Ever wondered how you can get your coffee maker to turn on the airconditioning, while your robotic dog pressure-cleans your car… all with a couple of clicks on your iPhone? Well, here is the man to give you the lowdown on all embedded intelligence across all connected devices, the man who practically invented the term “IoT” for Gartner during a distinguished career with the Borg, before joining the HfS rebel forces as VP, IoT Technology and Services Research…. Jim Eastlake:

Jim – it’s just terrific to be working with you at HfS! Can you share a little about your background and why you have chosen research and strategy as your career path?

Hi Phil. I think that I can sum that up in one phrase….. ‘The Big Picture’. I began my career at Texas Instruments in 1981. It was a good place to learn the semiconductor business, but TI was very introverted in those days. So, after 6-7 years I decided to join Dataquest, THE preeminent chip research firm. It would only be for a couple of years, then I’d join another semis company. Little did I know that I would become hooked. I loved the opportunity to talk to senior management and strategists from across the industry (Gordon Moore, Charlie Sporck and Jerry Sanders amongst them), focus on the big issues…… and try to figure out what was going on. I’d then formulate my thoughts in research reports that I hoped would educate and inform, and, amazingly, I got good feedback.

Why did you choose to join HfS… and why now?

The world has changed just a bit since then! We now stand on the cusp of the next industrial age, Industry 4.0 and all that. It is the Professional Services firms that are performing THE vital task of stitching hardware, software and services together. They enable a myriad of “digitalization” projects that deliver huge benefits to society. So, what better place to continue my lifelong exploration of the big picture than at HfS.

Where is the industry right now, Jim? Are things really that different than five years ago when you started covering IoT?

We’re following a classic saturation curve Phil, and it’s very early days. Things change fast. The industry takes big strides forward all the time. In the past five years, much has changed: platform architectures, security, edge computing, contact T&C’s, formation of industry standards – just everything.

So what can we expect to see from you at HfS… can you give us a little snippet of what you’re going to be working on?

Most certainly Phil……

After two weeks with the company, I’m deeply into my first IoT Blueprint, scheduled for February publication. We’ve had a wonderful response from participants, so it will be an insightful report. However, feedback from our clients is also focusing my research thoughts on some meaty topics for 2018:

What are the top obstacles to IoT adoption, and how can Service Providers help overcome them?

What IoT platforms are winning out, and why? And, is there a trend to using “standard” platforms as opposed to a Service Providers’ proprietary offering?

What reasoning lies behind the Edge vs Cloud computing decision in a project?

Why do customers choose different Providers for different projects?

What comprises a true end-to-end IoT solution?

What proven business benefits of IoT are emerging in each of the industry Verticals?

And finally, is the analyst industry as exciting as it was 10 years’ ago?

Immeasurably more so, I’d say. Simply because of Digitalization. Change has always represented an exciting time for the industry observers, there’s not been a time like this during my, nearly 40-year, career in the industry. Everything from semiconductors to Services is involved in enabling change that is Societal in scale. Also, on a practical matter, it is now so easy to communicate with clients and to get research to them. Social media, chat rooms, Webex, Skype and the likes provide us with a much more effective communications conduit.

Jim – it’s terrific to have you join us and can’t wait to hear about the convergence of OT and IT!

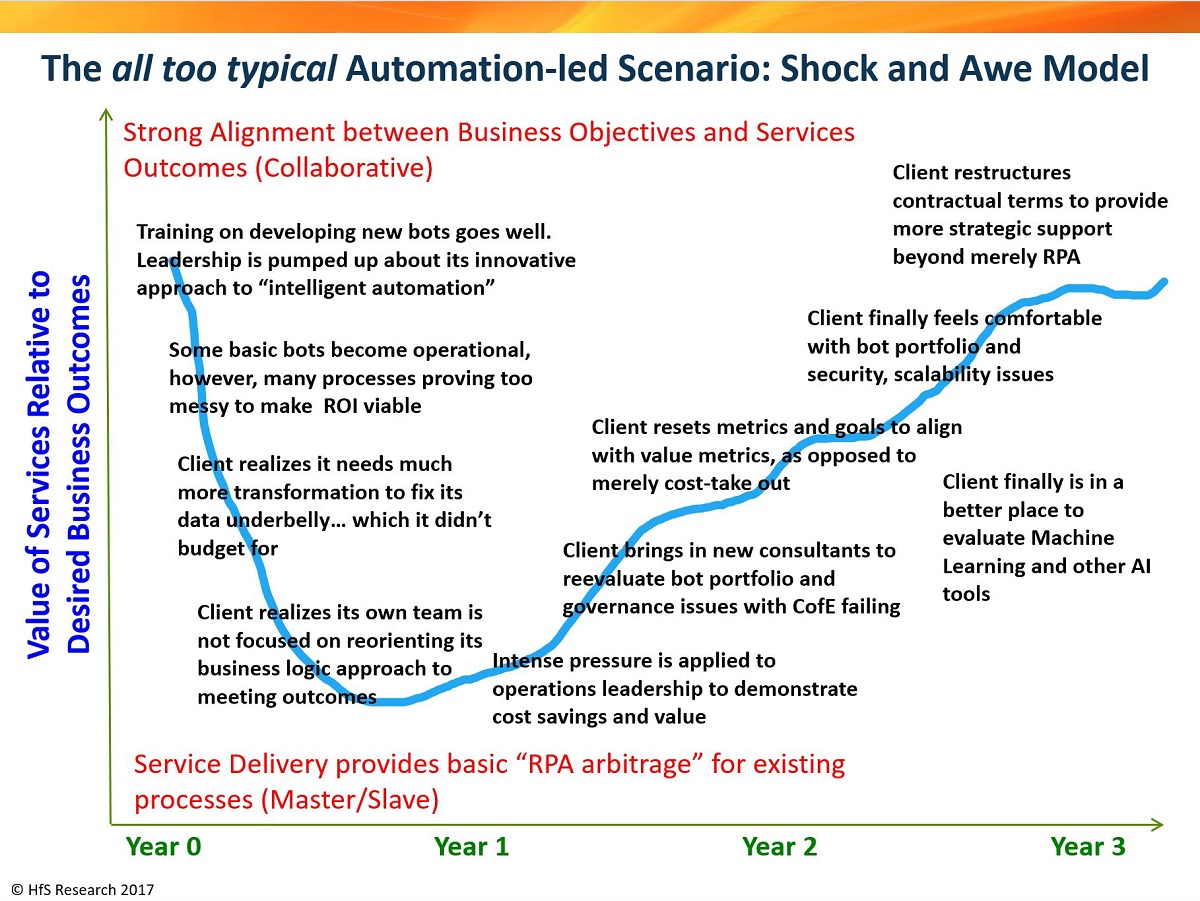

Isn’t it amazing how history has this habit of repeating itself? Especially when it comes to services engagements, where the buyer hopes to shed loads of cost and the providers hope to make a handsome profit, while building a utility model to resell similar engagements to many other buyers.

And that is what we’re seeing, as the services industry evolves from engagements deriving value from lower wage costs to one which combines lower wages with the RPA arbitrage of repetitive tasks being computerized in software recording devices. As one analyst firm once famously declared exactly five years ago: “Welcome to Robotistan, Outsourcing’s Cheapest New Destination“. Or is it?

The difference these days, is that many of the emerging services engagements are being based more on hope than certainty, where many buyers (often naively) think this is going to be just as easy as lumping the work offshore, and many providers simply have little choice but to sell them the dream, and live through the hell with them, if they want to stay relevant in this market. How else can you build an effective automation-led services model, if you don’t have the guinea pig clients to join you on that nice packaged holiday to Robotistan… And, let’s face it, how else are both buyers and providers supposed to behave, when there are so few historical benchmarks to set baseline metrics that both parties know are achievable? Yes people, welcome to the era of Shock and Awe automation deals… it’s the only way.

So let’s skim over the first phase of RPA: The discovery phase: “What is RPA?”, “Do I use AA, BP or UiPath?”, and “This stuff is easy, let’s just PoC it by ourselves”. And don’t forget the “Our attempts at CofEs always fail, but this time will be different because we’ve learned from our outsourcing and shared services experiences”. Let’s begin the new automation-led journey at the phase where they’ve selected their products, appointed the CofE lead, and signed a deal with a service provider daring to escort them to the pearly gates of Robotistan:

The issues that are starting to unravel in this robotic age, is the simple fact that most clients avoided the painful transformation to their data processes and people, during their earlier efforts to source work to lower cost global locations. They were pretty much able to delight their CFOs with 30%+ savings, without having to do much to change their underlying process architectures (the old “lift, shift then transform” approach usually stopped after the “shift”). The reality of moving into an automation arbitrage environment is that you can’t just replicate that work into an even cheaper robotic environment without really figuring out how to do this effectively.

Bot licenses are not cheap, and simply do not make financial sense for a lot of processes, the way they are currently being operated. You can simply end up paying $8K a year for a bot that only is utilized for 20 minutes a day, when you could streamline that process into a broader workflow and use that same bot to process a lot more work for the same cost. Looking at several engagements already in place, clients are committing to significant staff reduction within 12-24 month of contract signing, and many are quickly realizing they are facing some serious complications if they are going to meet the metrics their CFOs are expecting. Either they end up running operations on desperately thin staff numbers, or they own up that they need to rethink that they need a significant transformation on their data infrastructures, processes and people culture, if they are going to enjoy the delightful fruits of Robotistan. As several early RPA adopters will already tell you: You need to do MDM before you RPA.

When you talk to some of the leading consultancies in this space, they will tell you that they are making more of their revenues on pre-implementation transformation work, just getting clients into a place where they can do this. They will also tell you the issues are not about the technology, but much more about the change management necessary to deploy the technology effectively.

The Bottom-line: The early RPA adopters are doing everyone else a huge favor by writing the new rulebook

The biggest issue facing the services industry today is that we have run out of silver bullets, BandAids and scapegoats. In order to get to Robotistan, you need to finally look deeply into your underbelly of messy processes, spaghetti code, manual workarounds and other funky ways of handling exceptions. Moreover, you need to look at your people and figure out how to foster a culture of inclusion and innovation. Most enterprises have been stagnating for years, but as the guinea pigs find their way through their shock and awe of having to conduct real surgery – and psychotherapy – on themselves, a new rulebook that guides us through the steps we have to take to learn, think, calculate and act, will emerge that many of the laggards will gleefully follow.

Japan is currently the only major developed country that is experiencing a population decline and many of its ambitious enterprises are increasingly desperate to find new means to get work done without over-relying on human labor.

Unlike other developed economies, it is not offsetting population decline with immigration, and most its firms have proven very reluctant to engage in offshore labor arbitrage over the years. In addition, Japan has the largest proportion of elderly citizens of any country in the world. In 2014, 33% of the population was over the age of 60 and this percentage is increasing. Hence, getting the most out of its shrinking workforce to keep their enterprise healthy is of utmost importance to a country which loves long-term planning. No joke, but I was once asked to review a 100-year business plan from a major Japanese conglomerate!

Given its shrinking productive population, combined with its wealth, the cost of labor is high. Consequently, its companies are often the first to adopt new technologies, including artificial intelligence and robotics to increase productivity in a market with severe skills shortages. In addition, Japanese firms increasingly struggle to acquire necessary skills to optimize their technology investments which, in turn, raises the cost of these skills. This is leading to increases in spending with third party service providers that help to fill these skills gaps.

A massive automation-led services engagement is announced, placing RPA in a whole new bracket for value and cost impact

Hence, it was no huge shock when major Japanese financial services conglomerate, Sumitomo Group, announced an unprecedented RPA initiative (see the news release), with savings claimed to be in the hundreds of millions of dollars (also see link on UIPath’s website). However, while this is a tremendous public endorsement for the potential benefits of RPA, this appears to be a massive corporate restructuring that is using RPA as a catalyst for labor reduction. We already have discussed (see link) how Japanese firms love to deploy automation to increase productivity and competitiveness – it’s in their DNA as a firm with deep technology and manufacturing roots. In short, most Japanese firms do not suffer from the same negative connotations of automation that their Western counterparts – they are proud to be able to infuse quality and efficiency into their processes.

However, we caution enterprises to take some of the grandiose claims with a bucket of salt, as we’ve not seen anything near these touted levels of productivity gains yet realized, as outlined by HfS analyst John O’Brien in his latest POV.

It’s being touted by some participating suppliers as the largest-ever RPA implementations worldwide, although, ironically, we don’t yet know how many robots are going to be used.

We understand it’s a significant contract in terms of dollar value, and most of the implementation and transformation work is going to IBM. UIPath is doing the (attended) front office RDA automation and the (unattended) back office RPA automation. Blue Prism has also been involved doing some unattended automation in the back office, but SMBC declined to mention them in their press release (see link) which clearly points to UIPath as the prime automation software partner in the engagement moving forward.

According to SMFG/SMBC, the attended digital workforce supports the group’s front-office centric activities, enabling the staff to develop the automation themselves and to work alongside the robot by exerting direct command over it. Complementary, the unattended digital workforce targets all the high volume processes that do not require the human touch, working 24 hours per day and 365 days per year to sustain high-throughput, high-intensity processing. SMFG/SMBC has endorsed UiPath as ‘highly usable and scalable’ supporting the initiative during this week’s UIPath conference in New York.

Bottom Line: Massive kudos for RPA being demonstrated at scale, but this appears more like a massive corporate restructuring using RPA as a catalyst for change

There’s no doubt that right now this endorsement from SMFG/SMBC is great kudos for the RPA vendors aiming to scale enterprise-wide – the most jaw-dropping initiative yet that takes RPA to the 9-figure level in terms of perceived monetary value.

However, RPA initiatives, in general, have not nearly met cost savings and productivity targets anything near these touted outcomes. We’re just not there yet as an industry – sure, many of the more mature deals today are yielding value benefits in the $1m-10m range, once they are being managed effectively, but to jump from these levels to the hundreds of millions is massively far-fetched.

At HfS, while we believe there are genuine intentions from Sumitomo to leverage RPA to free-up and eliminate human labor, there has to be a much broader corporate restructuring plan, way beyond the digital labor initiative, that will get Sumitomo to these lofty targets. It’s also important to point out that these ambitious enterprise-wide deals are already going on in other organizations – for instance, we understand Blue Prism is involved in a number of projects of at least this size across the globe. But these companies are much less willing to share the details of their programs with the wider community – clients, employees, and shareholders are all going to be impacted in some way by the expectations being set, and whether they are realized or not.

Keeping quiet is often the easier way to avoid the kickbacks when things inevitably go wrong. Whether naïve or not, SMFG/SMBC’s level of disclosure means it’s going to be an important test case to assess the success of scaling RPA across the enterprise.

Accenture’s strategy has always been pretty straight-forward: focusing on its major clients and making sure it stays ahead of the pack, where the marketing is moving. This was pretty much the story when we spoke with Accenture Digital’s Group Chief Executive, Mike Sutcliff, two and a half years ago (view blog)… and today all these intentions have been backed up by billions of dollars of bold digital investments, vastly outplaying the competition:

So we hunted Mike down for an update to talk about these massive recent investments and how this Accenture Digital business is shaping up…

Phil Fersht, CEO and Chief Analyst, HfS Research: Good morning Mike – it’s been a couple of years since we first discussed the big digital push your firm is making. Can you share an overview of how the market has evolved since then?

Mike Sutcliffe, Group Chief Executive, Accenture Digital:Sure Phil. Thank you for having me. I guess the first thing I would note is that companies started thinking about digital as a channel or a technology, and then they started to understand that they had to design omnichannel customer experiences. They really started to think about how the digital channels and physical channels blended together.

But what’s happened in the past two years is they’ve started to understand that this is about the entire business model, the operating practices, the business processes, the organization and skills. Not just in the front office but the mid and back office. They are re-architecting their businesses to create fundamentally better experiences that scale across front, mid and back-office operations.

Phil: Do you feel the confusion has lifted around digital? Are clients more certain, now, of where they are going, when it comes to digital strategy?

Mike: I think most clients have really started to understand what the predictable disruption would look like in their industry. They have made choices on whether they want to become the disruptor or be a fast follower. They have started to think about what their roadmap is going to be as they chart out the course of creating, or depending on, new revenue streams in their businesses. The question though is no longer just “what should I do” but “how do I get it done”.

Phil: We’ve talked a lot in general about digital disruption and how traditional businesses are going to get wiped off the face of the planet if they don’t wake up and smell the roses. However, our recent research clearly shows a lot more organizational leadership today is far more bullish about opportunities than threats when it comes to digital impact on their business environments. Do you think traditional firms have figured this out? And who do you see as leading, and lagging, in your experience, when you look at different industries?

Mike: Well I do believe that most of the players in each of the different industry segments we participate in have understood what the disruptors might be. They have looked at what the start-ups are doing and what they are doing and then started to think about what assets and capabilities they have got, in order to give them an ability to win.

Now when they look at their financial flexibility and strength, their customer relationships, their brands, their knowledge, the constraints they are up against in the industry, they have decided that they have every right to innovate and create the next generation of the industry as well. We started with the consumer-facing industries like retail and consumer products, retail financial services, communications and hi-tech. But now we’ve seen that expand across all the industry groups, even the asset-intensive industries that are dealing with comprehensive disruption, where their ongoing business models are slowly degrading, they have started to really engage in what the right digital strategy is going to look like for their industry as it continues to rotate.

I would summarise by saying most of our clients understand what’s happening. They understand what they intend to do about it and now they are thinking about how quickly they move and how they pay for all this.

Phil: So tell us about this aggressive Accenture strategy, Mike. I think you’ve bought at least 20 digital agencies in the last 2-3 years and several other related firms that drive the digital paradigm. What is the grand plan here? Is it to integrate them all together under one common strategy, or are you trying to keep their cultures distinct, and perhaps take more time to see how this industry plays out? What’s the thinking here?

Mike: Well the first thing is that we are not trying to replicate the model of the agencies that do advertising and marketing work. In fact, we are not even really trying to go after the advertising and marketing market itself.

What we are trying to do is to create a single integrated capability, ‘Accenture Interactive’ that operates as an experienced agency. Their job is to design and create the best experiences in the world not just for consumers but for employees, for physicians, for participants in sporting events. What we really want to do is find a way to create better experiences at scale. In order to do that we need many of the skills in e-commerce and contact management and experience design in executing digital marketing campaigns that the agencies would have had traditionally. So what we have been doing is creating a combination of capability from creatives to content to commerce, experience design etc., bringing them into an integrated team at Accenture Interactive, but at the same time respecting the fact that their cultures might differ in terms of the tools, the techniques, the approaches they used to get the work done.

And what we really focused on is making sure that the cultures are all aligned to a core set of values that we’ve got about creating values for our clients as our primary objective and then doing whatever it takes internally to get the team together to make that happen.

Phil: As you look at the experience you’ve had in the last 2-3 years, meshing traditional consulting with these creative types, do you think you have found the secret sauce, or has this been more challenging than even you had envisioned?

Mike: We’ve discovered that the participants in the existing advertising and marketing world were watching the customer expectations evolve and they knew the model that they were working with was not going to be capable of satisfying the demands of their customers.

What we came to the industry with was just a different point of view on how to string together different types of skills and capabilities to serve those customer’s needs. We found that we are in the creative space because we have to be to serve the customer’s needs. The same thing with content, commerce and experience design. As we think about building Accenture Interactive, what we are really doing is appealing to the same objectives that those people have when they started their careers. They want to do great work for clients. We just take maybe a broader view of what it is going to take to do that work.

Phil: I think you already said you are not, but can you ever see Accenture becoming an advertising firm? I know folks in media who are already looking for jobs in Accenture. Clearly, digital media and advertising are merging. I mean do you think it is a possibility in the future?

Mike: No, I don’t. I think it’s absolutely the case that we will be creating products for clients that the advertising industry would call creative work. We are already doing that. It will absolutely be true that we will be either teaching our clients how to buy media and execute their own campaigns. We are doing some of that work on their behalf as part of a broader assignment. So I am not saying that we won’t be doing the work, but what we won’t be doing is trying to replicate the business model of the current advertising industry.

Phil: A very good answer, Mike… so disrupting the model in a different way =) What do you think we will be talking about in another two years? What do you think is going to become the dominant discussion in this digital sphere as we look at the development, the pace and the velocity of what’s been going on?

Mike: Well, Phil, we believe that all of this work in digital is about extending the capability of humans to do what humans are uniquely capable of doing. So I think we are going to be talking about how artificial technologies and immersive virtual and mix reality technologies can come together to enable humans to do the things that they do uniquely well.

We want to make sure that everything that we are working on is either creating a better experience for somebody or enabling somebody to do their job in a much richer way. I think that’s where the industry is headed, but there is lots of work to do to get there.

Phil:I think you once famously said to me “the future of work is going to be no work.” Do you still believe that’s the case?

Mike:Well I believe we will automate away a lot of the what I would call low-value work that humans are required to do today. But I think we will shift that energy to doing things that we don’t do today. I believe that humans will always be engaged in work but I think we will eliminate a lot of the non-value added things that we do today because we can let the technology handle that for us.

Phil: Thanks for your time today Mike – will be good so air your experiences again with our readers!

We seem to have suddenly shifted from the doom and gloom of robots taking our jobs to people proclaiming that AI is going to create millions of new jobs. And if you haven’t endured this latest round of hype, I envy your unique skill in removing fake news from your life.

Suddenly AI is the antidote to automation! Really?

Don’t we have a responsibility to inject some reality into this conversation? Today’s business world is about removing physical touchpoints, about fixing our data, about running processes faster, smarter, more autonomously, and cheaper… So where are the real links between the universities, the politicians, and the businesses? Why aren’t we really debating this stuff in the senates and parliaments if today’s organizations are on an inexorable drive to sub people for better data? Instead, we have academics and “analysts”, desperate for attention, making unsubstantiated predictions that are only fuelling the tech firms, desperate to sell their wares without this negative connotation that the real ROI of selling their products is tied to labor elimination.

Let’s just make the call – AI is indirectly and inextricably tied to the elimination of “unnecessary” labor, by nurturing systems that get smarter with each incident and transaction. The smarter and more autonomous your operations become, the more agile and efficient your business becomes. That’s not a terrible thing – in fact, you are doing your valued staff a huge favor by keeping them employed and keeping them relevant to your business. But you are not creating a net influx of jobs into your organization, you are becoming more fluid and competitive. Sure, you’ll probably look to add some Python and R developers, Machine Learning experts, serious data geeks and design thinkers – or you may just pay consultants to do it all for you – but the bottom-line, here, is that you’re going to be shedding a lot of your left-brained staff performing jobs that can be artificially automated, at a much faster rate than you’ll be adding the data-oriented people you need to digitize your business. AI is about doing more with less, not more with even more – let’s get real.

Don’t get me wrong, the possibilities of faster, smarter, touchless data flows between the customer and the operations of the business, are critical to promote competitiveness and survival, but let’s stop sugar-coating the true purpose of data driven intelligence – the less businesses need to rely on people and the more autonomously they can run processes, the more nimble and profitable they will become. Now if these businesses then choose to reinvest their new-found wealth hiring loads more people, I will tip my hat to these purveyors of job hope, but let’s fact facts, the companies of the future will be running a lot of smart technology with a smaller group of savvy people to manage it all.

Let’s take our much-loved services industry, which is pretty high up the tech-savvy ladder and comprises firms where efficiency and competitiveness are its very DNA

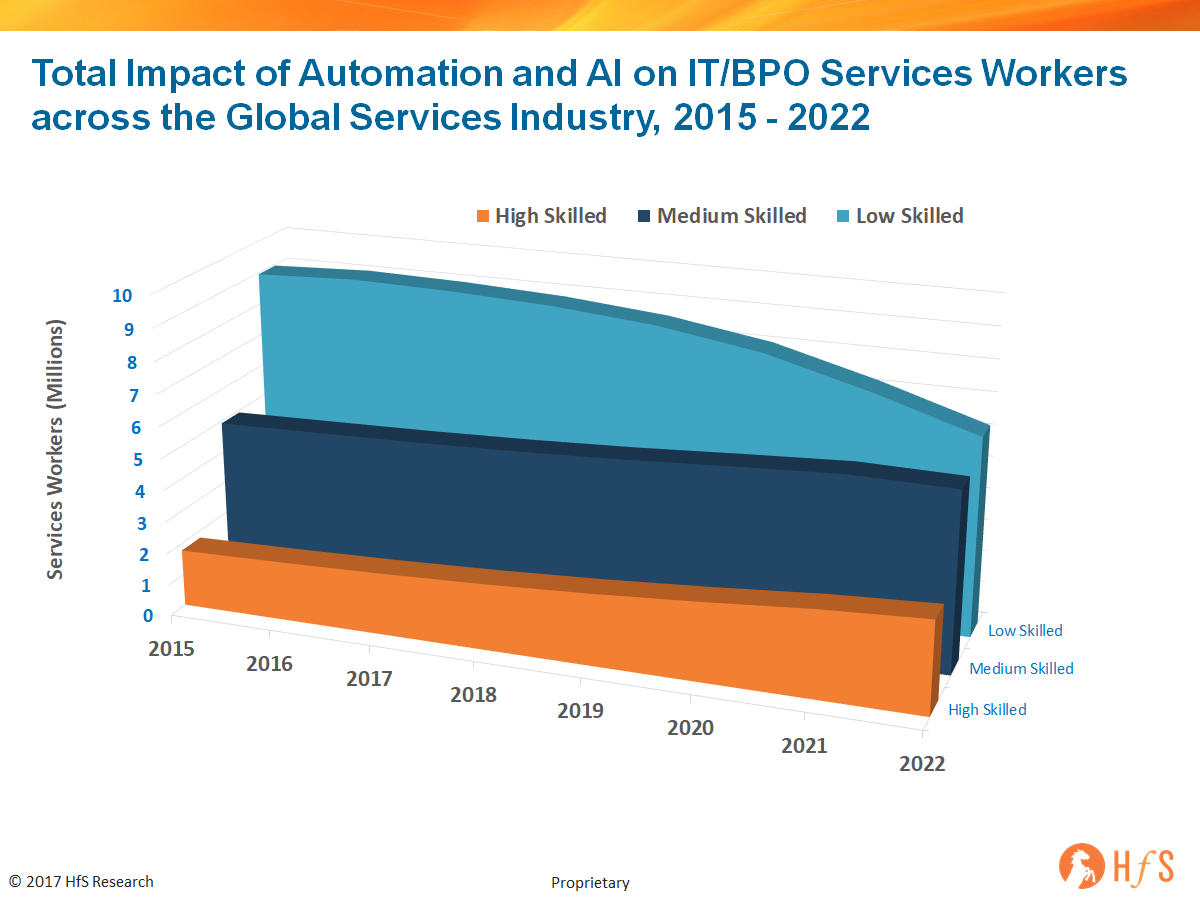

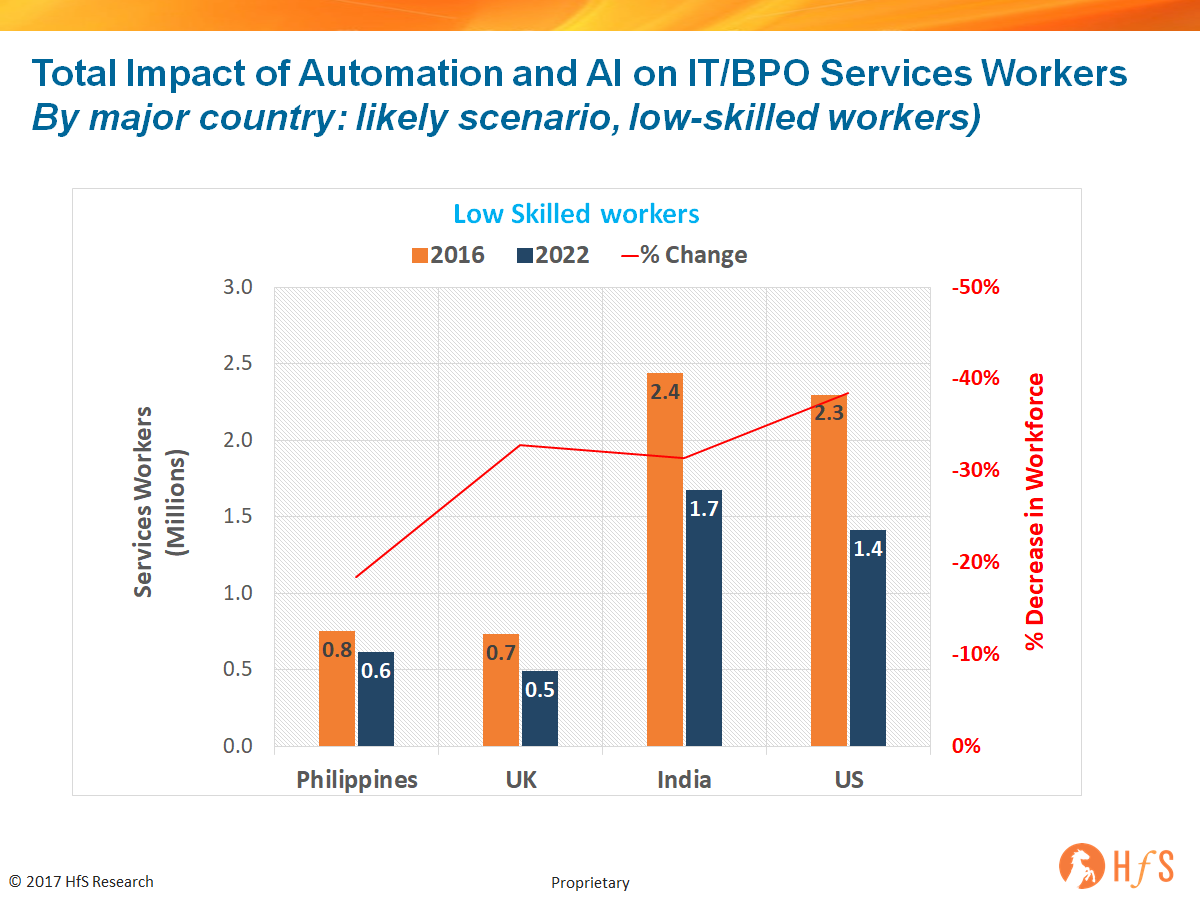

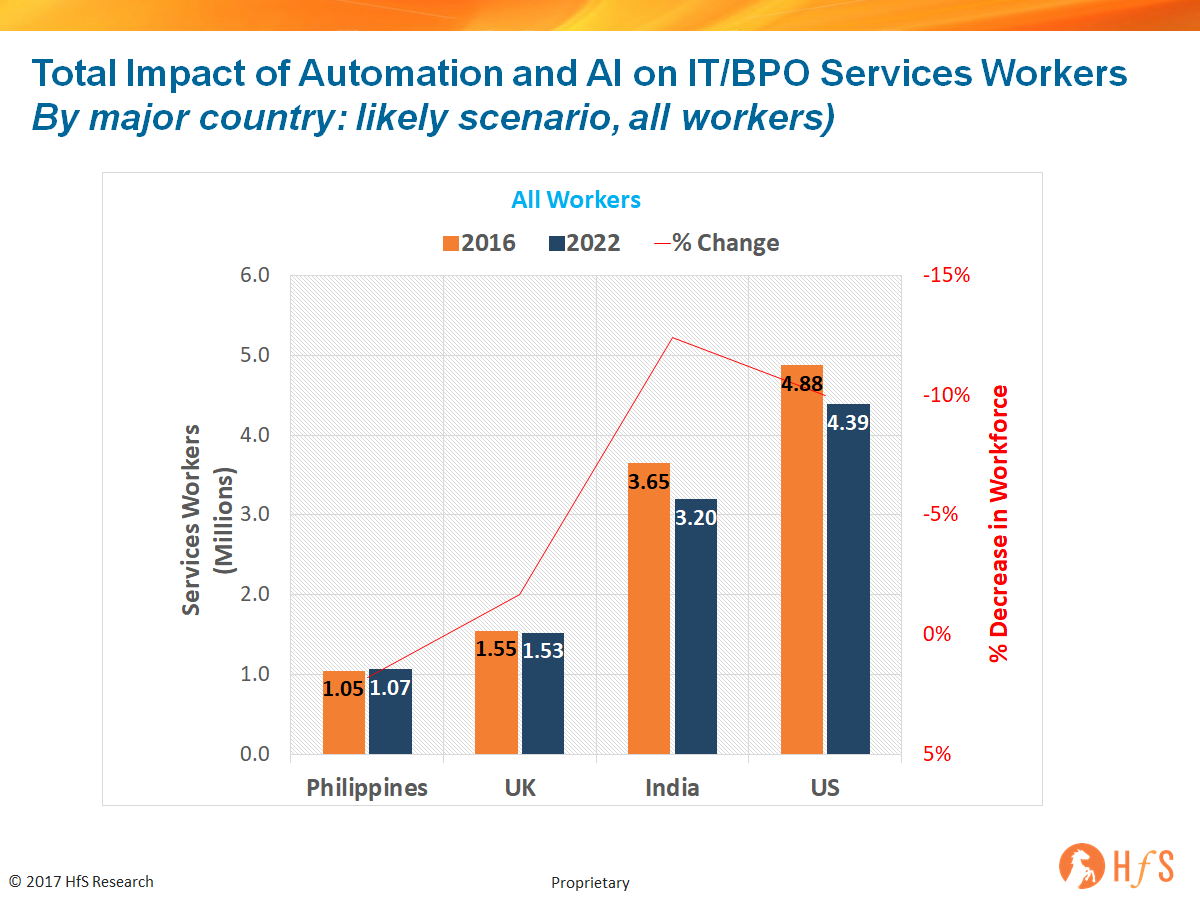

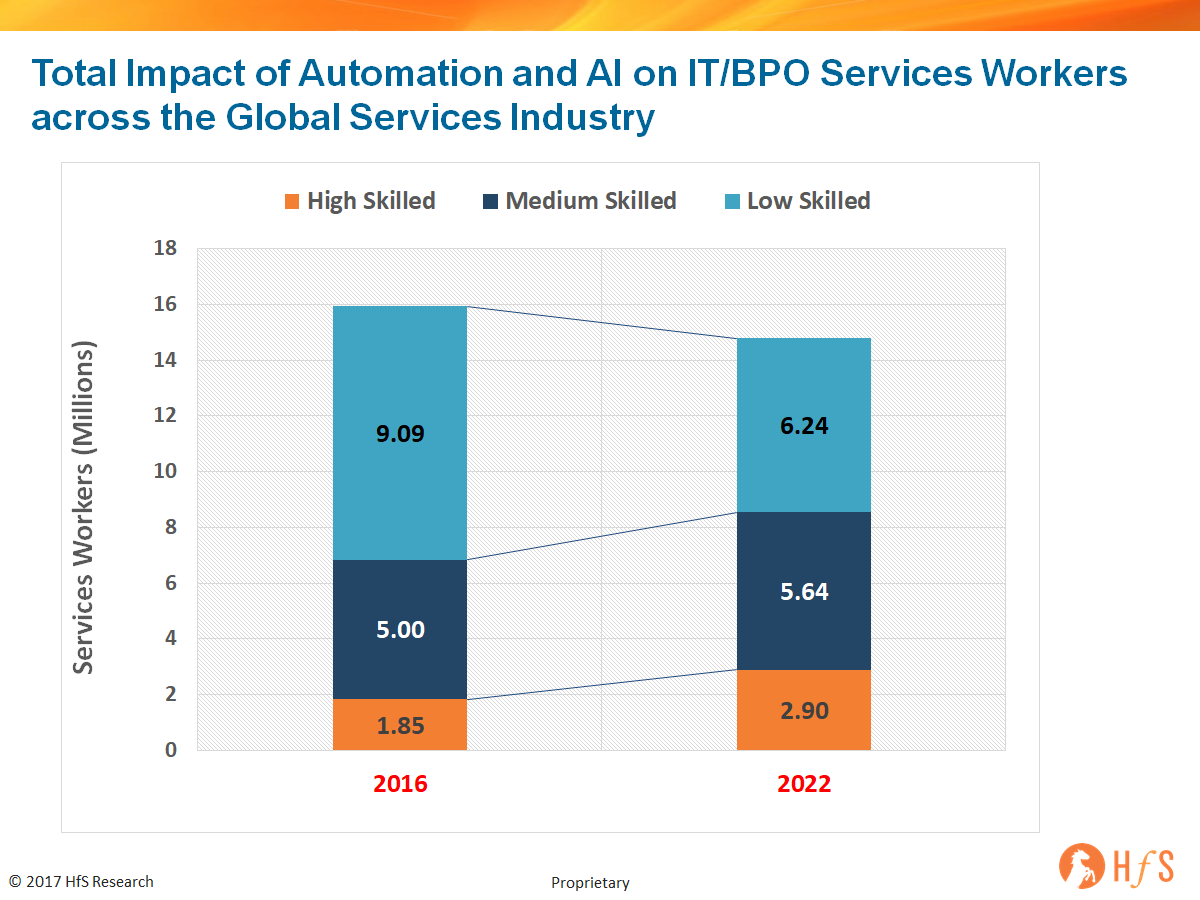

The global IT and BPO services industry employs 16 million workers today. By 2022, our industry will employ 14.8 million – a likely decrease of 7.5% in total workers (see our research methodology and full blog here). This isn’t devastating news – we’ll always lose this many people through natural attrition, but what this data signifies is this industry is now delivering more for less because of advances in automation and artificial intelligence technologies. The new data also shows how job roles are evolving from low skilled workers conducting simple entry level, process driven tasks that require little abstract thinking or autonomy, to medium and high skilled workers undertaking more complicated tasks that require experience, expertise, abstract thinking, ability to manage machine-learning tools and autonomy.

All major service delivery locations are expected to be impacted at the low-end, but the higher the wage costs, the higher the expected role elimination (750,000 roles in India and a similar number in the US)

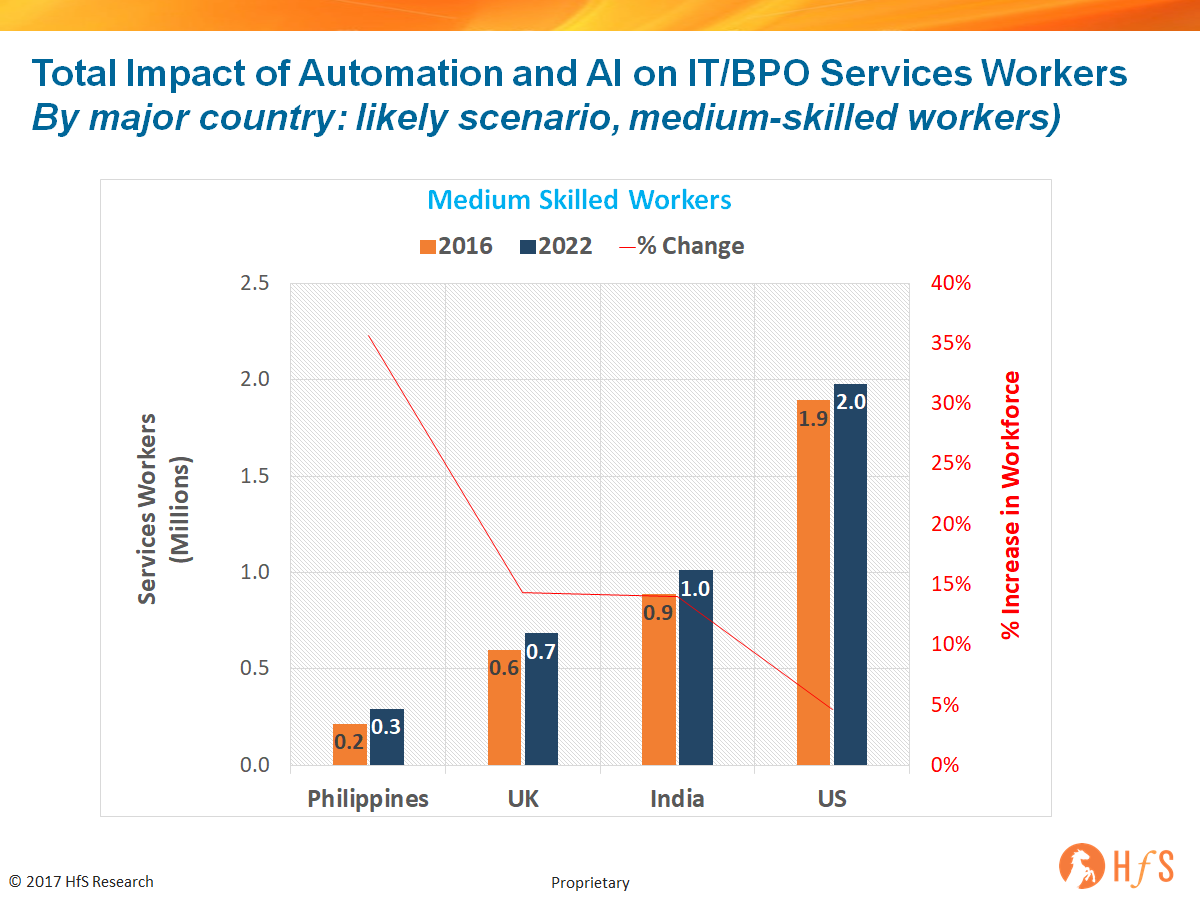

Medium-skilled roles are picking up across the board, especially in roles that are customer/employee facing with the need for more customized support, the ability to handle basic customer and data queries, and more customized service work with virtual agent models in 2nd / 3rd tier escalations:

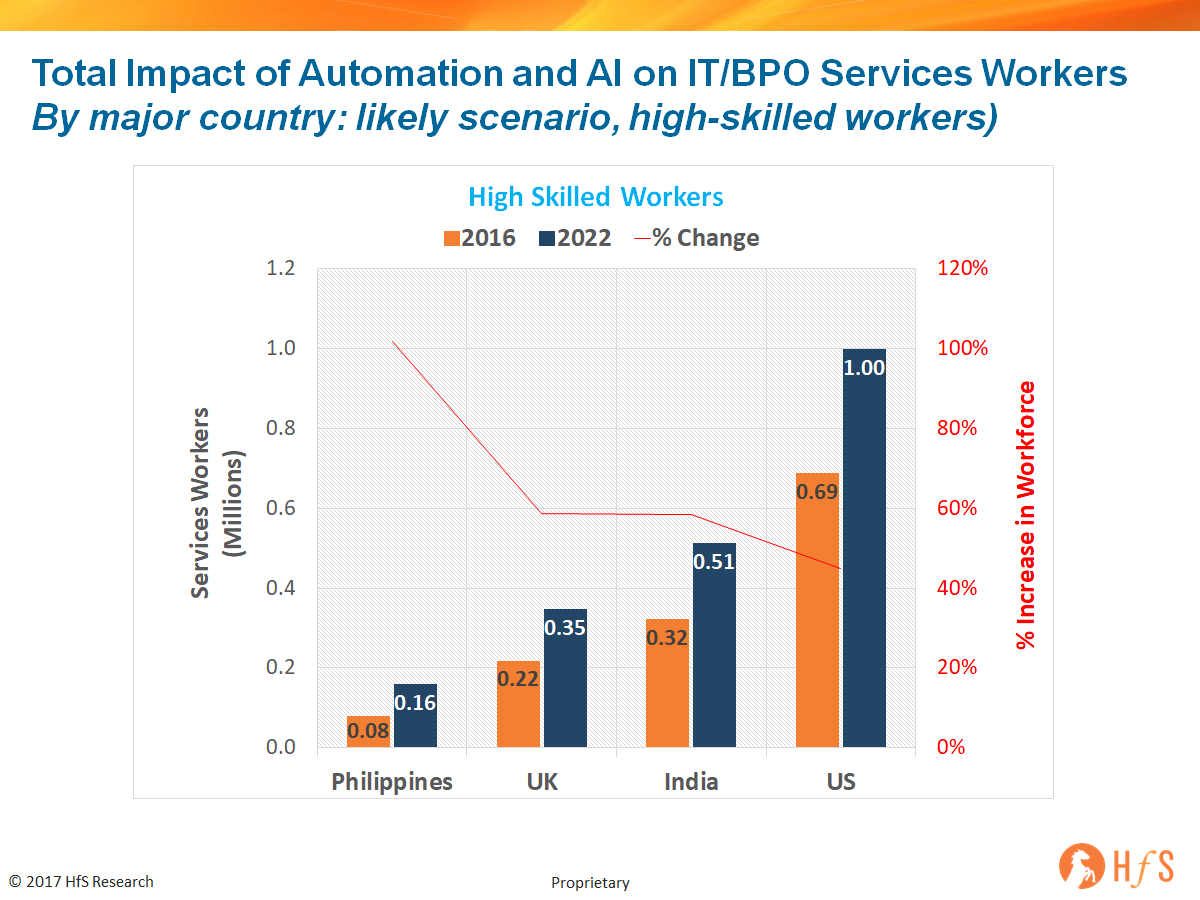

As this data illustrates, the more we automate, and digitize, and the more we adopt human + machine technologies, such as machine learning and cognitive solutions, the more we need people to develop skills in managing automated workflows, Machine Learning mechanisms, being able to interpret data, and service increasingly complex customer and employee needs. So when we take into account the total impact of automation and AI on services jobs, the impact is not nearly as severe as so many of the hypesters and fear-mongerers are prophesizing, but the reality is we’re definitely not creating jobs faster than we are digitizing them out of existence:

Philippines should actually increase its service delivery population due to its dominance in voice and capabilities to support increasingly complex and personalized customer models, the UK should be flat, especially with the challenges of Brexit and the slowdown in low cost worker immigration, while both India and the US will see a total worker reduction estimated at the 10% level between by 2022. You can view the total impact on the global services industry – a worker population decline of 7.5% here:

The Bottom-line: Many jobs that can be digitized are going to disappear, but there is time on our side to develop the new skills we need

The big narrative here isn’t about what’s going away, but more about what is emerging in its place. The next fives years we can manage, it’s the five after that when the impact on labor becomes much more challenging. Transaction roles at the bottom of the value chain have been under threat for many years now – with the impact of low cost location delivery and better technology. Now the emergence of RPA is eventually going to sound the death knell for most high-throughput, high-intensity jobs, as both service providers and enterprises master the ability to apply these technologies effectively. The good news is this takes time and there is no huge burning platform to do this overnight from most enterprises.

So our message to all stakeholders of operations and services is simply to get out of your comfort zones, accept that new skills are replacing old ones, and it’s critical we have a plan to train, develop and invest in changing what we have. I will leave you with six things to think about as you ponder your own value to this industry and your firm:

Which customers have you delighted recently?

What new relationships have you made that add value to our business?

What work have you done that excited people inside and outside of the business?

How are you helping energize your colleagues and exciting them with new ideas?

How have you helped add value to new business wins?

How have you contributed to new initiatives that improve productivity and effectiveness?

Well someone actually said it – and it may not come as a complete shock that it’s come from everyone’s favorite RPA evangelist Guy Kirkwood, of UIPath fame. Even more impressive is guy’s beautiful command of the English language to describe the latest hyped term “AI”, now that most the hypesters have got bored touting the massively disruptive impacts of IoT and digital – and the automation conversations have just got a bit rinse and repeat. Guy is saying that true AI is when we arrive at the “singularity” (which Ray Kurzweil predicts will happen in 2029), when machines will become smarter than humans, abruptly triggering runaway technological growth, resulting in unfathomable changes to human civilization.

Guy basically claims it’s incorrect that we are dubbing the conglomeration of tools, such as NLP, Machine Learning etc as “AI”. While I agree with Guy that the inane use of the term AI is driving me (and many of my colleagues) to scream “Please just stop the bollocks!”, my point to him is: what else do we call tools which are all about “the simulation of human thought processes across enterprise operations, where the system makes autonomous decisions, using high-level policies, constantly monitoring and optimizing its performance and automatically adapting itself to changing conditions and evolving business rules and dynamics.” So if this isn’t Artificial Intelligence, what is it?

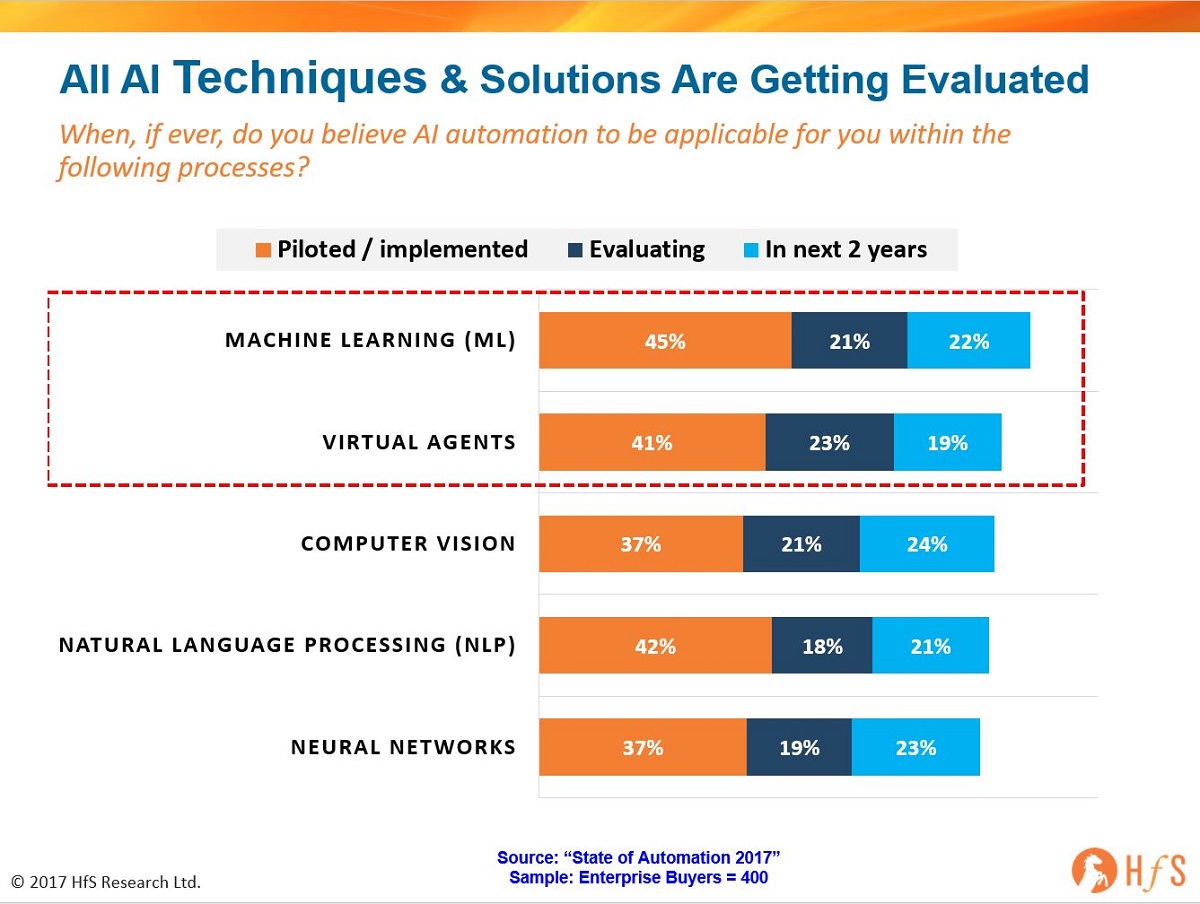

And my further point, here, is that these tools are already here and being heavily piloted and evaluated, according to 400 major enterprises in our recent State of Automation and AI Study:

Sorry, Guy, but while we all want to scream “bollocks!” at all the bollocks, I think we’re stuck with AI until the next buzz term comes along =)

HfS recently hosted the debut session of the newly-formed Future of Operations in the Robotic Age Leadership Council (FORA) in Chicago. The purpose was to bring together stakeholders across all corners of enterprise operations, services and intelligent automation software arenas to lock heads and map the course of this emerging industry: business operations being fundamentally redesigned by the impact of intelligent automation and digital technologies. We believe this is becoming known more broadly as the “digital operations industry”. So let’s hear the consolidated feedback from the industry’s key stakeholders:

The FORA Mandates, Q4 2017

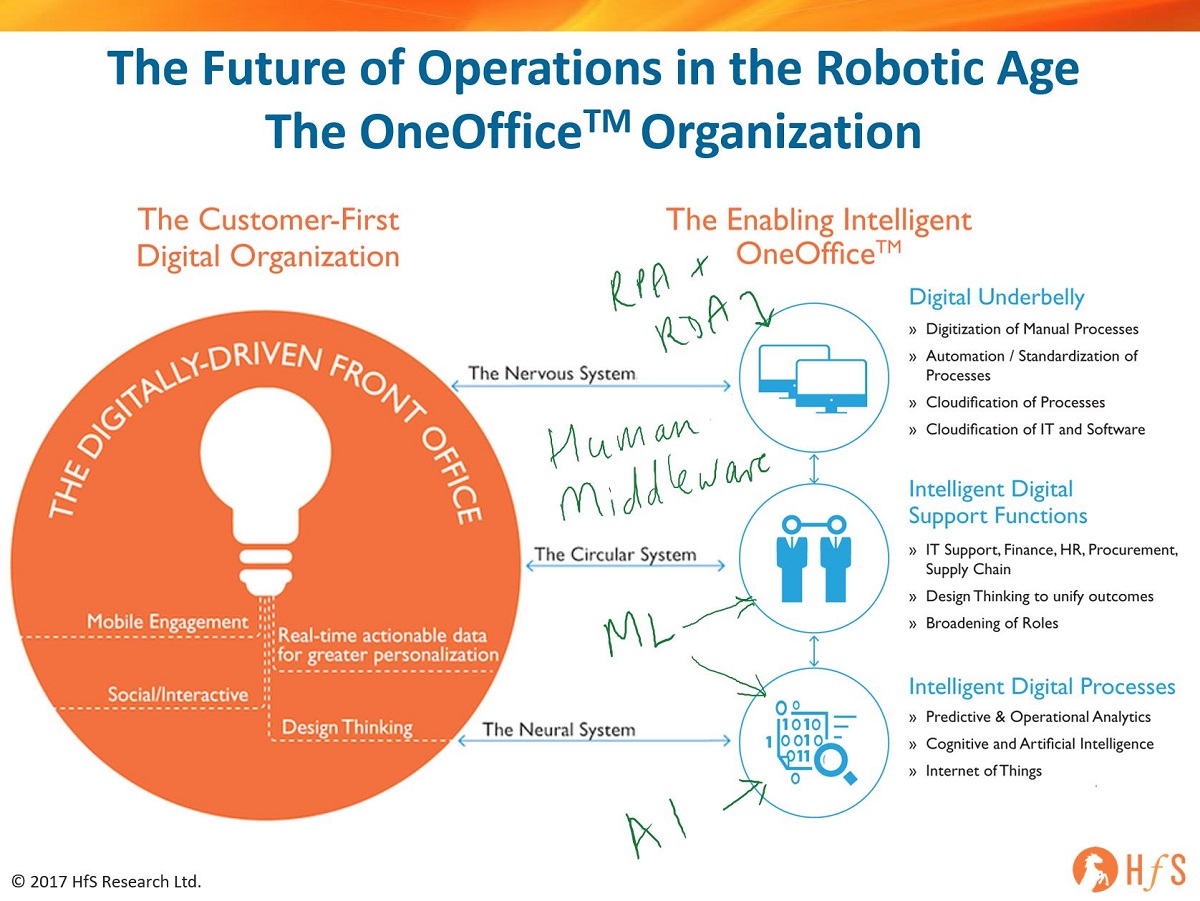

1) Automation technologies can collapse the barriers between front and back offices

While there’s a lot of noise and scaremongering in the public sphere around job losses, the real story is that automation technologies of various flavors and deployments — RPA, RDA, AI, etc. – are quietly creating a new execution layer on top of the IT “stack,” one that offers a flexible, reconfigurable operations platform for the business. Freed from the costs and rigidity of legacy systems, savvy enterprise architects see automation technologies, together with the data they capture and generate, as a way to digitally connect their back-, middle-, and front-offices for greater throughput, quality, and responsiveness.

2) Commercials of engagements must be reconstructed around the economic value of robots

Automation is destroying the traditional FTE-based cost/value equation for service delivery, and we need a new “post-FTE” commercial model, one based on partnership, business outcomes and joint value creation for buyers, advisors, and provides. The economic value of a robot is vastly different in kind, cost and scale from that of a human being, and is forcing us to rethink the value of different kinds of work – separating rote transaction work from judgment-based work. Ultimately, this will require all parties to re-think their offerings and value propositions and to demonstrate imagination, creativity and flexibility, while educating their respective stakeholder communities and managing the financial and human impacts.

3) From the C-Suite to the manager, enterprises need people who appreciate and understand the value of data

Success in achieving the OneOffice future requires a blend of strategy, business design, and technology skills to re-think and re-configure core processes with a singular focus on improving the customer experience v. just cutting costs. Automation per se looks deceptively simple (and is often sold with that promise) but can fail to deliver true value if simply retrofitted on existing processes; coupled with artificial intelligence and cognitive, automation can support new services and capabilities at speed and scale. But thoughtful tool selection and disciplined deployment is crucial. And as data grows exponentially, it becomes the essential raw material for every enterprise in every industry. At every level of the organization – from the C-Suite to manager – enterprises need people who appreciate and understand the value of data and who can identify/extract the most important customer-relevant insights.

4) Businesses must be redesigned from a logical rather than physical perspective

Native digital businesses have demonstrated the value and power of a digital operations approach by thinking about their business from a logical rather than physical perspective – focusing on customer outcomes rather than internal inputs. They begin with an intense focus on identifying their customers’ most important ‘priorities’ (as distinct from ‘needs’) to design a differentiated and dynamic customer experience. They then build and optimize a collaborative partner ecosystem to deliver that experience, leveraging specialist capabilities and resources. The result is a more disaggregated but fiercely cooperative business model. The challenge for non-digital natives is to re-imagine their businesses from this logical perspective and to demonstrate what one executive called the “willingness to let go.” That implies – and requires – a fundamental re-thinking around control and governance as well as motivation and reward, supported by deep and enduring commitment to change management.

I hope to see many of you in London on 7th December for our next round of pivotal discussions. A big thanks to all of you for your terrific support with the FORA Leadership Council initiative,

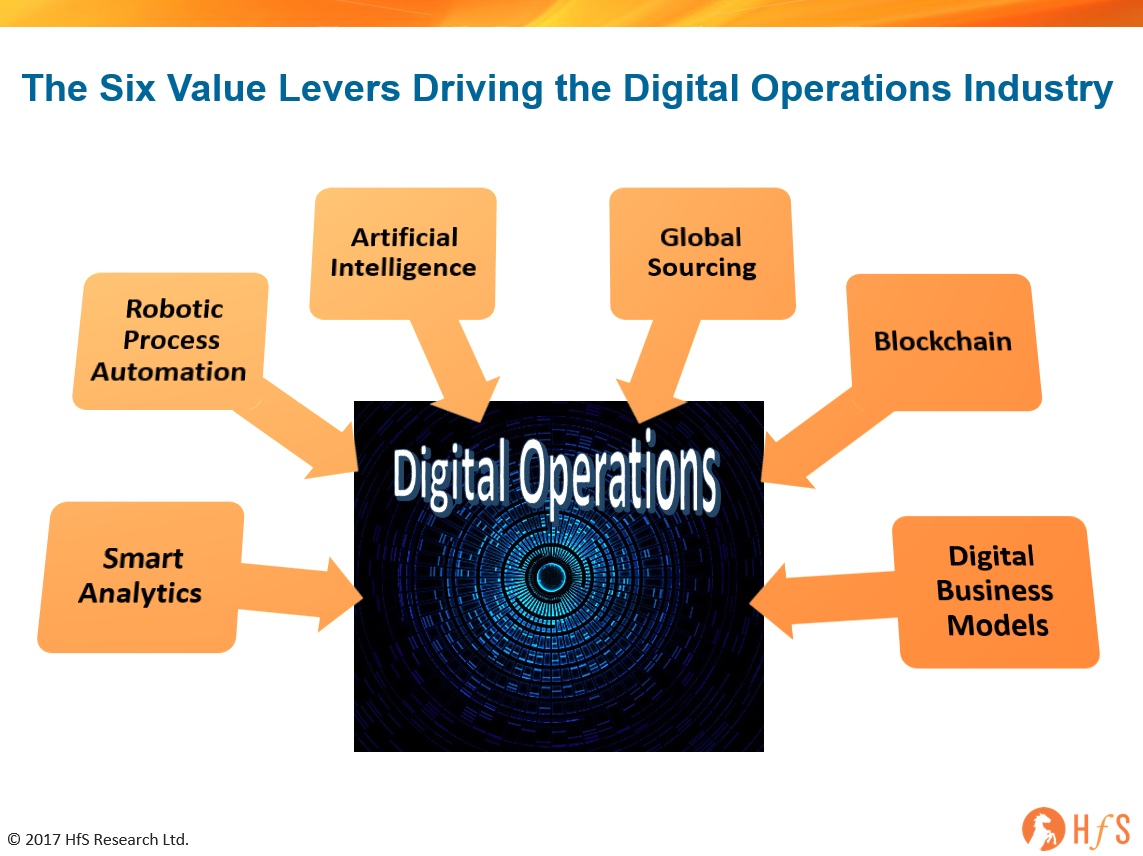

As we brace ourselves for yet another deluge of dodgy automation and AI predictions for 2018, where people just make stuff up and hope we don’t remember them in a few months, we thought we’d break the mold and actually release some real numbers based on real adoption trends and real expenditure date on software and services. We also had the audacity to define the market so this might actually make some sense:

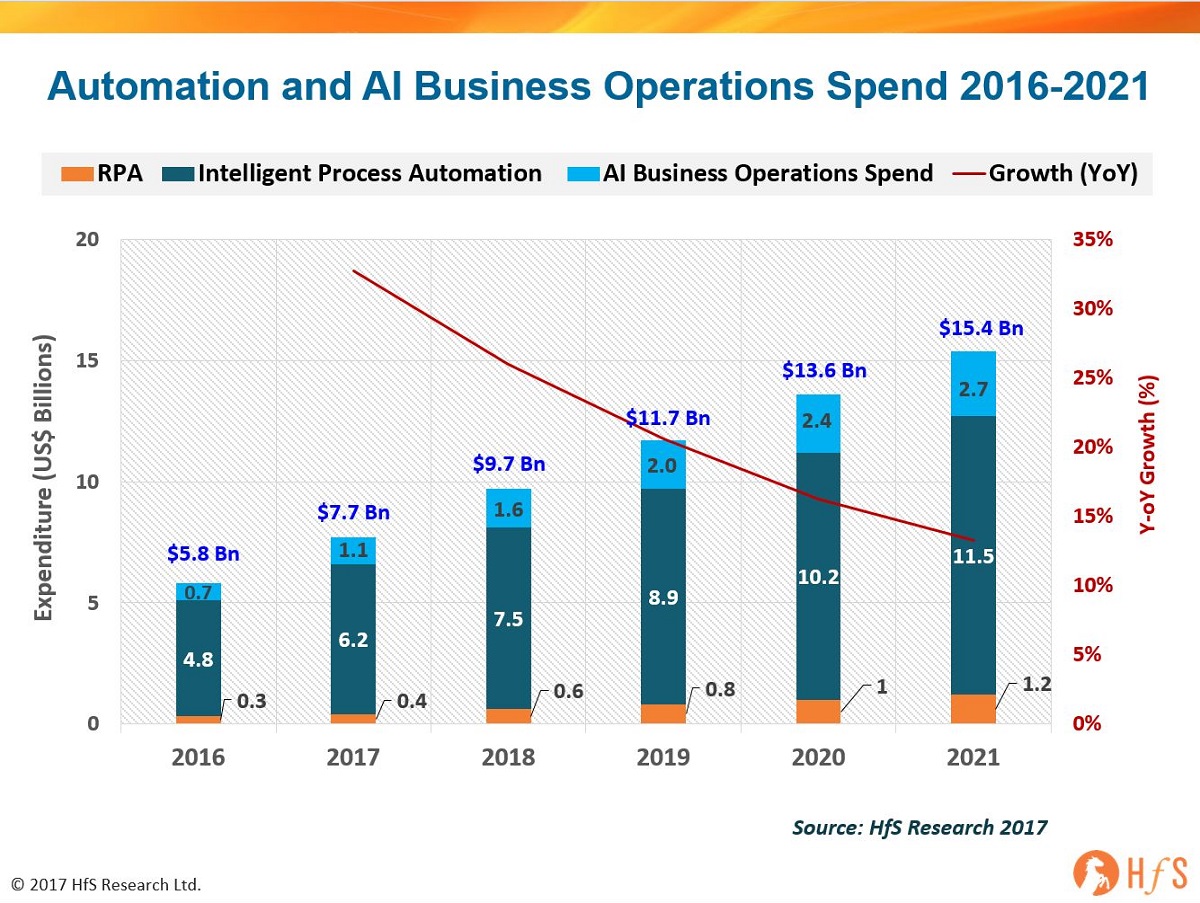

As we revealed earlier this year, despite all the ridiculous hype, the global market for RPA Software and Services will pass $400 million in 2017 and is expected to grow to $1.2 billion by 2021 at a compound annual growth rate of 36%. The direct services market includes implementation and consulting services focused on building RPA capabilities within an organization. It does not include wider operational services like BPO, which may include RPA becoming increasingly embedded in its delivery.

RPA Definition: RPA describes a software development toolkit that allows non-engineers to quickly create software robots (known commonly as “bots”) to automate rules-driven business processes. At the core, an RPA system imitates human interventions that interact with internal IT systems. It is a non-invasive application that requires minimum integration with the existing IT setup; delivering productivity by replacing human effort to complete the task. Any company which has labor-intensive processes, where people are performing high-volume, highly transactional process functions, will boost their capabilities and save money and time with robotic process automation. Similarly, RPA offers enough advantage to companies which operate with very few people or shortage of labor. Both situations offer a welcome opportunity to save on cost as well as streamline the resource allocation by deploying automation.

Intelligent Process Automation

RPA is only 10% of the true picture when it comes to total spending by enterprises on automating their processes. The internal training and development, pilot projects and trial implementations, is so much larger than simply software licences and third-party professional services to work the software effectively. We term this broader automation market, beyond RPA as “Intelligent Process Automation”. This market will surpass $6bn this year and more than double over the next four years.

Intelligent Process Automation Definition: Intelligent Process Automation (IPA) is the use of technology to allow a business function or part of the operation of a process workflow work automatically. It includes the use of RPA, BPM suites, Remote Desktop Automation, screen scraping and custom scripting and related technologies. IPA comprises of two core elements:

External professional services: Relates to all external spending focused on developing business process automation strategies / roadmaps and the use/ implementation of automation with business functions.

Internal operational spend: Includes internal and external spending on automation – change management, IT and operational teams focused on process automation and automation use as part of existing business process management initiatives.

Artificial Intelligence

And the most talked about area is Artificial Intelligence (AI), which is already emerging as a billion dollar market for enterprise operations, and could almost treble in spend in four years.

AI Definition: AI refers to the simulation of human thought processes across enterprise operations, where the system makes autonomous decisions, using high-level policies, constantly monitoring and optimizing its performance and automatically adapting itself to changing conditions and evolving business rules and dynamics. It involves self-learning systems that use data mining, pattern recognition, machine learning. virtual agents, computer vision and natural language processing to mimic the way the human brain works, without continuous manual intervention.

The Bottom-Line: Automation and AI have a significant part to play in engineering a touchless and intelligent OneOffice

However which way we spin “digital”, the name of the game is about enterprises responding to customer needs as and when they occur, and these customers are increasingly wanting to interact with companies without physical interaction. This means manual interventions must be eliminated, data sets converged and process chains broadened and digitized to cater for the customer. This means entire supply chains need to be designed to meet these outcomes and engage with all the stakeholders to service customers seamlessly and effectively. There is no silver bullet to achieve this, but there is emerging technology available to design processes faster, cheaper and smarter with desired outcomes in mind. The concept was pretty much the same with business process reengineering two+ decades ago, but the difference today is we have the tech available to do the real data engineering that is necessary:

In short, every siloed dataset restricts the analytical insight that makes process owners strategic contributors to the business. You can’t create value – or transform a business operation – without converged, real-time data. Digitally-driven organizations must create a Digital Underbelly to support the front office by automating manual processes, digitizing manual documents to create converged datasets, and embracing the cloud in a way that enables genuine scalability and security for a digital organization. Organizations simply cannot be effective with a digital strategy without automating processes intelligently – forget all the hype around robotics and jobs going away, this is about making processes run digitally so smart organizations can grow their digital businesses and create new work and opportunities. This is where RPA adds most value today… however, as more processes become digitized, the more value we can glean from cognitive applications that feed off data patterns to help orchestrate more intelligent, broader process chains that link the front to the back office. In our view, as these solutions mature, we’ll see a real convergence of analytics, RPA and cognitive solutions as intelligent data orchestration becomes the true lifeblood – and currency – for organizations.

Do take some time to read the HfS Trifecta to understand the real enmeshing of automation, analytics and AI.

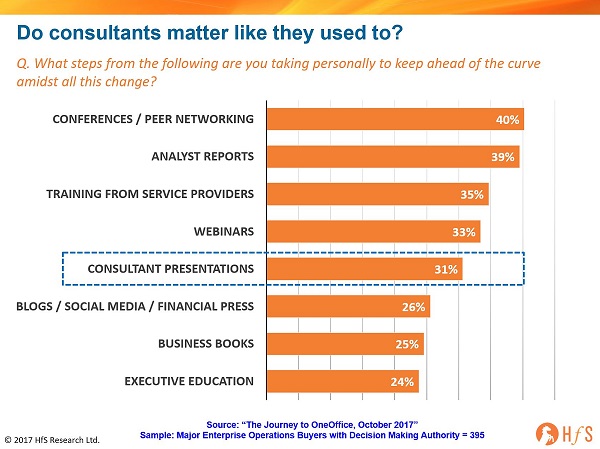

Over the last 15 years, we’ve witnessed the rise and fall of the sourcing consultancy. Clients needed help finding the right services partners – at the right price points – and the likes of EquaTerra, TPI (now ISG), Everest, Alsbridge were there happily to oblige. Today, only ISG survives as a credible boutique sourcing advisor, while the Big 4 have moved into developing sourcing practices of their own. However, new data from our soon-to-be-unveiled, Journey to the Digital OneOffice study, conducted with the support of Cognizant, shows that decision makers for business operations are looking largely to other places to stay ahead of all this change:

However which way we look at this, not even a third of decision-makers are relying on consultants in this ever-confusing market, when you would have thought consultants would be licking their lips at the opportunity. Don’t these guys feed off confusion, hype and nervousness from the well-resourced enterprise leaders, only too keen to pay their rates to get a steer on what to do next? What’s going wrong here?

Consultants just don’t do research. For example, I have yet to see a single set of publications from any of the sourcing advisors examining the performance of the RPA solution vendors. There are a million best practice pieces, but nothing of actionable substance. Clients want substance, not just the fluff. Clients are shifting to soliciting help from firms which can do the work and have the proven knowledge to support it, which is why so many are resorting to analyst reports to figure stuff out.

The MBA bus can’t find its usual parking spot in the visitor’s parking lot. As the demand for expertise in areas such as complex operating models, understanding murky automation challenges and being able to design outcomes-focused models is reaching unprecedented proportions, it’s just not possible for the traditional gaggle of consultants to serve up the inexperienced kids with their Visio charts and park them in the basement for six months to come up with a plan. While most of these people are brilliant, many don’t really know what they are doing. For them, doing RPA and automation tool selection is just plain scary.

Enterprises need consultants with deep, relevant and up-to-date experience. This market calls for hands-on experienced practitioners, skilled in understanding modern solutions and real change issues, who are prepared to roll up their sleeves and live their clients’ pain to find the answers. Simply rebadging outsourcing deal negotiators as robotic or digital experts does not work – these guys need serious retraining if they are to stay relevant in the current market – it’s not like the old days where you could hide behind some fancy new acronyms, utter the phrase “digital disruption” in every sentence, and promise “innovation”. Noone wants promises – they want real business cases, with genuine milestones and measurable, proven impact. They also want people who have got their hands dirty with these emerging solutions and can articulate how they can align to their processes and business models. In short, you can’t get away with half the bullsh*t these days…

Service Providers are in direct competition these days when it comes to transformation support with automation, digital and AI. In the heyday of sourcing advisory, advisors and service providers fed off each other as advisors cultivated clients and brought business to service providers, and service providers returned the compliment when they had clients in need of independent advice. It was a perfect symbiotic relationship. Now that model is rapidly atrophying as these two entities increasingly find themselves now competing for the same dollar. Let’s makes no bones about it, advisors and service providers are now in direct competition for supporting clients with their transformation journeys. Most the service providers are now offering intermediary services to provide automation strategy, implementation and delivery to enterprises, catering to whatever technology tools and platforms the clients require. As you can plainly see above, many operations leaders are now getting more value from them than they are from their advisor relationships. Clients can call on Genpact, TCS and Wipro these days, as much as they can KPMG, EY and Deloitte when it comes to the new stuff.

While service providers are integrating upwards into advisory services, advisors are integrating down into annuity services. Most the advisors are now evolving themselves as service providers and annuity-based revenue models in areas such as cyber-security services, blockchain services, managed RPA services – and even payroll services in certain countries. KPMG even declared it was in the Workday managed services market.

However, we might be on the cusp of a whole new era of new digital operations advisory boutiques, equipped to help clients make sense of it all

What gives me hope that we haven’t just witnessed the demise of the sourcing consultant, is the emergence of several small, but highly practical, boutiques of mid-career process guys who are in serious demand – and some of them are scaling up at a breathtaking pace – and we’re seeing some serious hitters make the jump from established consultancies to lead these boutiques, such as David Poole and his excellent team at Symphony, Paul Donaldson who has just moved from leading ISG’s RPA practice to being the new CEO at Robiquity with a very compelling automation bootcamp, Mohit Sharma and his determined drive from Down Under with Mindfields, the brand new “Agilify” (not quite launched) that Lee Coulter will head up as a new initiative from healthcare giant Ascension Health, Jan Rapala’s NEEOPS, driving RPA advisory from central and eastern Europe, Christian Voigt’s compelling Roboyo business emanating from Germany, and Richard Jeffrey’s ActiveOps firm, which is driving Workware, a back office optimization solution with a strong alignment to RPA effectiveness and now expanding aggressively from the UK to the US market. I’ll stop there for now, but there is a significant influx of very smart, experienced operations experts branching out and taking advantage of a market where clients need hands-on real help – and need it fast.

The emerging advisory market is about hiring people with the capabilities to understand client outcomes and implement solutions using the right mix of new tech on the market. What’s more, most of these consultants are relishing working in a boutique environment – it just feels like the age of the boutique is coming back, and we will see several more of these spring us with the barriers to entry still pretty low. Only GenFour has got absorbed (by Accenture earlier this year), as a first-mover in RPA implementation, but I’d be surprised if many of these other boutiques really want to get swallowed by the mega-firms… most seem to be hell-bent on building up organically in this market.

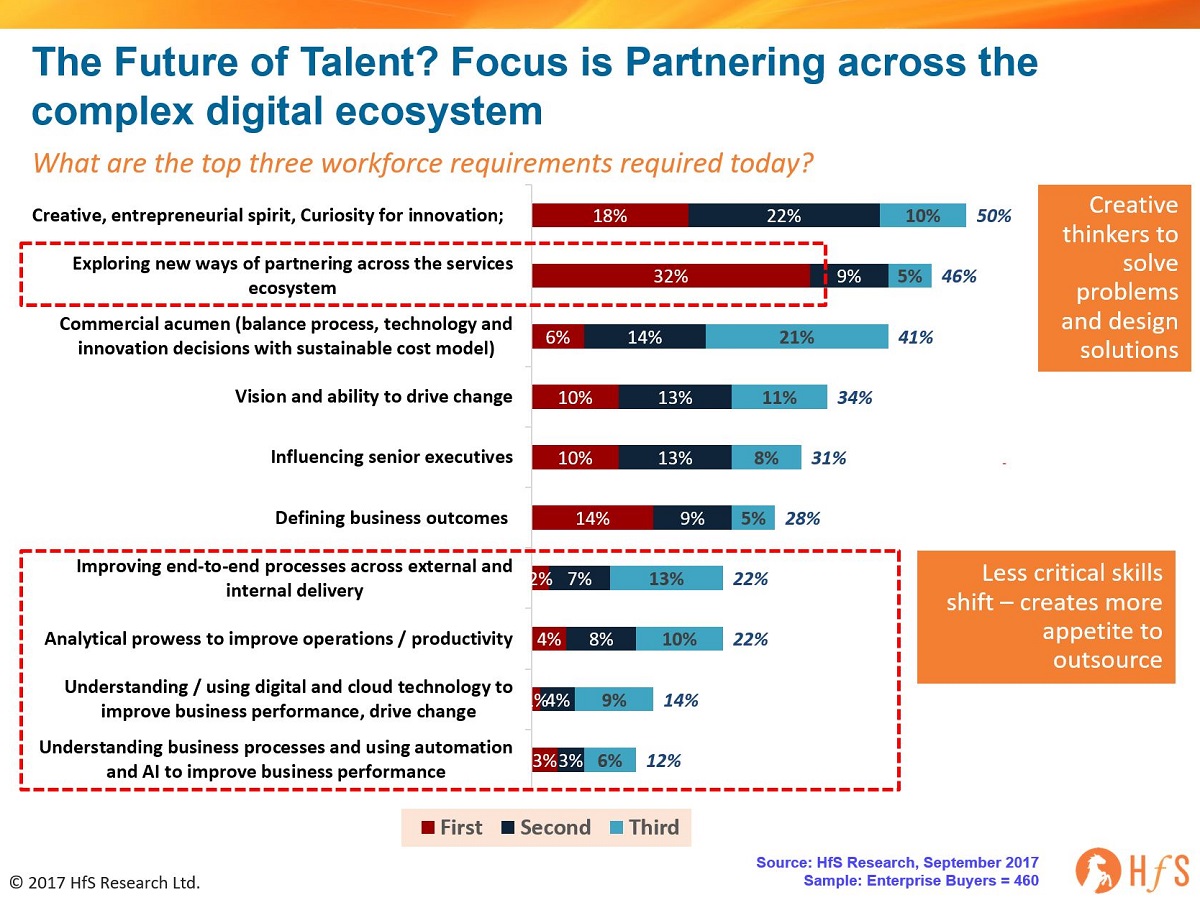

And there’s another reason why these emerging boutiques are so compelling… many have the emerging skills to support enterprises with their number one talent requirement – the ability to partner across these increasingly complex ecosystems of RPA, AI, and digital firms to help them:

While the traditional consulting firms have continued to bury themselves in supporting the “left-brained” areas of process delivery, digital tech etc., where clients really need help right now is understanding how to cement the right partnerships across the digital operations ecosystem to truly understand these change agents and devise the right plan to achieve their outcomes. Net-net, it’s not just about left-brain support these days, it’s about entrepreneurial, savvy, “right-brained” capabilities and nimble boutiques are able to mix up their teams with the talent clients really need to address the complexity.

The Bottom-Line: The digital operations train has already left the station and not all the consultants are on it

It’s not all doom-and-gloom in the management consulting firms, as KPMG’s Cliff Justice leads the firm’s AI strategy, with some promising key industry partnerships, most notably with IBM Watson, and Dave Brown’s SSO advisory is leading the industry with RPA transformation revenue; EY has jumped in aggressively with strong RPA deployments; ISG has held onto Chip Wagner, one of the first advisors to “get” RPA during his time running Alsbridge; Deloitte has developed its own brand of “process robotics” with some eye-opening projects, such as their work with NASA, and PwC is boasting some impressive work with the likes of Tesla, as it seeks to make up ground on the rest. The challenge is how to support clients with the experienced talent which actually understands how to implement this stuff in a way that is affordable.

However, the change upon us is seismic and we need advisors which can surf the wave of change agents forming the new Digital Operations industry:

In short, the worlds of software, business operations and services have always been chasms apart – different mindsets, vernaculars, conversations, ideas of what constitutes value – and vastly different cultures. Software people never understood the operations folks and vice versa – each thought they were top of the corporate food chain.

However, the past couple of years have seen the coming together of these diverse groups of people to rethink completely how we run global operations in this robotically digital era (or whatever we want to call this curious period of time in which we exist). What’s uniting this array of industry players is the fact that we’re all now in the business of addressing clients’ desired business outcomes, as opposed to simply selling them some product or service with some vague ROI attached to it. And those desired outcomes are unifying around the fact that nearly all clients are under immense pressure to become digital businesses with touchless customer interactions, supported by digital operations to make it all possible.

One thing is abundantly clear: the outsourcing phenomenon which has gripped the Global 2000 over the past decade is making way for a genuine industry in which we all play a part – an industry where we have no choice but to develop learning programs, sustainable business strategies and make real, actual investments in order to survive. And what’s most fascinating are the new conversations that have rapidly emerged to bridge this divide between the technologists and the business operators.

Suddenly, we’re talking about business logic, about datasets, about redesigning processes with genuine business outcomes in mind. We’re talking about deep learning AI systems that store what has been learned in the past, take notes of how variables and results have changed under different scenarios and then make decisions based on that.

The narrative has radically changed and the focus is now firmly on bringing together all the components that can escort us to this promised land of Digital Operations. And the firms to take us there might just not be the ones who got us here in the first place…