From An Interview with Charlotte Bui, Global Lead of Design Thinking at SAP

Recently a colleague in common introduced me to Charlotte Bui, Global Lead of Design Thinking at SAP, and I chatted with her about how design thinking is used with SAP clients. I’m sharing snippets of this interview to get you thinking about how to use design thinking in your work, and in your partnerships and outsourcing engagements to drive new levels of innovation and impact from them. Consider it a way to address the challenge Phil laid out in his October 2nd blog: “let’s make outsourcing great again”… because there is a lot of untapped potential …

Charlotte, how do you bring design thinking into your work?

We ask questions to uncover and discover the true needs of our customers as it relates to their business and their customers. What that means is that we often dig deeper to better understand the “why” behind their needs, their motivation. We ask questions about how the work they do impacts stakeholders and customers, such as: Why do they need this? Why do they care? What’s missing? These questions can be applied to any situation to get focused on how to solve problems with a human-centered, customer first approach, versus a business-centric, solution first approach. And by leading with listening, we work with them to help uncover what’s missing or even what could potentially change their entire business model.

Business process services and IT services is a process driven industry; what can you tell us about how to structure an approach to work that uses design thinking? We share customer stories and we talk through our method; there are many design thinking methods that all share a same common theme. At SAP, we use “look-think-do.” (link) It is about understanding WHO you are doing it for, cultivating ideas, finding the one (or more) that is real and can be implemented, and execute it. That last step is where the value is realized from the design thinking driven work. We use design thinking to understand what clients need, then work to define and apply the right solutions to bring those ideas to reality.

Will you share a story with us about how design thinking is part of a corporate culture?

Look at Discount Tire, which is a tire company mostly in Arizona, California, and New Mexico. They are well known for their friendly approach to something as common as tires because at the core of what they do is ensuring safety. Yes, they need to sell tires to be in business; but the tires need to support a safe drive. The team at Discount Tire continually thinks about how to create that safe situation for drivers, and that leads to services with loyal customers. In the video they made to capture their experience, Discount Tire employees talk about “slowing down and thinking more,” and “making decisions with empathy.” For them, it was not a “one and done” project. Discount Tire liked the design thinking approach and results so much, they created dedicated spaces for their employees to keep using the approach they learned while working with SAP.

A guiding principle of Design Thinking is prototyping. If you are talking about doing delivery services in a different way, how do you prototype?

We do low and medium fidelity prototyping: storyboards and vision videos, for example. We take ideas coming out of a workshop engagement and put it together into a story and then play the story back. For example, for a discrete manufacturer exploring the use of 3D printing, we would develop an end to end story, such as, if you used 3D printing on site, here’s how your supply chain might change… what it might look like… in a video or storyboard. The power behind low and medium fidelity prototyping is the ability to see the different ideas in action and imagine a future with those concepts applied. This allows for iterations without long-term investments, promotes learning, and embodies the concept of “fail forward” to ensure the changes can be easily adapted.

Have you seen other companies besides SAP that are using Design Thinking in their culture? Which ones come to mind as a good example of incorporating Design Thinking into the way they work? Has it helped them change their business?

There are several other companies that use design thinking although most of them are in the business-to-consumer market. Harvard Business Review recently profiled the CEO of Pepsi, Indra Nooyi, who introduced design thinking into the core of the company, driving change that has resulted in revenue and stock price increases for the past few years after stagnating. (link) Other familiar brands like P&G, Marriott, and Fidelity are well known in the design thinking sphere where they also customize the concept in order to ideate and co-create with their customers. These companies are going beyond just dabbling in it, and are working to make design thinking a part of their organization.

What if Design Thinking is not part of the culture or driven by the leadership in your organization? How can someone use it in her or his everyday work?

I rely on a broad ecosystem of people who leverage design thinking every day, including Mark Leung, Director at Rotman DesignWorks, who shared his approach around being a DT ninja at the onset. Even without a “guru” or network, you can practice with design thinking tools and techniques in your everyday work, like using empathy, thinking out loud (write up what you think on a board rather than your little black notebook), and doing small rounds of ideation and prototypes. You’ll find other tools on the Stanford d.school site, as well.

As part of our journey at SAP, we were very fortunate to partner with the creative technology firm Gorbet Design. During our time together, we built a business-focused design approach to working with customers, and learned how to leverage those tools and techniques to uncover and solve both internal and external business challenges. We found that a design thinking approach that includes perspectives from many people, rapid iteration, and a focus on the human in the system will generate far broader and more innovative ideas than a standard business approach.

I have learned that you don’t need to wait for permission to use design thinking, you need to just start doing it… delighted customers and powerful results speak for themselves. You’ll find examples in these customer stories.

Charlotte, thank you for sharing your experience and ideas that hopefully will inspire the designer in more of us!

In summary, design thinking can help you create “connections” with your customers and client base because it is about knowing, understanding, and creating new and creative ideas leading to solutions that enable those connections. Connections and experience create relationships and loyalty, which is good for business… and the financial bottom line.

Even if you are not a designer, don’t have a budget for engaging a third party for a workshop, or have a leader promoting design thinking, you can incorporate the principles of Design Thinking—asking questions, observing your end users, experimenting—into your own approach to problem solving and start a new movement.

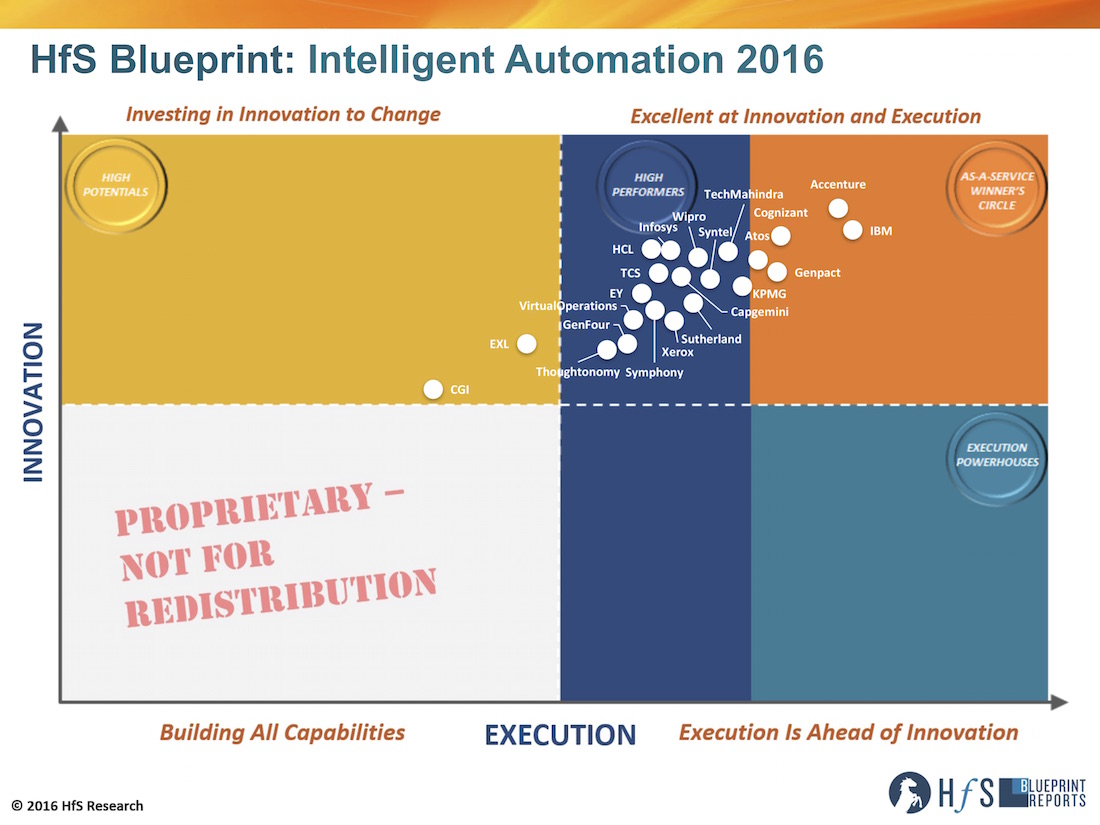

Finally… exactly four years after HfS introduced the concept of Robotic Process Automation (RPA) to the services industry, we can reveal to the world how our service provider and advisor friends are performing with the industry’s inaugural HfS Blueprint report on Intelligent Automation.

Back in 2012, HfS brought the topic of RPA (see link) to the attention of the sourcing industry by challenging its dependency on low cost labor made widely accessible through the ubiquity of global sourcing resources. The report, “Robotic automation emerges as a threat to traditional low‐cost outsourcing,” examined whether affordable, easy‐to‐develop software robots would eventually supplant many offshore FTEs to drive down the cost of outsourcing to an entirely new digital level. We concluded that robotic automation, or Robotistan as we affectionately called it nack then, had immense potential to be a highly disruptive and a transformative technology for buyers and service providers that would forge a whole new services industry landscape that incorporated truly global operating models that not only took advantage of globally available labor, but also accessible technology that could help digitize, streamline and standardize business processes. This wasn’t only about making thing run more affordably, but this was about helping enterprises digitize their business operations more effectively to respond to their customers’, partners’ and employees’ needs… as those needs arose. That was then, and was just RPA.

Fast forward 4 years, and the broader notion of Intelligent Automation (IA) is not only top mind of BPO executives but across the whole industry as all the facets of IA are about decoupling routine service delivery from labor arbitrage. However, despite the high profile, the understanding of how IA is impacting the industry is at best blurred as the marketing communication is both scarce and often confusing. Normally, no topic is small enough to be hyped, to be shamelessly exaggerated. Yet, in the context of automation the usual suspects, the service providers, ISVs and sourcing advisor remain coy and largely on the sidelines. Probably the two key reasons for that are that the impact on revenue models is not well understood and the disruption among workforces, the fear factor, the connotations around the topic. As such as our own Lee Coulter aptly put it, in the context of IA we have something akin to the Tower of Babel. We have many languages but can’t understand each other. Enough reasons for our Intelligent Automation expert in residence, Tom Reuner, to take stock as to where the development of IA has advanced to.

Tom, there appears to be a lot of noise around Intelligent Automation in the industry? Is the hype justified and where does it fit in strategically for buyers?

Noise is probably a good way of putting it, Phil. While many talk about automation or least refer to it, few actually provide insights about the market dynamics or even educate stakeholders about the many implications of IA. In my 20 years of being an analyst and consultant I can’t think of any comparable topic where the industry is so coy of effectively engaging with stakeholders. Thus, it is (the often tiny) automation tool providers and the specialist consultants who are leading the marketing communication and are educating the market.

While the market is still nascent, we are seeing signs for exponential growth kicking in. Both in terms of build out of capabilities by the supply side as well as by the scale of the deployments. The best way to think about it is the hockey stick effect, and we are starting to get to the long shaft of the stick representing hyper growth. As for your question, as to where IA fits in strategically for buyers, the answer is it is in the eye of the beholder. And this is not the usual analyst cop out. It really comes down to how stakeholders are approaching IA and what their requirements are. For HfS, the relevant context is service delivery and not function and features. Consequently, the discussion should focus on specific use cases and not generalist statements.

Regardless of the specific use cases, IA is a critical building block for organizations journey toward the As-a-Service Economy as it is significantly accelerating the speed of service delivery and moving toward notion to straight-through-processing. Critically, the mainstream view is that bots, robots and algorithms are supporting and augmenting IT and business analysts rather than supplanting them. Thus, notions of a virtual workforce are pointing toward blending bots and human workers. However, particularly among the more business process centric supply side, we are expecting widespread disruption as generic activities such as compliance, reconciliation, data entry etc. will be phased out and we will see a shift toward higher value activities such as analytical and cognitive skills. Therefore, we need urgently a fundamental debate about the transformation of knowledge work in order to help organization on this extremely challenging transition.

How are the winning service providers approaching Intelligent Automation today? What are they doing beyond more low level RPA?

Phil, to answer your question, let me level set on the key criteria that we were assessing the service providers on. What we were trying to assess was how service providers are orchestrating diverse sets of automation within the context of service delivery. How are they proactively transforming the processes for clients? Thus, the emphasis is not on task automation or isolated point solutions, but on automation from a business function or process point of view. Similarly, advisory is only relevant as part of implementations. These capabilities might sit within traditional business units, but we are seeing the leading providers build out capabilities across those business units. While IA can be an internal capability for delivery and costs optimization, we are trying to understand with this Blueprint is how IA is helping clients on their journey toward the As-a-Service Economy.

Against this background, the pace of change in building out IA capabilities is nothing short of astounding. All providers have built out centers of excellence that tend cut across the entire Continuum of Intelligent Automation ranging from RPA on the business process centric side to Cognitive Computing, AI all the way to self-learning and self-remediating engines. In this increasingly crowded space, Accenture stands out through investments in a holistic automation strategy. The reference point is the Accenture Intelligent Automation Platform integrates Business Workflow Management, Delivery Management, Intelligent Automation, and Analytics and Insights, with a neutral ERP interface at the core. This is further enhanced by the Accenture AI Engine that provides an architecture abstraction layer for interacting with various AI based services, such as natural language processing (NLP) and machine learning. In contrast to Accenture, IBM is pursuing a highly pragmatic strategy by driving scale through focus on core technologies: IBM is focusing on three core technologies and driving them out at scale: Blue Prism in RPA, IPsoft in Autonomics, and Watson as a virtual agent and broader analytics scenarios. This allow not only for scale but also results in robust delivery. These leaders are joined by Cognizant, Genpact and Atos in the Winners Circle. Cognizant is a reference point for thought leadership. Its automation team within the Emerging Business Accelerator (EBA) is at the vanguard of educating the market place on the implications of automation. Genpact stood out by proactively providing innovation. Clients praise Genpact for consistently proposing innovation. This includes a consistent approach to monitoring even for activities that are outside of scope. And last but not least, Atos stands out by driving IA at the heart of its service delivery backbone. This includes linking business services and applications orchestration with infrastructure cloud provisioning. A crucial element in this strategy is integrating big data and operational analytics into the automation approach.

What are the main lessons coming from the early deployments? What are the issues buyers should look out for?

Three issues are jumping to my mind:

Look beyond task automation: The marketing noise is largely around RPA and implicitly notions of task automation. Therefore, it can be challenging to get a sense of the bigger picture. However, as one provider aptly put it: “Automation success starts with good design, efficient processes, and data curation.” Crucially, what is the future state and how do organizations get on the path toward the As-a-Service Economy?

Automation is a journey: Automation is not a quick fix; it is a journey. It takes preparation to find the right candidates and can be done effectively only by taking support from the people who are involved in the business or IT operations. Projects should start with advisory and process consulting.

Data curation is critical: Applying Cognitive and machine learning solutions to IA requires access to large amounts of relevant data to build reliable models. Data can be pertinent to IT operations, business processes, and publicly accessible data. Thus, there is a need for quality and quantity of the data, and associated compliance considerations are often under-estimated by clients when they consider AI-based automation solutions.

How will all of that impact workforces, Tom, and what are the broader implications for talent? Are the fears justified or is it plain scaremongering?

Phil, this is probably the most contentious issue. We all have seen the studies by McKinsey and the World Economic Forum predicting the loss of hundreds of millions of jobs or Gartner’s assertions that in 2018 3 million employees will be managed by a robo-boss. HfS is taking a more balanced view that is both specific and relevant to our industry that we need an urgent and honest debate about the transformation of knowledge work. And you have been quoted left right and center that digital disruption is killing jobs – not automation.

For me two issues are standing out. First, successful automation projects require a proactive stakeholder management that is taking the concerns of employees serious. Change management is crucial for achieving projects goals. While anecdotal, examples for successful projects were where employees were giving automation terminals names and even window seats as they freed up from mundane and often boring tasks. Second, and very close to my heart, we need to rethink our approach to talent. Data scientists and cognitive skill sets are not growing on trees. Universities have to start adapting their curricula. But even more importantly, organizations have to fundamentally revisit their strategies on talent. Many activities that their employees will do today are not needed anymore in 2 or 3 years’ time.

Will the juggernauts finally start to properly engage with clients and stakeholders around the notion of Intelligent Automation? How do you see the market evolving in the next few years?

I am not holding my breath that the juggernauts will start to properly engage with stakeholders on the topic any time soon. It is a classic case of innovators dilemma. Many will continue to make more money with labor arbitrage. In the same vein the automation giants such as BMC or CA are ringfencing their licenses. But make no mistake, they are evaluating M&A opportunities and will pounce when they feel the time is right.

In terms of market evolution one of the key findings of this research is the emergence of Virtual Agents. These agents (ranging from the big beasts Watson and Amelia to OpenSoure avatars) are underpinned by broad process and automation capabilities. The case study that highlights this best but also underpins that looming disruption is KPMG. KPMG is anticipating and investing significantly in the disruption of their core business (tax, accounting, advisory etc.) through robo-accountants and advisors. And their core business is not high on the technology affinity list. And this disruption is not 5 or 10 years out but over the next 2 or 3 years.

So, what is direction of travel for the further development of IA? HfS believes the more service delivery is industrialized and automated, the more differentiation as well as value creation will be at the intersection of standardized service delivery and the plethora of unstructured data that will be increasingly integrated through neural networks and deep learning. Thus, vertically relevant insights and data is likely to be the endgame for both automation and service delivery. And it is here, where the providers in the Winners Circle are focusing their investments in and are ahead of the game.

HfS Premium Subscribers: click here to download the new HfS Blueprint Report, “Intelligent Automation 2016”

Although it’s not immediately obvious with all the talk of pilot projects and proofs of concept as businesses experiment with ‘the art of the possible’, there is a great deal of large scale and serious build out of modern digital stacks fed by modern sensor data transmission, also known as the Internet of Things (IoT). Like most competitive business differentiators, strategically important work is being planned and executed in great secrecy, which can skew perceptions of what the landscape looks like.

An illustrative example of the importance and power of the various data streams created and consumed around the IoT is precision farming.

Smart farming equipment is relatively mature, with multiple data flows about all aspects of, as a specific example, planting seeds. Heavy equipment manufacturers are under pressure to not become ‘dumb iron’ and therefore a price pressured commodity.

To avoid losing out to seed manufacturers over control of data streams and aggregated intelligence ownership, equipment manufacturers must compete by not just supplying the relevant industrial internet hardware.They must aim to control the farmer’s user interface and experience by providing the best data flows through continuous digital innovation.

Providing farmers with real time planting intelligence and best practice is the center of equipment manufacturers market leadership and survival, and data is the currency.

It’s a commercial battle: whoever is able to provide the most useful, intuitive and intelligent assistance to the farmer wins their trust, business…and their data, which can be aggregated and resold.

From a service provider perspective, the Internet of Things currently has two main dimensions, both of which are attributes of larger battles for digital dominance.

The first dimension is the Machine to Machine (M2M) industrial internet, which evolved from heavy equipment telemetrics (the measurement and transmission of data by wire, radio, or other means from remote sources to receiving stations for recording and analysis) and has matured and grown on a linear path alongside ‘traditional’ enterprise IT systems for the last fifteen years. Examples of this are ‘time to failure’ monitoring of all types of rotating heavy equipment, and data flows into and from ERP and other enterprise software.

The other, newer dimension is the explosion of product innovation enabled by new sensor developments and ‘big data’, enabling data flows from ‘born digital’ devices from and to physical ’things’ of all sizes to modern digital backbones.

Modern ‘things’ of all types are increasingly manufactured with sensors embedded in them, from tires to consumer products, and have associated API’s to send and receive data. These sets of data flows are rapidly transforming society as a subset of digital business.

There is an increasingly complex services market growing up around these two dimensions of IoT The services sector has several ‘born IoT’ specialists, multiple global IT firms expanding into IoT services, integration suppliers who have deep competencies in the industrial internet, and many more services firms with substantial multipurpose IoT departments in anticipation of increases in business demand.

We evaluated a representative 18 service providers in our IoT Blueprint research. In the process, we placed a bias on innovation, particularly around the“newer dimension” of IoT as described above. We also looked at many other contenders in the space but found inadequate activity to justify inclusion for now.

While the industrial internet is an industry in itself around all types of increasingly sophisticated data flows from manufacturing, heavy equipment, aircraft and supply chains, it is largely rooted in past technologies. Innovation for the industrial sector is around smart cars, buildings and infrastructure, which are all large scale investment projects, and are areas where there is a thriving, mature business for many of the enterprise suppliers of services.

Where things get really interesting around IoT (and where there is also substantial hype, red herrings and misunderstanding) is innovation across ‘born digital’ product and services lifecycles from inception to post sales support.

While there is hugely entrepreneurial innovation and experimentation with all the new ‘things’ made possible by sensors, connectivity and data, interoperability and integration are critical to avoid standalone solutions, which won’t work as contributing components of a larger digital framework. Revisiting the precision farming example above, the industrial internet underpinnings of a piece of agricultural equipment must be augmented with ever more innovative, newer dimensions of access and analysis of data to remain competitive.

The farmer may also choose to leverage additional ‘standalone’ IoT products and supporting mobile apps in their arsenal of digital intelligent aids, but these will be of limited and narrow use unless they can flow their data to a single digital backbone or core.This provides a more complete and sophisticated view of real time activities, with real time contextual intelligent assistance to the operator of the equipment.

Viewing the IoT services market from the client perspective, anxieties are high over security concerns and standards. The technology vendor partner ecosphere is fluid and there are concerns that placing big bets on complex integrated systems could cause headaches as technology relationships and standards evolve, resulting in disruption and forced redesign of systems created to be load bearing and mission critical. These anxieties are tempered by the reality that the world is changing fast and the fight for continued relevance in marketplaces requires being on top of customer facing digital strategies. High end-to-end security competency to protect exposed IoT data flows are table stakes to give clients the courage to embark on work with vendors.

IoT is a buyers market…for now…

Today IoT services is a buyers market as prospects and existing clients in other areas scope out the best size, specializations, partnerships and geographic location fit for their needs. There is a marked division between passive services providers with strong skillsets who are waiting to be told what to deliver and when, and the more innovate entities who will partner with their clients to innovate, perform design thinking together, and often to share risks and rewards. It is the latter who are likely to evolve to be top of a sellers market as reputations and track records are built.

The fate of being perceived as a lowest cost commodity delivery supplier is a threat to some ‘delivery only’ IoT partners, who share a similar danger with thefarming equipment manufacturers who fail to evolve and innovate in order to remain relevant to their market.

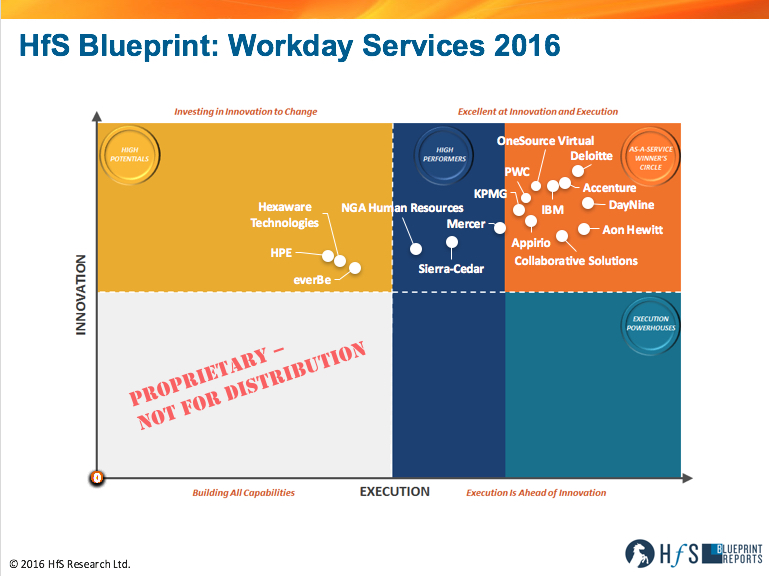

Consolidation in the SaaS services market continues apace with the boldest move yet by an India-headquartered service provider into the SaaS services market to date. Wipro has announced its intention to acquire Appirio, one of the strongest and most respected independent cloud services brands in the world for $500m.

This is a significant deal in a services industry struggling to find fresh paths for future growth, with revenues slowing and the traditional model of outsourcing around SAP and Oracle environments commoditizing. This has especially been the case with the Indian majors, whose leaderships are starting to panic with their hyper-growth days now a thing of the past. In our view, Wipro is stepping up to the plate right where the future growth lies, by adding significant capabilities around Salesforce, Workday and ServiceNow platforms, in addition to bolstering its digital and mobility capabilities in the retail and media spaces. Our concerns are whether Wipro can truly integrate the two firms effectively, with a poor track record of Indian-US acquisitions (Lodestone/Infosys and Genpact/Headstrong are example of mergers which struggled from both a business and cultural fit.)

Adding SaaS consultants to compensate for declining legacy ERP services revenues is the new enterprise services game

The traditional Western service providers have been hard at it picking up the niche “As-a-Service” providers, most notably Accenture’s acquisition of DayNine last month, IBM picking up Meteorix and KPMG’s acquisition of Towers Watson’s Workday practice in the Workday services ecosphere, and Accenture/Cloud Sherpas, IBM/Bluewolf and Capgemini/Oinio in the Salesforce market. While the Accentures, IBMs and Capgeminis et al have been in a hurry to replace declining ERP services revenues with the implementation and consulting dollars around the hot enterprise SaaS platforms, the Indian heritage majors have been notably absent in the SaaS services space. Until now.

The acquisition strengthens Wipro’s position in the Salesforce services market and gains it access to the fast-growing Workday services market. Appirio gains important global scale, particularly to boost delivery capability in Europe, and strengthened offshore capabilities (Appirio already has a delivery location in Jaipur).

Consulting + IT integration + BPO + Global Delivery Scale = Huge potential for Wippirio

Based on the data collected for the HfS Blueprint Report: Salesforce Services 2015, we estimate the combined Salesforce certified consultant pool to be 957, which places it just behind market leaders, Accenture, Cognizant and Deloitte. In Workday, Appirio has approximately 210 certified consultants and a wealth of experience with a total of approximately 419 projects and ongoing engagements, based on our HfS Blueprint Report: Workday Services 2016. With Wipro’s massive scale in IT services and its $720m dollar BPO business, the combined entity has huge potential if its leadership can get the integration right. Moreover, the merged entity is one of a very small band of BPO providers which has a massive call center scale and client depth and a worldclass Salesforce implementation capability. There is also future opportunity to bring together the firm’s strong F&A BPO presence with the nascent uptake of the Workday Financial Management suite, in addition to supporting HRO engagements based on the Workday HRMS and HCM platform.

Both providers are known for strong technical skills and have invested heavily in tools and technologies. Wipro has developed a wide range of Salesforce1 platform based solutions, including industry sector focused offerings, such as its Physician Relationship Management solution. In addition, Appirio’s web development services around Salesforce and Heroku have led to some very impressive work for clients such as Eli Lilly is a major plus for Wipro. Appirio, for its part, has the industry renowned Appirio Topcoder Platform, its proprietary crowdsourcing development platform, which now has nearly a million members. Moreover, Wipro’s focus on management services complements Appirio’s clear strengths in implementation services. Both providers offer consulting services, but this remains an area to strengthen and market to prospective clients.

Despite Wipro’s investment in Wipro Digital, it is still known predominantly as a technology services partner which enables the digital experience, as opposed to designing it from the customer end. Appirio’s digital and mobility focus, especially with retail and media clients, should benefit the merged entity considerably. Wipro should also benefit significantly from Appirio’s Worker Experience approach, which helps organizations transform their employee experience, to gain additional credibility in the HCM and CRM markets. Aligned to this are also Appirio’s expertise in servicing popular SaaS solutions Cornerstone-on-Demand (talent management) and Medallia (customer experience management), not to mention acumen in servicing corporate Google environments

Depending on the success of the merger, clients can potentially look forward to a full service suite offering around Workday, Salesforce and ServiceNow, with a focus on business outcomes. Wipro and Appirio clients we have spoken to in these markets are already pretty satisfied, highlighting Wipro’s ability to provide proactive advice, and Appirio’s focus on customer satisfaction. A smooth merger in the services industry is, however, seldom possible and a lot hinges on Wipro’s ability to hold on to the best talent at Appirio (there will be several hungry Workday partners ready to pounce) and integrate offerings. More importantly, the challenge of integrating cultures and business could be massive, especially since Wipro has to change mindsets, working attitudes and break down its internal business silos, to take full advantage of the potential here. If it pulls it off, Wipro will be joining the front-runners of the SaaS services market, and develop a strong differentiation from the other India-headquartered service providers.

Bottom Line: Wipro muscles its way to the front the SaaS services market, with few left worth buying. Does this leave the other Indian majors out in the cold?

With this acquisition, Wipro is officially the leading Indian major in the SaaS services space, boasting significant Salesforce resources, a decent sized ServiceNow practice and, perhaps most excitingly, a Winners Circle caliber Workday practice:

When you consider DayNine is now part of Accenture, you could argue that only OneSource Virtual and Collaborative Solutions are the last two “pureplay” As-a-Service providers left in the Workday ecosphere worth acquiring to come close to matching Wippirio’s combined strengths. So does this leave the likes of Infosys, TCS, HCL, Cognizant, Tech Mahindra et al out in the cold when it comes to being serious enterprise SaaS providers? Surely one has to make a move soon to add expertise and depth to compete effectively.

In order to stay competitive, speed and simplicity are of utmost importance to marketers today. Lionbridge is providing “smart” translation services by really thinking about how to make the marketing person’s job easier – through a simple, fast, self-service, and automated capability. We recently spoke with Life Fitness, a fitness equipment manufacturer, about their use of translation services for marketing materials. Life Fitness uses Lionbridge’s onDemand online service, a portal for uploading files to be translated in various formats, providing instant quotes for the timing and cost of completing the translation project.

As an international company, Life Fitness uses this service for translation and localization of all kinds of content, both customer facing and internal in 11 languages (Lionbridge serves 120 languages total). The content being translated includes MS Office documents, website content, email communications, YouTube videos and software on the cardiovascular products. The translation is done by employees, but Lionbridge onDemand automates the workflow process including: file analysis, quoting, delivery estimates, routing to translators, application of glossary and terminology, quality reviews, delivery notification and file delivery.

Life Fitness has had previous translation providers, but felt they weren’t working “smart” enough. The automation and speed that the onDemand portal provides is the big difference. “Quality translation is easy to find,” said a Life Fitness marketing manager. “A number of providers do this well. What they struggled with was the efficiency with the turnaround time and the business process and systems around the translation. That’s where Lionbridge was helpful because the portal is simple and straightforward.”

3 Ways to Simplify the Marketer’s Translation Ordering Experience

Life Fitness described the Lionbridge onDemand service as a straightforward process where its 30 users have their own accounts to log in and choose the product that they want to order. Once they upload the material they verify the source language (which is automatically detected), select the target language, and get an instantaneous quote, which is sent for approval. Before using the automated workflow, Life Fitness had to do a review for every project, which took two weeks to a month of extra time. They now have a 3-5 day turnaround period as a result of automating the file analysis and quoting.

The service has also shaved off time with automation for PO management and invoice payment and tracking invoicing with automated invoice generation—Life Fitness went from a 10 step process involving email coordination between departments and manual tracking in spreadsheets that could take up to a month, which has now been cut down to one day.

Life Fitness also appreciates the ability to receive an instant and reliable timetable for the delivery of a project. (onDemand published figures show a 99.6% on time delivery performance.) Lionbridge beat out its competitors for simplicity and ease of use, although perhaps “too simple” as when the Life Fitness’ technical publications team has larger, more complex file types, they have had some issues with the quoting feature. Lionbridge is working to address by developing an advanced quoting function that was launched in August.

Talent and Tech Combine for Plug and Play Service

The translation work is done 100% by professional, human translators all based in the target locales. What we should watch in the future for potential disruption is the progression of automated/machine translation; Lionbridge itself is making some strides in this area with its GeoFluent offering, targeted primarily at the contact center. In the meantime, this service is able to guarantee the quality of the translation by having efficient automated processes with a human touch in the background.

The Workday services market is growing rapidly, but remains relatively immature. With many of the service providers still finalizing their specific areas of market focus and are trying to find a clear identity and position in the service ecosystem. At the same time enterprise buyers are learning the intricacies of SaaS deployment and service provider relationship lessons in real time.

One of the most uncontroversial findings from our recent research (see: HFS Blueprint Report: Workday Services 2016) into Workday services is that enterprises are increasingly considering Workday solutions to manage both their HR and Finance functions. While Workday Human Capital Management (HCM) remains the leading solution, interest in Workday Finance Management (FM) has significantly grown in the past year. In fact, some enterprises are deploying the FM product first. We see a mix of deployment behavior, including:

Cautious Experimenters: Enterprises deploying a few modules at a time, across a few or all sites

The Big Bangers: Enterprises deploying almost the full suite of the HCM modules to all major sites at once

The All-In: Enterprises adopting the full platform deployment of HCM, FM and sometimes also Payroll applications

The Workday service providers profiled in our recently published HFS Blueprint Report: Workday Services 2016 expect this part of their services business to grow at an average of 46% in the next year. This is strongly supported by Workday itself, which works closely with each of its service partners to identify market positioning and opportunities. HfS estimates that the number of people in service providers’ Workday services practice teams increased by 64% from 2015 to 2016.* Service provider participants of this Blueprint have a total of nearly 5,000 Workday certified consultants.

Service providers and buyer organizations alike are investing in Workday skills and solutions. HfS has published two reports to provide recommendations to each of these parties:

In these reports we highlight the areas buyers and service providers need to focus to ensure successful Workday deployments. For example, service providers should demonstrate a commitment to investing in Workday services, and adopt an industry sector approach to service offerings and solution development. Buyers need to ensure that they understand what is involved in a Workday deployment, both technically and organizationally, and pushing all their service providers to share best practice lessons.

Both of these reports are available on the HfS Research web site at http://www.hfsresearch.com/research and, of course, are free to download.

*Footnote: based on service providers who were included in the HfS Workday Services Blueprints of 2015 and 2016. This also takes out the effect of major acquisitions that these providers may have been involved in.

The funny thing about innovative projects is that everyone likes to talk about buying them as if innovation is a product you just pick up off the shelf at the store. But real innovation – exploring ideas, opportunities, risk, and implications of change – means you likely don’t even know what you’re buying. You’re not buying a packaged piece of software or a defined solution. You’re really buying someone who can be a co-creator with you, helping you wade through the mass of tangled and often conflicting options available to discover and build something that adds a unique value to your business.

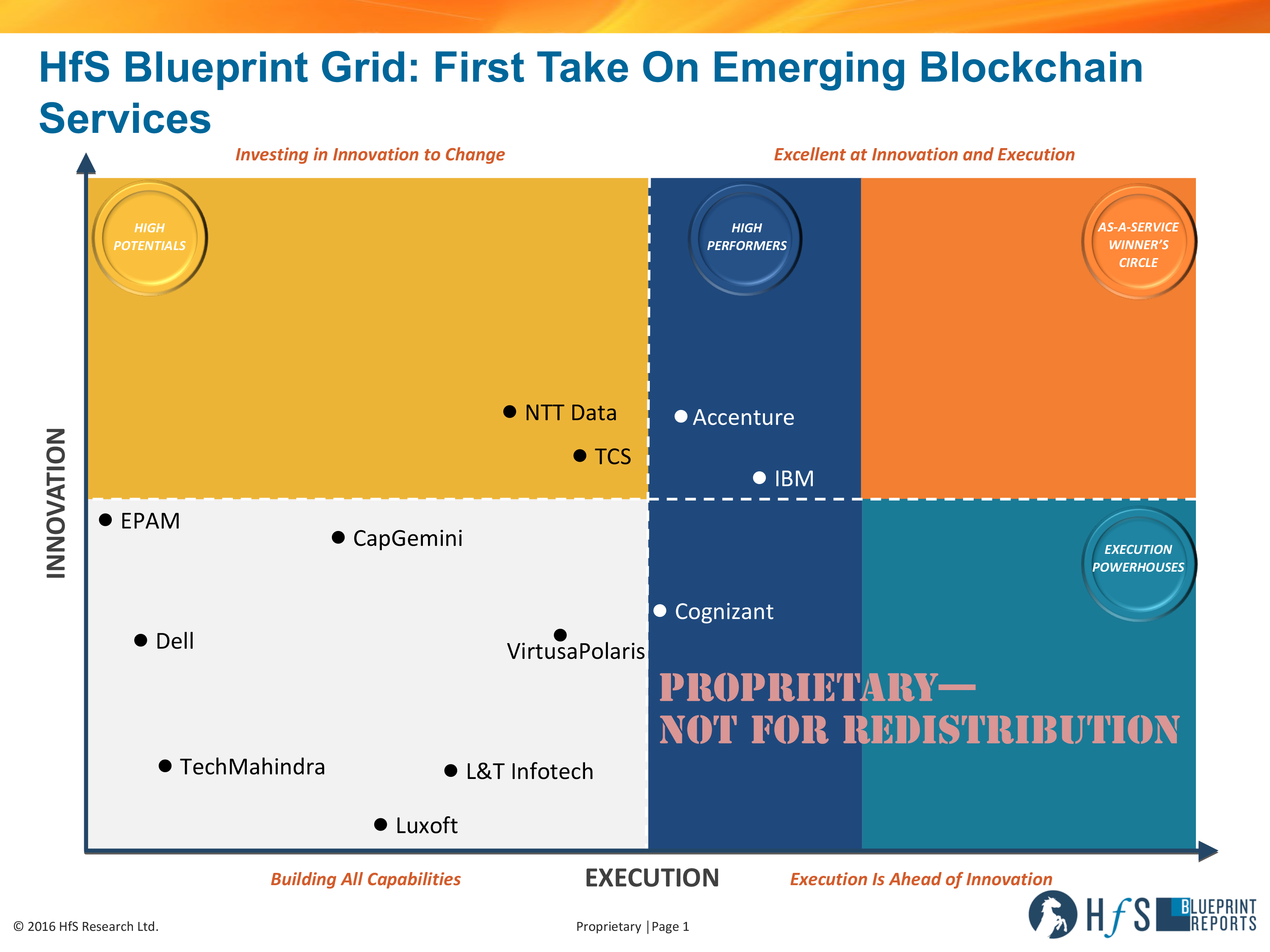

When you’re experimenting with business opportunities it’s complicated enough, but when you add a technology or solution area that’s just emerging, it gets doubly complicated because often the service providers don’t have tons of experience themselves in the new area. Blockchain is a perfect example – most service providers are themselves exploring what blockchain can do for their clients and vertical industries. My latest research into emerging blockchain services shows this, with most providers still in the early days of the blockchain efforts (see Exhibit 1)

Clients and their service providers are learning blockchain together. This is bad if you want someone to hold your hand and tell you everything is going to be ok, that they have the answer for you (by the way, no judgment from me on this – if there’s a well understood solution and you can hand it over to someone to get it done, go for it.) BUT it’s fantastic if you really want to take control of your own business destiny, be strategic and really work collaboratively with a partner to find the right opportunities and create solutions together. It’s a rare chance to be an equal intellectual partner with your services firm and in fact potentially for the provider to learn from you as your team researches opportunities and bring in the provider to help test some of those opportunities.

Five considerations for selecting a services partner for blockchain experiments

If you can’t just send out a standard RFI with what you’re looking for, how can you pick a service provider to help you explore blockchain? Try some of the following criteria:

Look for design thinking capability. Because design thinking is about looking at the human aspects of a situation, finding the problem to be solved, and then working backwards from that solution, it’s a great way to discover opportunities with blockchain. It also allows you to be respected an expert in your own right, unlike more traditional discovery projects where the consultants feel like they already know 80% of the answers.

Find great storytellers. It’s really important to understand the technical aspects of blockchain, of course. You’ll have an easier time finding technical skills than you will finding people who can really dream with you and tell you stories of how blockchain can change the world. This isn’t just about looking for strategists, it’s about looking for providers who can clearly communicate a vision for what’s possible, so you in turn have an easier time digesting the different scenarios and selecting the right ones to move forward on to the proof-of-concept stage.

Conflict resolution, problem solving, and negotiation. Innovation engagements are by definition environments of strong disagreements, opposing views, and conflicting information. Most providers are great at marching when you tell them to march. Far fewer are capable of disagreeing without causing an escalation in the account. Look for consultants with negotiation backgrounds and a methodology that explicitly calls out conflict resolution processes as part of their work.

Put more emphasis on service providers’ partnerships than usual. The market for an emerging technology like blockchain is filled with consortia, startups, and small vendors. Service providers that are just exploring should be comfortable saying they’re looking at a lot of players and haven’t made formal partnerships yet (we saw this often in our latest research.) But they should be able to demonstrate a broad view of those players and the segments where they’re trying to map the vendors. Spend more time understanding what criteria the providers are using to evaluate the technology vendors than you would normally, since this deep dive is going to be more important for you than in other more mature areas.

Ability to work in agile development environments. Yes, I know, you’re likely not even close to building anything right now. But keep in mind that you’re looking to find someone to co-create with you and that requires the ability to be iterative and flexible while still not losing sight of the original goals. Providers who have more rigid engagement methodologies will put more pressure on you to define your requirements probably even before you really know what those requirements are. So look for a player that has strong agile skills since those skills will transfer well to your blockchain exploration.

Of course this doesn’t mean you forget your best practices for hiring service providers: client references, checks into their technical depth and execution, client management and governance, etc. But those best practices need to be supplemented with a few more non-traditional evaluation criteria like the ones above. Ultimately, these kinds of engagements are a lot more push/pull than engagements for more mature areas.

What did I miss? What other less-asked qualifiers do you use when evaluating new areas like blockchain services? I’d love to know your thoughts as I keep researching blockchain.

In the meantime, here’s a link to the full HfS Research Emerging Blockchain Services Blueprint Guide, with definitions and descriptions of the current activity (particularly in BFSI) and how service providers are approaching this inevitably integral part of the future fabric of any industry.

Steve Goldberg (click for bio) is Research Vice President, HR Technology and Workforce Strategies at HfS Research

Back when enterprise time began and God was handing out the technology dollars, why was the Chief HR Officer always seemingly at the back of the queue? Why did so many of our beloved enterprises become plagued with the clunkiest, funkiest legacy systems we never could have dreamed up in our worst nightmares? Especially when you consider the data critically and sensitivity of one’s employees – their profiles, their health records, their compensation, their performance etc…

So it’s no surprise that the advent of the SaaS based HR suite has been embraced like manna from Infosys heaven. Suddenly, our HR-technology plagued enterprises can hatch a plan to rip out the cancerous legacy and slam in something that’s standardized, has hire-to-retire process that are sort of adequate, and doesn’t require that cobol transformation project each time you try to push through an exception payment. So what better timing than for HfS to bring aboard Steve Goldberg – a true veteran of the HR tech world – to lead our thinking in the space and is freshly returned to his desk from the HR Technology show (read his blogs here).

Welcome Steve! Can you share a little about your background and why you have chosen research and strategy as your career path?

Sure Phil. I’ve basically operated on all sides of HR Technology, so a real diversity of experiences. This includes HRIS and Talent Management practitioners in the U.S. and Europe, HCM product strategy leader at both PeopleSoft and emerging solutions companies, co-founder of a recruiting software company, HR-M&A and HR Shared Services exec, a previous stint as an industry analyst, and advisory engagements the last 10 years with solution vendors and end-customers around the globe. This pattern of diverse perspectives and experiences likely started in grad school, as I first pursued a Masters in Social Work and then made a left (or perhaps right) turn to earn an MBA in HR. On the research and strategy part of your question, strategy work is what I hope keeps my brain reasonably serviceable, and I guess research ensures the strategy work is based on what is really happening.

And why did you choose to join HfS… and why now?

I chose HfS for 2 main reasons: In my career I’ve always tried to be around folks smarter than me (the rising tide lifts all boats principle), and who are also thinking differently than most. A former colleague once told me that it’s not what you think, but how you think. The first time I read your stuff, Phil, that comment from decades ago came back — and frankly that’s when I reached out to you.

What are the areas and topics that you will focus on in your analyst role?

My role, and the themes I’ll be exploring, will focus on both the HR Tech solutions space and the HR services (or in HfS-speak) “as-a-service” market. I tend to study business value drivers and impediments, and how both vendors and customers maximize the former while minimizing the latter. As we know, the pace of innovation and product/services advances is often ahead of corresponding adoption curves, so my work will also try to help both vendors and customers navigate this challenge. Clarifying various vendor claims that can confuse buyers is also of interest to me; e.g., what is truly an industry or global solution?

And what hot trends and developments are capturing your attention today?

These would include what capabilities and innovations are driving the most business value, looking at the “big 4” themes in HR Tech — Social, Mobile, Analytics and Cloud — and discussing the likely trajectory of each with people on all sides of the value chain, and also collaborating with HfS colleagues on covering unique angles around more traditional services areas like Payroll, Benefits, HRO/RPO, etc.

So what do you do with your spare time (if you have any…)?

Well, I try to play piano almost daily as I never know when an opportunity will surface again to play in a local venue, I take walks on the beach here in FL when the heat isn’t too oppressive (so about 6 weeks a year), play computer chess, and get vicarious thrills from the lives my 2 adult kids are leading.

Steve – I look forward to challenging you to a chess game soon when you can hone those strategic skills against me =)

One of the age-old knocks on the HR profession is that it attracted those who prided themselves on “being good with people.” I was never really sure what this meant when I selected HR / HR Systems as a career path way back when, but it seemed better than being good with hazardous waste. This notion was eventually borne out by the fact that my shortest corporate HR stint was with a Waste Management industry leader.

So how does this relate to the recent HR Tech Conference? Well, beyond what was discussed in my last post about smaller players doing their share to drive product innovation, another realization hit me: Dozens of newer HR technologies are not just “good with people,” but “really smart about people.” This means knowing personal if not unique drivers, how to engage and motivate, and leveraging that context for the benefit of both the organization and its individuals. Employing different talent management and employee engagement approaches for different talent pools (e.g., early career vs. later career or more experienced employees, high potentials, high-value candidates, change-resistors, etc.) makes very good sense.

The personalization theme was indeed ubiquitous at this year’s HR Tech conference, and since forms of personalization within HCM solutions are potentially limitless, I suspect we’ll be seeing more product innovations relating to this theme with each passing conference. The reasons are indelibly clear. Personalization in a user experience drives user adoption and system stickiness, which drives value realization and ROI. It’s also a key by-product of cognitive computing; e.g., the system determines what data, metrics, other content, activities or actions is most relevant for the individual, making them more efficient and effective. And both of these benefits lead to other critical business benefits like engagement, retention and productivity.

Personalization is “killing it” in the recruiting space

It’s no revelation that thousands of recruiting professionals are tripping over each other vying for the attention and interest of the same top talent, many of whom are not looking for a job change or even interested in discussing one. Overcoming these challenges requires not just shiny objects, but shiny objects with initials engraved on them so to speak.

Why all the fuss about engaging passive candidates? Well, the quality of job candidates is generally better within this group for a few reasons: They have not been displaced by their previous employer, they are likely well regarded by their current employer and treated accordingly, and the best opportunities come to them so they are less frequently on the market. Engaging anyone that generally doesn’t want to be engaged isn’t easy, let alone engaging people already bombarded by social media and other technology-driven interactions.

Below are four impressive examples of personalization I observed from recruiting solution vendors at the conference; and I’d also suggest checking out HfS’ recent research on the talent acquisition services BPO market. It provides solid examples of how vendors differentiate with respect to their ability to engage top talent. You can find it here: http://www.hfsresearch.com/pointsofview/hfs-blueprint-guide-to-talent-acquisition-services

ENGAGE’s customers source from one of the largest pools of passive candidates available anywhere; and based on continuously refreshed industry and company data points, insights and inferences, recruiters get alerted real-time when a target candidate is likely to be receptive to a job conversation based on relevant triggers. Timing and receptivity are everything when competing for the best candidates.

The Muse, a relatively new but well-funded player whose first wave of customers would make any established vendor envious, is a career development and employment tool that allows prospective employees to immerse themselves in the experience of working in a particular organization or even role in the way that satisfies their curiosity and interest. This is achieved while getting coached with employment / job search tips along the way that are also highly personalized.

GetTalent helps organizations craft the right (personalized) message and recruitment campaign to attract and engage customer-defined pools of candidates, easily assign target (largely passive) candidates to pools, and track the efficacy of the various communications and campaigns.

1-Page also allows companies to find, qualify and engage passive job seekers; and breaking down technology and other common barriers to communicating with candidates — in the ways they prefer to be communicated with — is one of this vendor’s product strengths.

Not at all limited to Recruiting solutions

Certainly the personalization theme abounds outside the recruiting domain too. A company called Enboarder demonstrated how on-boarding is really meant to happen from a new hire engagement and emotional connection perspective. This is achieved using automated, highly personalized texts from managers and other colleagues based on personal info the new hire shares about themselves in a fun Q+A texted to their mobile.

Bottom Line

Almost all of the major themes swirling around the HR tech space these days seem to have some connection to the personalization theme, from user experience and solution design, to driving system adoption and usage, to – arguably most importantly — more effective ways to identify, engage, manage and truly leverage talent.

The market for talent has seen massive fluctuations over the last eight years. The 2008-9 global recession caused massive employment contractions across all major regions; however, the tide has now really started to turn. In recent years we have been witness to one of the longest sustained periods of economic growth in the last 100 years, and with this, the need for fresh talent is on the rise.

Coupled with the rise of the intelligent digital business, these two market dynamics have changed the way organizations have to approach recruiting new expertise and mindsets. With employees now augmented by this technological innovation, the potential for increased efficiency gains and quality of service delivery is greater than ever.

Here’s the talent challenge now: Employees now, more than ever, need to bring the ability to truly impact an organization’s bottom line, and recruiters need to find and attract them into their companies.

Candidates, particularly passive candidates, are in the driver’s seat and are becoming increasingly particular about which companies they will work for, doing their due diligence to find their right match, using the abundance of information at their fingertips. For today’s candidates, work-life balance and a fulfilling work environment are now at the forefront of candidate’s decision-making process. In addition, many candidates are now exploring contractual work; and this, coupled with increasing project specific assignments in the workplace, is leading to an increasingly active contingent labor market.

So what does this talent acquisition challenge mean for RPO?

Traditional Recruitment Process Outsourcers (RPO) that aim to purely fill permanent positions are no longer often an ideal, forward-looking fit for many companies.

Many organizations are now either partnering with multiple service providers to fulfill RPO (mostly for full-time permanent) and MSP (primarily for contingent/contractor) services separately or looking at service providers that can provide both options. Therefore, HfS is now seeing a convergence of the MSP and RPO market, into a broader Talent Acquisition Services market.

About This Blueprint Guide

In the Talent Acquisition Services Blueprint Guide, we take an innovative look at the Talent Acquisition Services market, reviewing the market activity and a comparative analysis of the innovation and execution capabilities of 10 multi-national, multi-functional service providers.

These service providers have Talent Acquisition Services support capability in their portfolio—at least three of the following services: Candidate Selection and Assessment, Workforce Planning, Employer Branding, Onboarding Services and Candidate Care. Recruitment agency work is not in the scope of this Blueprint Guide but it does include outsourced Talent Acquisition Services on a contract basis that extends one year and beyond in duration.

What does the changing market dynamic mean for recruitment stakeholders?

With service buyers identifying cost and shortage of talent as the predominant drivers in the Talent Acquisition Services market, you could assume that buyers should look for the lowest cost, high-volume Talent Acquisition Services provider, which therefore provide the lowest price but potentially the greatest number of candidates due to scale of operations and reach. Also, many buyers label themselves either cost or value play buyers, based on number of hires and scarcity of skillsets sought, and then source Talent Acquisition Services providers accordingly based on either cost or quality.

However, these sourcing tactics provide a false economy because they could ultimately negatively impact further business outcomes. For example, a sub-standard recruiting and onboarding function has been proven to negatively impact employee performance and increase the likelihood of churn. There is additional impact via an increase in the overall cost of hiring practices, reduced workforce productivity and negative impact on company culture.

With the rise of cognitive recruiting and sourcing platforms been able to identify talent in a cost effective manner recruitment sourcing no longer has to be delivered from offshore centers. Also, automated systems are removing much of the administrative work from the process. This means that the cost of higher value interactions with the candidate such as screening, interviewing and onboarding can be delivered from onshore or on-site locations for a lower total cost. Placing greater emphasis on quality interactions at this point has proven to increase employee productivity and tenure. In addition, these cognitive systems can also identify a better quality of candidate fit that leads to an improved cultural and performance fit of candidates by identifying and matching unique character trends and skillsets based on existing employee performance data.

As such, buyers should look to service providers that can support a proven record of higher quality recruiting services combined with the required level of scale, even if this means a marginal cost penalty at the front end. Therefore, it is vital to include the c-suite in sourcing initiatives and demonstrate long-term ROI of these initiatives. Engaging with a service provider that understands your ultimate business outcomes, strategy and culture is a crucial element in the equation.

Ultimately, organizations are only as profitable as the persons they employ and recruiting practices should mirror this goal.

To access and download the Talent Acquisition Services Blueprint Guide, which provides an overview of market challenges and activity and a high level assessment of service providers, click here.

We ask questions to uncover and discover the true needs of our customers as it relates to their business and their customers. What that means is that we often dig deeper to better understand the “why” behind their needs, their motivation. We ask questions about how the work they do impacts stakeholders and customers, such as: Why do they need this? Why do they care? What’s missing? These questions can be applied to any situation to get focused on how to solve problems with a human-centered, customer first approach, versus a business-centric, solution first approach. And by leading with listening, we work with them to help uncover what’s missing or even what could potentially change their entire business model.

We ask questions to uncover and discover the true needs of our customers as it relates to their business and their customers. What that means is that we often dig deeper to better understand the “why” behind their needs, their motivation. We ask questions about how the work they do impacts stakeholders and customers, such as: Why do they need this? Why do they care? What’s missing? These questions can be applied to any situation to get focused on how to solve problems with a human-centered, customer first approach, versus a business-centric, solution first approach. And by leading with listening, we work with them to help uncover what’s missing or even what could potentially change their entire business model.