Remember all that wide-eyed excitement when we first started using the “Information Superhighway” known as the Internet? Remember how we were all going to use this amazing new media to share information, to learn from millions of new information sources, and – even more importantly – to learn from each other?

So what’s gone wrong? Why has the Internet also become a mechanism to block out information and promote factless discussion and news, often based on misinformation, lies, propaganda and emotion?

How have we managed to survive a year and a half of election campaigning, where we endured two sides obsessed with battering each other with insults, almost completely devoid of any smart new policies, practical debate and absolutely no ability to listen to each other. Our whole world of politics has become driven by emotions and personalities, not facts, ideas and policies.

I am sure I am among many of you who have fallen out with friends, unfriended people (or been unfriended) on Facebook, received abuse on Twitter and been sucked into nasty arguments with others who just refuse to listen. And if I had to dig deep into my conscience, I have to admit I may not have always listened to the rationale of the other side also.

But can we all get past this experience and learn to listen to each other again? Can we learn to have rational debate and conversation, where we can express our views, back them up with real facts and ideas – as opposed to this closed, angry style of discourse, that is threatening to divide entire nations?

I like the steps I am seeing from Facebook’s CEO Mark Zuckerberg to clamp down on “fake media”, especially when you consider that more Americans admitted to relying on Twitter and Facebook for their news sources, than any other media source. And can you blame them when the likes of Fox, CNN, the New York Times and many other outlets – all have their biases and did little to bring together real discourse and debate. All they did was whip up more hatred, panic and emotion to divide us further.

So… we all ended up take to social media to get our news and views away from the blurred lines…. and instead of sharing facts, all we are doing is winding ourselves up, blinding ourselves from finding compromise and hiving off social contacts we once considered “friends” (both the physical and electronic varieties).

The Bottom-line: It’s time for all the stakeholders in society to get meaningful and respectful again

Whether we like it or not, we now have four years of President Trump – he got himself elected. He won – seemingly against all the odds. Now let’s sincerely hope he can work to bring together a divided nation and bring together people across this divide of hate which he helped create. If he is to be successful as a President, it’s healing this awful culture of factless, meaningless squabbling. The US doesn’t need it’s own half-Brexit, where the country can’t decide what it wants anymore and people have to move forward clouded in uncertainty and confusion.

In the last week, President Trump has made appointments to his cabinet that are concerning for many. But sensationalist reporting devoid of actual facts has also skewed the true merit for concern and the weight of the issue. We need our media to provide information so we as citizens can express our voice based on facts and not fear that may or may not be warranted. The last thing we need are our already-fractured social networks being further eroded by all this emotion, paranoia and hype.

We need decisive policies, politicians working together and (at least try) to develop some mutual respect with people, whose views may not be entirely aligned with us. I don’t like the way the world has become, and I think most of you here will agree that it’s time for our media, our politicians – and ourselves – to get meaningful and respectful again.

The latest acquisition targets for large system integrators are SaaS services providers. And why not? It’s one of the hottest, fastest growth areas in the IT services market today, and a natural evolution for the traditional IT services providers, whose revenues from supporting legacy on-premise ERP engagements are in gradual decline.

Unlike the obedient, tuck-in acquisitions of yesteryear, however, system integrators realise that the acquired SaaS services specialist providers need to be highly visible and prominent to clients, and even lead the newly-combined practices.

The reason for this, is that system integrators are buying a new generation mindset and client engagement approach in their SaaS services acquisitions that they are struggling to adopt themselves. Yes, they also gain access to some new strategic clients, and boost their certified consultant pool, which remains important to maintain credibility and scale in the market. But the real nugget to succeed in delivering SaaS services, lies in understanding the massive change management challenges enterprises face, when migrating from an on-premise environment to a SaaS one, and the ability to offer the emerging flexible services that support clients through their SaaS transformation journeys. The traditional IT services life cycle of old, that includes consulting, implementation and management services, requires a serious overhaul to meet emerging client requirements (see: Thinking Outside The Box To Support SaaS Applications and SaaS Services Success Requires A Different Approach).

Clients want to work with service providers offering more flexible services, including access to skilled resources, whenever and wherever they are required, supported by flexible pricing models. Moreover, the service provider needs to demonstrate commitment and focus to its chosen SaaS service area. Clients also appreciate a service provider that is not afraid to challenge their decisions. In fact, they increasingly expect this, as service providers have the experience to understand the implications of all steps taken during the deployment phase.

System integrators’ understanding and development of the new SaaS approach to services vary, and convincing prospective clients about their renewed approaches often remains a challenge. Enter the SaaS specialist service providers, many of which have an established position and credibility in delivering SaaS services. They don’t just have an impressive pool of techie consultants that could slot into a larger practice seamlessly. They get it. They have developed a modern approach that is appreciated by enterprises and the SaaS software vendors alike. For this reason, we are seeing system integrators position their acquired SaaS service providers up front and central. Meteorix has a leading place at the IBM Workday services table (IBM makes a meteoric rise into the HR-as-a-Service big three) as does Bluewolf in the IBM Salesforce practice (IBM Culls The Pack Of Salesforce Partners By Buying Bluewolf). CEO and co-founder of Workday specialist, DayNine, Tim Ramos, will lead the new Accenture DayNine group to deliver Workday services, (Accenture Acquires DayNine and positions itself at the forefront of the race for Workday services) . And Wipro executives talked about a ‘reverse integration’ of Appirio’s business into Wipro’s cloud business (Wippirio could leave its Indian heritage competitors in the cold… if it gets this one right).

The Bottom line: It’s more about learning a new culture of service delivery, than simply retaining key clients and talent

Some analysts focused on whether there would be a culture match, and the challenges of client and talent retention, as the main success criteria for these and other SaaS services acquisitions. While these are important points to consider, the real question is whether the acquiring system integrator is willing to change their culture and approach, and learn from the acquired entity. Arguably, this is a harder task, but one that many of the recent acquirers seem to be embracing.

After blowing $17 billion in the Note 7 fiasco, what could Samsung have done next? Well, it could blow more money – and this time on IoT.

On November 14, 2016, Samsung announced the acquisition of HARMAN for $8 billion, taking the Korean giant into the HfS Winner’s Circle of IoT service providers, where HARMAN has performed for the last couple of years.

This acquisition follows the Samsung’s investment of $450 Million in Chinese Electric Car Company BYD, which it announced in July 2016. These acquisitions sparked the idea that Samsung is finally entering the automotive industry to diversify its portfolio from its stagnating consumer electronics division.

However, in our opinion, acquiring HARMAN is not all about a foray in the automotive industry for Samsung – the rationale goes beyond automotive and extends to the IoT market, which is an opportunity worth hundreds of billions of dollars. The acquisition gives Samsung complete end-to-end capability in the IoT value chain, as we show here:

HARMAN has four business divisions that cater to different part of the IoT value chain:

Connected Car: Navigation, Multimedia, Connectivity, Telematics, Safety and Security Solutions

Lifestyle Audio: Premium Branded Audio products for use at home, in the car and on the go

Professional Solutions: Audio, Lighting, Video Switching and Enterprise Automation for Entertainment and Enterprises

Connected Services: Cloud, Mobility and Analytics Software Solutions along with OTA update technologies for Automotive, Mobile, and Enterprises

Samsung Electronics has three business divisions that cater to different part of the IoT value chain:

Consumer Electronics: Digital TVs, monitors, printers, air conditioners and refrigerators

IT & Mobile Communications: Mobile phones, communication system, and computers

Device Solution: Memory and system LSI in the semiconductor business and LCD and OLED panels in the display business

The combination of Samsung and HARMAN will be a formidable force in IoT. We rated HARMAN in our “Winner’s Circle” in our IoT Blueprint.

In IoT, HARMAN and Samsung will have a very strong position in the connected car or automotive IoT segment. In our IoT study, we found out that connected car is the third largest segment after industrial IoT and smart cities. The HARMAN’s hardware capability also gives Samsung chance to play in the hardware IoT space.

Samsung has been investing in IoT from some time. In 2014, it acquired SmartThings, provider of the smart home platform. In June 2016, Samsung acquired Joyent, a leading cloud provider that can help Samsung connect the users of its devices to the cloud and IoT platform. Samsung has developed ARTIK IoT platform solutions. The HARMAN acquisition augments its IoT capabilities further with the connected car expertise and full IoT services portfolio. The combined HARMAN and Samsung offerings will get a strong foothold in both consumer electronics and connected car IoT market, developing an end-to-end solution for design, data, and devices.

IoT expertise has one additional benefit. It can help Samsung to differentiate its core consumer electronics products. HARMAN has already differentiated itself in the commoditized infotainment business with innovative connected car solutions.

Bottom Line

HARMAN brings real differentiation to Samsung and open the firm up to a huge future opportunity of it gets this right.

HARMAN is a strategic fit for Samsung for IoT and the combined HARMAN and Samsung will have strong IoT capabilities and credentials. Will Samsung blow this again or will HARMAN be the man for Samsung. Keep watching our IoT coverage.

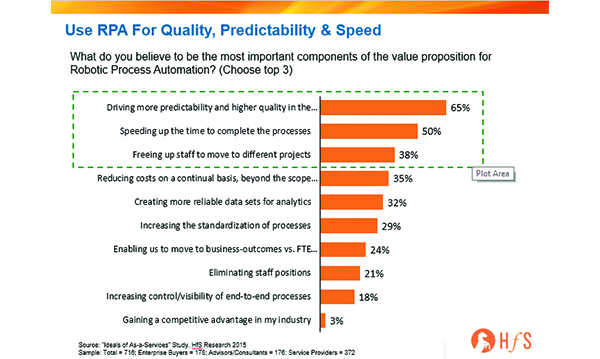

Are you using robotic process automation (RPA) as a way to drive better outcomes for your healthcare organization?

In our research, we are hearing that companies using RPA find the greatest value from it in the quality, predictability, and speed that results from the use of the software to automate rules-driven business processes (there’s your definition of RPA, by the way). And we’d like to hear more examples –stories to share –of how it is being integrated into healthcare operations to impact health, medical and financial outcomes.

Notice in Exhibit 1, that 65% of the respondents in our cross-industry survey say the most value they get from RPA is in driving more predictability and quality in the processes, and half add that speed is of value, while rounding out the top three is freeing up staff to move to other projects. Healthcare respondents mirrored this top three, adding that number four is “creating more reliable datasets for analytics.”

Exhibit 1:

I’d venture to guess that the value of more reliable data sets will increase exponentially as value-based care and reimbursements take center stage in the industry. Predictable, accurate data will be increasingly important in, for example, segmenting patient populations, identifying appropriate and timely care interventions, and capturing and reporting appropriate feedback and insight for reimbursement. Reporting results for reimbursement are absolutely dependent on accurate and timely data.

Where to use RPA in healthcare operations

We heard from one enterprising organization that “every activity, every process is an opportunity for RPA.” Most of the examples we see are in claims processing and coding changes, followed by provider data management where there are many steps that require checking and/or moving data from multiple systems. EXL will share examples of the applicability in care management, for example, on an upcoming webinar, Robotics: A Call To Action In Health Care Management.

But while a number of tasks, activities, and even processes are automated, it is still too often in isolation from a broader process, which can really make an impact. What we have yet to see is dramatic change and impact on the healthcare consumer experience through the use and integration of RPA into a business operation. We’d like to see a significant change to the experience of a healthcare consumer in their patient visit to payment processed, for example, involving RPA, analytics, and customer service.

Think big, and start small—and find your champions. Start where there is the greatest interest in the benefit from the use of it, and the willingness to experiment. It can be anywhere in the operation, really. The key is to identify people who have a passion for using RPA; and in them, you will also find the people who will help drive interest, momentum, business rationale, and results. Results should be about business outcomes, such as reduced fraud or waste, increased medical adherence, reduced readmissions, or better member or patient satisfaction.

In order to get people excited about the prospect of these potential results, it’s important to develop a story around RPA for your internal stakeholders. At a recent HfS Summit discussion with operations leaders, Lee Coulter, Senior Vice President at Ascension and Chief Executive of the Shared Services Subsidiary said that what worked for them was to build a 10 second message, a 30 second speech, and a three-minute story that should include a demo or video clip to “show” how it works. Focus on the impact and results that RPA can drive—the accuracy, speed, and predictability, for example.

Partnering for results

Service provider partners can play a strategic role in identifying opportunities to better leverage RPA. While they are at different stages of maturity, they have been developing capabilities and tools over the past few years on the processes they manage. The use of automation is becoming increasingly sophisticated, especially when you as a service buyer partner with an operations service provider to use RPA in a shared strategy. You’ll find a snapshot of how service providers and service buyers are incorporating automation into their operating models and infrastructures in my recently published POV, Getting the Ball Rolling with RPA in Healthcare Operations.

What’s your greatest challenge, success story, or tip to share?

Just with any change, it takes learning and collaboration to create something meaningful. We look forward to your questions, comments, examples, and stories over the coming months as we figure out how as an industry, healthcare can better leverage RPA to drive better health, medical, and administrative outcomes over time.

Everyone loves to hate grading reports (including the analysts who write them!) If the evaluation criteria are too numerical, some people think the report lacks any strategic analysis. If the criteria favor analyst judgment over hard facts, some people think the report is biased based on the analyst’s emotions or other factors.

And unfortunately far too many people care only about the one evaluation graphic — missing much of the depth and nuance about the market in the report itself needed to really put the graphic in perspective. In fact, the graphic isn’t about who’s good or bad at something, but about finding the best fit for a buyer’s needs and preferences.

My job is to give you my insights about a space but also to give enough context so you can make informed choices with that analysis. And that could include coming to the conclusion that you disagree with a result or a starting assumption.

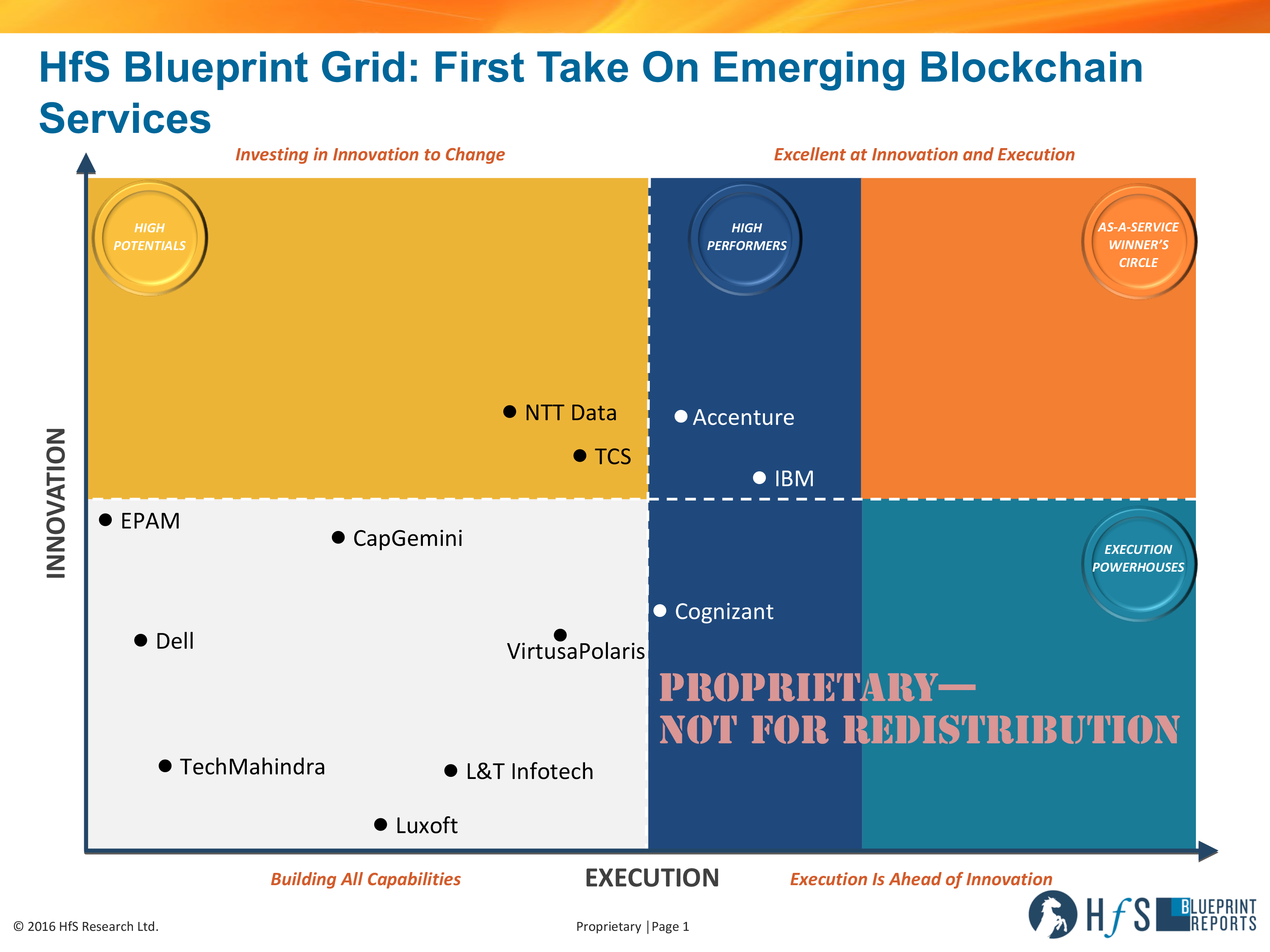

With that in mind, I want to be more transparent about some of the disagreements with the recent blockchain primer I wrote. I gave the service providers evaluated in the report the opportunity to tell me their thoughts.

Below are the comments from the ones who replied. (I choose to believe the non-responses from other providers as agreement that the report was perfect…)

The Providers React

Many providers appreciate HfS Research’s effort to take on this emerging area, noting that the market wants more information. They also mention many improvement ideas. Here are the questions I asked, the answers I received, and any final comments I have on the question.

What do you think the report missed/didn’t cover sufficiently?

Generally, the providers don’t have too many issues with what was covered but offer some ideas of places the report could have drilled deeper, including:

The report could have included more specific offerings and capabilities, like the availability of a provider’s internal and external training on blockchain as well as the availability of a consultative framework to support clients in identifying and qualifying use cases to co-creating the client’s product. Other examples of specific offerings include sandboxes and design thinking sessions.

While the report focused on BFSI, it could have included a broader perspective on where blockchain technology is heading, and which industries and segments are building the first implementations.

CFR’s Take:We’ll be doing a full blueprint in 2017, where we’ll dig into specific offerings and get more detailed about capabilities. We’re also doing more research on many areas of blockchain, so the feedback on giving a broader perspective of the space makes a lot of sense, too.

What did the report get wrong?

Several providers feel that the report didn’t clearly define execution (the X axis) and innovation (the Y axis.) Some feel that they would have provided different information if the criteria were clearer during the research process and mention the following:

The lack of clarity meant they couldn’t fine-tune their answers to what we were seeking. One provider pointed out that we didn’t specify if our focus on client projects was focused on something like numbers of billable blockchain consultants on projects or if it was people who had been trained on blockchain internally, or capacity available to start new projects.

Related to explaining innovation and execution axes, it would have been helpful to explain each provider’s positioning specifically. For example, what made one player more innovative than another? The mini-profiles didn’t specifically call out the grid positioning.

Is the Blueprint Guide the right way to measure blockchain, given it’s so new? Maybe a different report format to explore a market before doing an evaluation is a better approach.

CFR’s Take: Since this was an early first-pass at assessment and not a full blueprint, we used a starting point set of criteria. Also, we recognize that this report switched from one analyst to another, so each analyst always brings a different perspective. But the broader point is taken to be clearer in how we define criteria.

What would be the next logical place for HfS to explore blockchain further?

There are some common requests here, including:

Cover more industries. Several providers mention healthcare, retail, media, and government as other industries they feel should be covered and where they had good client examples that the BFSI report by definition didn’t demonstrate. They also want us to keep studying blockchain in financial services and not stop with just this one report.

By domain area, IoT and supply chain demonstrate great use cases for blockchain and need further exploration.

CFR’s Take:We’re researching supply chain and IoT in blockchain and agree that they’re great places to explore further. We’re looking at other industries too, but that may take longer depending market developments and other factors.

What Did The Report Miss Or Get Wrong About Your Firm?

Most providers didn’t take us up on the offer to publicly voice their issues with our assessments of their firms, but two did. I edited for space and clarity but otherwise used the exact wording from the providers.

EPAM

At EPAM, we’re working on different use cases with different clients and we realize that we can group use cases by technical requirements towards blockchain. We created two prototypes (platforms) that cover over a dozen use cases from multiple industries. After review, we realized that this was not very clear in our initial presentation.

More generally, EPAM believes that when it comes to implementing software solutions there are multiple components/layers in the game: Front End, Integration layer, Backend (business logic + storage). Blockchain is a variation of a storage and limited business logic with some features to improve collaboration between parties. There are a number of different Blockchain frameworks available on the market. Most of the core crypto functionality will be addressed by framework developers so there is no urgent need for service providers to have an army of cryptographers (this is good if they have several).

Service providers need to have Architects, Business Analysts, Testers, and Infrastructure Engineers to be able to integrate/use Blockchain into projects. Their readiness should be measured by the core knowledge they have, ability to scale this knowledge, availability of consultative framework, projects completed (PoC, Production), infrastructure readiness, and client feedback.

IBM

IBM thinks HfS may have underestimated IBM’s innovation in blockchain and offered the following further details. (CFR NOTE: IBM also referenced several documents on blockchain that are available on the company’s website for anyone who wants to get into the details behind the statements below.)

IBM thought leadership. IBM, with the support of the Economist, recently surveyed 200 financial institutions in 16 countries on their experience and expectations with blockchains. This study includes findings like:

Fifteen percent of banks and 14% of financial market institutions surveyed (the early adopters) intend to implement full-scale, commercial blockchain solutions in 2017, and roughly 65% expect to have blockchain solutions in production in the next three years.

Banks identified three business areas with the highest benefits (reference data, retail payments and consumer lending) and three areas where blockchain-based business models will have the most impact (trade finance, corporate lending and reference data).

Financial markets institutions are investing most in five areas: identity and KYC, clearing and settlements, collateral management, reference data and corporate actions.

IBM client innovation leadership with the most centers around the world to help clients get started on their first blockchain project, with IBM Bluemix Garage for Blockchain centers in New York, London, Singapore, and Tokyo. IBM can also dynamically open a “popup” center when and where needed.

IBM industry innovation leadership, as a founder and leading contributor to the Hyperledger Project.

IBM offering innovation leadership with IBM Blockchain, based on the Hyperledger Fabric, and available on IBM Bluemix, which enables developers to easily and quickly develop applications while testing security, availability, and performance of a permissioned blockchain network. IBM Bluemix also allows the IBM Blockchain service to be integrated with other Bluemix services such as IoT, Mobile, Analytics and Watson.

Read through this and then don’t forget to add your own thoughts in the comments. Let’s get a dialogue going about blockchain services.

Fed up with the same old “digital transformation trends” about to turn our world upside down… based purely on those crusty old Uber and AirBnb examples? Getting jaded by the tired old commentary about 20-year-old automation technology suddenly replacing labor… without any practical advice how to manage it all?

And that annoying old yarn about IoT turning the whole world into some massive interconnected computer without aligning it to real business solutions, beyond making your coffee maker more intelligent? Oh… and the hype about Blockchain disrupting the whole world of money and commerce, without any sort of sensible roadmap on how the technology is evolving, and how enterprise-ready this stuff is (or ever will) become.

Are you just simply comatosed by analysts talking in riddles about generic, bland mush you’ve heard a zillion times already?

The 2017 HfS Research Agenda: “Making it Real”

Well, people, your agony is over as the analyst team at HfS is charged with “making it real”… where we’re talking with hundreds of enterprises about how they are addressing all these changes to their world. Technology is moving at warp speed and people, simply, are not. Our 2017 plan is to address this gap between innovation and reality and help our clients really feel this stuff… really kick those tyres to sample how it can be done and how it shouldn’t be done.

We won’t be hyping up automation and digital technology as the critical ‘disruptors’ of business operations – because they are already are past being disruptive – they are already here. Intelligent automation and digital technologies have become the fabric of operations for modern enterprises, immersed in new generation services and platforms. Instead, we are already talking about OneOffice, where integrated business operations have the digital prowess to enable the enterprise to meet customer demands – as and when those demands occur.

Our 2017 Blueprint Reports address all aspects of achieving the OneOffice endgame:

Why is the 2017 HfS Research Agenda Unique?

Since the introduction of the HfS Blueprint in 2013, HfS has published 44 of these highly influential reference guides (see link) for enterprise buyers—to assist in selecting the best service provider for their needs. In that time, HfS has expanded from Blueprints covering core BPO markets such as F&A, Contact Centers, Procurement and Healthcare Payer to a broad range of markets, including IT and Digital Services, IoT, SaaS Implementation, Security and Engineering Services. In 2016, HfS introduced our first ever Blueprints on Design Thinking, Energy Operations, Block Chain, Pharma BPO, ServiceNow services, SuccessFactors services and Mortgage-as-a-Service.

For 2017, HfS is focused on researching the experiences, dynamics, intentions, challenges and opportunities of thousands of enterprises in their quest to align their operations with the rapidly changing needs of their clients. This will include interviewing 300 of the Global 2000 enterprises and several thousand quantitative interviews on a rolling basis through the year with the HfS global community.

Our Blueprint Reports focus on all key aspects of IT services and strategy, business operations and BPO, cognitive automation and the core industry-specific dynamics, namely banking, insurance, energy, utilities, manufacturing, healthcare, life sciences, travel and retail industries. HfS isn’t only focusing on the service provider performances within each industry. We are also helping clients take an “outside-in” approach to reaching a OneOfficeTM endgame, with a second annual Blueprint report on Design Thinking capabilities and a unique analysis of the deployment and enablement of cognitive virtual agents in the workplace.

This is an ambitious research agenda but something that we believe will provide real, unique, and substantial value for the industry in our effort to help enable more collaborative engagements for delivering business outcomes.

HfS subscribers can download their copy of the 2017 HfS Blueprint Agenda here.

If you have any questions on the HfS Blueprint Methodology or our 2017 Research Agenda, please reach out via email to [email protected].

For as long as the IT services world has existed, we’ve had to balance cost, quality, and speed of delivery to make it financially viable. The old adage being we offer 3 kinds of services good, cheap and fast, but you can only pick 2:

Fast & good won’t be cheap.

Good & cheap won’t be fast.

Cheap & fast won’t be good.

Will the cloud and As-a-Service delivery mean that the post-digital world will be free of this constraint?

Digital is the new normal, not the shiny new thing

Before we look at this question, it’s probably worth explaining what we mean by “post-digital.” When we say post-digital, we do expect eyes to roll and people to shout that they are still very much in digital transformation mode. When we talk about post-digital, we are talking about digital as a separate undertaking from business as usual. One of the key findings of our recent survey work and the driving force behind our OneOffice paradigm is that digital technologies are now well established and are already providing the catalyst to drive ambitious organizations to embed them into their business operations. This is especially the case in customer-centric industries where business strategy is aligned to customer requirements with the digital connection to the customer as the feedback loop. In the post-digital world, digital is no longer “disruptive,” it is an established concept, it is the norm, and digital strategy is a major component of overall business strategy. At HfS, we believe we are rapidly getting to that point. It doesn’t mean there won’t be legacy processes and challenges, but the using the term digital will be unnecessary.

So back to the question of balancing the cost and quality of services. HfS has looked at the thorny topic of cost versus quality a number of times, particularly in relation to IT infrastructure services. We published our view on the type of IT required for the As-a-Service Economy earlier this year – “Can Do” IT” Underpins The As-a-Service Economy, where we talked about the importance of attitude, when you can’t have all three of the good, cheap, fast Holy Grail together.

IT professionals must become problem solvers in the post-digital world

The post-digital IT world needs to break out from this constraint. As automation and standardization are applied to a service, the cost should plummet, and the quality of the underlying service should improve – and until cognitive computing starts to function effectively, you really won’t get a highly personalized service. But you will get a good, cheap and fast one. You just won’t get a butler bringing it to you on a golden pillow.

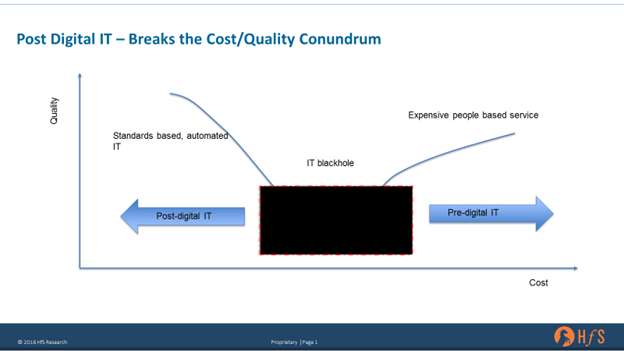

The diagram below visualizes the relationship we see between cost and quality in the traditional IT and post digital worlds.

The chart is conceptual, showing how not only the costs but also the quality of a people-based process should improve with standardization and automation. The costs get driven down as the service improves – fewer problems, more stable and less need for expensive people. The right side of the graph although driven somewhat by good process relies on better and more staff to solve the IT problem without addressing the complexity of the underlying architecture. Essentially, quality should be more or less proportional to the money spent in the old world. With platform based IT the relationship to cost is more complicated – the quality gets better as the service is more standardized and more automated – so the cost should decrease as well. Additional spending in the post-digital world should get you more functionality, not higher quality.

By the way, the chart isn’t supposed to be taken literally, as the real world costs and quality equation is a lot more complicated than this linear chart. There are lots of companies that are paying an awful lot of money for very poor IT in the traditional model – so the relationship isn’t always like this. This is also a point worth making about more process driven automated services – the quality and outcomes are much more predictable and are likely to better fit this model – at least in this idealized situation.

The Bottom Line: The more standardized IT becomes, the more the onus moves to IT staff aligning IT to the business as opposed to keeping the IT lights on

This won’t necessarily make all IT cheaper, but areas which can be standardized and automated will become platforms for expensive staff to create value for organizations rather than spending their time fighting fires and remedial responses to structural issues. This model for IT frees up cost to spend on more functionality and creative solutions for clients.

But baseline IT and IT services – the keep the lights on services – should be fast, cheap and good, all at the same time. Just don’t expect them to be served on a golden pillow. This is where the real challenge for IT starts, as the IT department needs to become one of the main brokers of capability for the organization – focusing its effort on creating value for the business not ensuring SLAs are met.

Since I penned this blog, Senator Chuck Schumer has been made Senate Minority Leader. Schumer has been the biggest and most active opponent of offshore outsourcing, in the US government, for the last several years – we even wrote about his failed H1B bill back in 2010 after his infamous branding of Infosys as a “chop shop”. Net-net – with Trump’s aggressive stance on protecting US jobs, massively raising the H1B minimum wage, combined with the determination of Schumer leading the Democratic Party faction, this does not bode well for the future of the offshore business for at least the next four years.

President Trump is the death-knell for traditional offshore outsourcing… as we know it

The traditional Indian-dominated offshore IT services market was already in the throes of desperation to find a new path for itself. Much of the global 2000 has already been pulling back on the traditional “mega deal”, amidst intense competition between a surplus of IT services providers and an increasingly desire to parse out smaller contracts to multiple suppliers.

The election of Mr Trump to the Oval pretty much just hammered in the final nail in the coffin for the traditional IT outsourcing market as we know it. The Republicans control the House, the Senate and Trump has a huge mandate to impose his will, not dissimilar from Obama and his healthcare reforms. Change is going to happen and it will likely have a very significant impact on global IT and BPO service delivery.

Why is this bad news for offshore services industry?

Temporary IT workers will likely be massively hit. Trump’s campaign has already outwardly promoted raising the H1B minimum salary to $100,000 per year (from $60K). This makes managing complex IT projects a lot more expensive and negate much of the cost advantage for complex engagement requiring “landed” IT staff. For the IT community of several hundred thousand H1Bs, L1s and B1 holders currently residing in the US, many of them will come under scrutiny if Trump holds true to his number one campaign promise – curbing immigration and protecting American jobs. So this doesn’t just spell bad news for the competitive of new IT services deals, it also threatens the viability of existing long-term engagements.

Enterprises will increasingly look to cloud-based solutions. With the cost of maintaining legacy ERP systems likely to spiral, many enterprises will be forced to write off legacy sooner than they may have wished and invest in cloud-based enterprise solutions that require less offshore labor components. Much of the Indian IT services industry, for example, grew up on supporting and maintaining now-legacy IT environments, such as on-premise SAP systems. While many long-term engagements will have already be well past the “labor arbitrage stage” and hard for the Trump administration to police, all US businesses engaging with large numbers of offshore services will become under increasing scrutiny. If there was ever a time to make investments in standardized IT solutions that do not have a heavy offshore dependence, this is it.

Automation is now the new labor arbitrage – and Donald just made it happen. Forget Brexit, Trump is now the new true friend of the fledgling automation industry (and he probably doesn’t even realize it). One of his last speeches was centered on his berating of IBM for offshoring a bunch of jobs from Minneapolis. Offshoring is often a prerequisite to automation… just look at the manufacturing industry where the work is initially moved to overseas factories, before being automated within those factories (or brought back on shore to factories employing a much smaller workforce). Just look at many car plants today which may have employed thousands of workers just 20 years ago, which now only need to employ barely a hundred. IT is no different and the tools are now in place to accelerate automation of IT and business processes faster than most people realize. With the use of IT labor now under so much more scrutiny, the service providers can no longer ignore the fact they need to pivot their delivery models away from labor scale even faster than they had feared. As we analyzed earlier this year, 9% of outsourcing jobs are likely to be displaced by automation over the next 5 years, but that number could be reached in two or three in this new climate.

What can the offshore industry do to survive this?

Invest in US companies employing skilled US IT and consulting staff. Wipro must be tickled pink it acquired US cloud services firm Appirio the other week. The best way to protect – and upskill – Indian based IT workers is by making investments up the value chain to front end new generation IT projects. Wipro can support many new engagements from this investment, where the client facing staff are all US natives, without the scrutiny of the offshore police. Other Indian-heritage IT services majors need to follow suit with US investments, especially in consulting domains. Consultancies like Bain and AT Kearney – while very expensive – could be very attractive acquisition targets for the likes of Infosys, TCS, Cognizant et al. In addition, cloud services niche providers, such as Onesource Virtual, Collaborative Solutions and Sierra-Cedar are possible targets to diversify and de-risk the traditional offshore model.

Invest in intelligent automation capability and embrace start-ups. Enough of the rhetoric… the leading offshore-centric service providers have to go down this path or face extinction in the future. President Trump may be able to make deployment of offshore workers unattractive, but he will really struggle to prevent the automation of processes and technology. The successful IT engagements of the future with traditional enterprises beset with legacy systems are already being increasingly dominated by the need for greater automation capability. That is bread and butter. The emerging wave is being able to make automation more intelligent with smarter analytics algorithms and cognitive technology. This means major investments need to be made in internal training to develop these skills and capabilities, in addition to smart partnerships with tech firms and startups. The huge bright spot here for India – and other developing nations like China and Eastern European countries – is the emergence of the start-up tech culture. Many investors are already fed up with the insane cost of priming start-ups in Silicon Valley… and are more than keen to look overseas for more fruitful, lower risk tech innovation initiatives.

The Bottom-line: This is the new reality for outsourcing and it’s time to pivot

The FTE model dies with the Donald – the offshore outsourcing industry must look to develop new generation engagements that do not involved labor-dominant pricing. The surviving service providers will start providing services and not “people”. Love or hate the election result, this happened. The one bright spot, in my view, is that these changes were happening in any case, and Trump’s protectionist policies are merely going to accelerate reality. The key now is to recognize what is going to happen and get ahead of it… get ready to pivot. This is real disruption hitting the IT services industry and it’s never going to be the same again.

Personally, I am desperately hoping Mr Trump embraces an amazing opportunity to unite the country – this will either be his defining moment, or a sad mess. Whatever we think of the man, what an amazing achievement. He was just relentless!

Procurement BPO has seen a more rapid move to “As-a-Service” — agile and on-demand — than other horizontal offerings. At the center of this movement is the maturity of procurement platforms and networks such as Ariba, Coupa, and GEP, the high degree of automation due to the transactional nature of large parts of the outsourced work, and increasingly strategic use of talent with subject matter expertise. These elements have led to more productive and “intelligent” operations. And at the same time…procurement outsourcing has become cheaper.

The increasingly common use of technology platforms, as well as maturity and confidence in service delivery, has driven down the contract value of procurement BPO deals. In the early days of procurement outsourcing labor-based deals often exceeded $100 million, this number dropped steadily to $50-60 million (five years ago) and currently sits between $25-30 million over five years. Growth dropped in five years to single digits from 12-15%.

Service providers have needed to develop and invest in a strong vision for procurement to drive change on themselves, or risk getting stuck in labor arbitrage. Bringing together an understanding of clients and technology plays a role of paramount importance in continuing to deliver on rising expectations.

A recent HfS Study on Intelligent Operations found the most important driver outsourcing is to drive up productivity. One in six respondents at the SVP level or higher, sees replacing their current (legacy) provider with one that is driven by As-a-Service (they’re more flexible, employ better use of technology and talent) as the way to get to this Intelligent Operations end-state. In this service engagement users in the enterprise get a better user experience—potentially resulting in more compliance, better stakeholder relationships, and stronger business alignment. We are currently exploring these stories and examples in our current research to be published later this month in the HfS Research Blueprint on Procurement Operations.

Moving to As-a-Service will lead to new opportunities and profitability for buyers and providers

Service providers are focusing on how to increase the value of their offerings to service buyers, and sustain their position in the market by investing in strategic sourcing and category management, areas that require higher skilled talent and are less suitable for Robotic Process Automation…and with potential for cognitive solutions. One service buyer we spoke with during our Procurement As-a-Service Blueprint research mentioned the big value she experiences from her service provider is a constant dialogue bringing new ideas about the future of procurement and challenging the current mindset and procurement operations model, focusing on more alignment with business stakeholders. In this particular engagement value add in service delivery has shifted from an execution focus to a strategy driven partnership approach.

Thus, procurement is a valuable area for many service providers and buyers. Buyers report more flexibility and scalability in their operations and experience more innovative input from their As-a-Service provider. And, some providers report achieving double-digit growth in the practice at the moment due to more technology in delivery—nonlinear growth. It’s a change we anticipate seeing more of in the outsourcing services market.

What to Watch

With the impact of the As-a-Service journey firmly visible in the industry, we stay focused on some key questions for the procurement services:

Has the downward spiral in procurement BPO contract value reached the bottom? How are service provider – service buyer expectations and relationships changing? Will we see service providers create new growth with Procurement As-a-Service delivery and commercial models? And will buyers get the support they need from As-a-Service providers in building Intelligent Operations? Stay tuned for more.

Thank the lord the worst election in living memory is only hours away from being done – whether a legacy politician or a dinosaur businessman wins, three outcomes are clear:

You need a couple of billion dollars in the bank before you can even contemplate a run (so much for “democracy”);

Neither candidate has any innovative policies to find a way forward for the country;

The system is “rigged” everywhere, but unrigging it requires a very difference approach.

So we can quickly avoid the first two issues – not much we can do about those right now, barring revolutions and assassinations. However, the third issue is something that we can associate within our very own industry of business operations.

The “system” is all about maximizing margins without too much disruption

I recall working an outsourcing deal, about 5 years’ back, and I was informed by the client “all roles we are keeping are to be created in India, unless there is a clear business case to keep them onshore”. I was recently consulted to talk to the same client about the “next phase” of their “value journey”, which was simply “all processes are to be automated, unless there is a clear business case to have a person involved”.

Great – so we’ve moved from shifting work overseas simply to eliminating it altogether. That is the “system”, where only money talks anymore – the same system that presented this poor US electorate with two awful candidates who have only been focused on outspending each other on negative commercials, rather than proposing anything sensible for the country to create jobs and drive new growth and innovation. Is this really the best “democracy” could come up with, in the richest country in the world posing as the “land of the free”.

It’s time for a big reset

Most people have got lazier in the last 5+ years. Virtual working, digital burnout, Millennials with a warped idea of what work actually is, new forms of adult ADD… whatever… something negative happened in the workplace and it’s getting harder and harder to find people with that “go the extra mile” attitude these days. So many people have a sense of entitlement we’ve never seen before. It scares the sh*t out of me. Forget “new normal”… we need a whole new reality.

We’re going to need a great big reset, driven by government, to get people relevant for this changing workplace. At some future stage, we are going to have another downturn and these issues of worker apathy and irrelevance will magnify exponentially. People will actually have to take shitty jobs again… my god.

The Bottom-line: It’s all about resetting, retraining and reeducating ourselves

Investments at a huge level must be made in training and education, not handouts to people who’ve just lost interest in working anymore and like to complain the system is rigged against them. This would also stimulate a much larger and more flourishing education sector that creates more jobs and innovation. We need less of the angry politicians playing on the increasingly disenfranchised population. We need leaders focused on inspiring people to reinvent themselves, re-educate themselves and find that zest for working again. And not only do we need people who can understand data, digital apps, robotics and artificial intelligence… we need people who can cook great cuisine, compose decent music, write great books, teach our kids, police our cities… we need to unrig this system that has lost itself somewhere between a balance sheet, social media soundbites and bad news coverage.