IBM’s Watson has come a long way since winning a Jeopardy contest in 2011. While popular games remain a benchmark for advances in Artificial Intelligence as seen in Google’s DeepMind winning at Go, Watson’s capabilities have evolved strongly. So much so that IBM is betting much of its fundamental transformation on the deep investments in the development of Watson. Thus, Watson has become a key strategic pillar for IBM next to cloud and Bluemix. Having had the opportunity to attend the World of Watson in Las Vegas, one couldn’t help to notice the scale of the evolving ecosystem as more of 17,000 people attended the gathering. Suffice it to say but the scale also references the complexity of the evolving ecosystem.

Charting the complexity of the evolving Watson ecosystem

The issue that struck us the most in Las Vegas was the comprehensiveness (put positively) or complexity (put slightly more negatively) of the various Watson offerings. The core Watson Cognitive Platform is composed of four components: cloud, content, compute, and conversation. From a service delivery perspective, the two key components are conversation and content. Within the conversational services, Watson Conversation enables developers to create dynamic interactions and custom applications using the full spectrum of Watson services.

In a nutshell, the two big themes in client examples we saw coming from the event are:

IBM enabling the creation of more and more ubiquitous chatbots in more front office focused activities to create “customer delight.” Pearson and Staples shared their use of Watson to drive new ways for customers to engage with their brands, with Pearson’s ‘interactive textbook/learning’ concept and Staples’ ‘That was easy’ button powered by a provisioning assistant. General Motors is putting Watson to work in its Onstar vehicle navigation system, which it is turning into a mobile-commerce platform in partnership with IBM.

Watson Virtual Agent enabling business users to quickly configure and deploy a virtual agent, without needing specific technical skills. The key value proposition focuses on providing these agents with pre-trained knowledge with the crucial differentiation of being able to take action. IBM is also rolling out new categories for Watson, which will focus on the notion of conversational applications – the next generation of systems that have the ability to interact naturally with business users to make operational decisions, in the areas of marketing, commerce, supply chain management, work, education, talent, financial services along with the existing Watson health group.

Increasingly the context and content for those agents is highly vertically specific, underpinned by the Watson Knowledge Studio. Critically this Studio can teach Watson the nuances of natural language in the cloud without writing a single line of code. The broader foundational services of Watson include a plethora of capabilities including visual recognition, emotional analysis and personality insights for consumption preference features.

At the same time IBM is accelerating the differentiation both from lower level chatbots but also other Virtual Agents by integrating industrial scale analytics capabilities through the Watson Data Platform. By announcing Watson Machine Learning that is available through APIs, IBM is further enhancing the ability to create vertically relevant insights. With the company’s new quest to “own all the data”, including acquiring The Weather Company and its Twitter partnership, IBM is very much highlighting Watson’s ability to draw insights from datasets that its competitors don’t have access to. This makes data and analytics services perhaps the most crucial differentiation of the Watson portfolio against other AI competitors. Despite all this complexity in innovation, in our view the most important aspect of the Watson portfolio is the portability of data. This mitigates concerns about vendor lock in. If needed data can get anonymized, however, customers that go down that route would lose the upside of continuous learning.

Overall, the examples are starting to trickle in, and experiments are underway for both client use cases and embedding of Watson capabilities into the broader IBM organization (e.g. GBS group, Cognos). What we still see as market confusion/hype is the pace of change, especially at the forefront with the timeframe for deploying Watson in a client environment. A financial services client we spoke to that has been on this journey with IBM Watson for a couple years now and had an insightful comment, “Watson used to be a product; it is now a brand.”

IBM must focus on not just painting the art of the possible with Watson, but also presenting the market with realistic expectations taking into account the level of customization, tuning and data curation needed to start driving value from Watson, the progress on integration into other groups and IBM’s overall positioning around Watson as a big scalable business as of today. Marketing strategies aside, in the Intelligent Automation market, we believe there is no such thing as a turn-key solution. it is all about transformation and data curation should be the centerpiece. As the player with the broadest set of capabilities in the cognitive market, IBM has had the largest learning curve that it can use to its advantage to guide enterprise clients on the journey to more Intelligent Operations.

The rise of the Virtual Agents

The strong expansion of capabilities of Watson is aligned with the findings of HfS inaugural Intelligent Automation Blueprint. Despite the market’s obsession with RPA, HfS is seeing broad AI capabilities coming to the fore. In particular, we are seeing the emergence of the notion of Virtual Agents that are underpinned by broad process and automation capabilities. These agents range from the heavyweights Watson and Amelia to OpenSource avatars. However, in this context Watson is standing out as IBM is turning it into an ecosystem play where partners can provide services and capabilities on top of the building block. At the same time, we are seeing traction of cognitive engines, such Celaton for integrating unstructured data or RAVN, as an example of vertically focused machine learning and Enterprise Search. Stay tuned for our upcoming research on the changing notion of service agents through cognitive computing.

The holistic notion of IA but also the disruption stemming from it, is best described by the case study of KPMG. The company planning for and investing in the disruption of their core business, i.e., tax, accountancy, and advisory, which can hardly be described as being high on the technology affinity list. If we see the rise of robo-accountants, one gets a feeling for how the disruption around activities such as compliance, reconciliation or data entry will look like a few years’ time. However, in the view of KPMG this rise is a double-edged sword as it is expected to create more work for its partners through much more thorough and efficient discovery processes.

Adjusting the ethics of AI

Having listened to the many use cases in the medical sector, notably around oncology research, is nothing short of humbling. Yet, the strong acceleration of AI raises also many ethical questions. Fundamentally, as an industry we have to help clients with the transformation of knowledge work but also have a much more honest and transparent debate of ethics. A first important step in this direction is the formation of what is awkwardly called the “Partnership on Artificial Intelligence to Benefit People and Society” supported by Google, Amazon, Facebook, Microsoft and IBM. More commonly referred to as AI Alliance, the new body is tasked to “conduct research, recommend best practices, and publish research under an open license in areas such as ethics, fairness and inclusivity; transparency, privacy, and interoperability; collaboration between people and AI systems; and the trustworthiness, reliability and robustness of the technology”. While it is easy to put down these ambitions as an aspiration, more openness and clarity is critical to advancing service delivery in a responsible manner. If we are really moving toward a virtual workforce, a blend of humans and algorithms, and broad consensus on ethics is mandatory.

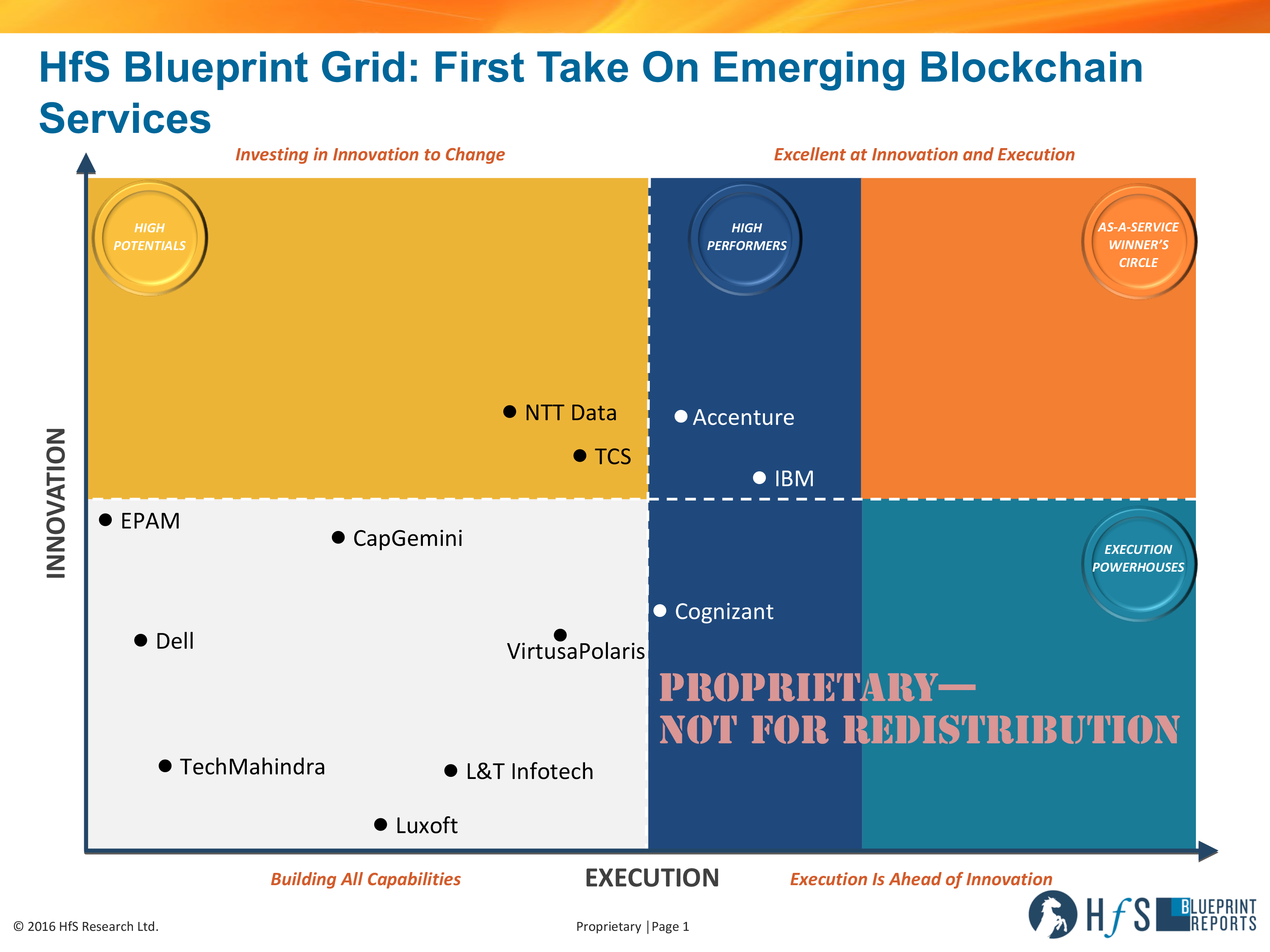

I love blockchain – all the hypesters think its the biggest thing since the Internet, primed to blow up the stranglehold banks and corporates have over the world and how we deal with money, while others are dismissive, viewing the tribalism of governments and their paranoia of loosening up cross-border regulations, as the ultimate impediment behind blockchain ever fulfilling its true potential. And there are the techno gloomers who struggle to see how we can really make this thing enterprise ready and feasible in real world business situations.

So why not read the first ever analyst view of how emerging blockchain capabilities are evolving with today’s fleet of service providers:

I wanted to share briefly some nuggets from report author Christine Ferrusi-Ross‘ great blog on the core recommendations:

Clients and their service providers are learning blockchain together. This is bad if you want someone to hold your hand and tell you everything is going to be ok, that they have the answer for you (by the way, no judgment from me on this – if there’s a well understood solution and you can hand it over to someone to get it done, go for it.) BUT it’s fantastic if you really want to take control of your own business destiny, be strategic and really work collaboratively with a partner to find the right opportunities and create solutions together. It’s a rare chance to be an equal intellectual partner with your services firm and in fact potentially for the provider to learn from you as your team researches opportunities and bring in the provider to help test some of those opportunities.

Find great storytellers. It’s really important to understand the technical aspects of blockchain, of course. You’ll have an easier time finding technical skills than you will finding people who can really dream with you and tell you stories of how blockchain can change the world. This isn’t just about looking for strategists, it’s about looking for providers who can clearly communicate a vision for what’s possible, so you in turn have an easier time digesting the different scenarios and selecting the right ones to move forward on to the proof-of-concept stage.

Put more emphasis on service providers’ partnerships than usual.Spend more time understanding what criteria the providers are using to evaluate the technology vendors than you would normally, since this deep dive is going to be more important for you than in other more mature areas.

Focus on service providers’ abilities to work in agile development environments. Yes, I know, you’re likely not even close to building anything right now. But keep in mind that you’re looking to find someone to co-create with you and that requires the ability to be iterative and flexible while still not losing sight of the original goals. Providers who have more rigid engagement methodologies will put more pressure on you to define your requirements probably even before you really know what those requirements are. So look for a player that has strong agile skills since those skills will transfer well to your blockchain exploration.

In the meantime, here’s a link to the full HfS Research Emerging Blockchain Services Blueprint Guide, with definitions and descriptions of the current activity (particularly in BFSI) and how service providers are approaching this inevitably integral part of the future fabric of any industry.

Service providers in the last decade have made significant efforts to pivot from commoditized IT and BPO services to more “higher value” services like research and analytics. We know this has been the direction of the industry up to today. Analytics services have had the fortuitous blend of:

higher margins

rapid market growth and demand

evolving offerings/scope for differentiation

the potential to make big impacts on clients’ business performance

From the likes of IBM to the smallest boutique analytics house, there’s enough room for everyone to grow right now because of these factors. However, with the significant pace of change we’re seeing in the services industry overall, will we still live in the same market in five years’ time? A few factors that our research points to could really shake up the portfolio of work that analytics service providers feast off of today.

Here are three critical success factors for analytics engagements that service providers will need to address if they want to be in business in five years’ time (btw 2021 is just in five years!):

Mash up automation advancements with analytics services: So much of analytics revenue in the days past and present revolves around better data management – extraction, deduplication, cleansing and enrichment. These are manual tasks that were often outsourced; and now need to be automated. Similarly, ongoing report generation has much room for efficiency where analysts spend too much time on routine data-pulls and chart population. The writing is on the wall – repeatable, rote tasks can be automated to a great degree today, whether you use RPA or other more intelligent IA technologies (read more about our continuum here). These big revenue sources will dry up or become even more commoditized as this shift occurs. Service providers need to test new grounds to find the right “human + machine” combinations across the lower rung of the analytics services value chain, not just concentrating on machine learning as a means of developing the next best algorithm.

Calibrate and experiment with the right skills/location mix to really deliver business value: Service providers need to partner and take some risks to figure out answers to questions like – How much onsite presence do you actually need vs. are willing to spend on, and what impact would that have on the results of the engagement? What types of multi-disciplinary teams do you need to bring together to bridge the gap of having teams that are “too technical”, “don’t understand our industry” or “aren’t really working on cutting edge data visualization?” These are the usual complaints I hear from analytics clients, even though they don’t have the right answers either – perfect data scientists that have advanced skills across tech and business are unicorns today. Providers that want to stick around need to invest in broad curriculum ecosystems (internal/external) to create this talent pool for the future as well as experiment with new team/skill compositions.

Develop IP, partnerships and business models somewhere between prepackaged portfolios and “futuretech”: Most service providers will have a traditional “restaurant menu” of analytics solutions for customer, risk, operations, and industry verticals…the models are 80% of the way there and customized for client environments, with ongoing model validation. They will also have a super-jargonated mega solution at the cutting edge of technology (read: no clients yet) that seemingly solves all your data and analytics challenges with one swift implementation, but comes with a significant price tag and a lack of resources that actually understand how to work the solution. The truth is, a lot of clients seek something in the middle – a stable, trust-based partnership where instead of being tied into global rate cards for traditional services, both parties can test and develop digestible new projects and incentive structures. The client of a big analytics service provider explained to me his challenge with this approach, “Their short engagements were never short, nothing less than 15 weeks. Their processes aren’t nimble enough for the kind of work we’d like to work on with them.”

In the next five years, wherever enterprises believe they are in their analytics journey, they are still going to be in an organizing phase. They are still figuring out how to develop further their technology platforms, data extraction and integration, big data infrastructure, data scientists, PhD and analyst skills development, relationships with analytics service providers, and an overall organizational reorientation to be more data-driven. To make real progress, service providers and clients will need to collaborate, experiment, and connect and partner across business units and regions. It also means partners will need to work through confusion, duplication of effort and change management, because we are talking about behavioral change here. Service providers that want to win analytics services business in 2021 need to be prepared for these changes, in client organizations as well as the analytics engagements that will be demanded by them.

Breaking down the barriers between the end-customer and the business support functions is so pivotal for success in today’s world of the OneOfficeTM. And one place to start is by identifying the potential intersections where there is a shared outcome. We’ve seen how this approach can work for sales and procurement, leading to increased sales and compliance.

In my colleague Derk Erbe’s post, Why We Should Love Procurement, he encourages the much-maligned procurement organization to “be a business facilitator” and the business to be a partner with procurement to contract, buy, and use services from third parties in the most beneficial way for the business.

Just recently, I heard three good reasons to “love procurement.”

This story of collaboration between procurement and sales led to (1) increase in closed deals for sales, (2) increase in compliance, and (3) increase in mutual respect. It also, by the way, caught my attention as an example of using Design Thinking for an internal function, taking a stakeholder-centered (empathetic) approach to defining and solving a problem.

Thinking “outside the box” on how the skills of a sourcing professional are relevant to the business more broadly

In this example, the global sourcing office that provides support for contract management at Equifax, among other sourcing activities, had little interaction with the sales team, whose activities had some “loose ends.” At times, contracts were signed, for example, with non-compliant terms and conditions, some of which the company was not set up to deliver effectively in a timely fashion… if, in fact, the execution team could access the signed contract, which may just be sitting on the sales team member’s hard drive. The right people were not getting involved at the right time with the sales team to help shape, close, and deliver the business. Some of these “right people,” the Equifax leadership team realized, are in the sourcing organization, and are not just compliance experts, but also have a negotiating capability that could be better applied to its business more broadly.

Here’s where Tim Brown, SVP, Equifax Global Sourcing Office, and his team took a Design Thinking approach to defining and solving the problem. Giving some thought to what matters to the sales team – closing deals and booking sales, he tapped into relevant expertise on the sourcing team—people who buy products and services. The sourcing team for the company is a set of professional buyers, and the sales team is a group of sellers. What if, under a mandate of change, instead of providing a checklist of terms and conditions and hounding sales teams which sourcing groups are often (justly or unjustly) better known for, he offered the sales professionals something that addresses directly what they care about: closing deals.

Role playing may be awkward at first, but it can turn into coaching and valuable interactions that drive business results

The sourcing team offered to role play – “let us be the buyer as we have sourcing buy experience and can help you practice and also test/understand the buyer point of view.” As the dialogue played out, there were times when the sales team realized that the procurement professionals were sometimes a step or three ahead of them in the negotiations… and the sessions turned into real strategy and coaching interactions.

In some cases, the sales team started bringing the procurement team proactively into deals and coordinating support through them. They became a team with a shared goal – grow the business, and in a compliant way. Because the procurement team is now a part of the sales process, there is more interaction, and therefore, more likelihood of adopting the common terms and conditions, faster escalation and resolution of issues, better contract management… In addition, the sales team is closing deals more expediently.

Bottom line: The sourcing team took an empathetic approach to understanding what would be relevant and valuable to the sales team, creating a valuable intersection, which also led to addressing challenges around contract management and compliance.

The teams, as a result, work more collaboratively and close business more effectively and efficiently. Procurement and sales, therefore, are partners in growing the business, from the back through the front office, most likely creating a better experience for their customers as well.

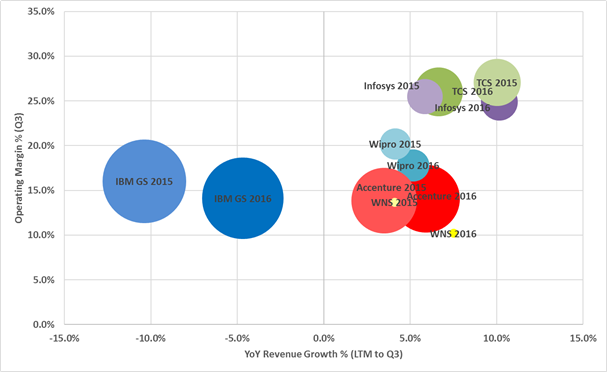

It is that time of the quarter again; we are about to see a whole raft of quarterly results for Q3. HfS uses the results as a barometer for market performance, and we make decisions around the market sizing and forecasting from these numbers. The Q3 figures will give us three-quarters of the year’s results, so they start to give us a good idea of what the year is shaping up to be. We have already seen some important results from the early announcers, Accenture, TCS, Infosys, IBM, Wipro and WNS providing us with an indication of what is to come and speculate about the overall results.

As we mentioned in our recent analysis of the HCL / IBM partnership, the IT market has become much more complicated. For services buyers, it has impacted their ability to choose the right solution alignment for their businesses and for service providers in selecting the optimum places to make their investments. This is exacerbated further with the emergence of new disruptive competitors, both on client and provider sides, threatening the marketplace. In the past, we tried to simplify this market disruption by characterizing it as “two tier”, with service providers either being traditional or more “As-a-Service.” The theory, over the past 2-3 years, has been that growth will be slow, or non-existent, in the traditional services markets, while we will see emerging As-a-Service markets like cloud, BPaaS, digital and intelligent automation, growing in multiple double digits. Many of the traditional providers will experience revenue declines in this period as they burn through their backlogs of legacy contracts, particularly the large multi-tower outsourcing deals they may have. With most of these contracts morphing into As-a-Service delivery models or becoming increasingly cheap as the FTEs get reduced over time.

When we looked at the early announcers, at the start of the year, we predicted that the market would find renewed growth, as the market started to adopt the Ideals of As-a-Service, and growth in new business outweighing the decline of traditional spend. If you look at the performance of the early announcers in the chart, broadly this is true, with all the providers improving in revenue growth over the past four quarters, compared to the same four quarters last year. We use the twelve-month trailing data, as quarterly growth for individual companies can often fluctuate, and this gives a better direction of travel.

Bottom Line: Early signs are encouraging, but we need a consistent cadence of positive results over a sustained period

It is still early days – both with these secular changes to the market and in the results season for this quarter. However, if we see the rest of the market improve in a similar vain, we may well see growth rates improve for the IT and BPO services market, right across the board. This may be confined to more discretionary IT services markets like consulting and systems integration for the time being, and industry-specific BPO markets, such as insurance and healthcare. However, if this trend continues, we may see growth in infrastructure management spend in 2017. This is particularly significant for infrastructure as the market has been in decline for the last three years.

Over the next two months, as we digest all the results from the major IT and business services firms, we will form a viewpoint whether the market, as a whole, is seeing improvement and in what sectors. For example, whether the shift left of the offshore majors is set to continue in 2016 and beyond. We may also start to see signs that the IT and business services market might escape the low single digital purgatory it has been stuck for the last five years.

Still confused about what robobosses are and why you may be working for one soon… according to some experts?

Well, your confusion will soon be over, as we’ve assembled the ultimate interstellar panel consisting of client leaders, technologists, service providers, analysts and advisors to debate – once and for all – the true impact of cognitive computing, artificial intelligence, IT automation, robotic process automation software and smart algorithms are having – and will have – on our lives, our jobs, our enterprises, our politics and our society.

Your Robo-Host: • Phil Fersht, CEO and Chief Roboboss, HfS Research

Robo-Participants should learn about: • How should we define what a “Roboboss” is… and should be? • How far from reality are today’s viewpoints from other “experts” – what’s real and what’s fantasy? • Do we need a Code of Ethics for Intelligent Automation and Cognitive? • Where are we going to see “real Cognitive applications” in the short-medium term? • Where should we start our Intelligent Automation and Cognitive journey? • Are today’s service providers really going to be the enablers of Intelligent Automation and Cognitive? • Buyers – if you could start this all over again, what would you do differently? • How can we develop “Cogno-boss” skills? • What is the Real Endgame with Intelligent Automation and Cognitive?

Your Robo-Panelists: • Lee Coulter, CEO Shared Services, Ascension Health • Matthew Heffron, VP Innovation Initiatives, Wells Fargo • Mary Lacity, Curators’ Distinguished Professor, UMSL • Cliff Justice, Partner and Innovation/Cognitive Lead, KPMG • Dr. Thomas Reuner, Research VP, HfS Research • Chitra Dorai, IBM Fellow & CTO Cognitive Services, IBM Watson • Mihir Shukla, CEO, Automation Anywhere • Chetan Dube, CEO, IPSoft • Alastair Bathgate, CEO, Blue Prism

After attending HR Tech in Paris this week, it became apparent just how much the HRO market is changing. This change has started to happen across the board: service and tech providers, buyers and (even some!) analysts are starting to identify and adapt to the new era of HRO—as HR “Intelligent Operations.”

Having personally had experience in different areas of BPO, it’s been extremely interesting to look at HRO with a fresh pair of eyes. So, given that it’s Friday I’m going to condense my takeaways down to the following points:

The move to the cloud is not the end point: In HfS’s Eight-Ideals of the As-a-Service Economy, the starting point for organizations in the As-a-Service journey is Overcoming Legacy. It’s important to realize that this is indeed the starting point and not the end goal. I hear all too often from buyers that they go through all the pain of implementing a cloud HCM system and then end up with the same functionality and using the same processes they had with their legacy system. This should be the organization’s first steps in transforming their HR function, so partnering with a provider that recognizes this and will take you on that journey is crucial.

OneOffice is alive and well in HRO: Having previously covered the contact center space, I’m noting the increasing parallels between the front office customer experience and HR. What I will say though is that HR is five steps behind the front office, but we all knew that, right? The increasing focus on the employee experience can be directly compared to the focus on customer experience we saw starting in the noughties in contact centers. The increasing use of digital employee engagement through mobile and social looks very similar, although very much less mature, to the frantic race for digitization of the front office. Essentially what we are seeing in HR is more of the consumerization we’ve identified in the front office.

Outcomes, outcomes, outcomes! And more OneOffice: Keeping to the OneOffice theme is the increasing focus on business outcomes through HR optimization. In my point above I mentioned employee engagement. While this is an important endeavor it, in itself, is an HR metric and should be viewed as such. Rather the focus should be on improving real business outcomes such as reducing product development cycle times, increasing revenue and improving margins. These business outcomes are influenced by numerous factors including HR, and metrics like employee engagement are a means to drive that, but employee engagement is not the end goal. It is important to note that employees are also customers, and alienating these customers through abysmal hiring practices and sub-standard HR functions seems counterproductive.

HR conversations are moving out of the director’s office and into the c-suite: With business outcomes been the goal of HR, HR now needs a seat at the c-suite and a an active voice on the relevance of digital. Cloud, analytics, and automation cannot be effective in enabling business objectives if they are implemented in a tick-box fashion due to a directive from above, with no real sense of what impact it will have. Therefore the c-suite firstly needs to realize the impact HR can and does have on business outcomes and then endorse the strategic changes to HR functions that are needed.

So this is my take on the changing shape of the HR market coming out of a week of conversations at HR Tech and findings over the last few years. Furthermore, I want to introduce the idea of the OneHR concept (more to come) where typically siloed aspects of the HR value chain (hiring, talent management, benefits admin, learning, payroll) are continuing to merge into a unified HR experience for the employee. This is taking place within the technology realm but has some way to go from a services standpoint. Like I said, more to follow.

Predictive analytics in human capital management continues its slow but inexorable march out of the sizzle phase and into the steak — or for my vegan friends quinoa — phase. As this phenomenon is occurring, a few topics are getting considerable air time.

These include:

How are predictive engines adapted and applied to the unique business context of every organization – and by whom!

What types of predictive capabilities in HCM solutions (largely algorithms coupled with machine learning and human testing) have the most relevance and value to a particular HR/HCM agenda?

Will the predictive analytics guide in solving business problems? … and the all-important …

How much do data scientists earn and can HR afford them?

Forecasting the winners… more to come (winners and research)

An HCM or Talent Management offering that lacks a compelling predictive analytics strategy and capability set, and is competing outside of smaller companies, is akin to the proverbial “dog that won’t hunt.” (Yes I’ve fully acclimated to living in the South). Although from the buyer perspective, trying to unpack a vendor’s people analytics strategy, or just distinguish it from other capabilities out there that sound awfully similar, might keep some dogs hunting for a while. I’ve maintained for years that the HR tech market needs much more clarity around how solutions are different and why the difference really matters, in a language that typical HR professionals relate to. The absence of this makes the landscape more cluttered and more confusing for buyers.

I’ll be covering key operational and technology dependencies that affect the leveraging of people analytics in my upcoming HfS Blueprint Guide entitled “Predictive Analytics in HR Technology.” This will be published in early March 2017, but way before that, my related HfS POV is coming out in the next week or so. Among other things, it will offer-up a new industry metric called “Time to Predictive Value.” For now, here’s a preview.

Assessing a solution’s predictive analytics capabilities – checkmark or not

Here are three lenses to apply when evaluating whether an HR tech product’s predictive analytics will achieve desired outcomes; and by product, I mean HRMS platform, Talent Management Suite or HR Point Solution:

Time-to-Predictive Value (“TtPV”) is my stab (POV forthcoming!) at creating a meaningful guidepost to help judge one aspect of a product’s capabilities in this realm. It will hopefully bring some much needed clarity to a domain where, for example, “retention or flight risk” -– not a very meaningful metric in isolation, as most metrics aren’t –- often gets a vendor a quarter or half-way toward qualifying for a predictive analytics checkmark.

There are various operational dependencies for leveraging predictive analytics in HCM (or within any business discipline), such as having a large enough relevant data set, sufficient analytics and data science competencies and staff, pursuing closed-loop validations with well defined scenarios, applying appropriate calibrations for different data (e.g., job and organizational) contexts either performed by people or machines (via machine learning), etc. These dependencies and conditions typically take time to be addressed –- from weeks to months or longer. Buyers should have a sense of when they will actually see the predictive value manifesting itself, as that influences ROI and is also a major input to my lens #2.

Degree of Predictive Analytics Business Impact: There’s a wide range of potential business impact and value to be derived from these capabilities in HCM. Two factors that seem to correlate with impact beyond TtPV:

– Whether the best actions or decisions are being guided by the predictive information. In other words, is the analytic prescriptive as well as predictive? (A reason why retention risk in isolation probably has less value than what is often hyped.)

– Is the business problem being solved/avoided, or opportunity created, going to deliver noticeable competitive advantage? Examples include knowing the most important predictors of job success in a critical role, or what factors materially drive or impede employee productivity or customer retention, or is the organization truly ready to succeed on a strategic initiative?

Finally, Innovativeness (yes, it’s a word) of the predictive analytics capabilities: The more innovative a set of these capabilities are, particularly if they lead to practical and measurable business value delivered in relatively short order, the more it inspires other creative ways for solution providers to help solve HCM business problems. Data correlations and cause-and-effect relationships that are very intuitive to discern or simply the product of good common sense (e.g., freezing salary increases or cutting back on company-paid benefits will likely result in a spike in employee turnover) earn very low marks on the innovativeness scale.

In contrast, when Walmart years ago determined that putting diapers on sale will often lead to increased beer sales (somewhat logical, but only AFTER the non-intuitive relationship was discovered), now that’s a winner.

Bottom line

People analytics is hot, and predictive capabilities is a major reason why. But in order for customers to derive business value commensurate with what they are paying for the surrounding solution, they must look beyond the sizzle and assess the quality of the steak in meaningful and business-relevant ways.

Procurement BPO has changed substantially over the last decade. Growing maturity of procurement technology and commodification of significant parts of the procurement value change altered the value proposition of procurement BPO: From very large lift and shift outsourcing deals, heavily dependent on labor arbitrage, to smaller (about a fifth the size of ‘legacy’ deals) engagements leveraging procurement platforms, advanced analytics and intelligent automation. This exemplary of the shift in services we call the “As-a-Service Economy”. As we interview service buyers and service providers for the 2016 Procurement As-a-Service Blueprint, we home in on five facets representing Procurement As-a-Service:

Continued use of automation and robotics in services. Transactional procurement has changed tremendously. Not only by better platforms (see #5) leading to fewer and fewer exceptions in processes, and processes and exceptions that can’t be handled on a platform can be done with Robotic Process Automation. As an illustration: in spend analytics automation is used to automatically aggregate, cleanse, validate, classify and report spend data. Further areas with lots of intelligent automation potential are invoice processing, purchase order management, contract management, auto-routing of exceptions to stakeholders, invoice matching procedures, payment status and tracking.

Traditionally, the ‘higher value’ activities in contract management, category management and strategic sourcing have been consultancy driven. Skills are scarce and hard to repeat and scale.

It’s about knowledge and expertise and labor intensive processes. The market sees an accelerating talent issue, as category and sourcing experience is scarce and you can’t buy experience. Really good sourcing or category experience is built over a minimum of 10 years and many experts are retiring at a higher rate than new talent can be brought on. So there is a need for knowledge management and an opportunity with cognitive and AI becoming more mature to solve a part of this puzzle.

With cognitive platforms maturing, we will see a change in the more strategic parts of procurement.

Strategic sourcing and category management expertise and capabilities. Sourcing and category management drive a lot of value for clients, for instance in tail spend. There are many small categories, small sourcing events and potentially poorly sourced products in enterprises, which don’t warrant building in house category expertise. Procurement As-a-Service providers are expanding internal category management and sourcing capabilities by attracting and retaining more sourcing talent, arming sourcing and category talent with more and better analytics, insights and market intelligence and nurturing an ecosystem of partners, growing in the role of brokers of capability.

End-to-end capabilities. Service providers increasingly bring in traditional sourcing consulting skills into Procurement As-a-Service delivery, opening new doors to buyers looking for consulting skills at lower (BPO) costs, enhancing capabilities across the value chain. Procurement As-a-Service covers the entire Source to pay (S2P) Value Chain. The growing role of technology is enabling closed loop processes, with advanced analytics creating continuous feedback loops. New value creation in transactional procurement hinges on one to many solutions and services, deriving data and bundling insights across multiple client engagements. The game in procurement business services is scale, being able to deploy limited skilled resources across multiple clients, not on the project basis but on concurrent, day to day, shared basis.

Providers’ ability to bring sustainable change to the client organization is key to Procurement As-a-Service. Traditional challenges are compliance with procurement policy, contributing to transforming the procurement function and stakeholder management as part of continuous change management, beyond the transition period.

Commercial models. HfS’ research shows that while As-a-Service delivery is gaining ground in many horizontal and vertical offerings, the adoption of As-a-Service commercial models is lagging behind. Gain-share was popular in the early days of procurement outsourcing, but its popularity seems to have faded since in many cases the wrong behavior was incentivized. Determining actual savings and which part of the savings should be contributed to whom proved a nightmare. We are having a good look at how service providers supporting the As-a-Service vision introduce new commercial constructs and if they are bringing those into existing client engagements.

Platforms. Procurement technology is now much more integrated in platforms, where much of the technology of the past was separate, heavily customized and bespoke (point) solutions. SaaS enabled technology platforms such as Ariba, Coupa, SMART by GEP, Tradeshift, Accenture’s Radix and Capgemini’s IBX have taken a significant role at the core of procurement. In a nutshell, platforms consolidate a set of suppliers, automate most processes and put (commoditized) processes at the fingertips of buyers.

Platforms are eating into the traditional procurement outsourcing model. The mega deals of the past slimmed down due to the degree of technology being sourced, reducing human labor dependency in procurement. Key ingredients of Procurement As-a-Service are usage of platforms, services with embedded platforms, services around platforms and integration of platforms in service delivery.

What To Watch

Winners in Procurement As-a-Service are those providers going beyond merely providing a replacement or extension of existing procurement, by providing a vision and strategy for the future of procurement.

This vision includes:

Leveraging multi client insights, experience and buying power

Models for Customer management

Providing smart solutions for indirect (tail) spend

Expanding expertise in strategic sourcing and category mgmt

Putting Intelligent Automation at the core of (digital) procurement operating models

Leveraging procurement platforms (proprietary and 3rd party) in engagements and the ability to provide technology management across clients in a one to many model

Building closed loop processes

Data and information foundations

Using advanced analytics for (near) real time information and insights

Skills in consulting, technology and relationship management

End to end supply management

Creating communities for clients

The 2016 HfS Procurement As-a-Service Blueprint will investigate the progression service providers have made on the As-a-Service Journey, their vision for the future of procurement and their ability to bring this vision into the real world of procurement.

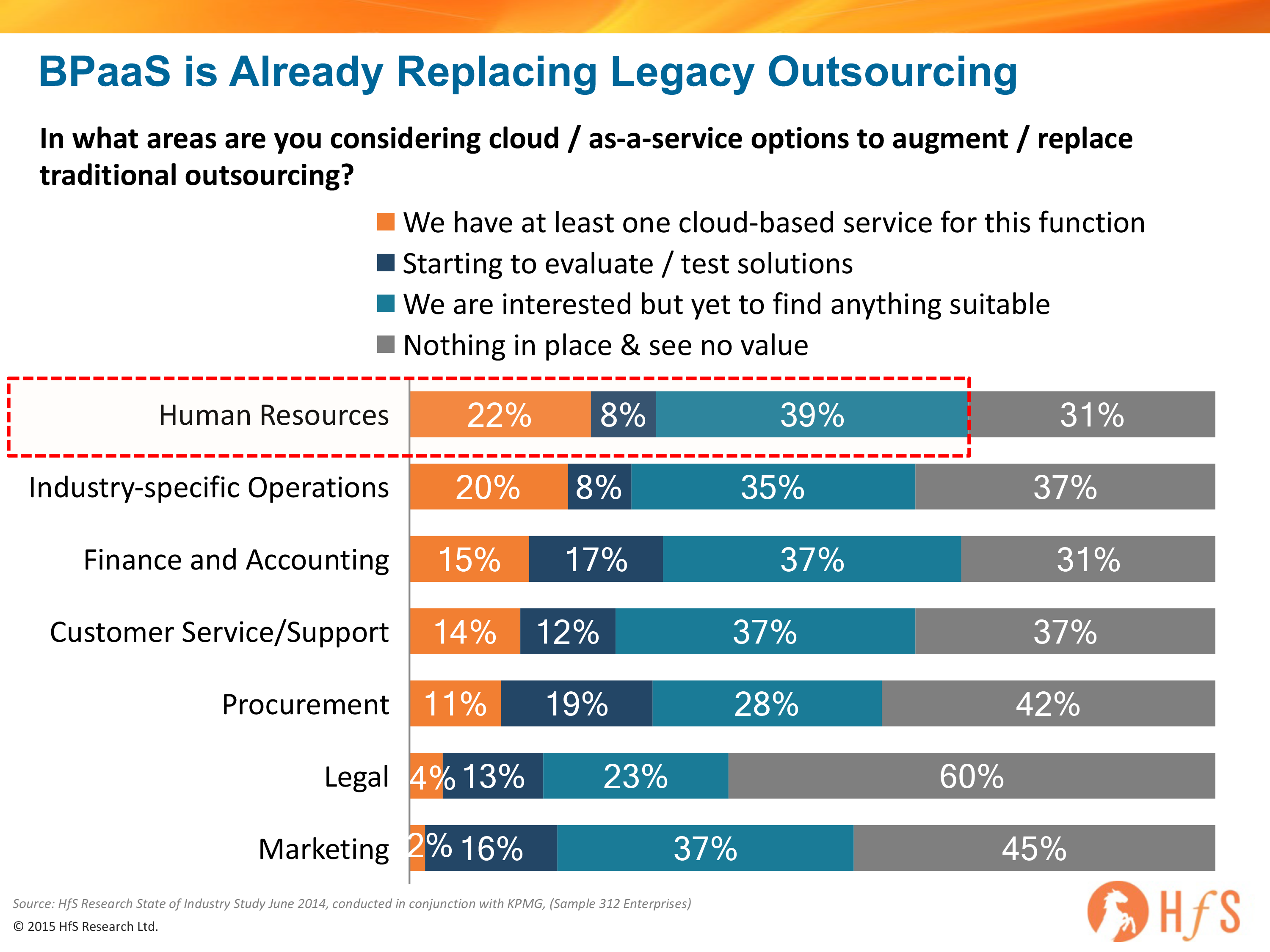

The rise of cloud-based HCM platforms has been a key driver in pushing the business case of HR to the c-suite and making HR one of the primary focus areas for IT managers. Further highlighting this point, in a recent study (attached chart) HfS identified HR as been the leading business unit adopting cloud implementation and BPaaS support. This movement is leading to the days of the dreaded green screen fading into the distance and slicker, user-friendly and more compliant HR cloud platforms becoming the norm, thanks to SaaS.

Whilst these platforms have largely been extremely positive for HR managers and employees alike, process change management and continuing integration issues have made these systems far from fool proof. Continuous updates are a headache for organizations to absorb, incomplete compliance functionality is a constant thorn in legal’s side, and piecemeal buying of these platforms has hindered the benefits organizations can glean from them.

NGA has just introduced a new offering into this market that is designed to be fit for purpose and globally compliant. It’s built around SAP SuccessFactors as a bundled software offering including the NGA’s proprietary MyHRW, and PEX platforms. PEX allows for integration with payroll systems. cleaHRsky will be front ended by SuccessFactors Employee Central and include an interactive case management portal, AskHR as well as transactional automation in support of processes, reporting, and interfaces.

Here are three characteristics of what NGA is offering:

Support for Local to Global Growth: CleaHRsky will be marketed to medium, private domestic firms that do not have established, centralized global HR functions and are mid-sized multinationals between 5,000 and 25,000 employees aspiring to become global. In the interest of practicing what they preach, NGA is in the process of rolling out cleaHRsky internally.

Plug-and-Play Functionality: The solution pivots around a “grow and evolve” approach. NGA is offering it to clients with Employee Central and therefore core HR at the heart of the solution. Clients can then opt in to deploy payroll and talent management support as well as expanding geographically. NGA is seeking an aggressive implementation time-frame of 14 weeks including change management for core HR functionality aspects of cleaHRsky

Mobile and Social Support: cleaHRsky will include essential components of SuccessFactors which will be optimized across mobile and social channels. In support of cleaHRsky, NGA will provide a global best practice catalog to support in-house processes of the implementation.

Will it work for everyone? No, the preconfigured nature of the offering will not work across the board. The solution is better suited to organizations that are seeking more vanilla HR standardization across their operation. There is a certain degree of customization within cleaHRsky, but its core aim is to be a fit for purpose SuccessFactors implementation. I have spoken to many buyers who have dived head first into implementing cloud HCM platform and in some cases, these buyers have ended up using the same functionality and processes that they did on their legacy platform. In short, a key attraction is that this approach is how it can remove much of the consultancy and internal debate over SuccessFactors module usage and processes to optimize use of SuccessFactors based on NGA’s experience.

The key challenge for NGA is selling an end-to-end solution of this ilk, especially in the upper end of NGA’s target market (up to 25,000 employees). At these larger companies, the need for customization to fit standard procedures generally increases and HR and finance departments are more formally separated internally, often requiring a top down, transformative approach to HR. Currently many of NGA’s relationships remain with the VP’s of HR making this level of transformation a challenge. NGA requires a new approach to get c-suite buy-in and has been acquiring sales talent, over the last year, in support of this.

NGA is putting its weight behind this offering and has stated that cleaHRsky will be its “go-to” offering for all organizations that fit within its target range. This big push could be just what NGA needs to kick-start adoption of cleaHRsky and entrench itself as an HR transformation partner.