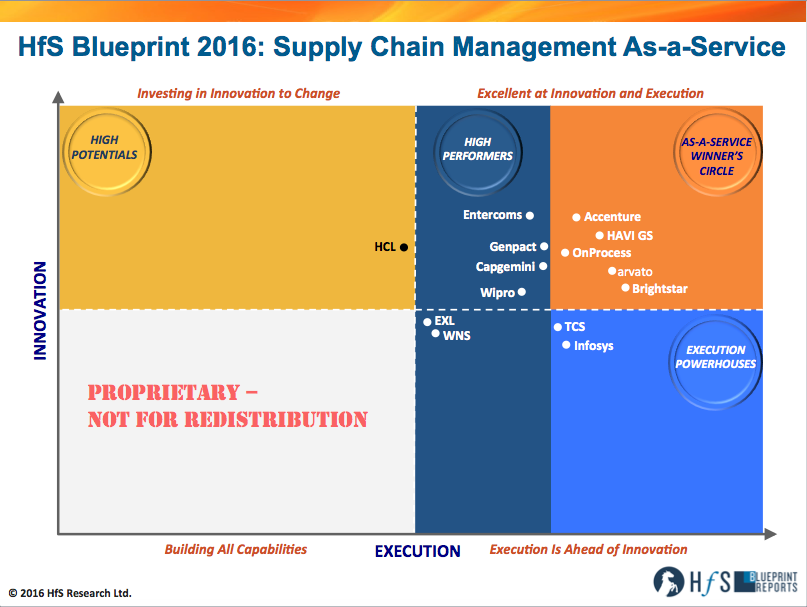

HfS supply chain process expert (among other things), Charles Sutherland has finally done what no other analyst has done before him… define and develop the first comprehensive view of Supply Chain Management As-a-Service….

Supply Chain Management BPO has, since its inception, been an enigma in the overall BPO industry. Combining both large-scale transactional order management contracts along with focused domain and analytic skill-enabled forecasting engagements, it has been both an outlier in the portfolio of many large service providers as well as a lucrative market for specialist pure play providers. Clients often considered these engagements as something more like prolonged consulting deals than actual outsourcing contracts, while service providers wondered where best to house the delivery teams inside the organization as a result.

Now, more than a decade into operations—and with total market ACV closing in on $2 billion—HfS is seeing that many of the characteristics of Supply Chain Management BPO that were once considered causes of its uniqueness (Design Thinking, Collaborative Engagement, Accessible and Actionable Data) are now traits sought for all BPO engagements as the market moves toward As-a-Service solutions.

Once ahead of its time, Supply Chain Management is now very much integral to the realization of As-a-Service and so it was time for HfS to look again at this market following our inaugural Blueprint in 2014 to describe how it is developing and which service providers are leading the way. So let’s get Charles’ thoughts on this market and its leaders…

Click to Enlarge

Charles, how would you describe the current state of Supply Chain Management As-a-Service?

We describe this market as one that is fast growing but still tiny against the backdrop of the entire BPO marketplace. But we believe the potential opportunity is massive—at potentially $300 billion-plus. So penetration today of this addressable market is less than 1% and we expect to see the current enthusiasm for participation by service providers to continue and only grow more in the next few years.

We covered 14 different service providers in this Blueprint (with 3 service providers covered for the first time) and what is striking, versus say the Finance & Accounting BPO marketplace, is how unique the offerings and capabilities are between these 14 service providers today in supply chain management. These service providers are not mirror images of each other. Each one brings different industry specializations, domain knowledge, technologies and commercial models to bear. This heterogeneity of service providers highlights the still early and evolving stage in the lifecycle of this offering and the scope of the opportunities left to be addressed.

We would also highlight that As-a-Service is the model today and for the future in supply chain management. As-a-Service has been part of SCM services since its inception. In particular, service providers have acted as “Brokers of Capability,” partnering with enterprise clients to identify operational issues and then bring the required insights and talent to improve business outcomes. In the last several years, the availability of deeper analytical talent, digital platforms and design thinking approaches has moved this market even further through the As-a-Service model.

Finally, this is also a market where service providers have to respond to an ever changing landscape. It is clear to HfS that the increasing adoption of IoT, the deployment of intelligent automation (both robotic process automation and cognitive computing) as well as the growing utilization of formal design thinking practices will impact this market tomorrow and for years to come. Success in this market comes from understanding not just the client business issues of today but how these issues will evolve and manifest in the future. So, more than anything else, this market today is one that both requires and rewards real and substantive collaborative engagement between service providers and enterprise clients.

Charles Sutherland, HfS Chief Research Officer and author of the HfS Blueprint Report: Supply Chain Management As-a-Service (click for bio)

How has that changed since our inaugural Supply Chain Management BPO Blueprint in 2014?

Already back in 2014, we could see many of the Ideals of As-a-Service nascent in the offerings of the service providers. But over the last two years we have seen a massive uptake in interest and investment in this offering by the service providers. Today, having a strong supply chain management offering is a way of showing commitment to the evolution of BPO from legacy delivery models to one that exemplifies as-a-service and clients are responding as well. Supply chain management growth rates at 20%-plus are well above the market norm and that is encouraging further attention and investment in this market as well. In 2014, service providers (and clients) were just starting to see how Control Towers—which can provide an end-to-end process view of operations in a supply chain—were important to service delivery. Two years later, it’s clear that this is fully recognized and so we are seeing a heightened level of investment in Control Tower solutions across the market. Service providers and clients are also seeing that, whereas in 2014 just getting visibility into the supply chain through a Control Tower was valuable, today it’s about modifying the processes around these solutions so that either party can intervene in the supply chain process when the analytics show an emerging problem and take actions to mitigate what might previously have been significant business impacts.

In 2014, many service providers and clients talked about how they were looking ad-hoc at issues and trying to solve problems before they impacted the processes. They weren’t calling it design thinking then but that’s what it was. Today, many service providers are calling this out and embedding a formal design thinking methodology into the way that service providers and clients work together over the life of a contract.

What’s also different since 2014 is the realization that other emerging trends such as IoT, 3D printing and intelligent automation are going to have major impacts on today’s supply chains and that the processes of tomorrow will be significantly different than in the past. The last few years really were about service providers and clients working together to determine what an end-to-end supply chain looked like. Now, in 2016, that is changing to working on how that end-to-end process view will need to continue to change into the future.

Tell us, Charles, which service providers are leading this market today?

Our HfS Blueprint methodology assesses service providers against a variety of criteria related to Execution and Innovation capabilities of the service providers based upon buyer reference calls, market interviews, RFI submissions and detailed market briefings.

The service providers in the As-a-Service Winner’s Circle are the providers that scored highest on both Execution and Innovation and included: Accenture, arvato, Brightstar, HAVI Global Solutions and OnProcess. These service providers stood out for the excellence of delivery operations, the depth of domain and process expertise, the inclusion of client feedback, the comprehensiveness of their vision for supply chain solutions and the effective utilization of accessible and actionable data to deliver business outcomes.

We identified two service providers as Execution Powerhouses—Infosys and TCS—that excel today in execution of supply chain management services and are making investments in innovation that should enhance future operational solutions as well.

Our High Performers, which captured a balance of strengths between Execution and Innovation, numbered six and included Capgemini, Entercoms, EXl, Genpact, Wipro and WNS, with some service providers really pushing the boundaries on overall innovation in the marketplace and all offering capabilities to meet the needs of today’s supply chain management buyers.

Finally, we also identified a High Potential service provider in HCL—new to our 2016 Blueprint. HCL is using a depth of capabilities in IT and engineering to deliver platform-based supply chain management with domain expertise.

What recommendations do you have for enterprise buyers looking at Supply Chain Management As-a-Service?

Our overall recommendation would be to jump in and test the waters if this is new to any enterprise. The offerings from service providers are maturing rapidly and the levels of strategic commitment and investment have never been greater. This will be one of the major growth offerings for the years to come and enterprises have a chance to shape those offerings to meet their own needs today.

Having decided to take the jump, adopt a design thinking mindset when it comes to assessing the issues in your supply chain and what solutions might be most suitable. Sitting down with your prospective service provider(s) to better understand the business context in which your current processes operate and what can be done to realign or reimagine those processes to achieve different and/or better business results is always an exercise worth undertaking.

Having made that jump, we encourage buyers to not test using labor arbitrage models from the past but to push for as-a-service solutions. With all the current (and future) business challenges enterprise supply chains face, it’s important to secure solutions that are flexible and agile and which can grow to meet your needs as they evolve over time. Don’t settle for a long-term fixed model of solution delivery that might work in F&A or HR because it won’t work here.

Along the way this year and beyond, also ask the service provider for insight into how 3D printing, IoT and other innovations are likely to impact the supply chain processes you have in place today. Use quarterly business reviews and other interactions with service providers to review their vision for the evolution of supply chain management as a service.

Having embarked on a collaborative journey together using design thinking, continue to push your service provider and your own team to be more collaborative, more visionary, more inclusive and more trusting together. Extend this same new mindset to how you think of data and physical security to make sure that your policies on security aren’t coming with unnecessary costs to your supply chain. Address the enterprise pain points of supply chain and realize the resulting business outcomes is easier in a close partnership than in a closed-off zero-sum mindset relationship. So, work with your service provider(s) in a manner that facilitates long-term mutual success.

So that’s our take on the state of Supply Chain Management As-a-Service at the start of 2016. Please share your thoughts with us as this fast growing and dynamic segment of the As-a-Service Economy continues to evolve.

Soon there will be nowhere left to hide. Everyone’s value is under the microscope from colleagues and management alike. Whether you turn widgets, manage a process, a set of processes, lead teams or manage team leaders leading teams… or run a whole division… or even an entire organization, you are under constant scrutiny in today’s open workplace.

Soon there will be nowhere left to hide. Everyone’s value is under the microscope from colleagues and management alike. Whether you turn widgets, manage a process, a set of processes, lead teams or manage team leaders leading teams… or run a whole division… or even an entire organization, you are under constant scrutiny in today’s open workplace.

When your enterprise is increasingly dependent on hiring “Millennials” with digital skills and lower wage needs, you’d better figure out a plan for creating exciting, challenging career paths, or you’re pretty much already doomed.

When your enterprise is increasingly dependent on hiring “Millennials” with digital skills and lower wage needs, you’d better figure out a plan for creating exciting, challenging career paths, or you’re pretty much already doomed.