Coming away from our Cambridge University buyers summit this week, I was pleasantly surprised by the increased level of sophistication and maturity many services buyers are now exhibiting.

Gone are the provider bitch-fests and endless ranting about failed promises and absent innovation (that they didn’t pay for in the first place). Instead, there was a desire to look at themselves, and really try to figure out how to broker change and run their outsourcing engagements as part of a broader business agenda, not some quirky siloed activity, forever tarnished by the word “outsourcing”.

Adopting a mindset to change today (not tomorrow), is where everything must start

Yes, the conversation has turned to buyers accepting they need to change first, before heaping all the blame for their woes onto their service providers. This is why our Ideals of As-a-Service begin with a mandate for buyers and providers to change how they behave, how they can adopt a mindset to start writing off their legacy processes and technologies. In short, it’s time we focused on fixing our present – it’s time we focused on Being As-a-Service:

Click to Enlarge

It’s time we stopped talking about this scenario of “this was legacy and this is our future desired endstate”… we’ll just remain stuck in this perpetual stranglehold of never getting anywhere. We’ll always we a work-in-progress, a project that never finishes…

As someone joked during our Cambridge University summit this week “Cognitive computing is always going to be huge in the future”… so let’s stop evangelizing about a nirvana we many never reach and, instead, start talking about what we need to do today. Let’s stop panicking about the future, which is scaring so many people, and start focusing on what we can do today to be more effective.

Let’s start talking about Being As-a-Service today… not tomorrow, or some far off point in the future, where we just hope this all becomes somebody else’s nightmare…

Bottom-line: We have to narrow the chasm between hype and reality in order to be successful in the present

Our industry is beset by fear, like never before. People are scared – they know their skills and capabilities could quickly become obsolete in a world where the job openings increasingly demand creativity, analytical prowess and an ability to pivot across domains. Suddenly, if you’re not a Digital native who talks about endless disruption and the coming robo-geddon, you’re a dinosaur… The gap between hype and reality has reached ridiculous proportions, and it’s time we stopped thinking about the fantastical future and focus on what we can achieve today.

Successful sourcing executives have to become “brokers of capability” (which one buyer commented sounds like a rock band) where they can live in the present to drive a change mindset for the future. Most of the executives have been tasked with adopting Digital strategies (whatever those may be) and to come up with smart approaches to take advantage of automation technologies. But to get there, they need to change how their teams think, collaborate and operate.

It’s a mindset change, it’s a culture change. It’s about bringing together the key stakeholders and delivery leads to address the As-a-Service Ideals today and stop looking at them as some far off nirvana someone else will take them to. Simply put, most firms can’t simply saw-off their legacy by disposing of some archaic ERP system and slamming in some SaaS product, or mimicking every defunct manual process into a piece of RPA software, or firing an entire department of ineffective process wonks. In fact, a lot of the legacy actually works and the ROI of binning it doesn’t make financial sense. Writing-off legacy is about starting the process of re-imagining a future without those legacy systems and processes that are holding back our businesses.

So the Ideals of As-a-Service can be initially addressed today by making the most of what we currently have, not simply waiting for the day budget magically appears from above to bring in teams of nose-ringed consultants to redesign our businesses.

Amidst the relentless robo-hype in our current era of robotic rhetoric, it’s fast-emerging that many buyers and service providers are really struggling to work together to create workable Robotic Process Automation initiatives – in many cases, neither are willing to make the necessary investments, trade-offs or sacrifices to make his work.

So let’s start with those selfish service providers unwilling to share the robotic rewards…

Some service providers want to implement RPA on themselves and avoid passing on the savings to their buyers. Having come off a great many buyer discussions about their developing Robotic Process Automation (RPA) capabilities to augment their BPO engagement productivity, I have been shocked to hear a common thread from several buyers: their service providers only want to implement RPA on themselves and insist on charging their buyers the same legacy FTE rates. Some service providers simply cannot stomach sharing gains with their buyers – some have, but the general experience, from the buyers, has been they are not really interested. And one of those service providers even boasts its own “cannibalization fund”, while refusing to do anything different with several of its biggest engagements. It’s quite mind blowing how contrary some of these service providers can be, when it comes to what they claim they are doing versus the reality of what they really up to.

Yes, amidst this talk of the leading service providers breaking away from the old model and openly exploring ways to invest in initiatives to delink headcount from revenue, it would appear that some are simply playing lip service to the industry while, in reality, they are just looking at RPA as a vehicle to drive down their own costs and improve their margins, while maintaining their legacy FTE-pricing. One buyer even mentioned to me that their service provider had the nerve to ask them if they could reduce their own staff delivery headcount using RPA, but keep charging them the same FTE rates…. no joke.

However, this isn’t just the fault of the service providers, many buyers are equally to blame for robotic restraint…

Buyers need to entrust their providers with more intimate data access. Most enterprise buyers, for security and control reasons, keep the providers at bay and force them to connect to their systems only using Citrix. This limits the effectiveness of RPA overall and encourages an “us versus them” mindset between buyer and provider, so it’s no surprise service providers do what they can on the other side of the “Citrix” firewall. Both parties cannot enjoy the full benefits of RPA and Intelligent Automation, without genuine collaborative engagements and a holistic security model that aligns the capabilities more effectively.

Greedy buyers need to stop treating RPA like legacy offshore BPO, demanding all the savings up front. I would also argue that many costs of RPA –greater testing, maintaining a fall-back agent pool and the incremental manner that robots are typically actually rolled out (versus a one time overall reduction in costs, as often asked by buyers) diminish the “greedy” aspect of this from many service providers. In addition, many buyers want royalties for advancing the automation initiatives of the sell side – there is a whole new business model evolving around access to data as well as contribution to IP, when it comes to developing effective RPA platforms.

Sadly, many buyers are often too greedy and want to get all the theoretical cost savings from a new deal up front, even before the RPA benefits have been formalized – and without realizing that RPA often drives up service provider costs in the short term for increased testing and QA. In this way, buyers are keeping the mindset used in legacy outsourcing deals, where savings driven through labor arbitrage were much more predictable and tangible. I would argue that many costs of RPA – a great deal of testing, maintaining a fall-back agent pool to mitigate transition risks, and the incremental way that robots are actually rolled out (versus a one time overall reduction in costs as often asked by buyers) put the service provider in a much riskier position to guarantee productivity benefits and cost efficiencies, than they ever were with their legacy outsourcing deals. Robots are not as easy to plug into legacy processes as offshore labor…

So clearly we are rapidly arriving at a juncture where a couple of scenarios will play out as to how buyers and service providers make RPA work…

Legacy BPO deals will continue to stagnate for some time. In most cases, deals struck several years’ ago have met their initial productivity targets through offshoring and some basic process standardization. The service provider has no incentive to do anything but maintain the same rates and same margin, and most are willing to risk their buyer trying to bring in a competitive bidding process. They know that in many cases, their business is not that attractive to other providers, and the cost of switching outweighs the benefits of “winning” the business.

Where we will see the advent of Robotic-led BPO solutions

Definition of Robotic BPO: “Applying robotics to transform legacy business process outsourcing engagements that were developed with a legacy FTE pricing and mindset. Deals are wholly or partially financed by the anticipated future headcount reduction and productivity improvements driven by the RPA, where the buyer and provider share the risks”.

It’s very rare today that RPA results in the elimination of entire job roles for staff in the BPO world (less so than with IT automation). Hence, we view an emerging focus on human-augmentation robotic solutions that combine people-driven processes with genuine RPA capability where it is cost effective and secure to implement.

We are already witnessing a serious potential for service providers to offer RPA-led offerings to streamline bloated stagnant BPO engagements, especially where there is a lot of very automatable offshore work that is efficiently run with well documented process flows. Enter R-BPO, where we will surely see the first automation-led human augmentation solutions, where the deals are partially funded by the expected headcount reduction and productivity improvements over the course of a multi-year engagement. We believe this will be especially relevant in F&A contracts which form the baseline of the BPO market today

Once we get passed the constraints of Citrix and the non-collaborative application and data security strategy of many enterprises there is real opportunity to reshape the market of F&A BPO contracts. In Finance and Accounting, many deals are mature and rooted in legacy models, the work is highly transactional, and buyers have been stuck with the same FTE loads for years (or decades). But the real reason why F&A is starting to deliver real potential for R-BPO is the simple lack of widely accepted enterprise F&A SaaS which can fix the dysfunction of a process, with a broad-brush implementation and hefty license fee. We are seeing it in pockets with SaaS solutions such as Workday FM, Netsuite and even FinancialForce, but it’s the ultimate failure of F&A to over-rely on legacy technology, maintain strict controls that defy collaboration, and keep bloated numbers of people to deliver legacy processes that is creating a huge potential new market for robotic-led processing and human augmentation.

The Bottom-line: Legacy BPO may be stagnating on its own, but it’s ready for R-BPO

What’s abundantly clear is that the outsourcing industry is caught in one bloody great rut: too many engagements are simply stuck in this Catch-22 where they are no longer attractive to competitive bids and the incumbent providers simply do not see the value (or have the onus) to invest in the buyer. You can’t trim the fat until you fix – and automate – the process underbelly, and today’s emerging RPA tools, such as Automation Anywhere, Blue Prism and UiPath, are increasingly providing the platform to do that. So the next phase is for R-BPO solutions to be come to market that are priced against future productivity gains through automation, not immediate cost-savings through labor arbitrage and elimination.

A momentous event occurred in the world of Robotic Process Automation (RPA) today, when its pioneering vendor, Blue Prism, became the first pureplay RPA vendor to announce officially its intention to IPO.

Naturally, this sparked some feverish debate among the RPA cognerati over whether we may see one of the established services firms make a play to own their very own RPA platform, as opposed the the currently practice of every service provider partnering with every RPA product on the market.

My personal viewpoint is that IBM should take a serious look at Blue Prism, especially now RPA is officially a market-worthy capital asset. IBM is a huge software company and could seriously benefit from having an RPA offering it can build out as an enterprise platform, provided it makes sufficient investment and has leadership attention to develop the solution.

So let’s look at the pros and cons:

Why IBM should probably buy Blue Prism

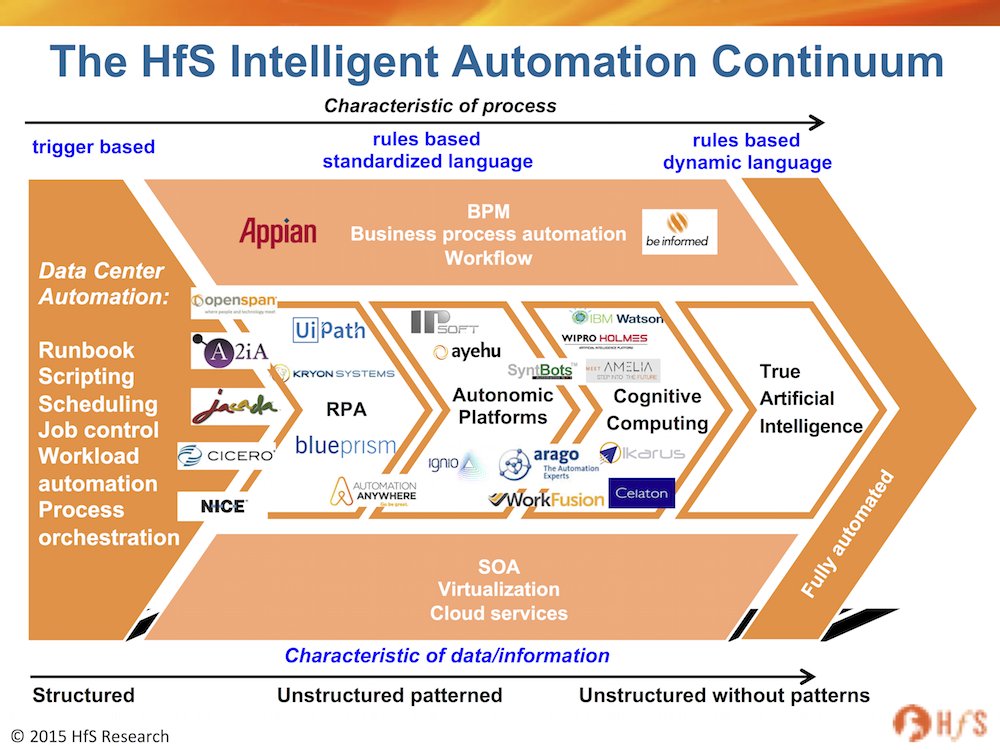

Watson alone is not going to do it for IBM in the Intelligent Automation space. IBM needs an RPA offering as the first building block along the Intelligent Automation Continuum (see below). Pushing RPA onto more clients will also open up the Watson conversation as a logical next step for many clients.

A Blue Prism + Watson platform could create a whole new ecosystem of possibilities. Adding Watson’s cognitive capabilities to Blue Prism would create a real differentiator in the Intelligent Automation domain – you would end up with a whole new ecosystem of services and capabilities for enterprises across automation, predictive analytics and cognitive computing.

IBM needs to focus on becoming the leader in industry-centric Automation/Cognitive services. This is where IBM can really make its future mark in 2020-and-beyond enterprise services. There are limitless possibilities with the potential of artificial intelligence in industries such as healthcare, manufacturing and retail. Simply providing a cognitive engine is not enough – IBM needs to build leading-edge business practices around it. It is doing some very cool stuff in healthcare and medical research, for example, but I believe it can do so much more to help enterprises streamline their processes and act on realtime data, with a defined Intelligent Automation roadmap.

A genuine RPA underbelly for enterprises. IBM can position Blue Prism as a true enterprise RPA platform, as opposed to a mere robotics tool for specific processes. It’s one thing tightening up a few loose parts, another entirely, when you overhaul the engine…

Brand credibility and IBM’s hooks into leadership discussions. IBM has real credibility to dominate the RPA conversation with enterprise leaders – having its own platform adds some serious fuel to the fire. Automation and cognitive are high on the leadership agenda, where IBM has the potential to make it a market of one.

More than BPO. In addition to fuelling its BPO capabilities, IBM could leverage Blue Prism as part of its management toolset and BPM portfolio

Modest initial investment. For IBM, the likely cost of acquiring Blue Prism would be modest compared to its regular mega acquisition habits

Why IBM probably should probably not buy Blue Prism

Alternative offerings could be considered. Some clients prefer (or claim to prefer) using Automation Anywhere and UiPath, among others. However, there is no reason why and IBM-owned Blue Prism could not operate in a multi-solution automation environment.

Citrix issues. Some Blue Prism partners claim they struggle with Blue Prism in Citrix environments.

Longevity of RPA as a “solution”. In two years’ time, nobody will talk about RPA anymore – it’ll be native in any enterprise process solution worth its salt.

Does IBM really need it? IBM’s current BPO business portfolio is active enough to drive significant bot deployments on its own.

Size of IBM’s box of tricks. Will the emerging roadmap for industrializing RPA become lost inside of IBM’s bulging software portfolio?

Reduces attention on RPA as a solution in its own right. Will embedding Blue Prism in IBM lead to a reduction of attention on RPA as a solution in its own right, just at the moment when RPA is becoming a coordinated strategy for many enterprises?

The Bottom-line: No clear Intelligent Automation services leader has yet emerged. Acquiring one of the leading RPA platforms could be the catalyst

IBM needs to do something – buying up Weather Channels and Workday implementers is all great for today’s markets, but with its huge bets on Watson and cognitive computing, the addition of an enterprise RPA platform underbelly could be a killer move. Service providers such as Accenture, Cognizant, HP and TCS are already very active pushing RPA deployments, and, while IBM is also deep in the mix, it is already playing catch-up to some of the service providers. And maybe Blue Prism is not the right move to make – there are other potentials to look at (which it surely is doing), but the pros are far outweighing the cons in today’s climate, where aggressive moves are critical.

One of the most significant shifts towards As-a-Service delivery, in recent times, has been the investments in delivering comprehensive IT and business process services to support the enablement of leading SaaS platforms. With the gravy train of revenue the leading service providers have enjoyed from clunky on-premise ERP services, over the last 2+ decades, now slowing, the land-grab to manage the data, business transformation and integration elements of the leading SaaS platforms is hotter than ever.

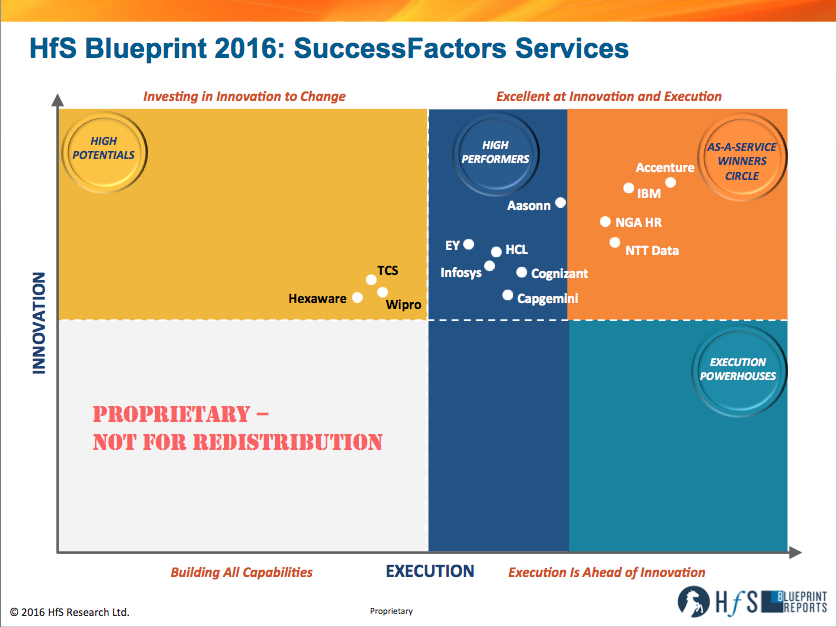

To this end, we’re very excited to unveil the industry’s very first HfS Blueprint on SuccessFactors Services. With HfS Principal Analyst in SaaS services, Khalda De Souza, at the helm, this Blueprint builds on the direction we carved out in our Workday and Salesforce Blueprints in 2015. So who better than Khalda to bring us up to date:

Click to Enlarge

Khalda, why have we undertaken an HfS Blueprint on the SuccessFactors Services market?

Blueprint author Khalda De Souza covers SaaS for HfS. (click for bio)

The SuccessFactors Blueprint continues our theme of looking at the markets for services around leading SaaS platforms, following on from our Workday and Salesforce Services Blueprints of the past 12 months. All of these markets are in high growth mode as enterprises seek flexible, user-friendly solutions to better manage their HR or CRM processes. The service providers included in our SuccessFactors Blueprint have experienced an average of 45% growth in SuccessFactors services last year and expect to see the same growth levels next year. Given that enterprises with SAP ERP in the back-office are more likely to select SuccessFactors for their cloud HR solution, the potential market is huge.

We also see snippets of the HfS Ideals of the As-a-Service Economy in the SuccessFactors service market. Clearly, enterprises are making the commitment to Write Off Legacy by moving to SuccessFactors and building new HR processes around the platform. Service providers are also driving Collaborative Engagements with flexible engagement methodologies and a key focus on desired business outcomes.

How does HfS define the SuccessFactors Services market?

HfS has defined a Value Chain of services that applies to all the SaaS platforms we cover. This includes the five components delivered by service providers to create value for enterprises: Plan, Implement, Manage, Operate and Optimize. For SuccessFactors services, Plan includes consulting services such as SuccessFactors business case development, compliance, security and governance services, as well as HR strategy and SuccessFactors-specific process and design services. Implement covers all the services and skills required for effective deployment, including but not limited to project management, testing, training and data migration services. Manage includes all ongoing integration and support services. Operate includes business processing outsourcing (BPO) services where they are delivered by the service provider around the enterprise’s SuccessFactors environment. Finally, Optimize services are intended to improve the impact of SuccessFactors solutions and may include: the assessment of new SuccessFactors releases and solutions and on-going HR strategy alignment.

So, which service providers are leading the services for SAP SuccessFactors market today?

Using our HfS Blueprint methodology we found four service providers who belong in our As-a-Service Winner’s Circle for SuccessFactors Services today. These are Accenture, IBM, NGA Human Resources (NGA HR) and NTT Data. These service providers stood out include the breadth of their delivery experiences, the strength of client references, the alignment of supporting tools and technologies to SuccessFactors coupled with visions for the transformation of HR processes using the platform.

Six service providers are in the High Performers category: Aasonn, Capgemini, Cognizant, EY, HCL and Infosys. All of these service providers also have strong capabilities and scale and have invested in a services vision for Success Factors, HR process knowledge, Design Thinking services and tools development to create value for clients.

We also identified three service providers in the High Potentials category: Hexaware, TCS and Wipro. The SuccessFactors service practice for these providers is in aggressive growth mode and, based on their solid investments and vision for this market, we expect these service providers to continue to grow their capabilities in the next few years.

What are the major trends we see which will impact these service providers over the next several years?

We see a mix of deployment behavior, with some enterprises choosing to implement only one SuccessFactors human capital management (HCM) module and run a hybrid cloud and on-premises HR solution, while others opt to deploy the entire SuccessFactors HCM suite. Service providers, therefore, need to continue to hire and train talent in all the SuccessFactors HCM modules.

However, it goes beyond just technical capabilities. Clients tell us that the single most important contributor to value is the service provider’s ability to share HR best practice advice. Hiring activities therefore also need to focus on people with good HR experience so that they can bring this business process knowledge to engagements. Service providers with a strong SAP practice and/or HCM practice are at an advantage as they can cross-train consultants to augment their SuccessFactors practice organically. In addition, service providers who have developed services and solutions to support and expand the payroll and analytics modules have opportunities to grow as these areas increase in popularity in the next 12 to 18 months.

What about the trends within the specific services?

Clients tend to contract a separate consulting provider, such as Deloitte and EY, to help with solution selection, HR process advice and roadmap setting. Service providers that have invested in SuccessFactors consulting services need to market these aggressively to ensure being considered for consulting services.

Implementation services are the biggest part of the SuccessFactors market today. Enterprises select a deployment partner based on service capability, geographical scale and cost effectiveness. There is often little or no scope for the implementation service provider to bring any vision or thought leadership to the engagement. While clients admit that they did not ask for this, they realize post –deployment that business-oriented advice from the implementation partner would have been useful. There are therefore opportunities for service providers to share HR best practice knowledge in implementation service contracts.

We also expect to see increasing demand for management and optimization services, with a focus on flexible services and pricing methodologies. Consistent with the SaaS service market in general, clients need access to skills and talent on demand to solve ongoing issues. Typically enterprises can purchase a bundle of hours per month to pay for these services. Operate or BPO services are still very small in the SuccessFactors service market. Service providers will general HR BPO capabilities are best placed to take advantage of this market as demand grows, but we don‘t expect to see rapid growth in the short-term.

Finally, what recommendations do we have for service providers through 2015 and 2016?

HfS believes that service providers that want to have the greatest impact on enterprise clients and lead the SuccessFactors services market should:

Invest in a functional understanding of the HR process: Leading service providers are able to share HR process best practice advice to clients. This is relevant in all the phases of the Value Chain. Service providers should hire and train consultants with HR process backgrounds.

Upsell management services more aggressively: Service providers should be proactive in explaining the importance of post-deployment management services, as most clients do not consider this.

Invest in tools and technologies: Service providers should continue to invest in tools and technologies to enhance their SuccessFactors service offerings. In particular, investments in HANA extension tools and industry focused templates and tools will stand out in this crowded market as clear differentiators.

Invest in account management skills: Service providers should prioritize strengthening account management skills to foster deep relationships with clients. This is an important factor in client satisfaction as well as a major consideration to engage the service provider for additional work.

Be flexible: Enterprises like to work with service providers that are flexible. Service provider teams should prioritize client needs and deliver the required service, without being constrained by strict contracts. Flexibility is also a key element in successful management and optimization services, where access to specialists is preferred on an on-demand basis.

“Our clients come back from conferences demanding they need an Automation and a Digital strategy, with no idea what they are”, said a senior partner in a Big 4 consultancy yesterday.

I have never known a time in the world of business when there is no much hype, confusion and unsettlement. Sadly, we are now living in a world where snippets of soundbites are so intensely shared across the variety media we use (I nearly said “omnichannel”) that our industry is completely dominated by hype, as opposed to reality.

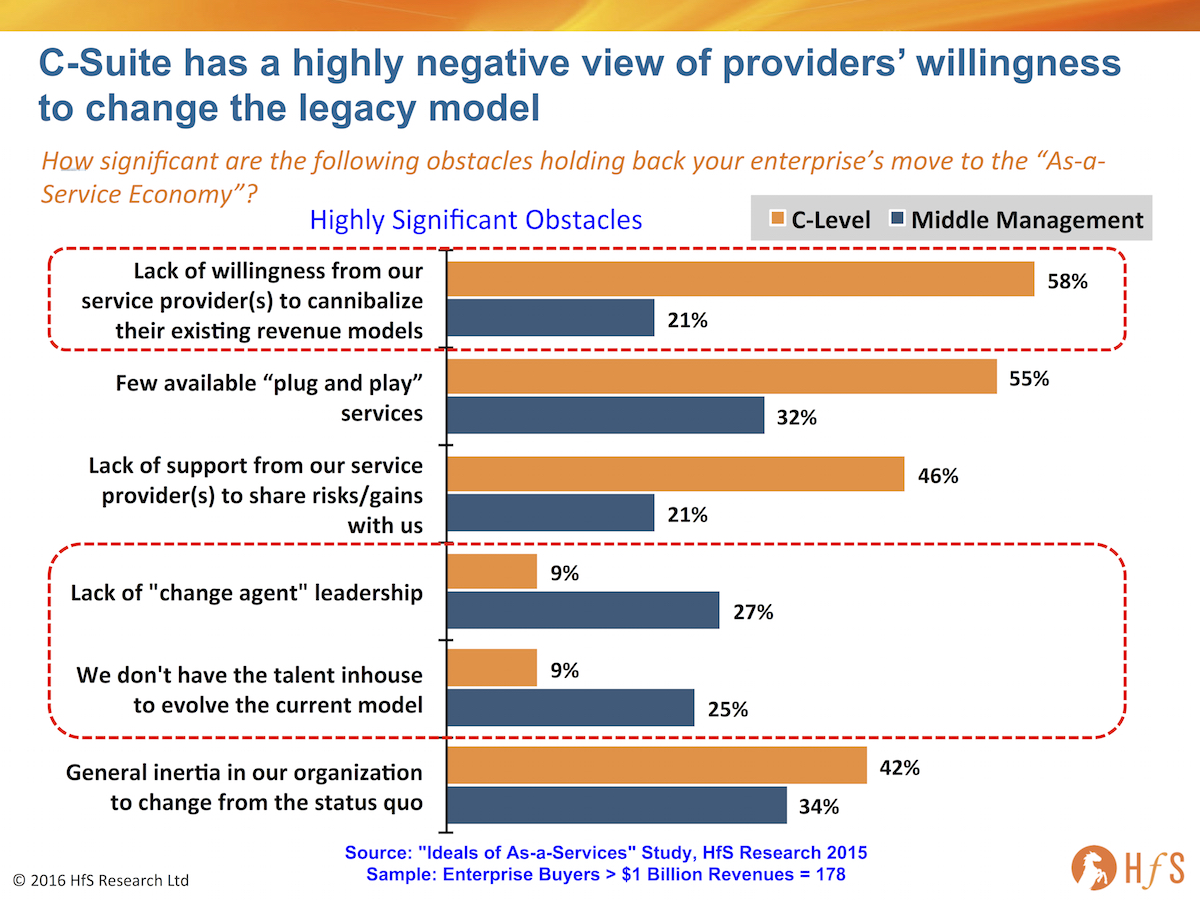

Data from our recent As-a-Service study just shows how alarming this disconnect is… the C-Suite is just living on a different planet from the teams below them trying to keep their businesses functioning:

Click to enlarge

“Cannibalization” is merely the C-Suite waking up to the realization they can spend less with their service providers

Let’s stop beating around the bush on this one – services providers (in most cases) make nice profit margins on their outsourcing deals. What’s happening is that supply is now outsripping demand – there are too many competitors vying for a pool of enterprise clients who want to decrease their external spend. The “demand” is coming from the next layer down of clients (the proverbial “mid market”) which just don’t have the size and resources to warrant the attention of the top tier providers. What’s more, the top tier of service providers is simply not structured to go after the mid-market – they can’t afford to – and are stuck circling the same legacy enterprises like vultures trying to find new ways to squeeze money out of them.

Terms like “Digital transformation” are being used as the new levers to encourage gullible C-Suite executives to part with budget in an oddly similar way ERP was used 20 years’ ago. The only difference being that, with ERP, you would buy a specific product and find very expensive ways to retrofit it into your enterprise, with “Digital” you just spend wads of cash on consultants to try and help you rethink how you do things… and they proceed to retrofit whatever new tech they can sell you to make those things happen.

So… when 58% of leadership sees a lack of willingness to cannibalize, it’s because they have wizened up to the games of the service providers and realize they can get away with spending less, not more. They want their providers to find smart ways to deliver the same (or more) for less cost. So the onus is moving onto the service providers to decrease the headcount provision for their clients and save them money. However, the middle managers actually running the operations know just how hard that is.

You can’t just remove staff from engagements because you automated a process, or eliminated some unnecessary sub-steps in that process. In most client scenarios, they just rely on too much unique (and usually legacy) technology to be able to create a true technology underbelly, where Automation and Digital functionality is native, that can help them unearth a lot more value for a lot less effort and cost. In their minds, the cost of the pain and disruption it could cause is just not worth the “desired outcomes”. Until those outcomes are proven, the status quo of inertia shall remain.

There’s just a lack of capability and incentive to do anything different

27% of middle management see the lack of change-agent leadership a significant obstacle, and 25% just admit they don’t have the talent. Only 9% of the C-Suite feels this way. The two go hand-in-hand – you need change-agents to incentivize workers to do things differently, and you need workers with the skills and expertise to learn use new systems, technologies, analytics and understand evolving business models. The middle management working the real operations realize this, while their leaders are convinced they can just saw-off their legacy and move to the promised land of As-a-Service. It’s a worrying disconnect and something that needs to heal for progress to happen.

The Bottom-line: The industry is piloting the next generation of solutions, but real action won’t happen until we see real, proven business cases

I’ve been amazed at the sheer number of Robotic Process Automation pilots and deployments that have sprung up over the past 18 months. Our forthcoming F&A-as-a-Service blueprint report will reveal just how widespread this is. Providers like HP, Accenture, TCS and IBM have been particularly active here.

In addition, there is a lot of enthusiasm for Digital initiatives – Genpact’s Lean Digital initiative is being talked about by several clients, and I have been highly impressed with Cognizant’s approach to “Being Digital” – they really get that this is a business model transformation, not just another app-dev play with Digital sugar-frosting. And I like the approach to As-a-Service which Wipro’s new CEO, Abid Neemuchwala, is driving. Plus, there is some pretty cool stuff being cooked up from Accenture’s operations group with its innovation networks and rethinking how they deliver their services.

So let’s not get too despondent about the world of confusion in which we currently live – once we really start to see the results of these early phase initiatives, I predict we’ll see a lot more “real” investments from enterprises to saw-off their legacy and changing how they run their businesses. This disconnect between leaders and managers will heal over time, just like it did 20 years’ ago.

One of the cleverest (and most subtle) pieces of branding you will ever see… but just think of the Design Thinking the branding agency applied to come up with this:

So how do you build a business where not a lot of people understand how you make money and many assume you’re a not-for-profit that provides the industry with free research?

The answer is simple: flood the market with a daily dose of insight and have everyone feel part of what you are doing. Make your information company open, social and collaborative; make everyone feel like they are a “client”, even when they are not. Make people want to spend time reading your stuff and also invite them to weigh in with their views and opinions.

Do you feel like a member of Facebook, or LinkedIn, even though you probably never gave them a dime? Of course you do – and you probably don’t think too much about their business models… However, because we do get asked about ours’ frequently, we thought is high time to reveal the secret source of our business model… in all its naked glory:

We make money selling premium research.

In case you haven’t noticed, we are producing over 30 awesome flagship Blueprint reports this year, each encapsulating an entire market, profiling and rating all the key service providers and defining the process value chain, the key trends and dynamics. That’s the core 30 services markets in the industry across IT Services and BPO. That’s a lot of research. On top of this, we produce service provider profiles, market sizing forecasts and a services price benchmarking service, PriceIndicatorTM , that is widely adopted by the services industry. Service buyers, providers and advisors all pay us subscription fees to access these services. More and more service provider selection decisions, today, are being made with the insights from an HfS blueprint.

We make money selling access to our analysts.

You want to find out how to get value from today’s RPA platforms, or how much you should be paying to process insurance claims in Colombia, then call us up. But I have bad news for you – you’ll need to be a subscription client if you want us to answer the phone. Our subscription clients get time allowances to have on-tap analyst support with their strategies – whether these are quick fire one-hour inquiries, or half day strategy sessions. We also do custom strategy projects from time to time, whether it’s a new market assessment study, a marketing strategy review or simply interviewing buyers to write about their experiences.

We make money orchestrating a huge global community.

We attract over a million visits a year to our websites and have well over 100,000 subscribers who regular access our ongoing research insights. We are constantly conducting both quantitative and qualitative research studies with our network, which forms the lifeblood of everything we do – sharing real-time market insights and dynamics with our clients, and performing exhaustive interviews with buyers to learn about their experiences and the performance of their service providers. We also get an average number of 500-1500 people on our regular webcasts, which provide a genuine window to interact with our community and share research insights.

Plus, our analysts get to conduct service provider reference calls independently of the same old rose-tinted clients who are the few willing to go on record regarding the performance of their service providers.

We make money selling research to buyers.

At HfS, we diversify our business across service buyers, service providers, consulting firms and investors to make our money. The biggest issue here is that if you are restricting your firm only to selling to tech vendors/ service providers, your growth is restricted to a small universe of clients. If you can cater your research to tech users and service buyers, you have literally tens of thousands of prospects out there. And you have to be objective when selling to buyers – they know when your research is too biased towards your sponsors.

We run the best buyer summits in the services industry, that bring together the physical experience with the electronic.

In today’s era of information overload, digital bullsh*t, fantastical claims of “disruption”, impending employment apocalypses, and just general confusion, there is more appetite than ever from enterprise service buyers to get together and decipher reality from the marketing hype. At HfS, we have created the community platform to bring together the global services community in private, unvarnished discussion forums. When we invite senior service buyers to attend specific summits to get involved in our community, many sign up as research clients because they see close up how valuable the HfS experience is. This is how we sell – we share the experience with people and they want to become clients. Simple or what =)

The Bottom-line: The HfS experience sells itself

Our golden rule is simple: if you’re going to give something away for free, it better be worth reading! Enticing someone to give up their precious time to read your insights is one of the hardest things to do. If you can’t create compelling insights, then just stuff all your “research” behind a paywall and invest heavily in sales people to convince clients it’s worth signing up.

However, if you can share a little bit of your experience up front, it’s a much less aggressive sale when your prospects have already seen a glimpse of the goodies they will get when they sign up to the premium stuff. What’s more, you can’t build a global analyst brand in today’s market, if no-one is reading your stuff, networking with your analysts at your summits, and listening to edgy and informative webcasts. What worked 10 years ago no longer works today. The big established analyst brands will survive because they are a destination amongst the confusing clutter of information and wannabe experts all putting their stuff out into the market. The second and third tier analysts are struggling – and some are fading fast – because they just can’t command a global audience with a compelling research experience.

You may have heard we just announced our first-ever Working Summit for Buyers in San Francisco at the St. Regis Hotel May 26th – 27th. The summit’s theme—Vision 2020 for Intelligent Operations—brings together the IT and business process services industry’s brightest minds and stakeholders. Seats are limited and available at no cost to well-qualified senior buyers. So, if you are interested, pencil us in your calendar and apply for a seat now.

Unvarnished Discussion Sessions

The State of the As-a-Service Economy and Intelligent Operations: Is It Here?

Evolution or Revolution: What does the Future really Look Like?

The Current State of Intelligent Automation – what’s working and what’s not for buyers

Service Automation: Robots and the Future of Work

The Digitization of the Finance Function

Co-inventing for the As-a-Service Economy

Hiring for As-a-Service Skills and the Role HR must play in the As-a-Service Economy

The evolution of Omni-Channel for CRM: What is it really, and does is exist?

Analytics and Big Data in the As-a-Service Economy… what’s really coming next?

Getting ahead of Trust and Security in the As-a-Service Economy

The C-Suite Advisor – Buyer Face/Off

The C-Suite Service Provider Shootout

Featured Discussion Leaders

Mary Lacity, Curators’ Professor, University of Missouri

Lee Coulter, CEO Shared Services, Ascension Health

Allison Sagraves, Chief Data Officer, M&T Bank

Phil Fersht, CEO HfS Research

Carol Britton, CPO, Bank of New York Mellon

Charlie Aird, Global Leader, PwC Shared Services and Outsourcing advisory

Chip Wagner, CEO Alsbridge

Dave Brown, Global Lead, Shared Service & Outsourcing Advisory at KPMG

Dennis Howlett, Co-Founder, Diginomica

Dilip Vellodi, Chairman and CEO, Sutherland Global Services

Jay Desai, Senior Director, Enterprise Outsourcing, AbbVie

Gajen Kandiah, Executive Vice President and General Manager Cognizant Digital Works and Business Process Services

Harry Wallaesa, CEO, The W Group

Jesus Mantas, Head of Global Business Services, IBM

Joe Frampus, Partner, Avasant

Kevin McDonald, VP of BPO Governance, The E.W. Scripps Company

Leslie Willcocks, Professor, Workforce and Globalization, London School of Economics

Mark Voytek, Partner, Ernst and Young

Michael Corcoran, Head of Strategy, Accenture Operations

Pradip Khemani, Head of Global Business Services, Blue Shield of California

Scott Furlong, Partner, ISG

Shantanu Ghosh, SVP & Global Head – CFO & Transformation Services, Genpact

Srinidhi Rao, Head – Service Management and Process Excellence, Juniper Networks

Tony Filippone, Senior Vice President, Outsourcing Management, AXIS Capital

Robin Rasmussen, Partner, HR SSOA KPMG

Vishal Sikka, CEO Infosys

Wesley Bryan, Co-Founder, OneSource Virtual

HfS Analysts

As usual, we’ll have a full contingent of HfS analysts on site to present the latest data and stimulate discussions. In San Francisco, we’ll have Phil Fersht, Charles Sutherland, Barbra McGann, Fred McClimans, Melissa O’Brien and Reetika Joshi.

Stephen Hawking warns us that AI would be the biggest – and possibly the last – event in human history;

The Guardian (bless them) even highlights Scientist Moshe Vardi’s view that the oldest profession in the world is under threat of being robotized (interesting…).

The beauty of all these wild predictions is that few will remember who made them in a couple of years – or the fact they were made at all. That’s the beauty of being an analyst/visionary in today’s market – you can make up any old fantastical crap and never be held accountable for it in the future. (Not that I have ever been guilty of said behaviour…)

Most of these claims are moot, as most of these “jobs” have already been automated away, or moved offshore

Let’s dissect this quickly:

Rote B2B sales and customer service jobs have already gone away. Forrester’s jaw-dropping prediction is a simple case of analysts predicting things that have already happened to create some headline noise. Most B2B transactional customer service tasks have already been automated, or at least offshored. I’m sorry, but I can barely think of a single instance where I have spoken to a customer service rep, except some instances when I needed to make a large purchase, or I had an inquiry so unique, there was no way to automate it. And even when I do need to talk to someone, I often get scripted responses from some rep in India or the Philippines – my recent complaint to British Airways received some impressive canned email responses from Mrinal Samant, essentially telling me “Bugger off, you’re not getting anything out of us, and the only communication you can ever have with us – these days – is through scripted emailed responses from offshore call center workers.” If the likes of even a BA (long-famed for good service) is doing this, you can bet there’s not a whole lot of fat left for these enterprises to trim in their sales and support ops.

Manufacturing jobs have already been automated out. Sorry to be the bearer of bad news, but if you entered a car plant 30 years ago you may be greeted by scenes of 3,000 workers beavering away. Today, that same plant will be about 50-100 workers and a bunch of machines. It’s already been automated. Of course there is more to come, but I would argue we’ve already seen the worst of it. The biggest future threat are the Apple jobs outsourced to FoxConn in China, where over one million people are employed to make our iPads and iPhones, largely because the circuitry is too intricate for robots. However, new developments in robotics are even threatening to displace these Chinese workers, which could be a travesty for their economy.

Transactional back-office and IT work has already been moved offshore. We cover thousands of IT services engagements, over a 1000 F&A deals and several hundred industry-specific BPO deals – the main proponents of offshore. True, there is room to automate / offshore more processes from enterprises’ operations, but we’re talking relatively small numbers here – maybe 10-20% more labor reduction from some stagnating back office operations (in many cases) over the next 3-5 years. Much of the fat has already been trimmed…

Automation in the back office is about productivity improvements, not direct headcount reduction. Automation is only reducing small tranches of an employee’s time – it’s very difficult to remove an entire office job through automation, you are just making that job more efficient and freeing up that employee’s time to work on something else. Automation in the back office is about closing the books faster, about monitoring systems more effectively, about throwing off better data for analytics, about giving management much greater visibility into their operations, and integrating the back office with the middle and front. Better run companies can then look for people with more creative, socially-intelligent, analytical, innovative skills, once the rote work is chugging along the way it should be. Hence, the bigger impact is coming in the guise of productivity improvements from Robotic Process Automation platforms, better analytics and customer engagement through Digital technologies, and companies simply operating more effectively with better data to make decisions, and staff more focused on providing business value, than merely turning widgets.

Let’s dial back to reality and be honest about what is really happening

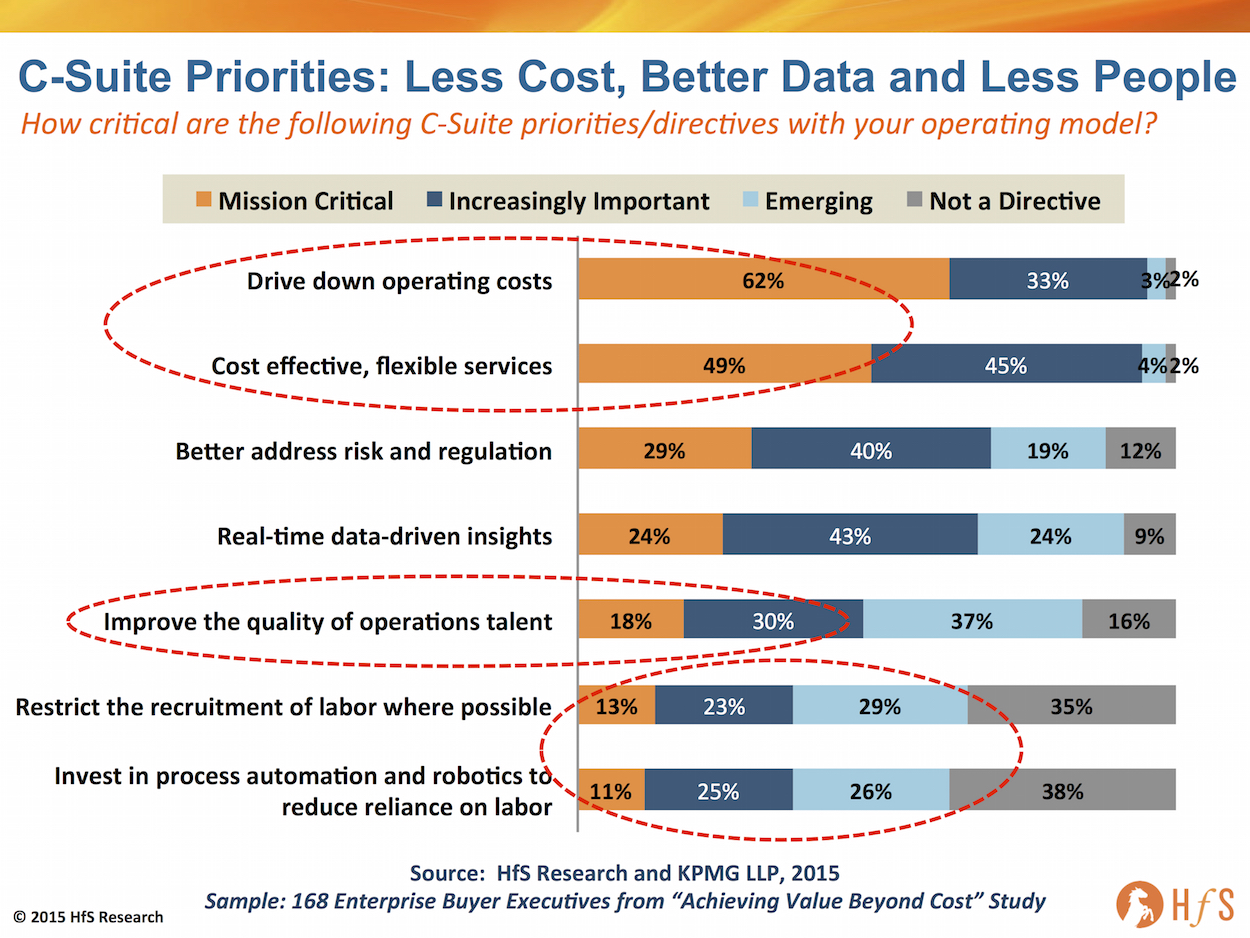

Enterprises want to restrict hiring people to do operational jobs – it’s not that today’s jobs are going away, it’s the simple fact that large numbers of operational jobs will not be created in the future, as enterprises can get what they need with less people. Just revisit our Value Beyond Cost study we ran with KPMG last year, where we asked 168 senior executives about the priorities of their C-Suites with their operations:

Click to Enlarge

What is startlingly apparent here, beyond the fact that well over 90% of C-Suite directives are obsessed with cost and flexible services as operational priorities, is that less than half (48%) view improving their operational talent as important, 65% are exploring efforts to restrict the recruitment of labor where possible, and 62% are looking, with varying levels of interest, at automation and robotics with the specific purpose of reducing their reliance on labor. The bottom line here is very clear – C-Suites are caring less and less about their people, and more and more about their services.

The big question many are facing now isn’t whether to invest heavily in their people – it’s whether to invest in technology to lesson the need to hire staff, or use outsourcing partners to reduce the burden of inhouse staffing cost, while improving their access to flexible services. Or use a combination of the two… or use an outsourcer which is using robotics on itself and is willing to pass on the benefits to its clients desperate to move from a legacy labor-centric operational infrastructure.

The Bottom-line: We have to stop the attention-seeking hype and refocus on the reality of our world

In recent years, the insane uptick of social media and information sharing has warped viewpoints and predictions out of all proportion. Now it feels that the only way people believe they can get noticed is by claiming armageddon is upon us. And the sad truth is, declaring doom and gloom may be their only avenue left to get some attention.

As we’ve analyzed, the future is more about the type of jobs we need to create, not the ones we could protect. I can assure you -right now – that the new generation of kids coming out of college are not clamoring to process insurance claims, sit on IT help-desks, input data into payroll systems or manage customer orders. Even if we still had demand for these jobs, we’d struggle to fill them! And most enterprises have figured how to shift these jobs offshore, where there is a cost-effective supply of labor to do these tasks.

Under the bigger threat from automation is the offshore locations which deliver these services, as most are, by and large, very robotizable tasks that smart service providers are already figuring out how to automate using the various RPA and IT automation tools available on the market today. If I were Narendra Modi or Xi Jinping (perish the thought), I would be very concerned that a whole workforce generation needs reorienting to address work activities that are growing in demand, as we are fast approaching a time of labor oversupply for the demand coming from North America, Europe and ANZ. The shift has already happened, we are now experiencing the aftershock of the shift towards the As-a-Service Economy.

So let’s stop trying to peer blindly into an uncertain future, and instead address an exciting present where there is real potential to achieve new thresholds of business value.

Last week, the HfS Leadership team went all in on the 2016 NASSCOM Industry Leadership Forum (ILF) in Mumbai with 4 presentations and panels, dozens of meetings with industry leaders from providers and clients, multiple media interviews and local delivery center visits thrown in for good measure. So myself and Charles Sutherland jotted down our thoughts as we fought off the lurking jet-lag demons on our way back to the States yesterday…

Most refreshing this time around, has been the toning down of the rhetoric and hype, as most of the providers tackle the winds of change threatening a worrying decline of growth in the global services industry.

From this year’s proceedings, we have taken to heart the near ubiquitous discussion of “Digital enablement and Disruption” to construct a sentiment analysis of where the stakeholders in ILF currently find themselves in their transition from a world of legacy operations to delivering what HfS has termed the “As-a-Service Economy”.

From enthused to unsettled, service providers sober up as reality sets in

In a word, we felt the sentiment of the ILF sessions in 2016 is best described as the global IT services industry being “unsettled”. Last year, we saw the pervasive adoption of “Digital” as the driver of future growth for every service provider at ILF, with a different definition in every instance as to what it meant. The ILF sentiment in 2015 was “enthusiastic” in a word. Over the the course of the past year, we believe most of the service providers are awakening to the degree of change necessary to move to a new model that delivers Digital value based on technical capable offerings, untethered to huge incremental headcount investments.

While seeing some early client successes, most smart service providers are also questioning whether each is as differentiated in their capability and messaging as they believed a year ago. It is becoming abundantly clear, as the industry wakes up to the reality of what is really needed to evolve to the As-a-Service economy, that the differentiation points between service providers has become blurred – and being able to demonstrate true distinctiveness and differentiation from each other has become a very difficult task.

If in 2015, every service provider at ILF wanted to brief HfS on the excellence of their Digital offerings, in 2016 the conversations were inquiries, seeking to test the efficacy of a service provider’s messaging against that of competitors and against buyer requirements and expectations.

Six Factors causing this “State of Unsettlement”

So what has caused this change to a State of Unsettlement, amongst the service provider community in just 12 months? In short, we believe it has been a mix of six factor factors, namely:

A rise in global economic uncertainty, exacerbated by the instability of the Brazilian, Russian and Chinese economies, record oil price lows, a volatile and unpredictable stock market globally and the creeping threat of deflation;

The rise of new “born in the cloud” competitors, such as: Aason, Bluewolf, Equiniti and OneSource Virtual which can offer significantly more cost effective solutions and different delivery models;

The increasingly viral adoption of Intelligent Automation in service delivery;

A recognition that Digital is not just a supplemental technology spend to the legacy business, but a fundamental change in how the underlying business model operates (for clients and for service providers);

The increased relevance and disruptive competitiveness of nimble mid-sized service providers (IT and business process) that can scale up and down aggressively to win deals, based on client needs and their own intentions to invest in the future model, such as EXL, Genpact, Hexaware and Virtusa;

Increasing engagement with mid-market clients, which frequently have requirements as complex as the high-end, but cannot spend anything like the same amounts. Many of these clients will form the FORTUNE 500 of the future and most traditional service providers are simply not equipped to take these clients on profitably with their current delivery models.

We believe these six factors are culminating to provide a growing recognition of the level of change required in sales, solutioning and delivery, in order to achieve or maintain market leadership in the emerging As-a-Service Economy.

Why the Global Services industry must align to the Eight Ideals of As-a-Service as to find its path to a Digital Future

We came to this view after we analyzed all of our discussions during the week with the lens of the HfS Ideals of the As-a-Service Economy. These Eight Ideals – as shown in the following exhibit – are the necessary change management and solution capabilities required to succeed in this new world.

Click to Enlarge

These Ideals resonate with leaders of both service providers and enterprise clients, looking for a way to understand the path that needs to be followed to succeed in the future. Yet, their adoption is not a binary achievement. No existing service provider suddenly executes against an Ideal at the flip of a switch, however much that might be wished. Instead, it is a journey of change and internal transformation as these Ideals are often dramatically different in nature and intent from what has previously created success in IT and business process delivery for the last few decades.

There are nuances to the realization of these eight Ideals across the different service providers, which all demonstrate varying vertical and horizontal capabilities. In short, no service provider can boast they are “all things to all people” like so many claimed in days gone by, but instead they need to focus on those areas where they can be truly distinctive and have real capability to take their clients to the As-a-Service promised land.

This sense of unsettlement at ILF 2016 comes down our recognition that the leading service providers are still very much swimming in a state of transition towards achieving these Ideals. Every one of these Eight Ideals formed part of the discussions on service provider strategies and investments, however, the depth and breadth of client experiences to-date against each Ideal is still very much at an early stage. Hence, the level of inquiry and intrigue form service providers as to how they were faring against each other, and how to make each Ideal more extensive in the year(s) to come.

Why we view Intelligent Automation and Design Thinking as the initial critical ideals to address

This was the first NASSCOM event, or any services industry event for that matter, where we had experienced a genuine atmosphere of honesty and humbleness that the winds of change are upon us and real shifts and investments need to occur for healthy industry growth to continue. There was a wide recognition that simply focusing on driving down costs and selling more aggressively will become futile as those service providers, which can genuinely decouple headcount from delivery, and can scale their offerings to suit the needs of clients of all sizes, will take over the leadership of the market.

The two main Ideals we believe service providers must urgently address over the course of 2016:

1) Intelligent Automation. Automation, coupled with offshore delivery, is the future of the industry and the only true way to decouple labor costs from scaling service delivery. Having a more automated offering allows service providers to take on the emerging mid-market deals more profitably. It also allows incumbent service providers to defend client contracts at the high-end, where the threat of disruptive competitors offering large efficiency savings through automation is emerging in an increasing number of competitive contract renegotiations. In addition, those service providers with great confidence in their automation capabilities, will be the most successful at stealing business from legacy incumbents failing to do enough to protect their existing contracts when they come up for renewal.

2) Design Thinking. The biggest single issue with today’s services relationships is the fact that only 20% (see link) are considered “collaborative” by clients. However, both the C-Suite and middle management recognize (see link) that having joint creative problem solving and “Design Thinking” with clients is a real way forward to embrace the Ideals of As-a-Service.

Click to read more about the move to the As-a-Service Economy

It is our firm belief that if service providers and clients can embed the principles of Design Thinking into their relationships, they will quickly become more collaborative in nature, and both buyer and service provider can really begin working together in earnest to achieve common goals and business outcomes. In short, As-a-Service is about a business model transformation – and how it can be empowered by Digital technology, made more effective and Intelligent by Automation and Cognitive Computing, made possible by smart change management and made trustable by proactive security deployment. Hence the need to design this seismic change, in terms of both talent and solutions, is what holds the keys to the promised kingdom.

Design Thinking is helping several relationships inject lateral thinking and renewed motivation to work together, not only in the customer-facing front office, but also in the back office operational functions. Design Thinking in services is based, primarily, on both service buyer and provider coming together to create business outcomes that are mutually beneficial – and motivational – for both parties. However, this must be established as ongoing collaboration across all key relationship stakeholders, and not simply two days of senior management putting sticky notes on each others’ foreheads. There must be senior pressure and buy-in to adopt Design Thinking as a means to move away from Six Sigma-obsessed old world models, and really change the way the service buyer and provider teams work together.

The Bottom-line: What to watch for in 2016

We firmly believe 2016 will be the year in which both Intelligent Automation and Design Thinking come to the forefront of the sourcing and services market. It will be the year when service provider leadership teams are sent to design camps, and a whole new set of conferences and workshops will feature Intelligent Automation and Design Thinking as their theme of the moment. Some of this may be hype, or even unnecessary, but at the root of it, the arrival of Intelligent Automation and Design Thinking into the mainstream of the IT and Business Process services world makes sense to us as a way to re-imagine more effective process-based solutions for this increasingly digitized As-a-Service world.

Further out, we really see the development of solutions comprising more Ideals of As-a-Service, most notably advances in predictive analytics for Accessible and Actionable data, Holistic Security and cognitive computing extensions to Intelligent Automation as providers and buyers seek the ultimate nirvana of Plug-and-Play Digital Services, but we firmly believe that Intelligent Automation and Design Thinking are the major Ideals to help write-off the legacy of the past and prepare for the value that is possible to attain in the future.

Amidst the relentless robo-hype in our current era of robotic rhetoric, it’s fast-emerging that many buyers and service providers are really struggling to work together to create workable Robotic Process Automation initiatives – in many cases, neither are willing to make the necessary investments, trade-offs or sacrifices to make his work.

Amidst the relentless robo-hype in our current era of robotic rhetoric, it’s fast-emerging that many buyers and service providers are really struggling to work together to create workable Robotic Process Automation initiatives – in many cases, neither are willing to make the necessary investments, trade-offs or sacrifices to make his work. A momentous event occurred in the world of Robotic Process Automation (RPA) today, when its pioneering vendor, Blue Prism, became the first pureplay RPA vendor to announce officially its

A momentous event occurred in the world of Robotic Process Automation (RPA) today, when its pioneering vendor, Blue Prism, became the first pureplay RPA vendor to announce officially its

Oh boy – the amount of fantastical claims we are being spoon-fed by some experts in the market today is just getting a bit absurd:

Oh boy – the amount of fantastical claims we are being spoon-fed by some experts in the market today is just getting a bit absurd:

Most refreshing this time around, has been the toning down of the rhetoric and hype, as most of the providers tackle the winds of change

Most refreshing this time around, has been the toning down of the rhetoric and hype, as most of the providers tackle the winds of change