Just stare at that digital underbelly… there’s a lot of work needed down there!

When the news broke last month about the second largest IT services merger of all time (after the 2008 HP-EDS whopper), the reaction among the services cognoscenti was – and has continued to be – one of confusion. Big services mergers have just not done very well over the years. HP/EDS was a culture clash of immense proportions – and occurred right before the great recession, while other mergers, like Dell’s acquisition of Perot, has resulted in the old Perot business being flipped over to NTT Data at a significant loss, and the Xerox/ACS merger has been shaken up and spun off and needs a major reinvention under new CEO Ashok Vemuri to get the company back on track. Meanwhile, Capgemini and IGATE are still figuring out the best pieces of each other to mesh together, while not taking their eye off the ball, during the services industries’ most cut-throat transition phase.

We heard HPE CEO, Meg Whitman, excitedly address the firm’s key clients and industry analysts at HP’s recent Discover event in Las Vegas, with an obsessive focus on “digital transformation” and the impending impact of “digital disruption”. However, the real opportunity for HPE isn’t really in the design of digital business models for clients, it’s the enablement of them – it’s the provision of the agile “digital underbelly” to make digital change really happen for enterprises.

It’s easy to be cynical about legacy IT services, but there’s an awful lot of it to scrap over as enterprises are forced to fix their plumbing

Digesting the merger of these two struggling services giants has resulted in more rumination than most, considering the timing, sheer scale, transitional uncertain market and motivation. This is not a time when most traditional service providers are looking to add more global delivery scale to already large foundations – most are trying to slim down their delivery armies and sales forces, choosing to focus on new and emerging areas for growth and getting more services delivered for less FTEs by taking better advantage of automation technologies, standard SaaS platforms and more affordable cloud provision.

However, when you consider only $15 Billion is being spent on public cloud services (IaaS) this year and $ 1 trillion being spent on services tied to traditional services delivery, there is a huge amount of “legacy” IT and BPO business in play – for another decade and beyond – to enable the enterprise digital experience. Hence, the opportunity HfS sees for Newco, is to attack the IT and operations plumbing necessary to enable the fast-emerging Digital enterprise, and take on the likes of IBM, NTT/Dell, Atos, Capgemini and the Indian-heritage majors.

Why the Digital underbelly poses a massive opportunity for cost-effective agile IT infrastructure providers, such as the HPE+CSC Newco

The onset of digital and emerging automation solutions, coupled with the dire need to access meaningful data in real-time, is forcing the back and middle to support the customer experience needs of the front. Our new study on achieving Intelligent Operations (see link), which canvassed 371 major buyside enterprises, reveals two key dynamics that are unifying the front, middle and back offices:

A “customer first mindset” is the leading business driver driving operations strategies. Over half of upper management (51%) view their customers’ experiences as impacting sourcing model change and strategy, which is placing the relevance and value of the back office in the spotlight.

Three quarters of enterprises (75%) claim digital is having a radical impact. We can debate the meaning and relevance of digital forever, but the bottom line is that enterprise leaders need to (be seen) to have a digital strategy – and a support function that can facilitate these digital interactions and data needs. The old barriers, where staff in the back office don’t need to think and merely oversee operational process delivery, and those in the middle, which only venture a part of the way to aligning processes to customer needs, are fading away.

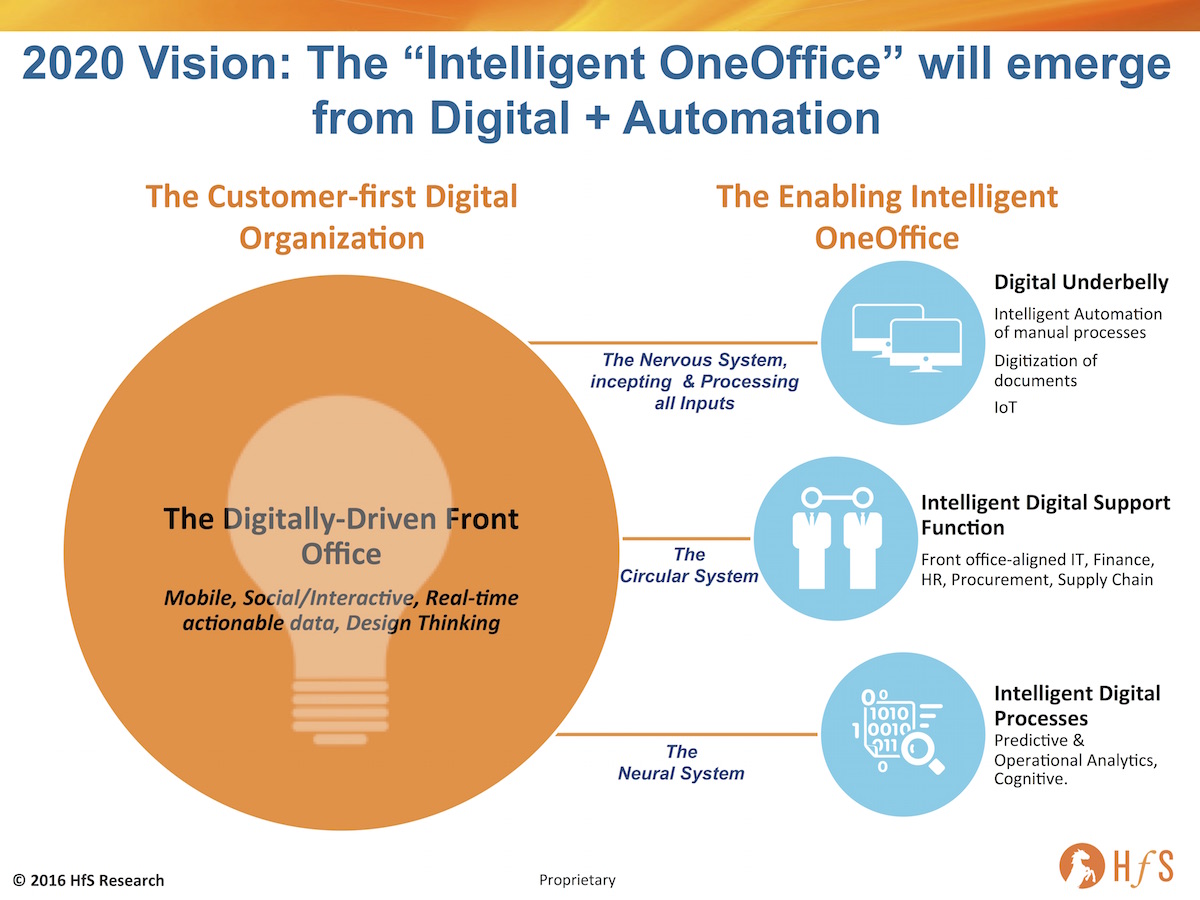

Consequently, we’re evolving to an era where there is only “OneOffice” that matters anymore, creating the digital customer experience and an intelligent, single office to enable and support it:

Click to Enlarge

The Digitally-driven Front Office drives the Digital Transformation

Digital, in its purest form, is all about transforming the business to create, support and sustain the digital customer experience. It’s about leveraging the omnichannel (mobile, social and interactive technology) and accessing meaningful analytics to make it happen. Digital enterprises need a support function to service those customers, get their products/services to market when they want them, manage the financial metrics, understand their needs and future demands and make sure they have got the talent which truly understand the outcomes of their work.

In their current forms, HPE+CSC has some real capabilities in industries like travel and insurance to lead the market here, but is its stated digital focus is going to be in the operations and infrastructure rather than on design and industry expertise; it will struggle in markets against service providers with very strong digital design practices, such as Accenture Digital and Deloitte Digiday. In fact, Newco would be smart to partner with these firms to provide the digital underbelly capabilities at scale.

The Digital Underbelly creates the building blocks

Digitally-driven enterprises must create a Digital Underbelly to support the front office by automating manual processes, digitizing manual documents and leveraging smart devices and Internet of Things, where they are present in the value chain. Smart enterprises have realized they simply can’t be effective with a digital transformation without automating processes and fixing manual interventions and breakages in their process flows. Service providers can get ahead by working with their clients to make their processes run digitally so they can grow successfully their digital businesses and create new growth for themselves. Think about a central nervous system that incepts and processes all the elements necessary to make the enterprise function.

This is where HfS views the sweet spot for Newco, provided is can really optimize the economies of scale with the merger to be price competitive with the Indian heritage majors, such as TCS, Wipro, HCL, Infosys and Cognizant. It also needs to convince clients it brings world class engineering talent, security and automation expertise to the table.

Intelligent Digital Support breaks down the legacy functional silos

Enterprises need their support functions (like an enterprise circular system), such as IT, finance, HR and supply chain, to be aligned with supporting the customer experience, as opposed to operating in some sort of vacuum, hence, we are terming this “Intelligent Digital Support”, where broader roles can be created. HPE and CSC together have tremendous depth in areas like finance and accounting, contact center and HR from HPE’s traditional services business, while CSC brings it’s newly acquired procurement capabilities from its Xchanging acquisition.

Newco’s focus needs to shift towards creating a work culture where its delivery staff are encouraged to spend more time interpreting data, understanding their clients’ needs at the front end of their businesses, and ensuring the support functions keep pace with the front office. This is especially the case in industries that are more dependent than ever on real time data, using multiple channels to reach their customers and being able to think out-of-the-box with disruptive business models.

Intelligent Digital Processes must help enterprises predict and orchestrate, as opposed merely to react and maintain

Newco much focus on enabling business processes that align with their clients’ desired digital customer experiences. It’s not about throwing off historical data just to discover what went wrong, it’s about being able to predict when things will go wrong and finding clever ways to get ahead of them. It’s about embedding smart cognitive applications into process chains, about learning from mistakes and new experiences along the way. This is the enterprise neural system. Several of HPE’s IT service competitors have already made strides here with autonomics platforms, such as IBM’s Watson, TCS with its Ignio , Wipro with Holmes, Infosys with Mana and Accenture’s evolving partnership with IPSoft’s Amelia. Without a genuine story in service orchestration and autonomics, Newco could quickly fall behind, as its customers become increasingly eager to embed cognitive and self-learning elements into their business and IT processes.

However, one key service orchestration platform where we see some real growth potential for Newco is with CSC’s industry-leading ServiceNow practice, which has enjoyed continued growth, especially following its 2015 acquisition of Fruition Partners. As CIOs increasingly seek ServiceNow implementations on their CVs (in a Workday-esque manner), Newco should be able to divert many existing HPE clients onto its newly-acquired managed service. Newco just needs to figure out how to grow that competency as two forces coming together, as opposed to ending up with competing P&Ls.

The Bottom-line: The industry is in transition and the winners are those which can pivot and focus fast. Those which can’t will fail

Let’s cut to the chase here – we’re operating in a services world obsessed with preserving the past and ignoring the new. The past was all about predictable revenue and highly-visible cost reduction opportunity – there was a method to the madness. But this was because the true value was about doing things slightly better, but at much cheaper costs. The future is not so predictable – it is about being smarter, more business aware, and technically superior to piece it all together for clients. Oh, and without increased investments. It’s hard, and requires a very different focus, which is one of developing talent to learn on the job, one of evaluating experiences professionals to assess their ability to change, of being able to learn new tools and platforms, which require a mixture of process and business understanding to align with real business outcomes.

The Newco that is HPE+CSC has as good a shot as most to survive the impending service industry carnage, as growth flattens and prices hit the floor for anything that is a mainstream service. It’s sheer size and client portfolio should help it absorb the blows as the market shakes out and the need for increasingly complex “digital underbelly” services proliferates. As we evolve the levers for the survivors to pull are the right combination of labor arbitrage, automation enablement, cognitive understanding and digital enablement. But spending years constantly reorganizing internally to create the beast to deliver all of this with the speed, affordability and agility needed will not work. These two firms need to be slammed together with an urgency and focus not yet seen in our industry. This won’t be pretty and needs to be like a very sticky BandAid being ripped off very, very quickly…because their biggest threat is within themselves.

For a deeper dive into the nuts and bolts of the HPE+CSC merger, download our POV now!

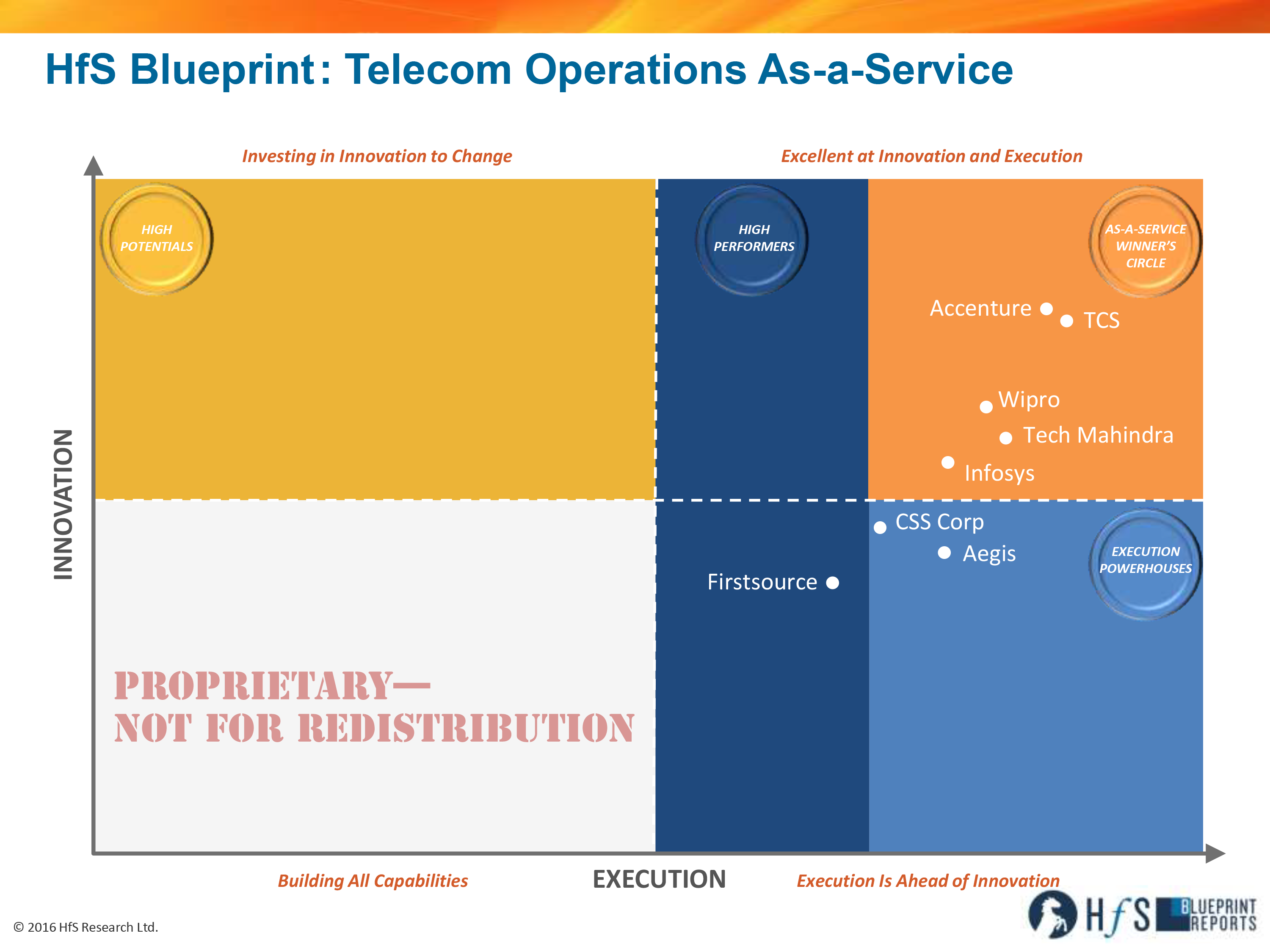

HfS Telecom guru, Pareekh Jain, is back with his second blueprint looking at service provider capability delivering telecoms business services, following his debut analysis at the end of 2014:

Click to enlarge.

Pareekh, how would you describe the current state of Telecom Operations As-a-Service?

We describe this market as a under-penetrated market. Our research suggests the current global telecom operations market (i.e., business processes under network, fulfillment, assurance, and billing) is perhaps one-third of $10 billion potential.

The telecom market is perhaps only vertical market with the dubious distinction of both enabler and victim of the digital transformation. Telcos have enabled cost-effective communication with likes of WhatsApp, Skype and in turn, they have eaten telco’s lunch. Telcos worldwide are struggling to find their right place in the digital world. As-a-Service solutions can enable service providers to help telcos to prepare for the digital era. The As-a-Service is the model today and for the future in telecom operations services.

Tier 1 telcos have generally been early adopters of telecom operations services. Now, there is an opportunity to provide services to Tier 2 and Tier 3 telcos, too leveraging As-a-Service solutions. As-a-Service solutions are driving growth in this market.

The eightservice providers we evaluated for this Blueprint approach this market in essentially two ways. Service providers with strong IT offerings focus more on non-voice solutions whereas pure-play BPO service providers focus more on voice-based solutions. Service providers with strong IT offerings have taken the lead in platforms replacing legacy stack, plug and play business solutions, intelligent automation, holistic security, design thinking, and collaborative solutions while analytics and social is on the agenda of all telecom operations service providers.

How has that changed since our inaugural Telecom Operations Blueprint in 2014?

Pareekh Jain is Research Director, HfS (Click for Bio)

Even back in 2014, we could see many ideals of As-a-Service present in service providers’ offerings. In the last two years, As-a-Service momentum has accelerated.

Compare to our analysis couple of years back, we see the rise in collaborative engagements driving business outcomes. Analytics is now embedded in most of the engagements. Service providers are launching new services incorporating design thinking. We see more examples and use cases of automation. Also, telecom operations service providers are becoming effective brokers of capability by partnering with IT, platforms, local construction companies and telecom domain experts.

We see industrialization of few new service offerings such as network rollout management, revenue assurance in last two years. Also, service providers are constantly innovating with developing further new offerings to solve telco’s pain points incorporating design thinking.

The heartening development is that we see elements of As-a-Service ideals in new contracts more than in existing contracts. These new contracts are either of new greenfield operators or MVNOs. We see some existing customers moving to As-a-Service ideals when renegotiating deals with revised scope.

Tell us, Pareekh, which service providers are leading this market today?

Our HfS Blueprint methodology assesses service providers against a variety of criteria related to Execution and Innovation capabilities of the service providers based upon buyer reference calls, market interviews, RFI submissions and detailed market briefings.

The service providers in the As-a-Service Winner’s Circle are the providers that scored highest on both Execution and Innovation and included: Accenture, Infosys, TCS, Tech Mahindra and Wipro. These service providers are all process experts and stood out for the excellence of delivery operations, solution expertise for all telecom operations processes, the plans for As-a-Service, usage of platforms, and investment plans.

We identified two service providers as Execution Powerhouses—CSS Corp and Aegis—both new to our 2016 Blueprint that excel today in the execution of telecom operations services and are making investments in innovation that should enhance future operational solutions as well.

Finally, we also identified one High Performer service provider in Firstsource, which is leveraging its expertise as a pure play BPO service provider in delivering services in different channels for telcos too.

All service providers are offering capabilities to meet the needs of today’s telecom customers.

What can you predict will happen in the next 2-3 years for telecom operations?

We see four major developments in next 2-3 years in telecom operations,

The first is that analytics offerings will evolve from operational analytics to business analytics. Some service providers already embed analytics in their all engagements. We believe analytics will become all pervasive for all tier-1 service providers.

The second is that intelligent automation and, in particular, robotic process automation (RPA) will become deeply integrated into telecom business processes reducing the size of current labor arbitrage–centric contracts.

The third is that with automation, omni-channel and self-service initiatives the share of voice channel will decrease. Subscribers will use voice for complex issues. So while the share of voice channel will decrease, the average handling time (AHT) will increase and service providers will require higher quality talent to support it.

The fourth is that network rollout management offering by service providers will become extensive. Also, we will see introduction and maturity of new telecom operations services offerings. Service providers will figure out their value proposition in IoT value chain and support telcos in capitalizing on IoT opportunity.

Futuring Gerd Leonhard will keynote at HfS’ Cognition Summit this September

Now we have finally managed to get past that frightfully riveting conversation about doing some rudimentary process automation with our invoice processing and customer collections (aka RPA 1.0), we can finally get to the heart of what new technology capability – much of which is already here – is really doing to our world.

With human brain power and computing power on collision course to become one, the enmeshing of human behaviour and thought processes with self-learning and self-remediating cognitive systems is set to confuse, frighten and – ultimately – inspire us to change our whole approach to managing our technology investments, making data meaningful, collaborating with work colleagues and creating new business models.

This is our goal, this September, in White Plains, New York, where we are, once again, bringing together the diverse stakeholders of the operations and services industry to get past the fear, and find the inspiration to drag us out of this transition phase, in which we currently find ourselves.

Phil Fersht, CEO and Chief Analyst, HfS: Good evening, Gerd. Great to have you on the HfS platform today! We’re very excited to have you join us at Cognition, our coming flagship event in New York this September. But maybe before we start, could you give me just a little bit about your background and how you’ve ended up as such a visionary in the Artificial Intelligence (AI) Space these days?

Gerd Leonhard: CEO of The Futures Agency: It’s a long story. I’m a futurist. But I started as a musician and producer, and then in the late ’90s I went on the Internet and I did a bunch of music startups. It was an interesting time, but I was too early and ahead of my days. I think I realized in about 2001, when everybody went bankrupt that my vision was better than my implementation. So basically I realized I was very good at seeing things ahead of time a little bit. Then I wrote a book called “The Future of Music,” which led to me being called a futurist.

Then over the years, the last 15 years, I’ve branched out into media, marketing, advertising and then ultimately, of course, technology and software. And now I run this company called The Futures Agency. There is about 25 of us and we’re essentially what we call futurizing businesses. So we help companies, organizations and governments, to reinvent how they do things—what they’re going to be in five years. And, of course, a lot of that has to do now with big data, artificial intelligence, cloud computing and digital transformation.

Phil: In terms of the way you see things going in the AI space, you’ve come up with some very interesting thoughts around Digital Ethics. The fact that governments and society need to take a stronger viewpoint, even a stronger regulatory viewpoint in the impact of technology on society and jobs and that sort of thing. Maybe you could share a bit more of your views and opinions here?

Gerd: Yeah. I think it’s pretty straightforward, Phil. First of all, we have to distinguish between intelligent assistance, IA. Which is really what we’re seeing these days, mostly. Then AI and then AGI, which artificial general intelligence. So IA really is anything like Google Maps and Siri—things that give you a simple assistance by having a sort of a minor brain in the cloud. You can speak to Siri but not much will happen. You can use Google Translate, but it’s kind of all minor stuff. There is no super computer in the cloud doing what Watson does.

Artificial intelligence as the next step, where you can actually have deep learning computers that are not being programmed—and this is the Google’s DeepMind, for example. This will be the self-driving car that says, “OK, I can learn how Gerd is driving. I can learn the environment and then I can act accordingly and add value beyond the programming.” That’s really what we’re seeing as the big hope of artificial intelligence: to solve very large, very complex problems like social security, air traffic, environmental control, desalination.

To basically do that with computing power that is unheard of, like a million times that we have today. At that point we wouldn’t really understand how this artificial intelligence does things. We would just know that it does it infinitely better than we do. So that’s all happening in the next few years. We’re going to realize very quickly what Ray Kurzweil calls the Singularity, which is maybe six or seven years from now, when the first computer will have the capacity of the human brain.

At that point, it becomes entirely feasible to outsource major decisions to machines that we don’t know, whether they are right or not and how. At that point, it’s basically imperative for us to use what I call the precautionary principle—which is to say that we should use this, but we should make sure that we can still control it in some way, or at least find a human leverage to it. It goes all the back to the discussion of the three laws of robotics, right? But basically at a certain point there, there is a very big question about technology going beyond our actual control and actual understanding. At that point it may become dangerous, not in a sense of Ex Machina or so, but in the sense of technology basically ruling what we do, so as a consequence we become kind of like machines. We’re forced to comply.

I think that creates all kinds of issues and ultimately, when I speak to businesses, everybody wants to use technology to be more efficient and to make more money, and to create some margin. Which is understandable. But in the end, if you have a business that’s just algorithms and just efficiency, you have no value. Because it’s a commodity then. That’s important to remember.

Phil: So Gerd, looking at how the impact on the future of work and jobs dominated the conversation at our recent event in San Francisco, we came to conclusion that a lot of the kind of the work that’s been automated today aren’t jobs that we would create today, in any case. These are legacy-type jobs that were created maybe 10, 20, 30, even 40 years ago to fulfill tasks. Now they should be automated and should be run electronically. So the bigger issue now is: How do we create work, not necessarily save legacy jobs? Is this something that you would agree with or do you think we need to go further than that?

Gerd: That’s a complicated question, Phil. First of all, I think we need to decouple work from income. So the possibility of doing work that you want to do is extremely fulfilling, but it may not make money. For example, building a playground for your kids or staying at home with your grandmother or writing a book, or whatever. Lots of us think about work as something that makes money—and that will have to stop, because, basically, technology will afford us to work a lot less for the same money because it becomes infinitely efficient and abundant.

Just like music and films are already abundant, other things become abundant, including food, transportation, electricity, energy. That’s about 15 years away. So at a certain point we have to say, it’s great if we make money with this. But maybe we can just make money and also do the work that we want to do, at which point it’s not really important if technology would remove that or not, we would do it anyway just because we want to.

The other thing is that, there is some work that can be automated that we probably shouldn’t automate. So this is a very important decision for government, for employees, for employers and for HR departments. For example, hiring and firing, in my view, should not be automated. It should use the tools, just like I use Trip Advisor to evaluate a restaurant, but I would never rely on Trip Advisor in a sole, exclusive way. It’s just a data point. So if I use IBM Watson for hiring or firing, I think that’s kind of taken to the extreme. It would probably be wrong and also unethical in many ways.

So I’d say a lot of people are always saying that technology removes the bias as an objective thing, and that’s absolutely not true. Technology will have whatever buyers were using to build it. Or whatever data give the AI to learn, is going to create the same kind of bias, right? So we shouldn’t pretend that there is no bias. We should just take it as it is and take it as a data point for a human evaluation. My view is that the jobs are shifting up the food chain, the Maslow Pyramid, basically from the very simple taken-care-of-stuff, to the meaningful or the self utilization, the purpose, the brand, the story telling, the emotional, the human thing. That’s basically what all our jobs will be in the future.

Phil: So we obviously have a big election going on in the US right now…

Gerd: Ah, really?

Phil: This is not really being discussed and it should be, in my opinion. Looking out in the future, at job and wealth creation and the impact of technology, it doesn’t seem have hit the big political conversation yet. Do you think this will happen in the next couple of years? When do you think this will become a much bigger, more societal conversation?

Gerd: We’re having a conversation in Europe everywhere now. In Switzerland, we had a referendum on the basic income guarantee. It didn’t go through this time, but we voted on it and it’s been discussed in lots of places. Basically, I think the government and the US government is looking at this. I know they have a special commission that convened for artificial intelligence. I dare say that Trump probably doesn’t know what it is, but in general I think all governments need to look at this and say, “OK, technology will really solve a lot of these issues and make it abundant, make it possible, make it cheaper in the end.”

For example, right now the cost of healthcare and medical are rising, they’re not decreasing. But ultimately when technology solves this, they can decrease. And that’s a very positive thing. In return, there are other issues that governments have to look at. For example, application of authority, dependency, addiction, which is a huge thing—we’re already at the point of where we feel kind of lost if we don’t have a mobile with us. That’s kind of a childish thing, right?

But think about five years from now, when you’re literary connected to the cloud at all times. You cannot function, like air or like water, if you’re not connected to the cloud. I think at that point we’ve closed the barrier toward human existence that is probably scary. And it’s probably not a good idea, just because it’s more efficient. That’s something to compare. I always say, we should embrace technology but we should not become technology, because when we become technology we lose the value that we have left—which is human, humanity.

Phil: I agree with you there, Gerd… maybe governments need to say, “This is where we draw the line, in terms of when technology does start to take over our lives and our jobs in a way that is detrimental to society at large.” Do you think that is going to happen, when you get to the point where technology becomes a destructive tool rather than a productive tool to society? Do you think that’s going to happen? How could this happen in a way that that could be feasible?

Gerd: I have to say, I’m, in principle, not necessarily for regulation. I’m, in principle, for being able to try things out and innovate the market, and push things forward as we’ve done in the US for a long time. However, there is potential existential risk here. Inventing things that are larger than us, and it’s like we don’t want the guys in Bern, in Switzerland, in the lab, we don’t want them to experiment with the black hole. They could basically make crater out of Switzerland. We need to find a way of saying, “Do what you need to do but without that risk.”

It’s the same with artificial intelligence, with genetic engineering—those are the major two things. And with material and nanoscience, we need to find ways to try this and to investigate it. Then we have to have control mechanisms in place. For example, if we can actually beat cancer by genomic engineering of humans, which seems doable, then we can also build super humans right? Who is going to be in charge? Until we have solved that problem, then we can’t do it. It’s just like the internet of things, we can’t realize the Internet of things until we figured out how they use all that data to its 98% benefit.

Because otherwise, my digital money, my health records, my driving records, my whole, my everything will construct a giant profile of me. Which I’m not afraid of, but I think it’s extremely dangerous when you go about it the wrong way. Until we’ve solved that, then trusting the system to take care of itself, I would say is dangerous. Look at Facebook or Google, Baidu, that sort of thing. They’ll do whatever makes money, which is a good ride in the capitalist system. But it’s still a fairly tilted relationship, Phil, right?

Phil: It is, Gerd. Finally… what can we expect to hear from you, when you speak in September? Anything up your sleeve that you’d love to share with us in advance…

Gerd: Yeah. I’ll share some tips on we can use these amazing technology that are happening all around us in the next five years without getting too many of the unintended consequences. And I think it’s also really important to realize that efficiency isn’t the final destination. People are always looking at technology and saying, “Oh, great, I can fire 80% of our call center staff to make it more efficient.” That’s probably all true, but at the same time, what is the value of a business that has so little people and so little purpose, and so little humanity in it? We have to think about what that means. Maybe sometimes it’s better not to automate and to keep the human value, even if it’s more expensive. So we have to think about what that means ultimately as to where we want to go and where we want to be in five years. I always say, it’s a combination of data, intelligence and humanity that will be the winning factors in the end.

Phil: Gerd, we cannot wait to meet you again and hear your talk, and I can tell you you’re going to have a very excitable, knowledgeable and passionate audience – see you in September!

Dinanath (Dina) Kholkar is Global Head of Business Process Services at Tata Consultancy Services

As we endlessly debate the future of the global IT service delivery in the wake of advances in automation, digital disruption and the ability to maintain double digit growth rates, one area that has steadfastly kept to respectable growth and improved delivery confidence is our beloved business process outsourcing services.

In fact, we are about to reveal to all of you that the growth in Indian-heritage BPO has been consistently out-performing IT services over the last year. Why? Because BPO is several years behind IT in terms of widespread adoption, but is now coming to the forefront as processes can be better-enabled by cloud platforms and maturing global delivery models.

In this vein, I thought it timely to interview Dina Kholkar, TCS’ global head of BPS, who has helped steer his division to $1.9 billion at a 6% growth clip… making BPS now represent 12% of the total TCS business…

Phil Fersht, CEO and Chief Analyst, HfS: Good evening, Dina. It’s great to have you on HfS for the first time. You’ve been one of the best kept secrets behind the exciting growth in the Business Process Services (BPO) team at TCS. Maybe you can share a little bit about yourself, your own background and how you ended up leading the highest-growth division in TCS today.

Dinanath (Dina) Kholkar, Vice President and Global Head of BPS at Tata Consultancy Services: Sure, Phil. I’ve been at TCS for a very long time. This is my 27th year in TCS! I started in 1990 as part of the IT business. I managed a few IT projects, went on to manage accounts across different geographies, different types of roles. The longest stint I had was in the capital markets area. I also spent a few years in TCS’ R&D unit, predominantly focusing on data warehousing and data mining. Those were the years when data had started becoming a focus in many organizations. I did have a stint in operations when I was managing customers, but I never really managed the business of running operations until I got the opportunity to manage e-Serve, which TCS had acquired from Citibank. After a few years, when it was integrated into TCS, I took on the role of the overall head of the TCS BPS business. So we’ve had quite an exciting and an interesting journey, a journey filled with lot of learning and a lot of customers we’ve been able to positively impact over the years. And I feel quite proud about the type of opportunities that I have gotten and the way I have delivered on the objectives that TCS has laid out for itself.

Phil: So what can you share with us then about the secret sauce at TCS? What is it that makes you guys really tick?

Dina: One thing which I have always seen probably over multiple generations—and all three CEO leaders of TCS—really strikes me is the customer centricity. We go the distance, which means we do whatever we need to do for the customer. We do the right things and ensure that we are taking care of the customer’s business, bringing all we have as an organization to solve problems that the customer has. I think that customer centricity is paramount in the organization. I think we also support and move with our customers. And a lot of our customers have enabled us to expand, to diversify, and take those new skills to new business lines. For example, we were predominately an IT business, but many of our customers felt we could expand and provide business process services and infrastructure services, which is why we started delivering those services.

I think customers have benefitted from our service predominantly because of our relentless focus on them. And, more holistically, look at Tata Group over a long period of time and you’ll understand the philosophy that we bring into doing the business, the ethics that we have and the overall commitment to society. There is a lot of pride in what we have managed at TCS and in the Tata Group. All in all, I think it is very important for us to delight our customers and continue to make a difference in society through the companies that we work for.

I think it’s really an ecosystem and an environment which is exciting to work with. And it’s a joy to collaborate with my colleagues. There is never an instance where I needed help and didn’t get it. You know there are always people wanting to help you whenever you need it.

Phil: So, Dina, when we look at the inflection point that’s going on in BPO services today, where do you see the challenges and opportunities for a firm like TCS? And how do you see TCS getting ahead of this disruption curve?

Dina: I would say, let’s step back and look at TCS as an organization and the way we actually started the entire BPS business. We focused predominantly on the core part of the customer’s business from an operations point of view. So in a way we actually disrupted the typical functions of operations by actually focusing a lot on the core part of the domain. The reason why we did that was we believed that, with the DNA of IT and innovation transformation we had, we could actually present more value to our customers right from the time we engage with them.

The entire idea about IT-BPS synergy and bringing value by leveraging technology into core operations is pretty much driven by us an organization. The entire digital economy has been a great change for us because it enables us to digitally reimagine our customer’s business. So when we look at where we were with BPS as a business a few years ago, we were managing SLAs, focusing on operational metrics. We have now moved and matured into leading change, influencing the entire digital journey of our customers and clearly making a difference to the business metrics. And with that, we have connected to business heads—to the CEOs and the CFOs and even in some cases the board members of our customers that we service. So clearly, I think BPS as a business has the potential to make an impact through the entire journey companies take as they embark on Digital Re-imagination™.

From a challenges perspective, clearly we have a large workforce which predominantly focuses on managing and running day-to-day operations with a significant amount of repetitive tasks. And as we drive our robotic automation agenda, using some of the relations that we are building that specifically focus on cognitive learning, we will definitely see a need for driving a lot of competency development initiatives to retool and retrain our people. And that is a journey we have already embarked on. You might have heard about the entire focus that we had on digital—within the BPS organization itself, specifically around data science and automation.

We have already started the journey of retooling our people, getting them to a different set of competencies which are required as the new order sets in the BPS organization. As far as disruption goes, we may not necessarily come up with solutions within the space we currently operate in. The disruption we will look at will be in areas where we don’t necessarily have a focus. We can potentially bring in disruption using some of the cognitive learning solutions that we are building and you will soon see some of these make an impact as we roll them out.

We are working with TCS’ Digitate unit, which has developed ignio™—enhancing it and focusing on certain areas which we believe have the potential to disrupt the marketplace and make a big difference to the entire Digital Re-imagination™ journey of our customers.

Phil: That’s very interesting. So, as we look at shifting value propositions towards outcomes and getting away from this linear scale that we have been obsessed with for so long, there has been a lot of talk about Design Thinking. How do you think this can be applied to BPS? Is this something that you, at TCS, are taking seriously?

Dina: Absolutely. You know, one of the things which I have been driving personally, given the businesses that I manage, is a multi-industry mix. One of the biggest themes that I have been driving is the interconnectedness of technology-leveraging the solutions of one industry for a completely different industry. Design thinking has been a very integral part of our entire journey. We have been embarking on building relationships with some of our partners in academia. We have a very strong alliance with the National Institute of Design in India and the Royal College of Arts in the UK. Plus, you may be aware that we have created a design studio in our Santa Clara office, where we bring in people with different capabilities and different types of skills to solve core problems. It is not just about creating solutions for the current set of issues that our customers have in their businesses, but about helping them completely reimagine their business.

You may be aware that as part of the BPS business, we launched our ValueBPS™ framework. Design thinking has been an integral part of the entire framework. We have been able to bring in different levers to solve customers’ problems, and these solutions that we are creating are very high on business impact. So as a leader, I have completely relooked at how we are currently selling value propositions to our customers and how we are bringing value to our customers.

And as I mentioned, the agility and the ability to actually make a big impact to the business is playing a big role in the way we are going forward. So the very core of our entire approach is the design thinking mode and we do believe that there is a tremendous amount of potential to help people in different walks of life solve problems from the perspective of a consumer of the end-service. And I think that will make a lot of difference to the industry.

Phil: So I am going to get to my final question here, Dina, which is: If you were given the keys to the BPO kingdom – and you rule the BPO world for one week – what’s the one thing you would do to change this industry for the better?

Dina: One thing I see when I look at the industry is that it has not gotten the credit for the knowledge and expertise that it really provides. If you really look at the types of services that we provide across industries, across different geographies, the tremendous depth of knowledge that the industry has is phenomenal. And one key difference is that we’ve probably not looked at the mechanisms of learning and specifically using cognitive learning. I believe that this can really disrupt the industry. It can learn global systems and learn about businesses across the board. A combination of people who have the expertise in running some of these operations, in creating solutions plus machine learning will make a big difference in the industry.

Today, the industry as it exists is probably a small fraction of what potentially is there as a market. And I personally believe that bringing in machine learning into the entire industry would free up people who have the expertise and the ability to do much more intellectually challenging things. Mobilizing that skill would be very important. So I would primarily focus on what is it that we can do to reimagine the BPS business itself. If we talk about Digital Re-imagination™ in the context of our customers, why can’t we reimagine our business? And I think that will be the key thing. What does Digital Re-imagination™ really mean to our business?

And one of the key things which we will look at is how to leverage the multiple levers that are available—what we call the Digital Five Forces, including cognitive learning and artificial intelligence. This is one key element I would drive. We have a huge amount of human capital in the industry, and how we are able to maximize the benefit of that human capital will make a difference to the industry as we go forward.

Phil: That’s a fantastic answer, Dina =) I really appreciate your perspective today and I look forward to sharing it with our community. It’s great to hear about the energy and the passion behind the TCS BPS business, which has been growing so well. So thank you very much for your time today.

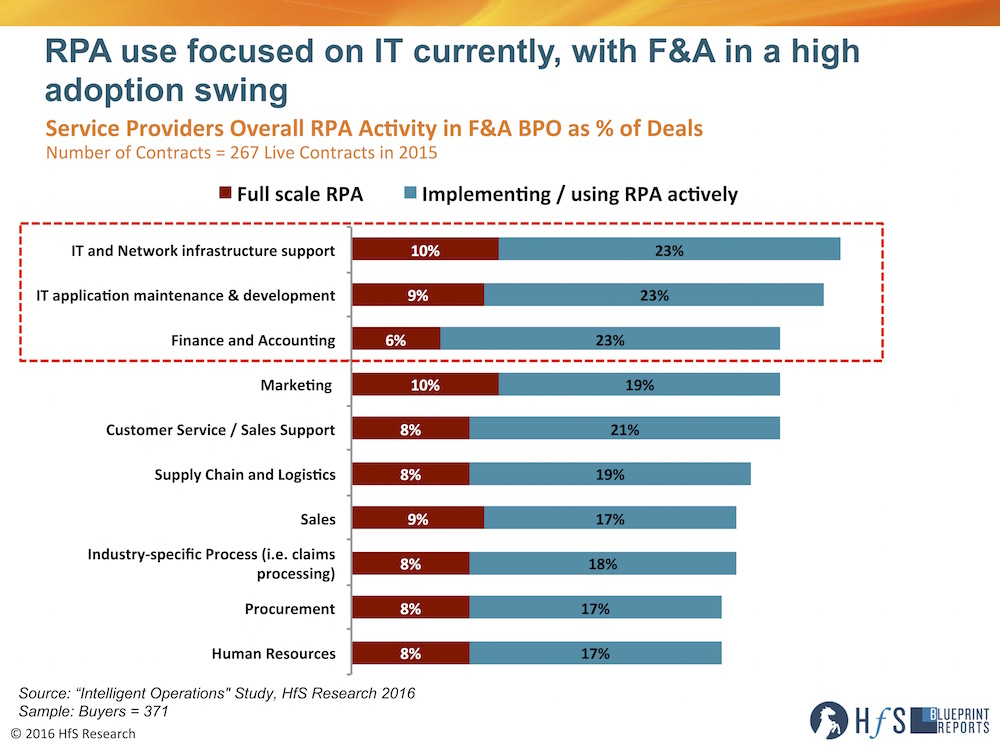

RPA 1.0 is a done discussion. We know what it is, we know what it can do, we know how it can augment operations and help digitize broken processes. To this end, our brand new study on Intelligent Operations, which canvassed the dynamics of 371 global enterprises, already shows a third of them are very active with RPA within their IT and finance and accounting processes:

Click to Enlarge

RPA is here and being adopted at a fast clip

All the incessant RPA hype has done its job – it has literally dominated IT services and BPO conversations at every conference, provider strategy deck, advisor “new practice” press release and many buyer converations. Indeed, we can even forgive those cheesy sales presentations from guys who suddenly claimed to have 20 years’ experience as automation pioneers and talked about bot farms as if they were actually hand-raised on one…

The overwhelming conclusion is that a large chunk of enterprises are actively implementing it, and 10% even claim to have full scale RPA platforms up and running (let’s not dwell too much on the finer points of defining RPA here – the bigger picture here is the obsessive widespread focus, testing and deployment of automation tools).

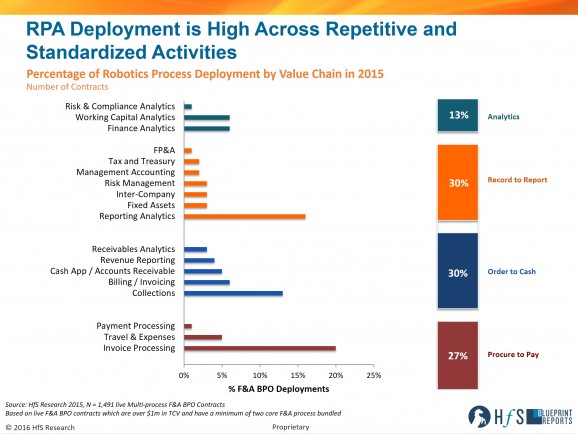

What’s also significant is the deployment across processes that have been beset for so many decades by manual interventions, such as invoice processing and collections, in addition to higher knowledge-value areas, such as reporting analytics; this graphic illustrates the RPA implementation activity across all live F&A BPO engagements from our recent F&A-as-a-Service Blueprint report:

With the market moving so quickly, let’s not get overly-obsessed with this snapshot view as it’s likely to change considerably in the next couple of years, but you can already see how embedded the leading BPOs are getting deploying RPA elements into their existing engagements to advance the old model away from manual processes and shape up delivery into a more digital environment. When you look at the shift to the Intelligent OneOffice, RPA is a key component of the digital underbelly, which we describe as the nervous system of the emerging digital enterprise:

Click to Enlarge

The Bottom-line: RPA is just one of several levers to pull for enterprises to achieve a true Intelligent OneOffice

Automation is just part of the story as enterprises look to bring the back office in line with the middle and front – albeit a very important one, as many enterprises will simply fail if they cannot digitize many of their core processes (and decide which ones to focus on, as they cannot digitize everything). Being suffocated by manual interventions, legacy applications and mainframes, still reliant on spaghetti code and COBOL, is becoming such an irritating impediment holding back so many enterprises from benefiting from operating in the digital world. RPA is just one tool to help get there – and it’s now here and ready to use. So let’s advance the conversation to driving the circular and neural systems of the enterprise to really make the shift by orienting our talent, creating data access capabilities that are predictive and cognitive… which we can use meaningfully to create opportunities, not simply react to them.

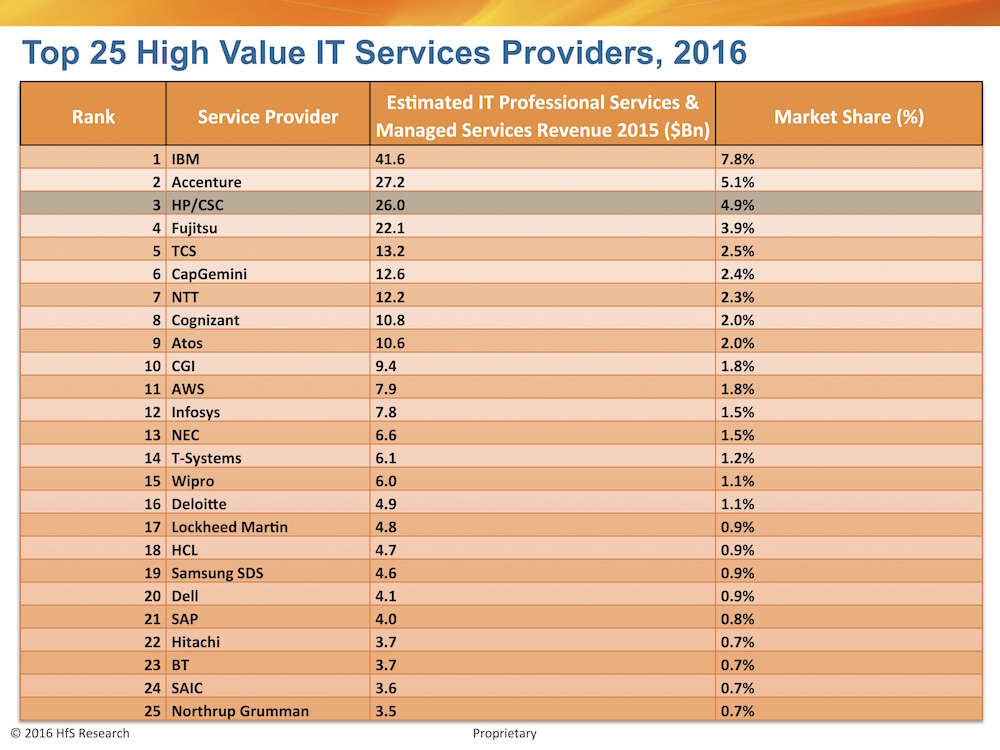

Love this merger or loathe it, the marriage of HPE and CSC has just spawned the third-largest high value IT services provider in the world – and happened just in the nick of time for our 2016 HfS IT Services Top 25:

Click to Enlarge

So, let’s ask HfS’ lead analyst for market sizing and forecasting, Jamie Snowdon (bio), how we fleshed out “High Value IT Services” from the general morasse of IT services:

We estimated all this data from services provider financials. Revenues are fitted to nearest calendar year. We attempt to make the IT services numbers as close to HfS definition as possible—as part of this exercise we exclude revenues from subcontracting, we don’t include BPO or business services revenues in this definition and some product services revenues were classified out of scope, if the equipment serviced is not IT – for example, telephony related equipment. These numbers do not include software-as-a-service, unless included within a broader managed services agreement.

Jamie, how did you come up with the $26 Billion number for the new HPE?

The merger of HPE Enterprise Services and CSC, brings together the high value services of HPE and the commercial revenues of the old CSC business. The $26 Billion revenue figure takes $8 Billion as CSC without the hived-off public sector business, and $18 Billion from HPE Enterprise Services division, much of which was the acquired EDS business unit.

And what’s your initial take on the merger, before we get deep into the weeds of the broader implications?

This deal brings together two of the original outsourcing behemoths EDS and old rivals CSC. The reasons for the merger given by management focus on the scale of the new company. Certainly scale was an important requirement for IT outsourcing providers in the past, as it gave flexibility and economies to these asset and labor intensive businesses. However, in asset light world of modern IT managed services and the increased use of automation – scale is not a vital component. It does give them access to the very largest of global deals, but HPE, and depending on location, CSC, would have been able to handle anything that crossed its desk. What we have is two large services businesses that have spent the last 3 years hemorrhaging revenues, because they weren’t offering what many enterprise clients wanted or there was another provider able to do the same task cheaper and more nimbly. This issue is not going to be resolved by this merger. The two firms have to reinvent themselves as a modern services firm when contracts are more open-ended, value is counted in revenue growth, not just cost savings and scale is replaced by other features such as agility and innovation as the key differentiators.

It suddenly dawned on me what the core issue is with the future of the workplace: the simple fact that company leaders and their stakeholders started viewing employees as walking costs at some stage over the last 30 years, and have devoted a huge amount of focus and energy trying to figure out how to remove as many of them from their business as possible… without it impacting the top line.

Surely, people, human labor should be viewed as a valuable commodity that adds value to a business, not some burden on the profit margin that needs to be eliminated at all costs? So what’s really gone amiss here?

Enterprises hired people into jobs they no longer value. Over the decades, our enterprises have ballooned with staff hired to provide inputs into process chains to keep them ticking over – whether they were writing lines of spaghetti code to make processes flow from one subtask to the next, or producing reports out of SAP for a historical view of the business some manager will archive away somewhere. Or taking customer orders over the phone… or faxing insurance claims from doctors’ surgeries and inputting the data into some system. Today, many of these jobs could have been avoided, if these enterprises had simply invested in a better suite of software applications (which may not have been available 10-20 years ago), or cost-effective service providers were on hand to do the work – and were trusted enough to take it on. Today, the vast majority of enterprises are trying to figure out how to eliminate these jobs that they themselves created in the first place.

People have just stayed consistent to performing tasks that now fail to align with today’s desired outcomes. Many of the staff hired to produce these tasks just haven’t evolved into doing anything else. The only innovation in their lives is going from Windows 8 to 10, or adjusting to the latest Oracle upgrade. On the surface, this isn’t their fault – they are merely performing tasks they were hired to deliver. In reality, they should be smart enough to realize their job is becoming legacy and should be working with their employer to find areas of the business to work on where they can add real value. “Let’s talk about my role” is usually a welcome discussion to have with your boss to work out additional areas you can focus on that align with the evolving goals and desired outcomes of the business.

People have grown entitled to being employed and lost sight of their value in the workplace. Some people simply think they deserve a chunky paycheck because they turn on their laptop and forward around a bunch of emails, perform a series of rudimentary tasks that just about check the “enough not to get fired” box. It amazes me how some people have hugely over-inflated views of their own self-worth and self-importance to the business. People need to take a serious look at the value they deliver to their employer – do they help bring in new clients? Do they go out of their way to keep existing clients delighted? Do they produce work that is unique and differentiated? Do they do things that are very distinctive and hard to find in the workplace today? Are they proactive and actually do things on their own initiative that they were not merely instructed to do? Get a reality check, people…

The workplace ethos is no longer about creating a safety net for people. Ugh – but it’s true. Employers, by and large, only care about themselves and pay lip service to their staff to make them think they really care. Just look at people who quit their jobs after years of service and wind up being sued by their former employer who they thought cared about them… This is not a loving, caring, fluffy work environment, people… and this goes both ways for both employee and employer. The same can be said for employees who pretend to love their employer, then shaft them over when something better comes along. This is not a love-fest, this is business. Let’s just be honest with each other about our goals and expectations.

Governments have lost touch with reality. Just watching this US election in full swing baffles me. Politicians are out of touch with the realities of the modern workplace. Make it attractive for employers to hire people again and curb draconian labor laws and payroll taxes. And create tax incentives for businesses to employ and train people… seriously. It’s no wonder so many firms only want to add headcount offshore, where they are not subject to all the risks of hiring locally.

Academic institutions are not aligned with economic reality. Sad, but so true. Are most kids coming out of college truly trained and ready for this workplace? Or do today’s enterprises have to manage all the orientation to mould them into an effective working style? I look around so many industries today and only see aging management teams and pathetic succession plans in place.

The millennial generation mentality is a poor fit for many legacy businesses. When the meritocracy in many firms is still based on the length of service performed, they are going to struggle to create a fruitful environment in which most ambitious millennials can flourish. They want a sense of purpose and a flatter organization structure, a more collaborative style of working that encourages creative thinking and a broader set of work activities that align them with the goals of the business. Apologies to many legacy businesses bending over backwards to change their cultures to adapt to more of a “startup” culture… but my client interactions are not giving me the warm and fuzzies that things are really changing… all that much.

Bottom-line: Fear the next recession, when it comes, as this could get really ugly

The thing I hate about these long, sustained periods of economic growth is the simple fact that enterprises just paper over the cracks of their failings and only deal with them when disaster strikes. And when disaster strikes, the solutions are usually draconian short term measures, like wide-scale damaging layoffs, travel freezes, marketing cuts etc. My fear is the last 6 years of (largely) false economic prosperity has instilled a sense of denial that we need to make deep, painful changes to how we manage people, and how we run our enterprises. When employees are largely viewed as “costs to be reduced” (which is all I pretty much hear from leadership today), as opposed to “people from whom we can source real value”, there is only going to be one likely outcome when the xxxx hits the fan…

Now enjoy your weekend and forget I wrote this cynical distribe =)

The market for talent has seen massive fluctuations over the last eight years. The 2008-9 global recession caused massive employment contractions across all major regions, however, the tide has really turned to turn after one of the longest sustained periods of economic growth in the last 200 years, with the need for fresh talent is on the rise.

Coupled with the rise of the intelligent digital business, these dynamics have forever changed the way organizations have to approach their HR function as seek new expertise and mindsets. As such, optimization and smart thinking across the entire HR stack is a critical requirement to attract, onboard and nurture talent within organizations.

As more and more millennials enter the workplace (now making up a third or staff), employee interaction has to change. The always-on, always-connected workforce is here. Organizations need to adapt HR functions accordingly and embrace mobile and cloud technology that can be accessed anyway and anytime.

Cloud HCM platforms have developed user interfaces that speak to this new workforce, but with ~50% of buyer organizations still using on premise legacy HCM systems, there is still a long way to go for many organizations. By partnering with proven service providers, organizations can now make the migration to the cloud quickly and efficiently. Also by leveraging the managed service expertise of these providers, organizations are more enabled to focus on key moments of truth with employees thereby reducing employee churn and having a more aligned, motivated and focused workforce.

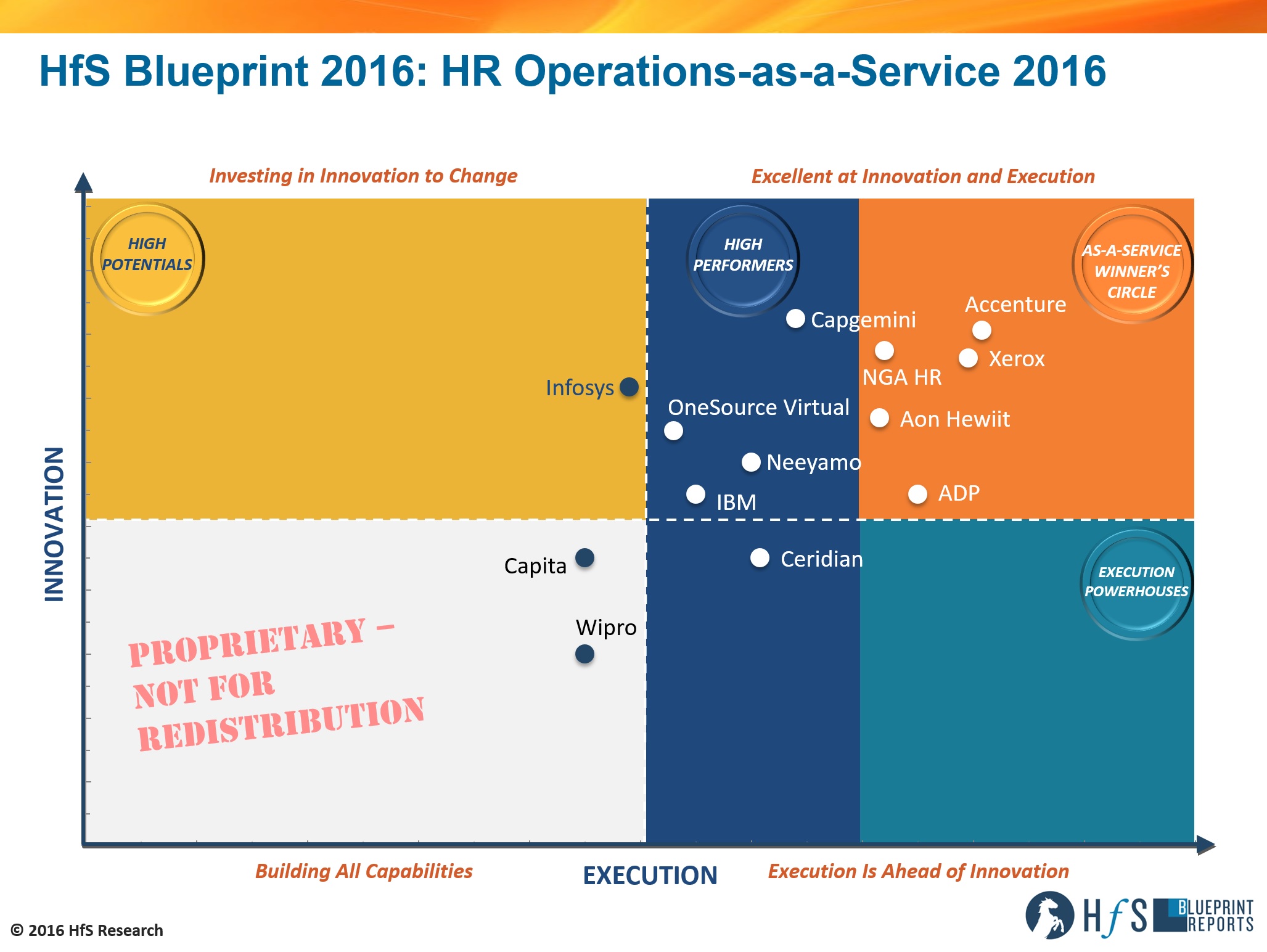

Knowing the importance of these solutions for the very future of HR, we put our best and brightest on this. And the result is HfS Human Resource Services Research Director Mike Cook’s first Blueprint for HfS: HfS Blueprint: HR Operations As-a-Service 2016. So we invited him in to tell us all about it.

How did this Blueprint take shape, Mike?

In this HR Operations HfS Blueprint, we take a look at the evolution of MPHRO to “As-A-Service”–a services market that is increasingly agile, collaborative and employee-centric. HfS considers this transition in outsourcing a move to the As-a-Service Economy, placing increasing value on diverse talent, analytics, and collaboration, as well as increasingly on platform-based services.

To develop this Blueprint, we spoke to service buyers and service providers to understand the innovation and execution capabilities of thirteen multi-national, multi-functional service providers with MPHRO business process support capability in their portfolio: Accenture, ADP, Aon Hewitt, Capgemini, Capita, Ceridian, IBM, Infosys, Neeyamo, NGA HR, OneSource Virtual, Xerox and Wipro.

And how did the service providers perform, based on your research with the buyers?

We want to understand a variety of different things in order to compile this Blueprint. How do service buyers approach business process outsourcing—what is working well and what could use a “rethink” or refresh? How are service providers extending their capabilities for data management, analytics, talent development and management? And how are digital technologies such as automation, social, mobile, and cloud being approached and used; what value are they providing for BPO? In short, how is this market changing to become more “As-a-Service”—business-outcome oriented and flexible through the combination of capable people and digital technology. As-a-Service Winner’s Circle:

Accenture has proven to be extremely forward thinking and innovative in the way it brings MHRO services to market. The service provider has made extensive use of automation, integrated services and technology across its MPHRO stack. The development of HR apps that address multiple HR touch points across the employee lifecycle are a differentiator for the service provider. Accenture also has the “critical mass” to deliver on large multi-country, multi-language deals.

Xerox has focused its MPHRO practice on operational and customer experience excellence. The service provider has received high praise from clients for its on-demand and proactive account management. Xerox leverages it in-house HCM consulting capability, partnerships with “best of breed” HCM implementation organizations and proprietary HR technologies including, Life@Work and DiscoTM, to overcome client’s legacy technology.

NGA HR has proven tactically excellent on delivering the minutiae of contracts. The service provider has made extensive investments in making ResourceLink a plug and play platform as well extending its SuccessFactors, Workday and Oracle HCM implementation capabilities. NGA is also aiming to further evolve into an As-A-Service provider through its ongoing development of automation initiatives.

Aon Hewitt is a well-established and reliable MPHRO service provider. Clients have praised Aon Hewitt’s account management team for its proactive nature and the wider organization for its adaptive and collaborative business model. The service provider has a well-established Workday implementation practice in addition to the development of in-house tools including Total Benefits Administration (TBA) and UPoint.

ADP is the largest global provider of payroll services. The service provider has embraced the As-A-Service ideal of Design Thinking through the launch of its two innovation labs. Through the employee first focus of these labs ADP has launched its ADP Mobile Solutions application, aimed at improving employee experience and reducing frustration.

As-A-Service High Performers:

Capgemini is establishing itself as an up and coming service provider and is a one of the market leaders in delivering on innovation initiatives in the MPHRO market. The organization is implementing elements of plug and play digital business services, analytics and automation within its MPHRO stack. Capgemini now needs to fully develop its RPO offering to transition into the Winners Circle.

The extensive internal changes at IBM have renewed the company’s focus on HR. The service provider is an implementation partner for all the tier-1 HCM platforms and is leveraging its Watson platform to enhance analytics and cognitive automation across client’s operations. IBM does have gaps in its MPHRO portfolio, specifically benefits admin and workforce development services, which it will need to address to enhance its position in this market.

OneSource Virtual (OSV) has a strong As-A-Service mentality in its DNA and has polarized itself through its sole Workday services practice. The service provider has received praise from its client base for its responsiveness to client demands and the way it adapts to new business challenges. OSV has made extensive use of automation in its MPHRO practice through its proprietary Atmosphere Workday automation platform.

Ceridian, a previous heavy hitter in this industry, appears to be moving its focus away from MPHRO service delivery and instead focusing on its proprietary Dayforce sales and implementation practice. The service provider has developed a well-established analytics component into its service delivery. However, feedback from clients has been sub-par on the organizations recent performance.

Neeyamo has proven to be an operationally efficient and responsive service provider. The organization has effectively introduced design thinking into MPHRO service delivery through its innovation hub which has designed the company’s HR tools including Aloha, VMS and White Glove. As-A-Service High Potential:

Infosys is aiming to become an MPHRO service provider of choice. The company has made extensive investments in automation and next level analytics, through feedback received from clients. At present, however, Infosys has been lacking in effectively communicating and implementing these As-A-Service ideals to its client base.

What do we see changing in the future?

In general, HfS believes that the MPHRO market is fragmenting, especially in the Western world, as buyers of services look to implement specific transformational point solutions from service providers as opposed to the previous practice of acquiring end-to-end solutions. This is not to say the MPHRO market is contracting, HfS forecasts the market to grow at 4.5% through to 2017, although it is at a slower rate than the overall HRO market which is currently growing at 6.5% through to 2017.

HfS is also of the opinion that buyers are increasingly seeking support in HR transformation from their service providers. Therefore, service providers, such as Accenture and Xerox, which have a robust consulting practice, are leading the way in this market.

The development of cloud HCM platforms has lowered the entry point to new entrants in the MPHRO market (for example OSV) which has taken advantage of tailoring processes specific to one platform. However, in order for these new entrants to be successful, an in-house, or bought in, application development practice is still needed to deliver on client’s expectations across automation and analytics delivery as the majority of cloud HCM platforms available are still not up to the job.

And what do you see along the road, for MPHRO, Mike?

HfS sees a few areas taking shape where service providers can play a valuable role, although it must be said that it does require a buyer to be willing to collaborate as opposed to traditional directive outsourcing arrangements. Therefore, both parties need to be willing to share the risk and investment. These Include:

Recruitment: This is increasingly becoming an area of focus for MPHRO service providers as there is significant opportunity in the market for process improvements, specifically around the onboarding function. Losing candidates at this stage of the hiring process is both costly and frustrating, although minimal focus has traditionally been aimed at this crucial juncture. The likes of Accenture, Xerox and IBM have all developed services around onboarding which have reduced attrition from successful candidates in client’s organizations.

Analytics: While all service providers have, or are in the process of, developing analytics offerings in support of HR functions, the majority of clients interviewed in this Blueprint still require greater workforce and HR insight. A key point raised by buyers has been the need to link HR data to business outcomes. At present few service providers, with Infosys, Accenture and Capgemini been exceptions, are delivering this next level insight.

Automation: The HRO market has been slow to embrace wide scale automation within service delivery. At present most of the automation available is for simple transactional processes such email actioning. More intelligent automation such as workflow routing and prescriptive HR management functions are beginning to come to market and are in the development or pilot stage with numerous service providers including: OSV, Neeyamo, Infosys, Capgemini, NGA, Aon Hewitt, Xerox and Accenture.

As more than one service buyer pointed out, innovation is often kept back by their own internal resistance to change. The development of innovative HR solutions is fully underway within all leading service providers, although challenges are arising in MPHRO deals in which there are often numerous stakeholders, and therefore opinions, on the buyer side (HR department heads, etc.) and large organizations that are holding onto legacy platforms and processes.

The way forward in this market needs to start at the negotiation phase of the contract, whereby both c-level and departmental execs are included to act as sponsors for change within the HR function and contracts are priced in a way that promotes constant innovation from service providers. Pricing models that have proven most effective include an element of per employee/transaction in addition to outcomes pricing, FTE pricing is dead in the MPHRO As-A-Service environment! Furthermore, there needs to be more collaborative engagement and ongoing industry discussion with clients, in ongoing contracts. The only way for the As-A-Service environment to really take hold in this industry is for organizations to interact in meaningful dialogue with both peer organizations and service providers.

If someone called you “back office”, I’d imagine you’d be a little bit offended. It’s probably not much worse than being called “useless”, or “about to be automated out of existence”…

But I have good news for you back-office rebels – your time spent festering in the backend of yonder is finally coming to an end. Why? Because the onset of digital and emerging automation solutions, coupled with the dire need to access meaningful data in real-time, is forcing the back and middle to support the customer experience needs of the front.

Our soon-to-be-released study on achieving Intelligent Operations, which canvassed 371 major buy-side enterprises, reveals two key dynamics that are unifying the front, middle and back offices:

A “customer first mindset” is the leading business driver driving operations strategies. Over half of upper management (51%) view their customers’ experiences as impacting sourcing model change and strategy, which is placing the relevance and value of the back office in the spotlight.

Three-quarters of enterprises (75%) claim digital is having a radical impact. We can debate the meaning and relevance of digital forever, but the bottom line is that enterprise leaders need to (be seen) to have a digital strategy – and a support function that can facilitate these digital interactions and data needs. The old barriers where staff in the back office don’t need to think and merely oversee operational process delivery, and those in the middle, which only venture a part of the way to aligning processes to customer needs, are fading away.

Consequently, we’re evolving to an era where there is only “OneOffice” that matters anymore, creating the digital customer experience and an intelligent, single office to enable and support it:

Introducing the Intelligent OneOffice, where the barriers between front, middle and back are forever going away

The Digitally-driven Front Office drives everything. Digital, in its purest form, is all about transforming the business to create, support, and sustain the digital customer experience. It’s about leveraging the omnichannel (mobile, social, interactive tech, etc) and accessing meaningful analytics to make it happen. But then you need a support function to service those customers, get their products/services to market when they want them, manage the financial metrics, understand their needs and future demands, and make sure you’ve got the talent that truly understands the outcomes of their work.

The Digital Underbelly creates the building blocks. Digitally-driven enterprises must create a Digital Underbelly to support the front office by automating manual processes, digitizing manual documents, and leveraging smart devices and IoT where they are present in the value chain. You just can’t do digital without automating smartly – forget all the hype around robotics and jobs going away; this is about making processes run digitally so we can grow our businesses and create new jobs. Think about a central nervous system that incepts and processes all the elements necessary to make the enterprise function.

Intelligent Digital Support breaks down the legacy functional silos. You need your support functions (like an enterprise circular system), such as IT, finance, HR, and supply chain, to be aligned with supporting the customer experience, as opposed to operating in some sort of vacuum. Hence, we are terming this “Intelligent Digital Support,” where broader roles can be created. Today’s college graduates are simply not coming out of school willing to perform mundane routine work: operations staff proactively need to support the fast-shifting needs of the front office. So the focus needs to shift towards creating a work culture where individuals are encouraged to spend more time interpreting data, understanding the needs of the front end of the business, and ensuring the support functions keep pace with the front office. This is especially the case in industries that are more dependent than ever on real-time data, using multiple channels to reach their customers and being able to think out-of-the-box with disruptive business models. Of course, we all need to make sure we can keep the operations functioning by paying the bills, responding to customers, processing the claims etc, but if we can’t be proactive and look at how we can create a better customer experience using digital channels, or challenging the logic of running a process a certain way, we’ll never create work cultures that will attract the bright minds to take us forward. People want to feel a part of something and that their work matters – and the best way to do this is to move away from rigid corporate structures of the past, with too many management layers and departments run siloed like mini-empires. We need to invest in driven managers which understand how to motivate and collaborate across business functions. Sales, marketing, customer service, IT, finance, HR and supply chain are functions that all depend on each other to be effective. Smart enterprises are already breaking down the silos and creating multidisciplinary teams, using collaborative tools and Design Thinking methods across delivery centers to help their staff be more motivated, creative and challenging the old way of doing things.

Intelligent Digital Processes can help us predict as opposed to react. And finally… it’s all about designing business processes that align with your desired digital customer experience. It’s not about throwing off historical data just to discover what went wrong… it’s about being able to predict when things will go wrong and finding clever ways to get ahead of them. It’s about embedding smart cognitive applications into process chains, about learning from mistakes and new experiences along the way. This is the enterprise neuralsystem.

The Bottom-line: OneOffice is the real alignment of operations with the business end of the organization

We’ve been talking about aligning support functions with the goals / mission of the firm for decades now, but digital is realigning us all with the true uberlord of the organization – the customer. If our supporting technologies and people can finally respond to, interpret, predict and be part of our digital customer experience, we’ll finally see those barriers stagnating organizations come crashing down.

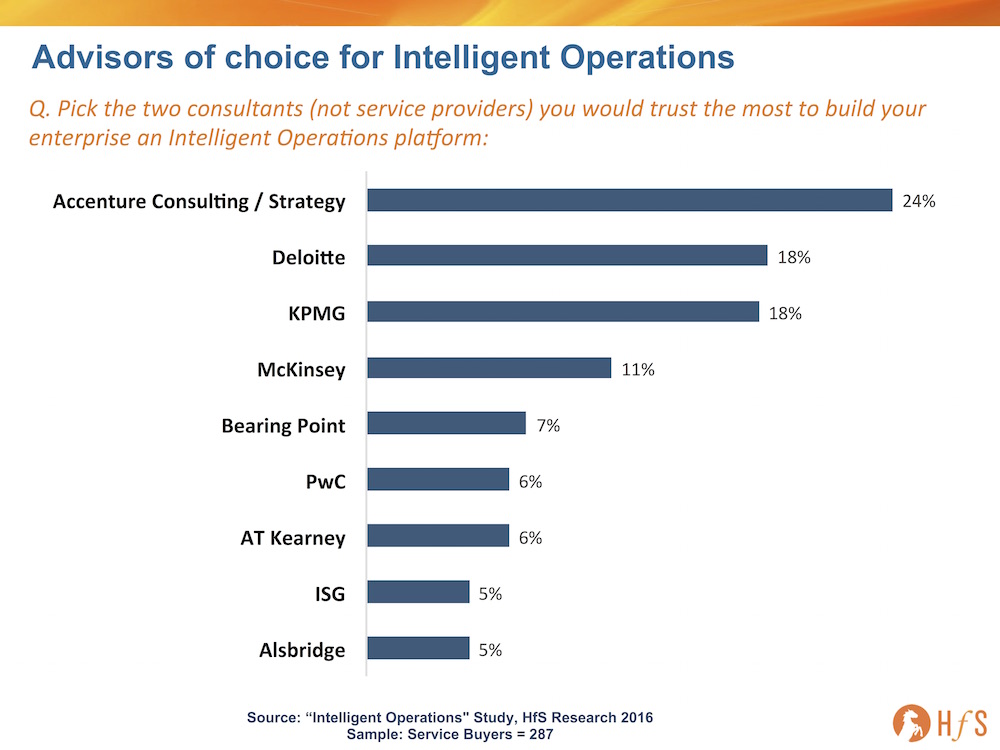

In 1588, the English dramatist John Lyly, in his Euphues and his England, wrote:

“…As neere is Fancie to Beautie, as the pricke to the Rose, as the stalke to the rynde, as the earth to the roote.”

In other words, “Beauty is in the eye of the Beholder”, which just about sums up how buyers perceive consultants when they need some serious rethinking and rewiring done to their operations to make them more intelligent:

Click to Enlarge

So what’s actually surprising here?

In the past, you may have expected to see the pureplay strategy houses rule the roost, however, when we break down the Change Management and Solution Ideals enterprises need to achieve more Intelligent Operations, the focus shifts much more to using consultants with real change management, process transformation, analytics and automation chops… this is less about strategy, and more about just driving through the changes. Most company leaders know where they want to go – it’s now more about executing a plan to get there:

Click to Enlarge

The Bottom-line: We’re moving to a world where the expertise enterprises need to be successful is really changing

One of the above firms asked me recently if it should start an automation practice. My response was “If you’re only asking me this now, then you’re already too late to the game”. In a nutshell, enterprise operations functions need genuine expertise in adopting a mindset to write off their legacy systems and obsolete processes – and a real understanding of how to approach automation and embrace digital opportunities.

A lot of this is about prioritizing what not to automate and learning where digital transformation actually makes business sense. This is about creating an operations function that can pivot and support the rapid changing needs of the front office with actionable data, that is secure and available in real-time. This is about defining and devising a digital strategy that has the customer at the forefront of the business and an operational support function that has the customer experience at its core.

Hence, consultants need talent that can not only think creatively with their clients, but also create an ongoing environment for writing off legacy, embracing change and being smart and proactive about leveraging automation and real digital strategies effectively. The speed at which some of these advisors must make the pivot from merely brokering transactional contracts, or spouting off some high level fluffy strategy, to supporting real change is critical – I’d imagine we’ll know in the next 9-12 months which ones will genuinely be helping their clients achieve these ambitious ideals.

At that point, it becomes entirely feasible to outsource major decisions to machines that we don’t know, whether they are right or not and how. At that point, it’s basically imperative for us to use what I call the precautionary principle—which is to say that we should use this, but we should make sure that we can still control it in some way, or at least find a human leverage to it. It goes all the back to the discussion of the three laws of robotics, right? But basically at a certain point there, there is a very big question about technology going beyond our actual control and actual understanding. At that point it may become dangerous, not in a sense of Ex Machina or so, but in the sense of technology basically ruling what we do, so as a consequence we become kind of like machines. We’re forced to comply.