Everyone is talking about how to get to the right strategy for omnichannel customer communications, yet no one really knows what it means. First of all, let’s just get it out there that omnichannel is one of those terms everyone loves to hate. It’s ubiquitous, it’s vague, and it’s a misnomer– “omni” is impossible and customers don’t think in terms of channels. That said, omnichannel is an aspirational goal pointing many service providers and enterprises in the right direction toward really getting customer experience right. So with that in mind, it has become my mission to dissect the subject, get past the hype, and figure out where the opportunities lie for the services industry.

The keys to creating an omnichannel experience are the following:

Non-creepy Individualization: “We know the name of your cat because we stalk your Facebook updates” (we’ve seen these creepy mistakes backfire bigtime). And please stop talking about customer “intimacy.” Customers don’t want you to be intimate with them, they just want to be acknowledged as individuals (especially those self-centered millennials), and for you to know their buying patterns and preferences. This is part of the Amazonization of the consumer experience that just isn’t going away anytime soon – and striking the right balance is essential.

Simplicity: Making it easy for the customer to do business with you is at the heart of customer satisfaction. More than anything, customers want want to be able to get information, interact, and buy products and services easily, without jumping through hoops. Our “one-click” ordering culture has raised the bar for the way we expect to get things done. Look at reservation systems for example—why should I have to call, sit on hold, and speak to a person when I could simply use an online scheduling system?

Consistency: Whether it’s about product pricing and discounting, visual design or cultural feel, it’s crucial to the omnichannel experience to have consistency across devices, physical experiences and interactions. Making a brand one that customers relate to and develop an affinity with goes a long way toward generating loyalty. Apple for example, has done this well with creating an in-store and online consistent experience as well as developed a culture that people want to be a part of.

Executing on these concepts is no easy task, involving many facets of the organization, and most companies are coming nowhere near these ideals. One of the biggest opportunities, and yet most troubling elements of this omnichannel notion is where contact center fits into the paradigm. The conversations consumers have with businesses are at the heart of creating a differentiated experience, but let’s face it, right now contact centers are not pivoting to be strategic differentiators. Most of us deal with this pain regularly in our personal lives. Just last week I called my bank with a simple question (which could have likely been answered via self-service), was transferred and repeated information 3 times before I even reached the right department. As much promise as there is for a utopian omnichannel world, most are struggling with the basics.

The Bottom-line: work on fixing broken customer service (keeping the goal of omnichannel in mind)

Contact center service providers are acutely aware of these opportunities and desperately trying to carve out an omnichannel story and capabilities. As we noted in our recent Contact Center Operations Blueprint, while many of the pilots and messages are spot on, client adoption is low and stories of omnichannel success are few and far between. Many buyers are just grappling with implementing digital channels, and a total redesign of customer experience is far too daunting. Service providers need to help their clients (with the goals of personalization, consistency and simplicity in mind), to start making some real changes in bite sized pieces to improve customer experience. Instead of trying to “delight and surprise” the customer at every turn, just taking some basic steps to make customers’ lives easier could go a long way. Omnichannel is the future of customer experience (or whatever the next buzzword that encapsulates a seamless customer journey may be), and one of the biggest steps toward that is a clear and focused contact center strategy.

This is my all new spot on Horses for Sources. The home of razor-sharp analysis and the place where hypes are crushed and real trends are born. Phil has set the bar incredibly high over the past decade. Inspired by the best analyst blogger around, my aim is to be as edgy as you are used to on Horses for Sources.

What you can expect on Berzerk with Derk I lead the energy, utilities and natural resources practice at HfS. I’m passionate about these industries and the huge shifts they need to make to stay relevant to this world. These are the largest and most fundamental industries in the world. The looming departure from fossil fuels mean the world’s energy systems, which have historically been slow to change, are in an unprecedented period of rapid transformation.

Renewable energy is the next normal – but the world has not woken up to this new reality yet This blog will help you stay abreast of all these fast-moving trends plus cut through all the hype that is out there. We’ll be covering the energy markets and the ongoing energy transition; away from fossil fuels and toward renewables. And specifically zoom in on the transformation of energy companies and service providers. The As-a-Service Economy has arrived in the services world and holds the potential to play a critical role in the energy transition.

The holy triangle of services; People, Process and Technology In my focus areas, besides aforementioned Energy, these are Supply Chain Management and Procurement, we see a fast convergence of people, process and technology, forever changing market demand and the offerings of service providers. Talent is a major topic for enterprises and service providers; there is a deficit of skills needed in the As-a-Service Economy. We need more people who can be strategic, experiment, play with business and revenue models, design new organizational structures and cultures, implement and pivot rapidly. People who have a keen eye for societal, political and technological developments and its ensuing opportunities and threats. There is an enormous opportunity for technology and business service providers to become part of the solution. This requires investment from both sides, real partnerships and the application of leading-edge technologies: intelligent automation, IoT ecosystems, actionable data and analytics are essential ingredients of digital transformations designed to push energy providers forward on the energy transition journey.

Change = new stuff = hype The common theme in much of our work at HfS is change. The old, legacy way of doing things is not cutting it anymore. Labor arbitrage, lift and shift and the traditional models of outsourcing are well past their prime and the services industry is transitioning into this new phase of As-a-Service. Before new things come to fruition, there is often a lot of hype and fluff surrounding them, clouding the view of what is real and what is not (yet). This is where HfS analysts come in… This blog won’t shy away to expose bs, calling out cookie cutter hype and identifying what is real.

All nice and well Mr Erbé, but why should I care? My goal is to tell you something you may not know with every post. I have been in the trenches of technology implementations, business transformations and operating model changes. I’ve managed the backlash of failed implementations on the business, designed business and IT functions. So in a lot of situations where theoretic solutions and vendor promises have broken down and the real issues still need to be fixed.

On this blog I will address the real-world issues screaming for real change, exploring what works, what doesn’t work and what needs to be done.

I will be:

– Harsh (sometimes)

– Real (always)

– Candid (the key to being an analyst isn’t it)

Are you of the curious variety, care about the world around you and the vast opportunities there are for business and you as a professional? I will introduce you to the most intelligent, innovative and forward looking folks in energy, supply chain and procurement. And help you navigate the real-hype divide, which solutions are aspirational and which solutions can bring scale, results and impact now.

When I entered the industry in 2008, working for a boutique research firm in Pune, India, the research themes floating around were about “what’s next for BPO, because this recession changes everything.”

We studied the knowledge process outsourcing (KPO) segment (“KPO” sounds so dated now!), which included service areas such as legal services, marketing, publishing and digital media management, e-learning, engineering services and market research and analytics. KPO services were perceived and categorized by the market to be different because they involve a) specialized skillsets, b) judgement based work with complex sub-processes, c) greater degree of partnership between client and service provider beyond process compliance and d) required a greater degree of specialization from the service provider in a horizontal/vertical, making them “higher value services” that came along with premium billing rates.

This definitional distinction that our research revealed between KPO services and “vanilla” BPO is worth unpacking today. Our conversations now are about enterprises operating in an As-a-Service Economy, heading towards Intelligent Operations. We’re actually seeing these traditional KPO markers becoming a core part of BPO and BPaaS service delivery.

Our Blueprint scoring methodology, based on HfS’ 8 ideals of As-a-Service has Collaborative Engagement as a key parameter for success, and we see promising examples of how a partnership-driven approach has helped set up engagements for success by focusing on business context and outcomes.

As for judgment based work and higher value services, this is very much the future of the industry for three reasons:

The robot will be taken out of the human. We will reach a point in the not-too-distant future where we can leverage talent to do meaningful, value-adding work, essentially taking the rules-driven robot out of the FTE. This is already happening in pockets as the services industry makes progress on embedding intelligent automation technologies, including robotic process automation, autonomics and cognitive platforms.

Industry domain knowledge is critical. Every service provider worth its salt lives in a “verticalized” client market, and our research in core operations outsourcing often reveals how buyers hang on to providers because their delivery staff has deep domain knowledge, “know more about our industry than we do” and have the certifications for their talent to prove it.

End to end service platform-based delivery demands deeper skillsets. Thirdly, service providers today (at least the preferred/strategic partners) manage a lot more parts of the services value chain than just backoffice transaction processing/call center operations. With more platform-based delivery of services that have straight-through processing and analytical insights baked-in, buyers are incentivized to carve out more end-to-end service delivery that includes both complex sub-processes and volume-driven processing.

The speed of change in today’s global environment can’t be captured any better than news coming this week of UK’s tentative departure from the EU, and speculations are flying wildly about the implications of this U.S. election year. And so here we are, as an industry, once again, wondering, what happens next, because emerging digital business models and the global environment is changing everything.

The Bottom-line: KPO really became “As-a-Service” – Smart talent and technology delivering value via the on-demand delivery model

HfS defines a future state for the services industry where As-a-Service is native to enterprise operations instead of a set of processes and technologies being retro-fitted in painful increments. Investments are made in outcome-centric services first, followed by talent acquisition to broker these capabilities and align them to the revenue-generating, customer-first activities of the business. In the next few years, as more outsourcing engagements o down this road…leverage actionable and accessible data, common standards, automation, digital tools and apps, powered by cloud delivery, priced As-a-Service, we will need a lot more judgement, and reimagination to navigate through it all. The KPO terminology might not make a resurgence, but its distinction will continue to blur as service providers morph the business they want to be in and the value they deliver to foster genuine, long term partnerships with their clients.

Procurement’s very existence is in trouble. The function must be part of the whole negotiation process, not only to protect the company from making deals that do not benefit the firm but also ensure they are sensible, cordial and well-balanced – and both supplier and buyer realize the outcomes they both want to achieve. Sadly, this is so not the case with so many pivotal business deals today.

The fact of the matter is, for some bizarre reason, most senior executives just don’t care about them, and they seem to show up when the deal is already made and “promises” have been made that are hard to break. All that transpires is both the senior executives from the supplier and the buyer end up frustrated – and feelings of mistrust can really break down what was a blossoming partnership with a very “transactional” experience.

The problem really is two-fold – executives doing the buying probably don’t even think about involving procurement, as they see no value in their contribution – or have no awareness of any potential value. They probably never even thought about involving them. In many cases, they never even intended to include them and procurement only inserted itself when they were asked to make the payment. Which means procurement’s role has been reduced merely to a last minute attempt to sabotage a deal; otherwise, its existence in the company is rendered completely useless, and you might as well phase it out (or replace with some software).

Who’s to blame when procurement comes along to mess everything up? Yourself!

To all executives out there who like to spend company money on things:

Ignoring procurement in the buying process nearly always ends in tears for everyone. I often feel the amount of time, negative energy and lost money tied to the procurement experience is simply not worth the investment of having them in the first place. So stop acting like they don’t exist and start communicating.

This means getting procurement into the loop regarding your intentions, once you know what it is you want to invest company money in. Train your sales people that procurement exists for a reason and that they are not the boogie man from the outset. The reason it often goes wrong at the end of a sales cycle is that procurement people feel they are not participating in the process and need to make last minute changes to the contract (which is usual to try and squeeze the supplier on price, which just pisses everyone off).

When procurement people are feeling ignored, all they will try and do is derail the buying process, as opposed to helping shepherd it through and add some value (or at least a few sensible suggestions) along the way. Procurement needs to feel it has a reason to exist, like any other business function. With HR, we often know it adds no “strategic” value in the hiring process, but at least it will run the background checks, the references, sort out the payroll, etc. At least HR has a role in the company, whereas procurement is in danger of extinction if its contribution is worthless. So while procurement still exists, you must involve it, or it will make everything unravel down the road.

To Procurement Executives:

Be a business relationship manager, not a transactional negotiator. Get off your backsides and serve the people who pay for your salary. Yes, we are a team, but sending these emails such as “No more discount or we need a minimum of 20% margin”, or “We only accept 90 days payment”, do not help at all. You’ve made it clear in the time your profession exists that you are not business people and care nothing for “customer service” or “employee experience”. The fact you feel you are the police of the people that call themselves “sales” is a fairy tale. You should get up and try to understand what your firm is doing, the clients you are serving and the history that exists between your company and your customers. Only looking at making a personal gain is not a solution for anyone but yourself. If you like to have war stories, join the army. Don’t pull this nonsense on the work floor.

Bottom line: Communicating with each other is the first step to getting business done

We all need to live with certain professions within a process. Some we like, some we just have to tolerate. But we can make it nice along the way to work more closely together and stop pretending we do not exist or need each other. If you listen, you will learn, if you keep doing what you always do, you keep getting what you always had. We have enough islands in this world, let us not fight internal battles all the time, but let us communicate and not harm the clients and eventually our business.

It’s easy to make a compelling case that ‘digital’ will ultimately replace what was once ‘IT’ at some point in the future as the former rapidly evolves and the latter become more and more associated with legacy technology and practices. hedging bets on what will happen and when however is a different matter entirely and hugely variable from business to business.

A historical analogy I’ve used frequently is the period when steam power slowly gave way to electrification. Steam enabled the industrial revolution and generations of power creation and transfer expertise. Simplifying, early manufacturing typically had one giant steam engine driving multiple leather belts to various ‘creating’ contraptions.

Along came electrification and boilermakers and belt tensioning experts started to work alongside electric motors and light, but the period when these two power sources co existed was surprisingly long as companies sunsetted their amortization of steam power and invested in electrical.

It wasn’t until the 1930’s that ‘as a service’ from the plug socket and light switch regulated electrical grids were established in north America. Prior to that electrification was very parochial and needs driven for the creation of electric light and to power specific factories.

Just as early use of digital media for marketing is analogous to the creation of neon signs and electric light arrays in cities as soon as their generation was possible, today the focus on ‘digital’ has been skewed towards marketing though social networks and ‘customer conversations’. Electric light displays in places like Times Square NYC were the wonder of the world only 100 years ago, initially hand switched on and off in sequence by staff.

All fascinating history, what has this got to do with our digital ‘as a service’ world? The period when steam power slowly moved to the less visible role of creation of distributed electrical power is analogous to the way enterprise computing has evolved. Cloud and mobile networks have transformed our world on an individual basis but as we all know there’s an awful lot of mainframes and cobol out there.

As HfS’s Phil Fersht recently wrote

When you consider only $15 Billion is being spent on public cloud services (IaaS) this year and $ 1 trillion being spent on services tied to traditional services delivery, there is a huge amount of “legacy” IT and BPO business in play – for another decade and beyond – to enable the enterprise digital experience.

It’s amazing to think that less than 100 years ago people would go by horse drawn carriage to see people turning arrays of lights on and off in Times Square on a Saturday night as ‘advertainment’. The pace of change has sped up enormously just within this century alone: as an example AWS delivered the first storage service (Amazon S3) in the spring of 2006 and compute (Amazon EC2) in the fall of that year.

For the services world the twin speed world we live in of legacy IT and digital evolution has some similarities to the past era of boiler makers and electricians – today most of the work is in keeping the steam boilers ever more efficient in the enterprise world, but everyone knows the increasingly automated grid is evolving fast. Making the decisions of what to focus on with staff and technology – what skill sets are needed and how and where to apply them – is doubly difficult when for decades most of your waking hours have been focused on ‘busy work’ to keep IT systems running. Quote to cash isn’t going to go away but it is certain to evolve and be ever more connected to other parts of the digital continuum most companies now have in focus strategically and aspire to.

Where steam power was rigid, brittle and inflexible despite enormous power generation, eventually ‘ always on’ electrical power provided plug and play secondary, tertiary and on usages (light, power, heat, production lines etc). This is the analogy the services sector are increasingly aware of and where ‘core digital’ is arguably emerging to supersede ‘IT’.

These are absolutely fascinating times, not least because this new world allows an astounding pace of innovation and appetite for the new. Steam power didn’t go away of course – as late as the 1960’s steam locomotives were the way people travelled by rail, and the electricity I am consuming to type this post may well have some steam generated electrons commingled. As the transition and automation of older services yield to newer digital needshere at HfS we will be commenting and informing on where the power and growth centers of the ‘as a service’ world opportunities are.

“When we first outsourced, our service provider had the newest ideas, but now three years later, we have caught up to them and they’re treading water. So what’s next?”

These are quotes from operations executives over the past months of research, when asked about whether or not they (still) consider their service provider “innovative.” Since the term is open to interpretation, for the sake of this blog, let’s view it as an ongoing improvement in the impact of the work being delivered by doing something differently… something over and above the basics of what you would have expected, beyond the letter of the contract.

And, often, these comments are followed by, “it may be… well it likely is, our organization that is holding us back.”

If you really want what’s next… your service provider might actually have the ideas… but is your leadership willing to listen, invest, give them access to your intimate data, and give it a try? Is your organization genuinely culturally ready for innovative change? And is the service provider capable and culturally aligned as well? If not, maybe you aren’t ready for innovation; or, maybe not with your current partners.

Consider three “Power Ups” to change the face and increase the value of outsourcing: Courage, Budget, and Stories

Harken back to the days of Mario brothers in the video games, when Mario and Luigi tapped into “power ups” to help achieve their goal. (Maybe this is not such a leap in time for you!) “Super mushrooms” gave them temporary size and height advantage, ability to take multiple “hits” before dying, and additional lives. The “super mushrooms” of outsourcing—to achieve innovation and increased value through partnership—are good for use by any player—operations executives, delivery staff, service buyer or service provider:

Courage: The “gumption” as a leader to “allow,” and as an employee to “take” a chance, to leave egos at the door, to experiment, to “play,” to quickly acknowledge and shut down what does not seem to be working.

Budget: Realistically, nothing much will happen without a dedicated budget to finance time and materials that support research, dialogue, and prototypes.

Stories: Visuals and stories connect with our emotions, and are memorable. When you really want someone to understand, appreciate, engage, own, and promote a concept, a result, an idea, or a change, then “show and tell.”

If you want innovation—new ideas implemented to drive step changes in results—you need to be willing to do 1-2-3. If not, you are probably keeping yourself in a dangerous continuous improvement cycle—and also likely to get lost in the dust of other companies that are innovating.

I don’t believe there is any digital business or consumer that can be 100 percent secure 100 percent of the time, unless they opt to abandon technology and live in an obsolete analog world. It’s as simple as that.

As we continue the shift from the legacy, analog economy of the last century towards a still emerging 21st century digital economy, new opportunities abound. Brands that couldn’t have existed 20 years ago now dominate our global economy. Facebook and Google are almost totally digital, while others such as Uber, Amazon, and Apple blend the physical and digital to perfection. These are among the most recognizable, but there are countless more that make up a marketplace of brands and consumers that function in a totally different way that we did a decade ago—and the change is unlikely to stop any time in the near future. As rapidly as the human race embraced the digital wave, we’re just barely beginning the transition.

But for all the opportunity, there is tremendous risk. Our human existence has been shaped for millennia by the analog experience. It’s where we learned to live, learn, and trust the world—and the people—around us. It’s also where we learned not to trust.

For modern-world youngsters born in the ‘90s and ‘aughts, the digital world is all they know. My kids and their friends have never known a world without smart, mobile phones and online shopping, or where homework was not assigned online (and the homework dropped into a teacher’s shared Google drive), or where friends—that they’ll never meet face-to-face—are found and relationships built.

But for most others, this has been a period of transition that has brought both significant challenges and even more significant risks (from the challenges of shifting from paper to electronic bills to having your personal data stolen and sold on the open market).

The same is true for businesses. As my children are digital natives, so too are many brands, but far more are struggling to change—to reinvent themselves digitally as quickly as possible and shed old analog roots in favor of digital opportunities. But the most important, and common, issue that we all face is one of trust. It’s difficult to trust the company you can’t see, the bank you never visit, or the online contact you’ve never met. It’s even more difficult to protect, and leverage, your assets now that they’ve shifted from the mattress to the great cloud in the sky.

When we talk about protecting assets, we’re talking about employing cybersecurity to protect our digital assets against the threat-actor who would hack, steal, or destroy all that is ones and zeros. This is the dark side of digital, driven not by the greater good, but by personal, or state, gain—the world of the cyber threat.

In the analog world, we know how to counter, or at least avoid, most threats. We know how to learn to trust a friend, or a brand. Digitally, however, it’s a different story. The markers we used to look for to create bonds of friendship and trust simply don’t have direct analogues in the digital world. The business processes that we used to rely upon are also no longer the same, as technology has given us a powerful tool to rethink not just what we do, but how we do it, and why.

In this blog (In Digital We Trust?), we’ll be exploring a number of themes, primarily from an enterprise, provider, and consumer perspective—themes that share a common focal point: digital trust. As cybersecurity is core to securing our information and our brands, expect a healthy dose of that. But we’ll also be taking a hard look at the way we use digital today, from the technology to the processes that keep our corporate and our personal data both safe and accessible.

Some of the questions we’ll be discussing include:

What is digital trust, why is it so important, and how can enterprises, partners, and providers collaborate to leverage it for greater business success?

What are the “transformational” roles within the enterprise that are key to digital transformation?

How can a holistic approach to security be woven into the overall business process, from product development to marketing to sales and customer support?

How will emerging technologies, such as analytics, automation, and cognitive/AI help us secure our digital assets against ever-evolving cyber threats (both within and external to the enterprise)?

Will nascent technologies, like blockchain, actually become mass-market viable and allow us to build a more transparent, and trusted, transactional infrastructure?

How are mobile and cloud, and the shift away from legacy IT models, forcing enterprises to rethink the architecture of security?

How is customer experience influenced—positively or negatively—by our ability to implement enterprise-wide holistic security?

Who are the key providers, of both technology and services, that are reshaping the digital enterprise, and how are they promoting the ability of enterprises to achieve a state of digital trust?

We won’t shy away from controversy, and we certainly won’t shy away from sharing a strong opinion or two. Where providers and enterprises are doing it right, we’ll give them props. And when they miss the mark, we’ll let you know as well.

To help kick this blog off, here’s a link to our just-released report, The State of Cybersecurity and Digital Trust 2016. In this ground-breaking research, also published today, we discuss the challenges faced by enterprise security professionals and the steps they must take to ensure the integrity, and trustworthiness, of corporate and consumer digital assets. This report digs deep into five critical gaps—involving talent, technology, organizational parity, budget, and management—that are inhibiting digital trust across all industry verticals and geographic regions. Give it a read, and let the conversation begin.

The vote for Brexit wasn’t really about debating the finer points of EU membership – it was a big thumbs down for the establishment from over half the UK voters who feel disenfranchised. This is a reflection of the ever-widening gap between the wealthy and the working classes, the educated and the uneducated, the socially-connected ambitious younger generation and the disconnected older generations, who’ve lost interest in the direction of the modern world that no longer represents their interests.

Moreover, this rebellion against the establishment can be clearly mirrored in many of our enterprises, where similar issues of disenfranchisement are rapidly permeating.

Rote jobs are being eliminated with limited reorientation and progression planning

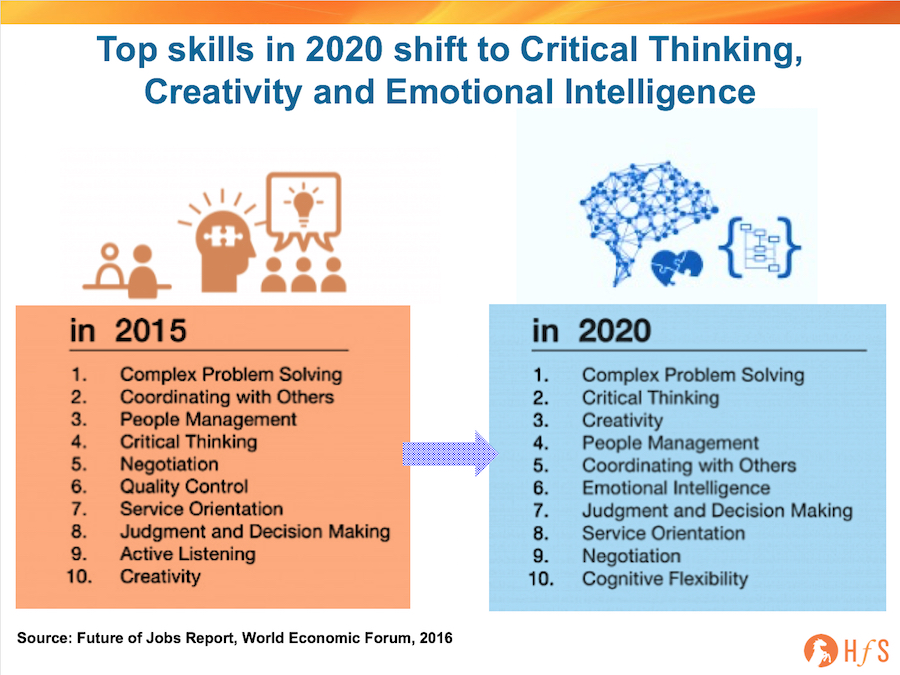

We talk a lot about the new work and career opportunities being created by digital disruption and digital business models, but these require greater problem solving skills, critical thinking and creative capability, if the World Economic Forum’s new jobs report is to be believed:

Click to Enlarge

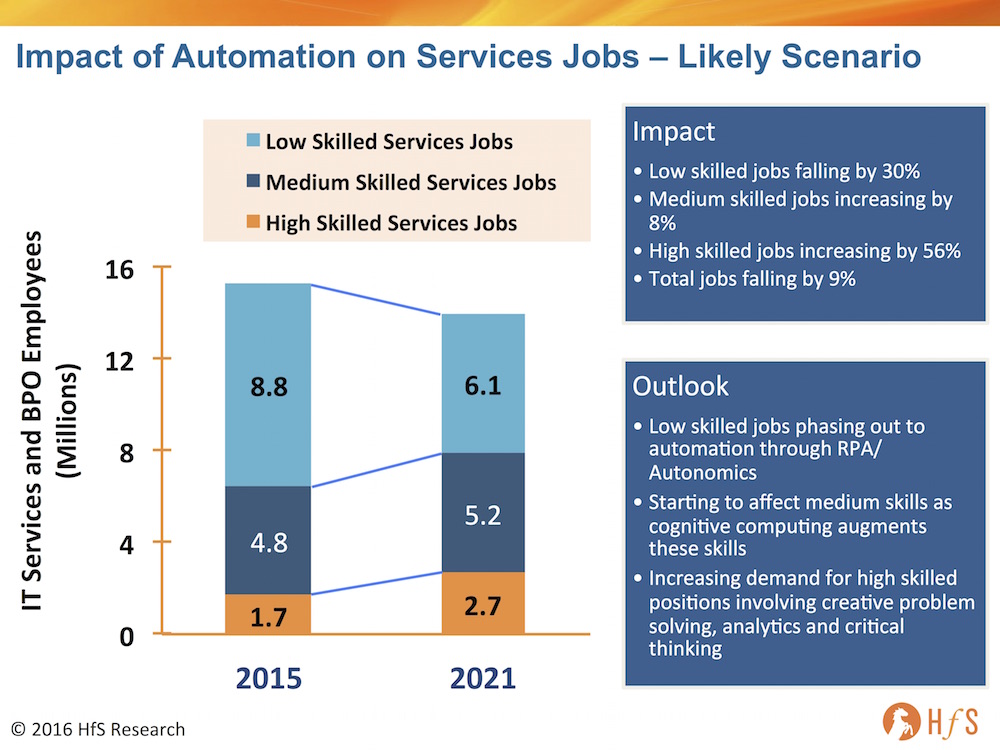

And while we can complacently talk about all the exciting work creation the As-a-Service Economy is bringing, we’ve already precisely pinpointed that 30% of routine, low-value positions are being phased out through automation over the next five years, far outweighing the expected new jobs being created in the medium-high skills areas:

Click to Enlarge

This means we need to ensure our businesses and colleges alike are actively involved in reorienting this 30% to avoid their exit from working society. This is serious stuff which needs to be urgently addressed by our politicians, if they genuinely want to get back in touch with their increasing base of disenfranchised voters.

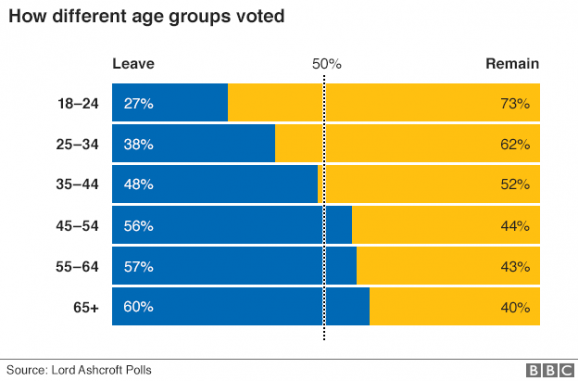

The younger generation, clearly more in tune with opportunities of free labor movement and their career growth, overwhelmingly voted to remain in the EU. In fact, the majority of British voters under the age of 45 want to stay “in”; it’s the 45+ year-old people which see no value of EU membership for themselves, which opted to stick it to the faceless politicians:

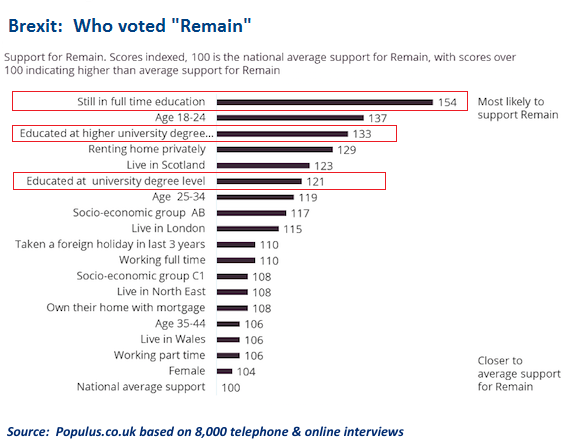

And when we delve even deeper, it’s also highly obvious that the better educated the person, the more they were inclined to vote “remain”:

The Bottom-line: As automation and further outsourcing take a firmer grip on enterprises, we face an almighty challenge – and cost – to reorient staff in low-skilled jobs

We’ve long-countered the whole argument about job elimination and offshoring, with the response that businesses need to be competitive and this is all part of the natural evolution of society and business. However, when 30% of services jobs are likely to be phased out over the next five years, we need to ensure these people can orient themselves into new jobs. Politicians need to forge closer ties with business leaders to ensure this happens, otherwise we’ll have more Brexits and more fascist lunatics creating frightening futures for us.

When you have 52% of your voting public sticking it to the establishment, there is a serious situation emerging that could change the game forever: if we can’t have leadership that can get back in touch with the people doing these rote jobs, we will end up with governments that force even more draconian measures on businesses to protect jobs. And this will likely mean less competitive businesses and less jobs to go around in any case. This is a journey to the bottom if we give in to archaic government measures and an avoidance of investment in work creation through re-education and training.

Taking away EU employees from British firms, and the ability for low-wage EU workers from places like Poland, Ukraine etc to wait on tables and clean hotel rooms, the economy is much worse off. Just as a benchmark, British science is hugely dependent on EU grants and talent to keep it going. It’s the same with university programs and technology start ups benefitting from EU synergies and subsidies alike.

Many governments need to accept the fact that this 30% of future job elimination is caused by woeful education systems over the last few decades that long lost touch with the reality of business and modern day commerce. Serious investments need to be made by governments to fund the reorientation of workers to be relevant for the future workplace. Our businesses need to be funded to retrain staff and retain them, not simply look to reduce headcount wherever possible.

Brexit symbolizes the failure of government to listen to so many of their people who are just angry. They feel neglected at the ever-widening gap between the rich and the poor. There’s a reason Bernie Sanders and Donald Trump (for various reasons) gained so much popularity. Love or hate their policies, many people see them as politicians who can “hear” them. David Cameron may have fought – and lost – the cause to keep Britain in the EU, but the majority of his people felt cut off from the future and made their voices clear.

The painful process now begins for legacy establishment politicians across the globe to wake up to the reality that an increasing majority of their voting bases are fed up with their lack of affinity to the common workers, and the fact that our business leaders have limited (or any) incentives to protect them or reorient them. Otherwise, they will get voted out and we’ll have some alarming social unrest that could well put us all out of business. This is serious stuff, and we can’t afford to keep brushing these issues under the carpet in a democratic society.

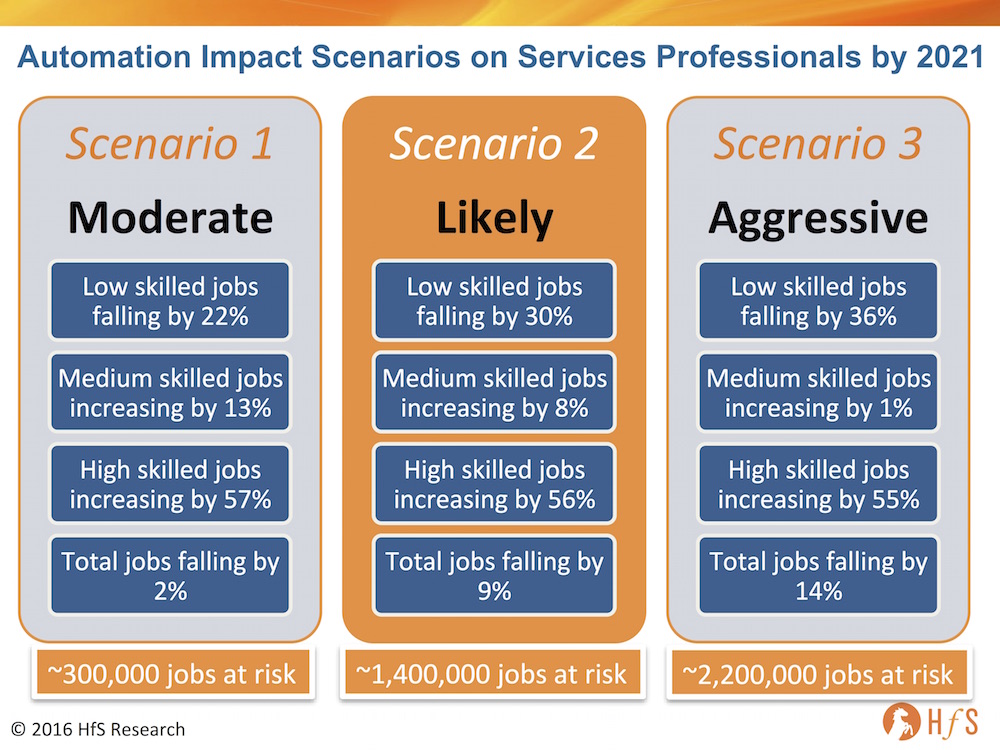

It’s time we dispelled the scaremongering and hype and gave you the true picture of how advances in automation tools and methodologies, such as RPA and autonomics, will impact the global IT services and BPO industry over the next five years.

The current debate on these issues is as polarizing as it is confusing. On the consumer-facing side of technology, we have a fervent and far-reaching debate about the ethics of artificial intelligence and automation, led by executives from the likes of Google and Facebook. On the enterprise side, we frequently see quotes from studies from firms such as McKinsey and Gartner predicting seismic job losses through the impact of disruptive technologies that could have a devastating impact on the global economy and society in the next few years.

Yet, many of the leading stakeholders much closer to the true deployment of emerging enterprise Intelligent Automation tools and platforms—namely the service providers, the ISVs and the sourcing advisors—remain on the sidelines when it comes to discussing the true impact of automation as it’s adopted by many enterprises today.

We’ve been talking, for the best part of two decades, about how to “transform” business and IT processes after the cost benefits of labor arbitrage have been maximized. Well, the simple fact is that much of these arbitrage costs are close to optimization for mature services providers that have well-honed global delivery machines. As enterprise clients demand further cost advantages, and as competitors become increasingly aggressive with their service pricing, the focus shifts toward clients attaining outcomes that are not always directly linked to lower headcount rates.

“Intelligent Automation-as-a-Service” is a genuine lever for enterprises to pull for further productivity gains beyond low-cost offshore labor

Consequently, many enterprises that have chosen to externalize their service delivery can enjoy even more cost effective services, as ambitious service providers further rationalize their delivery organizations by taking advantage of automation to standardize and scale service delivery to their clients. In short, while many enterprises can invest directly in Intelligent Automation into their own processes, they can also simply outsource those processes to service providers, which can embed further productivity gains tied to automation, in addition to labor arbitrage. “Intelligent Automation-as-a-Service” is quickly emerging as a significant productivity option for enterprises as part of their service delivery.

Sadly, greater productivity and effectiveness through “digital labor” comes at a societal cost—jobs that were once required are no longer needed. However, we would point out that the jobs that are being phased out are no longer being recreated in any case, and much of this shrinkage will likely come from natural attrition as some people leave the service industry for more relevant jobs in other industries.

The Impact of Automation on Services Jobs

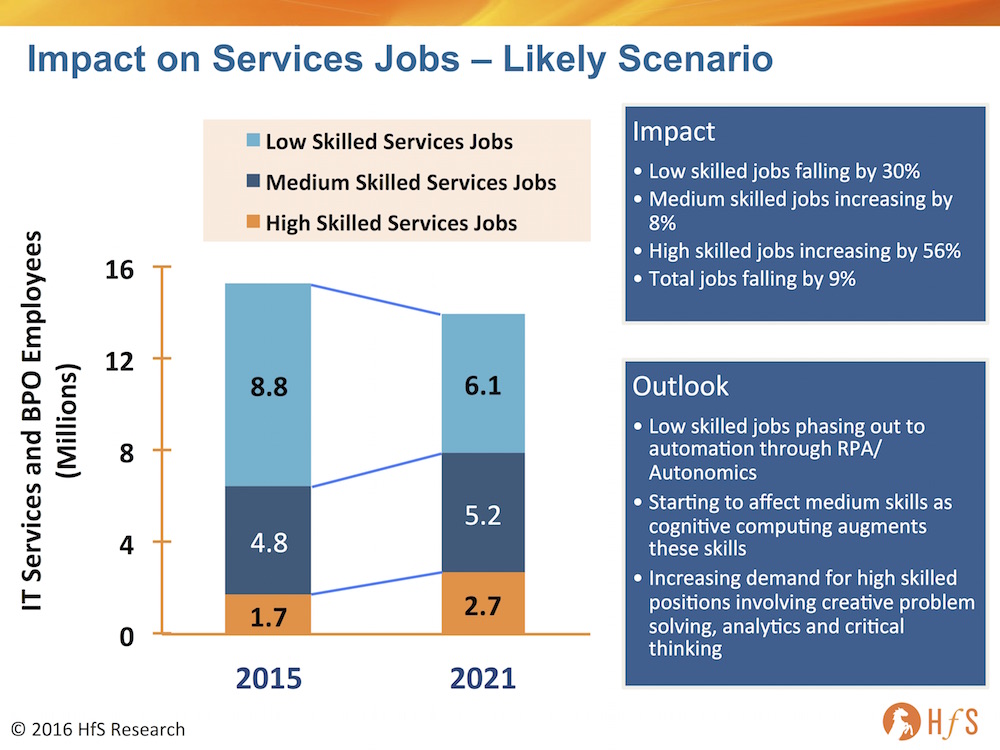

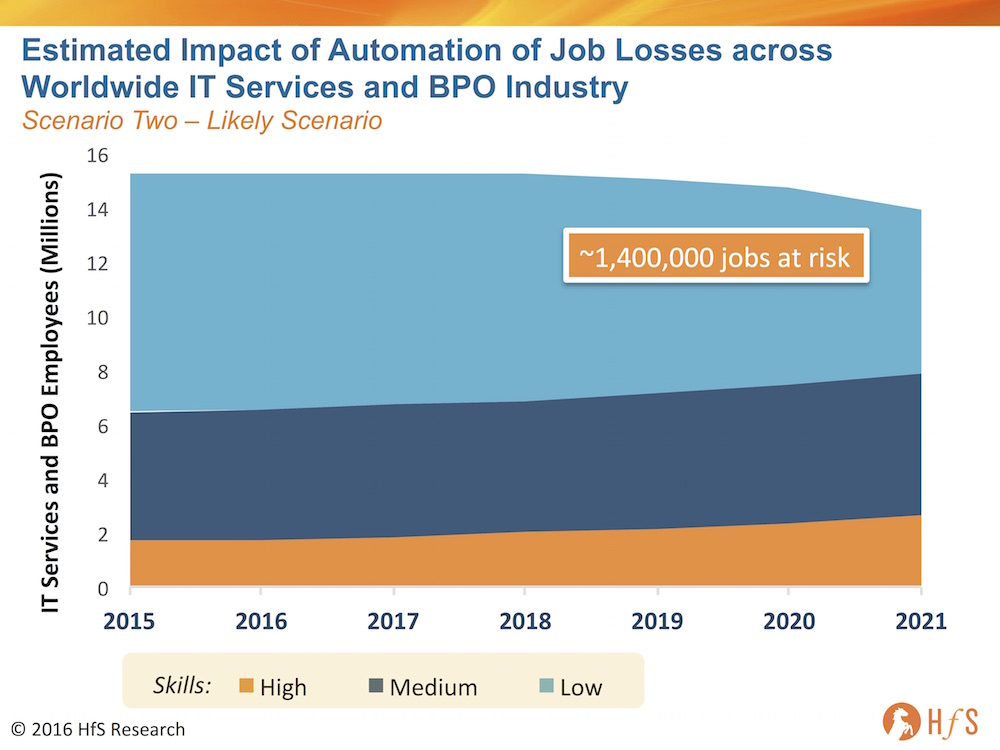

The following graphic shows three Automation Impact Scenarios for the IT and BPO services industry, ranging from a modest/conservative prediction which is a continuation of current RPA use to a scenario we consider more likely where adoption of RPA and more Intelligent Automation increases to an aggressive scenario, where automation adoption hits a broader range of the skills. If we examine the most likely outcome, Scenario 2, we see strong growth for highly and medium skilled personnel—with highly skilled positions in our industry increasing by 56%, and medium-skilled by 8%. However, low skilled, routine jobs drop 30% as many of these roles get phased out over the next 5 years, resulting in a net loss of 9% of jobs, totaling 1.4 million:

Click to Enlarge

The following graphics shows Scenario 2, the Likely Scenario, in more detail, outlining the number of workers being affected within each skill category over the next 5 years:

Click to Enlarge

Click to Enlarge

So what does this mean for the future of the global services industry?

The business and IT services industry has grown rampantly since the early service deals in the 1960s (with the likes of EDS, IBM and Hewitt Associates) and has reached a colossal scale we estimate close to 16 million workers across the prime delivery locations. Like any major industry that reaches a saturation point, as technological and operational methods improve, the need to continue adding staff will decrease once customer demand slows to modest levels. Just look at the evolution of automotive, aerospace and general manufacturing industries; now the same is finally happening to white collar industries where it is now very feasible to digitize work that was previously manually driven. Finally, automation has truly reached “swivel chair” business processes where manual interventions to process chains can be mimicked into software “recordings” to conduct said sub-task. While smoothing out various processes has the impact of freeing up time for existing office workers to focus on other (possibly higher value) activities, the ultimate effect, besides “human augmentation” is to enable businesses to conduct more of the routine work with less human effort and, potentially, less headcount.

How enterprise buyers and service providers of IT and business services will adopt digital labor

Most buyers are constantly investigating how to improve processes and where automation makes sense for them. It’s simply not possible to automate every flawed process chain—the cost and time is simply not worth it, so they need to select processes that warrant the Intelligent Automation investment—usually ones with high intensity repetition and throughput (and lots of paperwork that can be digitized), where RPA has a sizeable positive ROI. In most cases, Intelligent Automation potential is overlooked because the buyer just didn’t have enough financial incentive to make the investment.

However, on the sell side, the more service providers can deliver standard process delivery models to their clients, the more cost effective they become and the more price competitive they can be. Hence, smart automation is critical to their business models and competitiveness, and this is where we see most of the impact in the services industry in the coming years. The service providers will delivery efficiently automated services and then be able to pass on these “savings” from “digital labor” to their clients. This is why we envisage significant updates from the service provider community as Intelligent Automation capabilities quickly get embraced and embedded in service models across all core business and IT processes.

The Bottom Line: Automation and digital labor are increasingly pivotal elements of service delivery—we need to be smart about increasing human value in services

The choice will largely be down to the workers figuring out whether they want to stay in this industry and learn new skills and ways of working, in order to continue to be effective. As the data plainly shows, the services industry, from an employee standpoint, is likely to be 10% smaller in five years’ time. That may be a significant number of workers, but this reduction is gradual and gives ambitious workers the chance to reorient their skills and job focus. Our industry will likely lose that number (or more) through natural attrition over a five-year time period, so the core issue here is to embrace the value of making processes run better and how this helps us focus on growth initiatives and customer-aligned initiatives. As the head of a call center recently declared to us: “As long as we touch the customer in a valuable way, we can’t be automated.” That says a great deal about where we need to focus as this industry goes though this evolution.

HfS subscribers can click here to download the full POV, which details the HfS sizing and forecasting methodology for the impact of digital labor

Just stare at that digital underbelly… there’s a lot of work needed down there!

When the news broke last month about the second largest IT services merger of all time (after the 2008 HP-EDS whopper), the reaction among the services cognoscenti was – and has continued to be – one of confusion. Big services mergers have just not done very well over the years. HP/EDS was a culture clash of immense proportions – and occurred right before the great recession, while other mergers, like Dell’s acquisition of Perot, has resulted in the old Perot business being flipped over to NTT Data at a significant loss, and the Xerox/ACS merger has been shaken up and spun off and needs a major reinvention under new CEO Ashok Vemuri to get the company back on track. Meanwhile, Capgemini and IGATE are still figuring out the best pieces of each other to mesh together, while not taking their eye off the ball, during the services industries’ most cut-throat transition phase.

We heard HPE CEO, Meg Whitman, excitedly address the firm’s key clients and industry analysts at HP’s recent Discover event in Las Vegas, with an obsessive focus on “digital transformation” and the impending impact of “digital disruption”. However, the real opportunity for HPE isn’t really in the design of digital business models for clients, it’s the enablement of them – it’s the provision of the agile “digital underbelly” to make digital change really happen for enterprises.

It’s easy to be cynical about legacy IT services, but there’s an awful lot of it to scrap over as enterprises are forced to fix their plumbing

Digesting the merger of these two struggling services giants has resulted in more rumination than most, considering the timing, sheer scale, transitional uncertain market and motivation. This is not a time when most traditional service providers are looking to add more global delivery scale to already large foundations – most are trying to slim down their delivery armies and sales forces, choosing to focus on new and emerging areas for growth and getting more services delivered for less FTEs by taking better advantage of automation technologies, standard SaaS platforms and more affordable cloud provision.

However, when you consider only $15 Billion is being spent on public cloud services (IaaS) this year and $ 1 trillion being spent on services tied to traditional services delivery, there is a huge amount of “legacy” IT and BPO business in play – for another decade and beyond – to enable the enterprise digital experience. Hence, the opportunity HfS sees for Newco, is to attack the IT and operations plumbing necessary to enable the fast-emerging Digital enterprise, and take on the likes of IBM, NTT/Dell, Atos, Capgemini and the Indian-heritage majors.

Why the Digital underbelly poses a massive opportunity for cost-effective agile IT infrastructure providers, such as the HPE+CSC Newco

The onset of digital and emerging automation solutions, coupled with the dire need to access meaningful data in real-time, is forcing the back and middle to support the customer experience needs of the front. Our new study on achieving Intelligent Operations (see link), which canvassed 371 major buyside enterprises, reveals two key dynamics that are unifying the front, middle and back offices:

A “customer first mindset” is the leading business driver driving operations strategies. Over half of upper management (51%) view their customers’ experiences as impacting sourcing model change and strategy, which is placing the relevance and value of the back office in the spotlight.

Three quarters of enterprises (75%) claim digital is having a radical impact. We can debate the meaning and relevance of digital forever, but the bottom line is that enterprise leaders need to (be seen) to have a digital strategy – and a support function that can facilitate these digital interactions and data needs. The old barriers, where staff in the back office don’t need to think and merely oversee operational process delivery, and those in the middle, which only venture a part of the way to aligning processes to customer needs, are fading away.

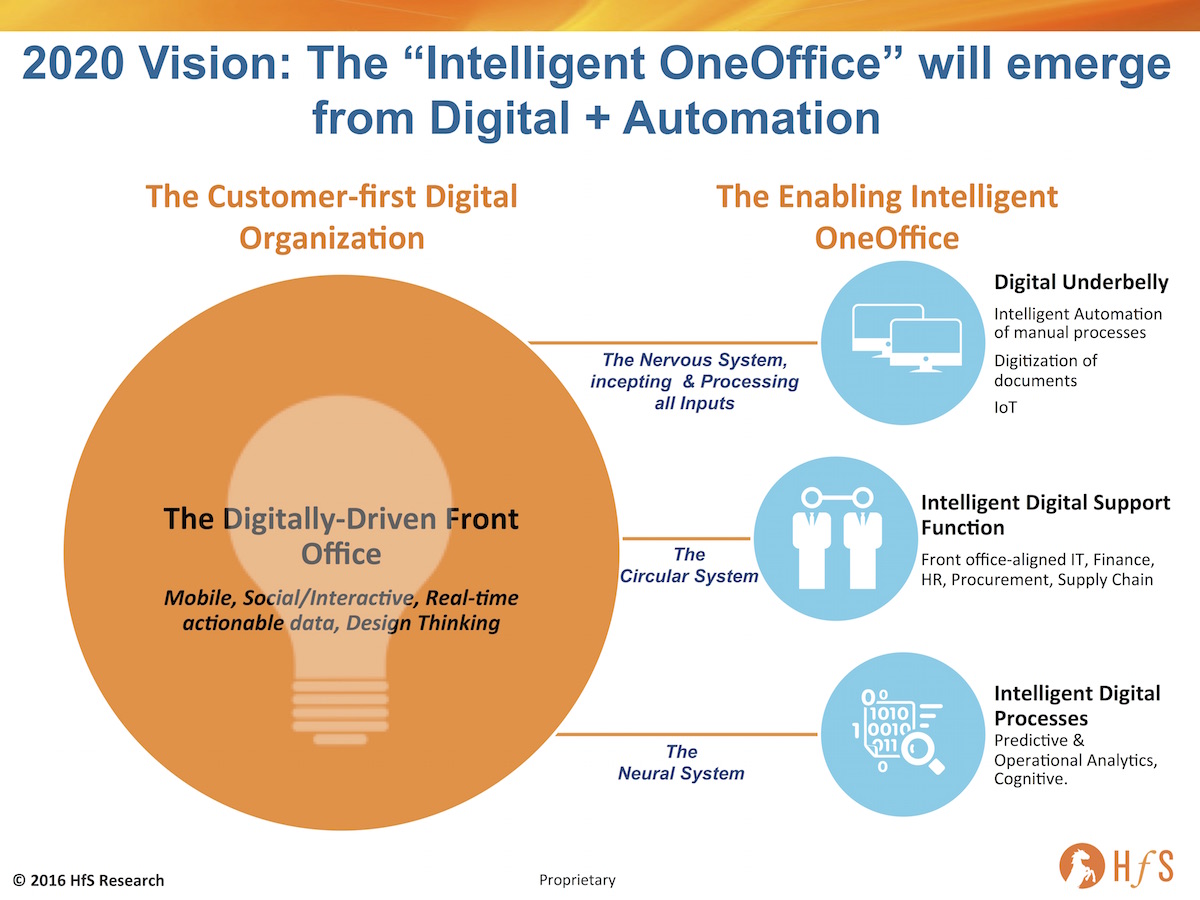

Consequently, we’re evolving to an era where there is only “OneOffice” that matters anymore, creating the digital customer experience and an intelligent, single office to enable and support it:

Click to Enlarge

The Digitally-driven Front Office drives the Digital Transformation

Digital, in its purest form, is all about transforming the business to create, support and sustain the digital customer experience. It’s about leveraging the omnichannel (mobile, social and interactive technology) and accessing meaningful analytics to make it happen. Digital enterprises need a support function to service those customers, get their products/services to market when they want them, manage the financial metrics, understand their needs and future demands and make sure they have got the talent which truly understand the outcomes of their work.

In their current forms, HPE+CSC has some real capabilities in industries like travel and insurance to lead the market here, but is its stated digital focus is going to be in the operations and infrastructure rather than on design and industry expertise; it will struggle in markets against service providers with very strong digital design practices, such as Accenture Digital and Deloitte Digiday. In fact, Newco would be smart to partner with these firms to provide the digital underbelly capabilities at scale.

The Digital Underbelly creates the building blocks

Digitally-driven enterprises must create a Digital Underbelly to support the front office by automating manual processes, digitizing manual documents and leveraging smart devices and Internet of Things, where they are present in the value chain. Smart enterprises have realized they simply can’t be effective with a digital transformation without automating processes and fixing manual interventions and breakages in their process flows. Service providers can get ahead by working with their clients to make their processes run digitally so they can grow successfully their digital businesses and create new growth for themselves. Think about a central nervous system that incepts and processes all the elements necessary to make the enterprise function.

This is where HfS views the sweet spot for Newco, provided is can really optimize the economies of scale with the merger to be price competitive with the Indian heritage majors, such as TCS, Wipro, HCL, Infosys and Cognizant. It also needs to convince clients it brings world class engineering talent, security and automation expertise to the table.

Intelligent Digital Support breaks down the legacy functional silos

Enterprises need their support functions (like an enterprise circular system), such as IT, finance, HR and supply chain, to be aligned with supporting the customer experience, as opposed to operating in some sort of vacuum, hence, we are terming this “Intelligent Digital Support”, where broader roles can be created. HPE and CSC together have tremendous depth in areas like finance and accounting, contact center and HR from HPE’s traditional services business, while CSC brings it’s newly acquired procurement capabilities from its Xchanging acquisition.

Newco’s focus needs to shift towards creating a work culture where its delivery staff are encouraged to spend more time interpreting data, understanding their clients’ needs at the front end of their businesses, and ensuring the support functions keep pace with the front office. This is especially the case in industries that are more dependent than ever on real time data, using multiple channels to reach their customers and being able to think out-of-the-box with disruptive business models.

Intelligent Digital Processes must help enterprises predict and orchestrate, as opposed merely to react and maintain

Newco much focus on enabling business processes that align with their clients’ desired digital customer experiences. It’s not about throwing off historical data just to discover what went wrong, it’s about being able to predict when things will go wrong and finding clever ways to get ahead of them. It’s about embedding smart cognitive applications into process chains, about learning from mistakes and new experiences along the way. This is the enterprise neural system. Several of HPE’s IT service competitors have already made strides here with autonomics platforms, such as IBM’s Watson, TCS with its Ignio , Wipro with Holmes, Infosys with Mana and Accenture’s evolving partnership with IPSoft’s Amelia. Without a genuine story in service orchestration and autonomics, Newco could quickly fall behind, as its customers become increasingly eager to embed cognitive and self-learning elements into their business and IT processes.

However, one key service orchestration platform where we see some real growth potential for Newco is with CSC’s industry-leading ServiceNow practice, which has enjoyed continued growth, especially following its 2015 acquisition of Fruition Partners. As CIOs increasingly seek ServiceNow implementations on their CVs (in a Workday-esque manner), Newco should be able to divert many existing HPE clients onto its newly-acquired managed service. Newco just needs to figure out how to grow that competency as two forces coming together, as opposed to ending up with competing P&Ls.

The Bottom-line: The industry is in transition and the winners are those which can pivot and focus fast. Those which can’t will fail

Let’s cut to the chase here – we’re operating in a services world obsessed with preserving the past and ignoring the new. The past was all about predictable revenue and highly-visible cost reduction opportunity – there was a method to the madness. But this was because the true value was about doing things slightly better, but at much cheaper costs. The future is not so predictable – it is about being smarter, more business aware, and technically superior to piece it all together for clients. Oh, and without increased investments. It’s hard, and requires a very different focus, which is one of developing talent to learn on the job, one of evaluating experiences professionals to assess their ability to change, of being able to learn new tools and platforms, which require a mixture of process and business understanding to align with real business outcomes.

The Newco that is HPE+CSC has as good a shot as most to survive the impending service industry carnage, as growth flattens and prices hit the floor for anything that is a mainstream service. It’s sheer size and client portfolio should help it absorb the blows as the market shakes out and the need for increasingly complex “digital underbelly” services proliferates. As we evolve the levers for the survivors to pull are the right combination of labor arbitrage, automation enablement, cognitive understanding and digital enablement. But spending years constantly reorganizing internally to create the beast to deliver all of this with the speed, affordability and agility needed will not work. These two firms need to be slammed together with an urgency and focus not yet seen in our industry. This won’t be pretty and needs to be like a very sticky BandAid being ripped off very, very quickly…because their biggest threat is within themselves.

For a deeper dive into the nuts and bolts of the HPE+CSC merger, download our POV now!