With our governments going broke and looking to go even broker, here is my simple wish-list to fix our endemic societal issues, and recoup some much needed tax income, so we can start dreaming about things like improving disastrous education and health services…

Trump is gone …and a new political party emerges in the US that isn’t controlled by greedy corporations and corruptible misogynist dinosaurs. The American voters go back to voting on policies, not stereotypes and hatred. Wouldn’t that just be so awesome? Is it illegal to dream these days?

Britain finally gives up on Brexit, realizing that changing the color of passports from red to blue doesn’t make up for trashing the country’s economic future and hurtling it back into the 1970s. Please can we all just admit there is not one single good thing about Brexit for any living being, so we can just consign the whole thing to the time-capsule of bad ideas, along with communism, dodgeball and the George Foreman grill. Bad ideas are OK, as long as we admit later they were bad ideas…

Political leaders finally realize that smartphone addiction is the worst disease to affect society since cigarettes and booze. In fact, it’s worse – they could fund entire health, military and education programs taxing booze and ciggies, but with smartphones, all the money is now getting sucked offshore somewhere, and into Mark Zuckerberg’s and Jeff Bezo’s bank accounts.

Re-open pubs and bad discos. Back in the pre-smartphone era, our social world was centered on bad pubs and even worse dance floors. Yes, we had to get drunk and make idiots out of ourselves to meet people and get married… now it’s just swipe left or right, a few photos and you’re all done. Where did all the “fun” go? Can’t governments declare what’s left of our pubs as places of national heritage and conserve what we have left of life before Instagram? Is the joy of youth consigned to sharing bad selfies and playing online video games alone in their bedrooms?

Tax gym memberships. What was wrong with a few extra pounds and a beer gut? Now, if you don’t have a perfect six-pack on your chest, rather than in your fridge, you’re not exacty making friends like you used to… where did all the fun go? Not sure about you, but I don’t have much energy left for socializing after 45 mins on the treadmill and benchpressing 130lbs, so I might as well donate the $20 I should be spending on booze to the government to fund the reopening of classic pubs.

Tax anyone trying to buy Bitcoin. Just because.

Tax vendors double for sponsoring every ropy conference under the sun. They’re wasting their money in any case, so why not make them do something useful with it?

Place income tax on robots. This will end the inane conversation about “digital” labor, as everyone goes out of their way to call it something else, like workflow efficiency… which is what it really always was, right?

Tax vendors for using the term “digital” in their marketing. Why not make some use out of a meaningless overused term…

Tax #fakenews. Forget the detritus of Obamacare, this will fund a whole new health system, right?

Tax bloggers for writing opinionated blogs, because they think they can. Make them realize there’s no such thing as free opinion these days…

The Bottom-line: As we near the end of a ridiculous year, we can all dream, can’t we?

On behalf of the HfS analyst team and global community, I am delighted to announce our flagship FORA summit taking place this coming March 7th and 8th at Convene, Times Square, Manhattan, New York City.

This will span the entire two days with the theme “Learning to Change” dominating the conversation. The tech is here and is being proven, but are we really, truly ready to disrupt our underlying corporate DNA to exploit it to its full potential? Can we really change how we operate, think, collaborate and focus to embrace the new wave of data-driven transformation that is engulfing us?

Key Topics up for Debate:

Intelligent Automation in Practice (not theory); Blockchain demystified; Emerging Sourcing Models and the Digital OneOffice; The Emergence of the Chief Data Officer; Making Change Management actually work.

Key Speakers and Panelists:

Tim Leberecht (Author of the Business Romantic); Tony Saldanha (VP, IT and GBS P&G); Phil Fersht (CEO, HfS Research); Mike Salvino (Pioneer behind Accenture Operations and a key investment partner for Carrick Capital); Larry Carin, Professor of Computer Engineering, Duke University (More to follow….

CEOs of the leading Intelligent Automation software firms and IT/BPM service providers

Key enterprise leaders managing data, automation, global business services and operations initiatives

HfS analysts spanning emerging technologies, industries and sourcing solutions.

Why FORA is Special:

The worlds of software providers, business operations leaders, and services providers have always been chasms apart – different mindsets, vernaculars, conversations, ideas of what constitutes value – and vastly different cultures. At FORA, we are bringing together these diverse groups of people to rethink completely how we run global operations in this robotically digital era, to debate the challenges and opportunities posed by automation, AI, analytics, blockchain, global talent on our business operations and our careers.

If you have further questions regarding FORA, how you can attend, sponsor, speak, or just make suggestions, please drop us a note at [email protected]

When the statement “It’s just like BPR from twenty years ago, but with tech that actually works” rang out at the recent London FORA Summit, the nods around the room were palpable.

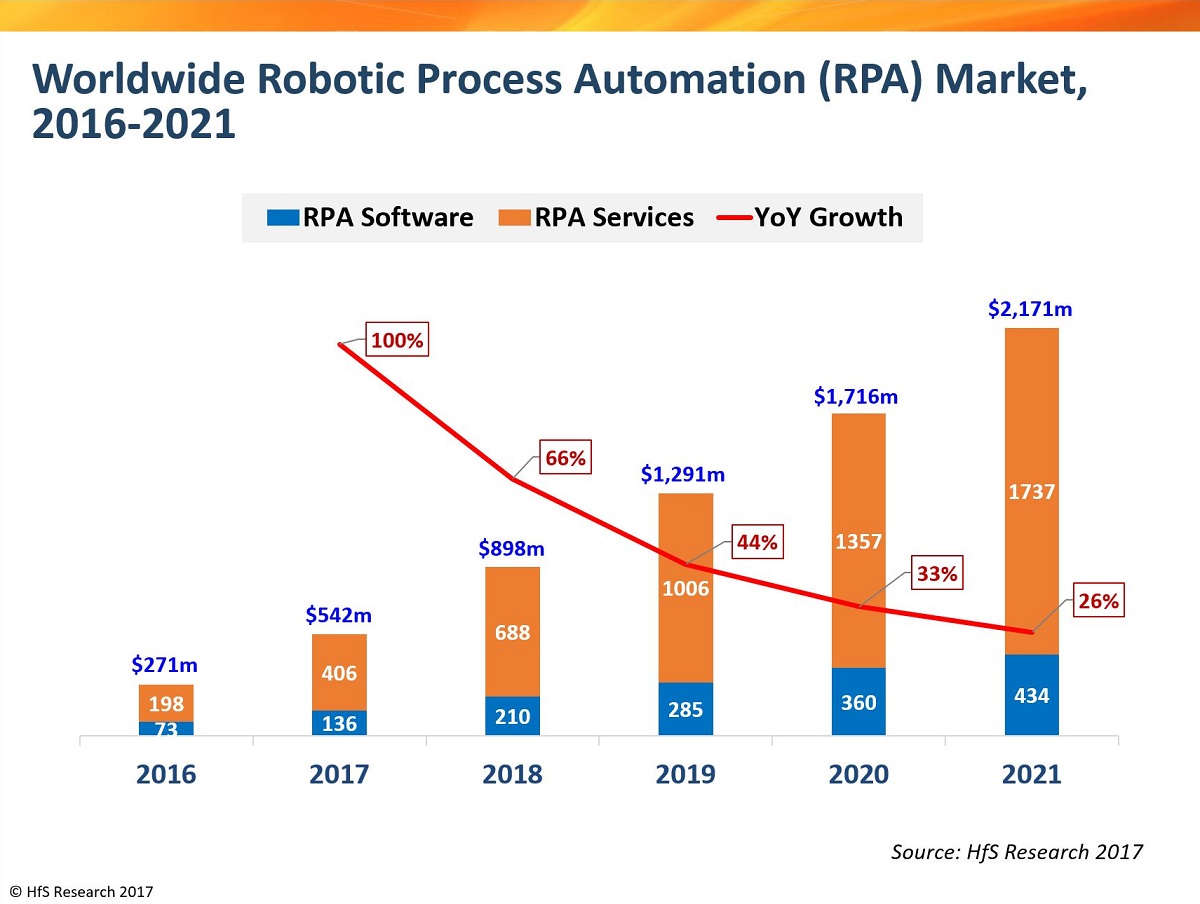

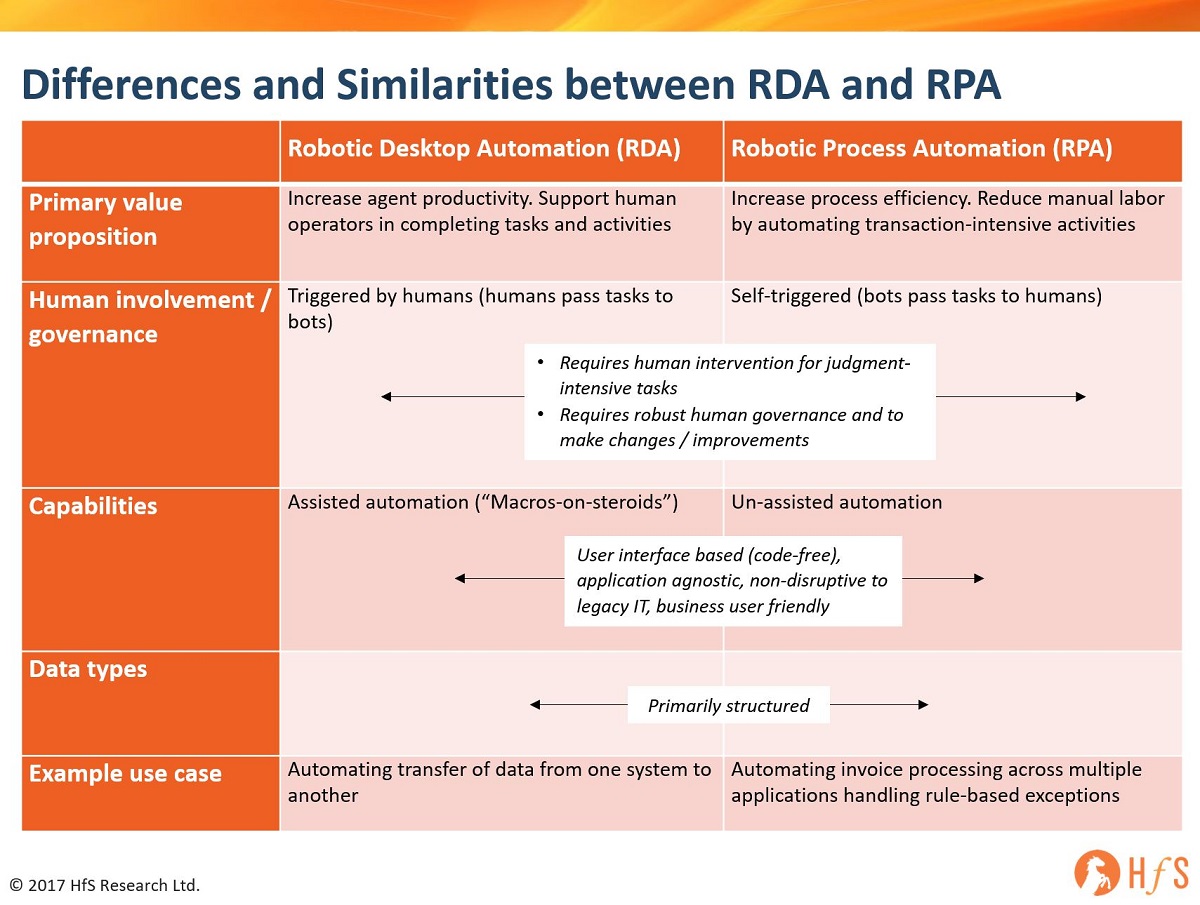

2017 has undoubtedly been the break-out year for enterprise robotics software. We witnessed a whole new industry emerge around robotic technologies that can stitch together workflows, processes, applications and desktop interfaces to provide a genuine transformation of the digital underbelly for so many enterprises, many of whom have suffered for decades from inefficient manual workarounds and spaghetti code clogging up their ability to access data and run their businesses properly. Today, the emerging solutions available on the market do not load the enterprise transformation blunderbuss with silver bullets, but they do provide a starting point to improve fundamentally the data underbelly of an organization. And, for so many organizations, they are turning to robotics software RPA (Robotic Process Automation) and RDA (Robotic Desktop Automation) as the starting point.

Robotic Process Automation

The global market for RPA Software and Services will reach $898 million in 2018 and is expected to grow to $2.2 billion by 2021 at a compound annual growth rate of 54%.

RPA Definition:

Example use-case: automating invoice processing across multiple business applications handling rule-based exceptions. RPA is different from traditional automation software as it is inherently capable of recognizing and adapting to deviations in data or exceptions when confronted by large volumes of data. In effect, it can be intelligently trained to analyze large amounts of data from software processes and translate them to triggers for new actions, responses, and communication with other systems. RPA describes a software development toolkit that allows non-engineers to quickly create software robots (known commonly as “bots”) to automate rules-driven business processes. At the core, an RPA system imitates human interventions that interact with internal IT systems. It is a non-invasive application that requires minimum integration with the existing IT setup; delivering productivity by replacing human effort to complete the task. Any company which has labor-intensive processes, where people are performing high-volume, highly transactional process functions, will boost their capabilities and save money and time with robotic process automation. Much fr RPA is self-triggered (bots pass tasks to humans), but requires human intervention for judgment-intensive tasks and robust human governance and to make changes / improvements.

Similarly, RPA offers enough advantage to companies which operate with very few people or shortage of labor. Both situations offer a welcome opportunity to save on cost as well as streamline the resource allocation by deploying automation. The direct services market includes implementation and consulting services focused on building RPA capabilities within an organization. It does not include wider operational services like BPO, which may include RPA becoming increasingly embedded in its delivery.

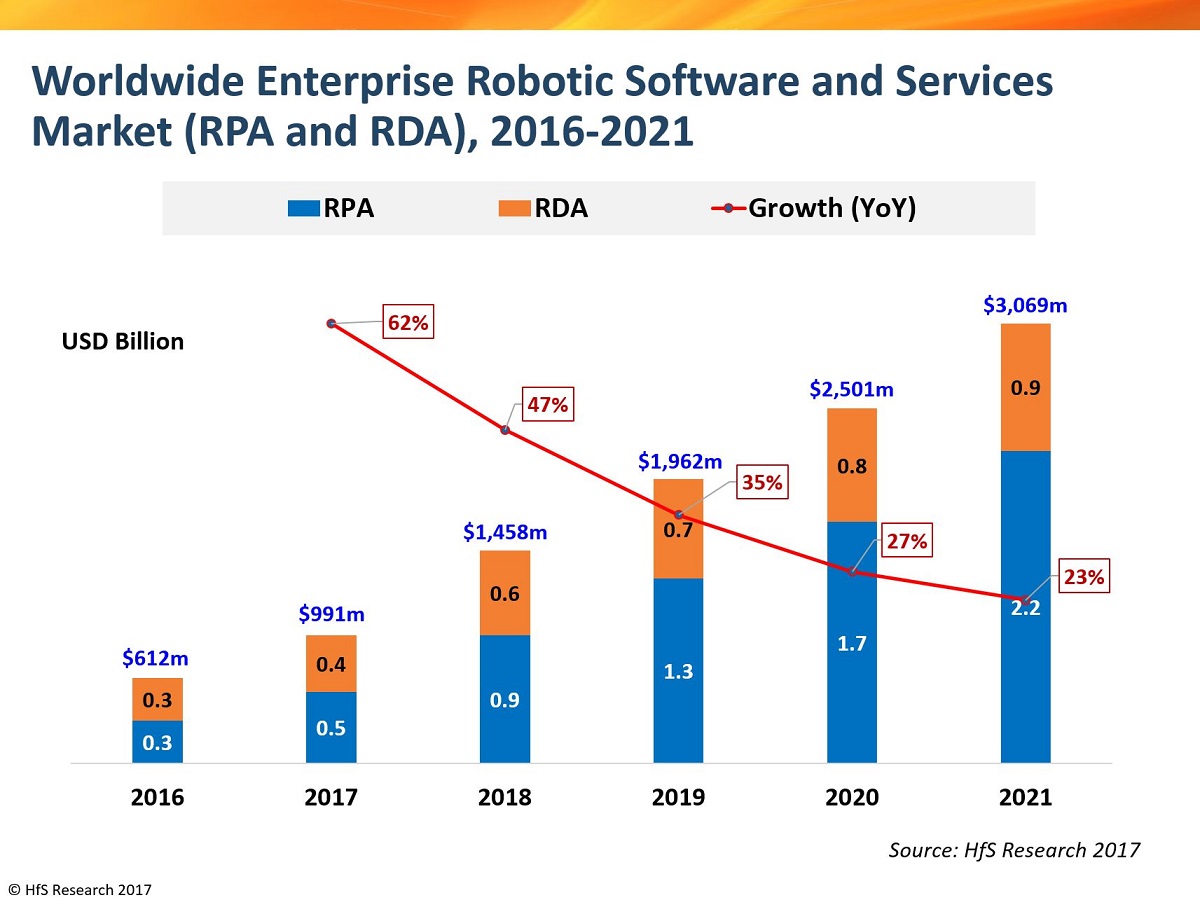

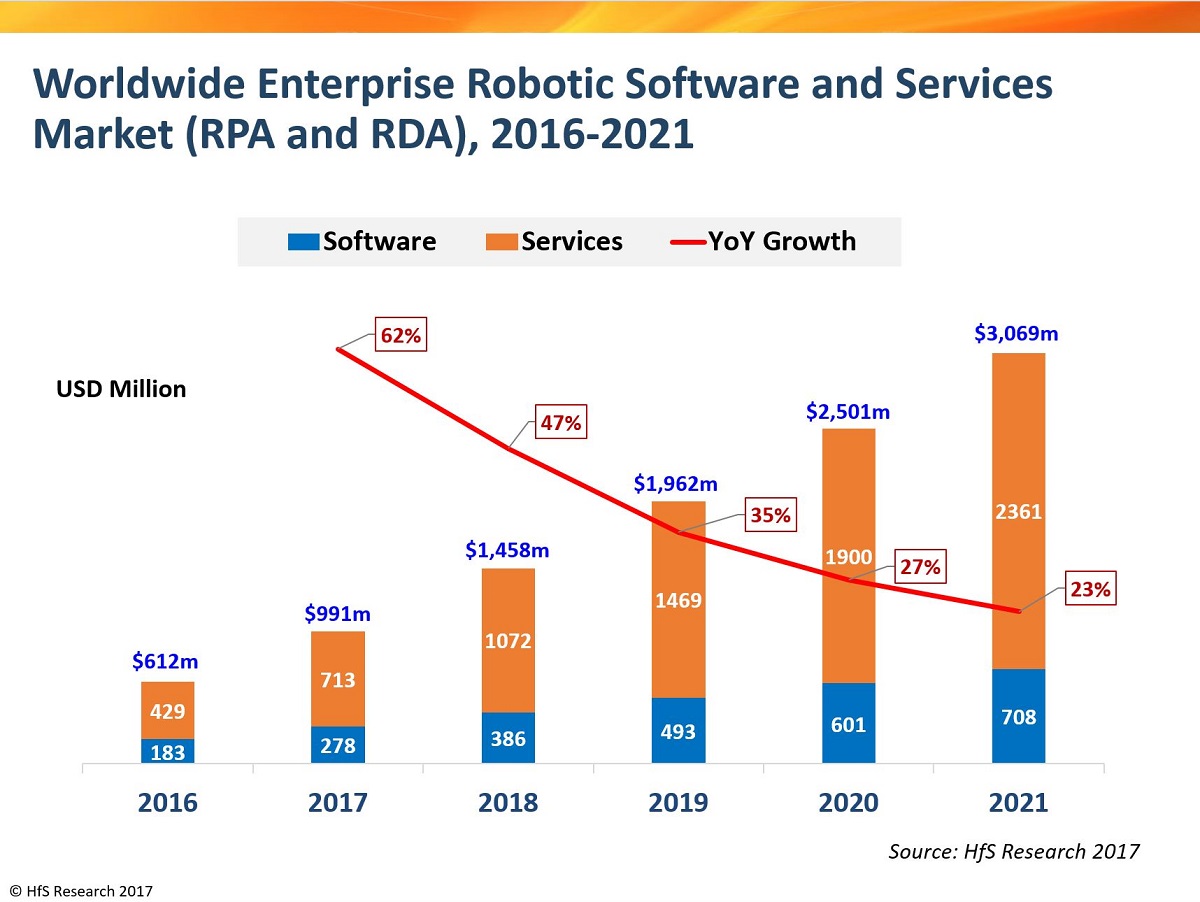

Robotic Desktop Automation

In addition to RPA, the other software toolset which comprises the emergence of enterprise robotics software is termed RDA (Robotic Desktop Automation). Together with RPA, RDA will help drive the market for enterprise robotic software towards $1.5bn in software and services expenditure in 2018 (with close to three-quarters tied to the services element of strategy, design, transformation and implementation of enterprise robotics). HfS’ new estimates are for the total enterprise robotics software and services market to surpass $3 billion by 2021 as a compound growth rate of 39%.

RDA Definition:

Example use-case: automating transfer of data from one system to another. RDA is essentially surface automation, where desktop screens (whether desktop-based, web-based, cloud-based) are “scraped”, scripted and re-programmed to create the automation of data across systems. A well-designed RDA solution can automate workflows on several levels, specifically: application layer; storage layer; OS layer and network layer. Workflow automation on these layers requires equally specific technologies but provides advantages of efficiency, reliability, performance and responsiveness. Much of this automation needs to be attended by humans as the automation is triggered by humans (humans pass tasks to bots), as data inputs are not always predictable or uniform, but adaptation of smart Machine Learning techniques can reduce the amount of human attendance over time and improve the intelligence of these automated processes. Similarly to RPA, RDA requires human intervention for judgment-intensive tasks and robust human governance and to make changes / improvements:

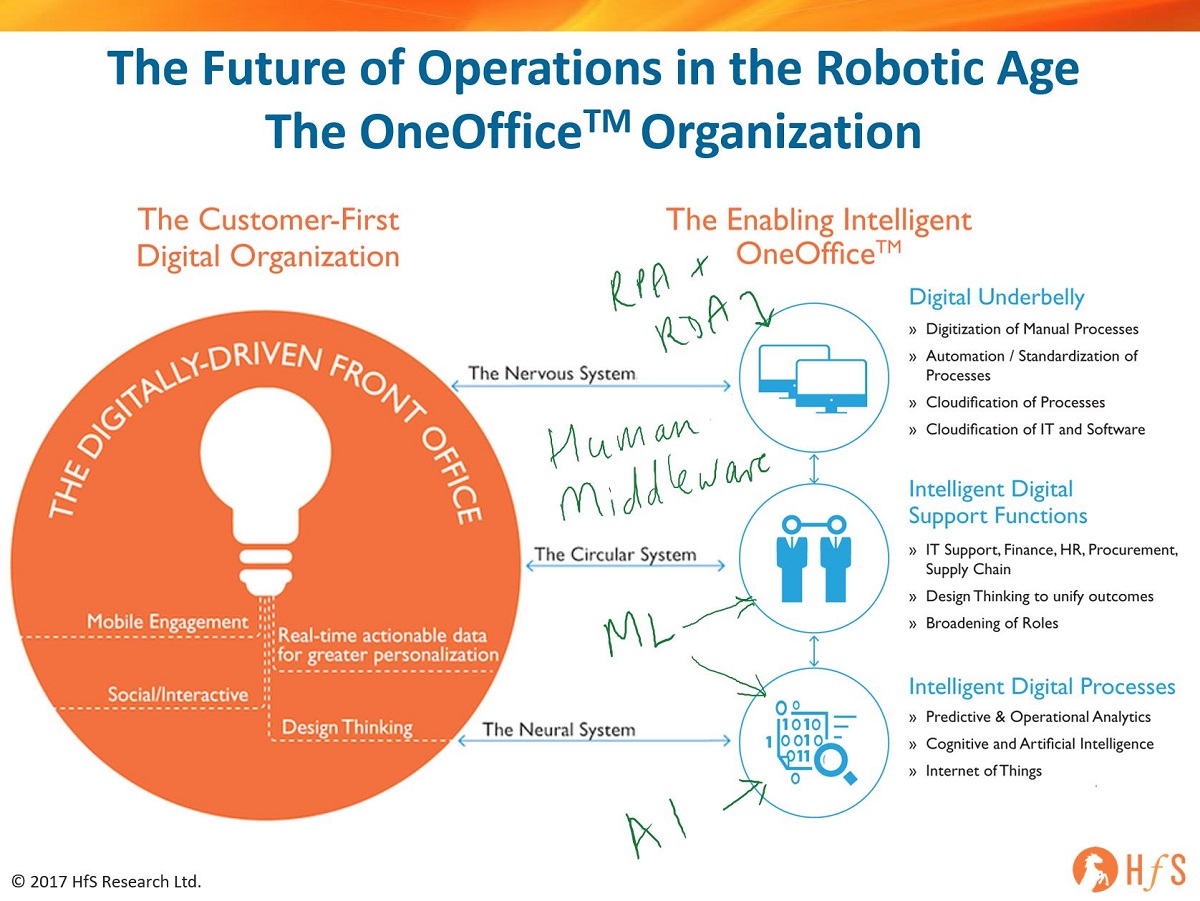

The Bottom-Line: Automation and AI have a significant part to play in engineering a touchless and intelligent OneOffice

However which way we spin “digital”, the name of the game is about enterprises responding to customer needs as and when they occur, and these customers are increasingly wanting to interact with companies without physical interaction. This means manual interventions must be eliminated, data sets converged and process chains broadened and digitized to cater for the customer. This means entire supply chains need to be designed to meet these outcomes and engage with all the stakeholders to service customers seamlessly and effectively. There is no silver bullet to achieve this, but there is emerging technology available to design processes faster, cheaper and smarter with desired outcomes in mind. The concept was pretty much the same with business process reengineering two+ decades ago, but the difference today is we have emerging tech available to do the real data engineering that is necessary:

In short, every siloed dataset restricts the analytical insight that makes process owners strategic contributors to the business. You can’t create value – or transform a business operation – without converged, real-time data. Digitally-driven organizations must create a Digital Underbelly to support the front office by automating manual processes, digitizing manual documents to create converged datasets, and embracing the cloud in a way that enables genuine scalability and security for a digital organization. Organizations simply cannot be effective with a digital strategy without automating processes intelligently – forget all the hype around robotics and jobs going away, this is about making processes run digitally so smart organizations can grow their digital businesses and create new work and opportunities. This is where RPA and RDA adds most value today… however, as more processes become digitized, the more value we can glean from cognitive applications that feed off data patterns to help orchestrate more intelligent, broader process chains that link the front to the back office. In our view, as these solutions mature, we’ll see a real convergence of analytics, RPA and cognitive solutions as intelligent data orchestration becomes the true lifeblood – and currency – for organizations.

Do take some time to read the HfS Trifecta to understand the real enmeshing of automation, analytics and AI.

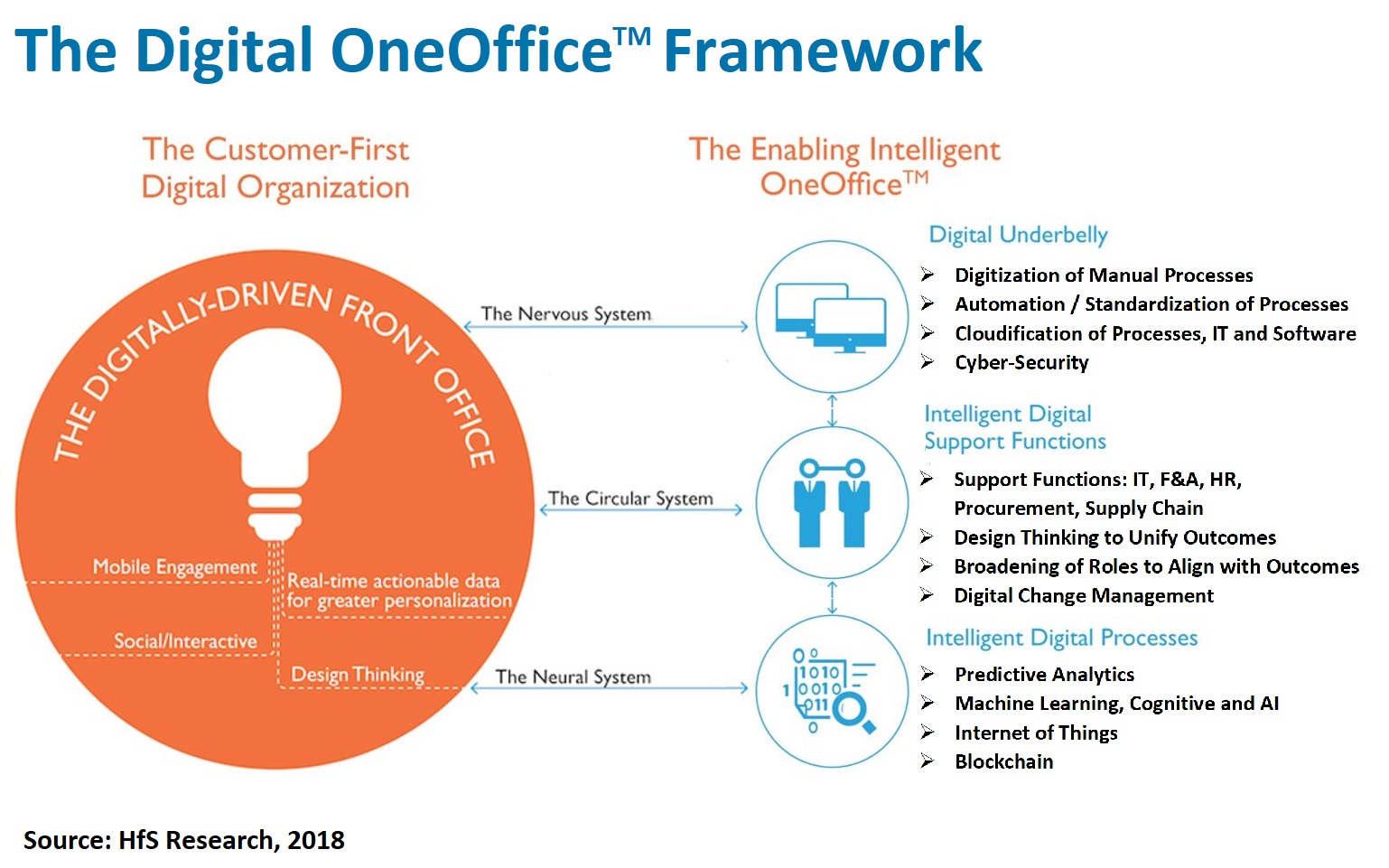

What we love about the Digital OneOffice™ is the simple fact it not only defines “digital”, but it also provides a meaningful framework, comprising of five fundamentals, that must come together to create a real-time flow of data across customers, partners and employees:

Fundamental 1) – Fostering genuine Digital Customer, Partner and Employee Engagement

A genuine “digital” organization has the ability to take all the cool social, mobile and interactive tech we use in our personal lives and create that experience for all the people in its environment – its employees, customers, and partners – and empower them to interact with each other seamlessly, and in real-time.

The outcome is all about creating, supporting and sustaining an immersive customer experience, where all touchpoints across an organization are tied to serving the customer as effortlessly and seamlessly as possible (and often not necessitating any actual human to human interaction). These “immersive” customer experiences are about leveraging these omnichannels (typically mobile, social, interactive technologies) and creating meaningful analytics from these converged datasets that make this real-time digital experience happen for the organization and its customers, its employees and its partners, right up and down the supply chain. The OneOfficeorganization needs a support function to service those customers, get its products/services to market when they want them, manage the financial metrics, understand their needs and future demands and make sure it has the talent which truly understands how to meet the desired outcomes of their work.

Fundamental 2) – Embedding Design Thinking Techniques to achieve Continuous Digital Outcomes

Design Thinking offers an approach for a diverse group of people to work together to identify and articulate a common problem, brainstorm ideas for addressing it, quickly prototype/wireframe/storyboard and test it, and continue to iterate on the idea as it takes shape into a proposed solution. A Design Thinking led approach to designing a Digital OneOffice framework moves the focus of the operations executive and service provider partner away from the process itself, and the internal, “what’s wrong inside of what we do” to “what do we actually want to achieve” (the business outcome), and what do we want people to feel and do naturally that will lead to further engagement and new—and different—results.

At HfS, we are finding that Design Thinking is actually changing the way many clients and service providers work, that there is a real complement between designers, consultants, engineers, and service delivery as organizations seek to bring the front, middle and back offices closer together to achieve common outcomes. Moreover, it’s vital that Design Thinking is firmly embedded as the method for ongoing engagement across all organizational stakeholders, as outcomes constantly evolve as markets evolve and business needs change.

Fundamental 3) – Building a Scaleable Digital Underbelly that Automates, Digitizes, Cloudifies and Secures

Every siloed dataset restricts the analytics insight that makes process owners strategic contributors to the business. You can’t create value or transform a business operation without converged, real-time data. Digitally-driven organizations must create a Digital Underbelly to support the front office by automating manual processes, digitizing manual documents to create converged datasets, and embraces the cloud in a way that enables genuine scalability and security for a digital organization. Organizations simply cannot be effective with a digital strategy without automating processes intelligently – forget all the hype around robotics and jobs going away, this is about making processes run digitally so smart organizations can grow their digital businesses and create new work and opportunities. This is akin to a “central nervous system” that incepts and processes all the elements necessary to make the organization function.

Fundamental 4) – Achieving an Intelligent Digital Support Function without Hierarchies and Silos

Enterprises need their support functions such as IT, finance, HR and supply chain, aligned with supporting the customer experience, as opposed to operating in a “vacuum”. We are terming this ”Intelligent Digital Support,” where broader roles are created and human performance is aligned with the achievement of common business outcomes. With the Digital OneOffice, the focus needs to shift towards creating a work culture where individuals are encouraged to spend more time interpreting data, understanding the needs of the front end of the business and ensuring the support functions keep pace with the front office. This is especially the case in industries that are more dependent than ever on real-time data, using multiple channels to reach their customers and being able to think out-of-the-box to get ahead of disruptive business models.

Progressive OneOffice enterprises prefer flat structures, where staff naturally collaborate in autonomous, cross-functional teams motivated by shared outcomes. They look towards much more dynamic management, where managers and staff constantly interact to fine-tune performance against evolving outcomes and manage diverse workforces across global cultures.

Fundamental 5) – Establishing Intelligent, Cognitive Processes that Promote Predictive Decision Making

The Digital OneOffice is not about collecting and archiving historical data simply to discover what went wrong, it’s about being able to predict when things will go wrong and devising smart strategies to get ahead of them. The Digital OneOffice is about embedding smart cognitive applications into process chains and workflows, it’s about learning from mistakes and new experiences along the way. This is the “organization neural system”. Cognitive technologies, advanced analytics and automation help create the capability necessary to operate in digital environments by automating and extracting the data needed real-time to respond to markets, support critical decisions and stay ahead of the game.

The Bottom Line: The secret sauce of the Digital OneOffice is the sum of the Five Fundamentals as one integrated experience, not merely the quality of individual fundamentals themselves

When we conducted the Digital OneOffice Premier League earlier this year, we focused on the ability of service providers to deliver each fundamental, and the winners were those who scored highest as an aggregate across the five. When we re-run this in the future, the Digital OneOffice framework should be mature enough to evaluate outcomes based on the ability of providers and their clients to create the most effective real-time digital experience, by managing the five fundamentals as one integrated organization unit, where teams function autonomously across front, middle and back office functions and processes to promote real-time data flows and rapid decision making, based on meeting defined outcomes.

And front, middle and back offices will cease to exist, as they will be, simply, OneOffice.

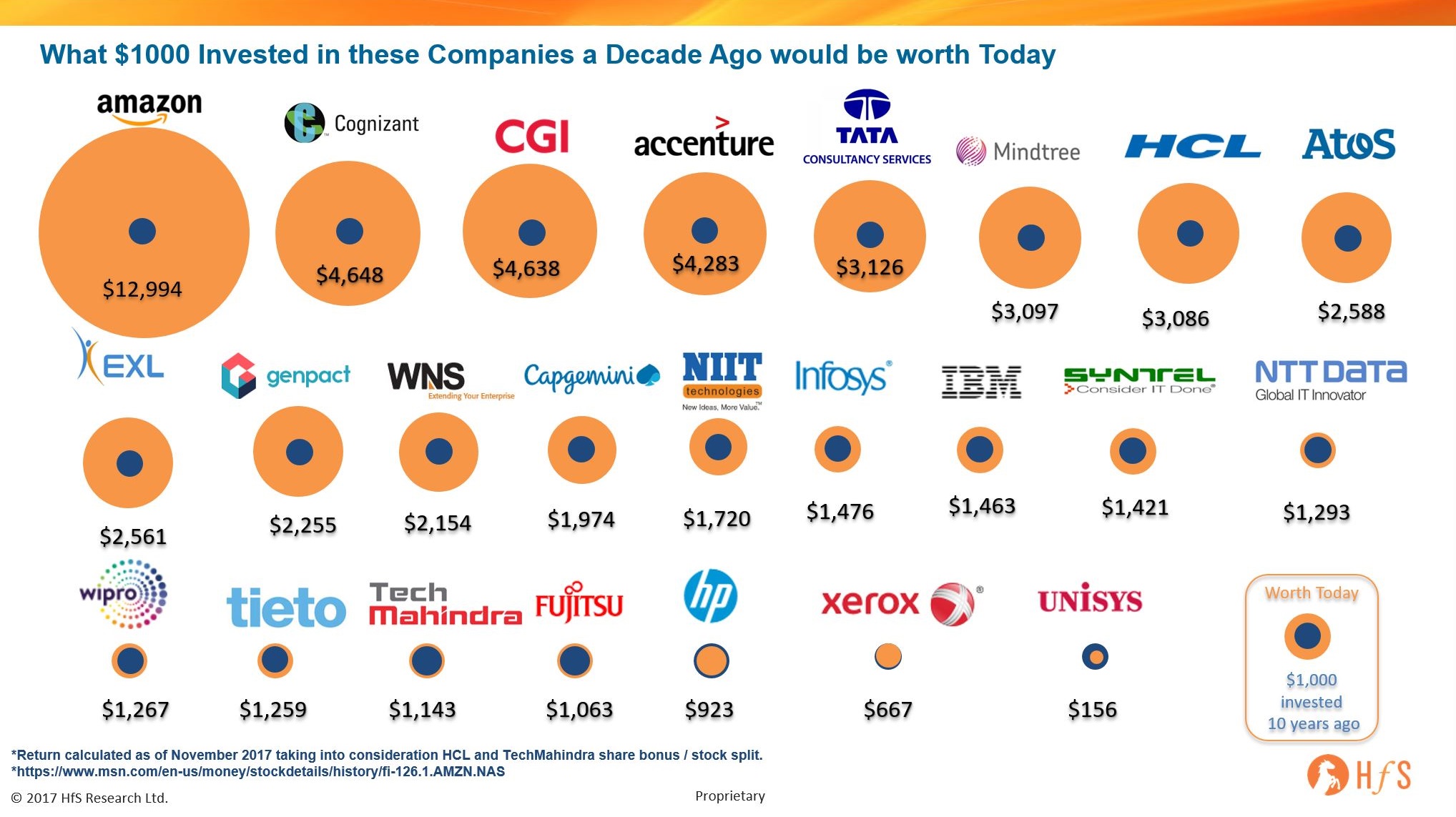

As a wise man once said: “It has been a mistake living my life in the past. One cannot ride a horse backwards and still hold its reins.” Well, if you’d listened to this horse, you may have turned a pretty profit =)

Kudos to HfS analyst Martin Gabriel for a very interesting analysis of how rich (or poor) we just could have been:

Terrific discussion from the FORA leadership panel featuring (from left to right) Mihir Shukla, Automation Anywhere; Dawn Tiura, SIG; Jesus Mantas, IBM; Cliff Justice, KPMG; Leslie Willcocks, London School of Economics; Mohit Joshi, Infosys and Ahmed Mazhari, Genpact.

Over three years ago, the Infosys board made the brave decision to look outside of its organization to bring in an “outsider” to transform its business and ready itself for whatever wave of disruption was coming to challenge a services model that still makes ~20% profit margins and grows ~5% a year. Yes, they appointed Vishal Sikka, and we all know about the ensuing soap opera that followed…

The decision to look outside was made in 2014, and that hasn’t changed

Hindsight is a terrific practice to follow, if all you really like to do is chew on historical occurrences to learn for the future. However, in the case of Infosys, the only real lesson to be learned from the whole Vishal saga is the firm needs a leader who understands how to grow, divest, acquire and lead a technology services and consulting business. Vishal provided the dreams, the style, technical prowess and the cultural impact… what he failed to deliver was being able to apply these skills effectively to a traditional services business.

Vishal was a software guy and that is the world he lived in – building very expensive platforms and hiring very expensive Californian executives to run them. Having said all that, Vishal did drive a huge amount of change, and most of it was positive – the only major negative was the fact he departed the firm, and everything he contributed left the firm in a state of paralysis. The only saving grace for Infy has been the confused state of the services industry in 2017, where most of Infy’s competitors have been too busy chugging down the Digital Kool-Aid trying to come across as a facade of flashy vernacular, rather than staying true to the secret sauce that made them great in the first place: driving out operating costs and providing innovations… and all at the same time.

The role of the services CEO is to steer the organization away from outsourcing and towards partnering

Another change to the world of Indian-heritage service providers, is the fact that most clients really don’t care all that much these days if the CEO changes – five years ago, they would make a big deal out of it and used it as leverage to change provider, or carve out a further discount for themselves. Today, they buy a service and want it delivered with minimal disruption – noone wants to rock the boat and create a crisis out of nothing. Will IBM customers flock to Accenture if Ginni left? Of course not. The CEO sets the tone and the strategy, while rest of the firms gets on with servicing the clients. What’s more, differentiation between services firms these days is much more subtle – it’s not all about the big vision and fancy speeches… it’s about being able to execute at competitive price points and commit to helping clients achieve jointly defined business outcomes. Winning in today’s services market is about being much more than outsourcing, it’s about clients working with providers as extensions of themselves… as genuine partners in business and technology.

The leader needs to make sure the company is set up with the right investments, people, culture and global resources to achieve this. Clearly, the Infosys board has felt for some years now it needs to bring in an outsider to get that balance right… there are just too many sub-companies, industry units, conflicting strategies and decades of politics to trust an insider with this massive task. Having someone who hasn’t been sucked into this internal quagmire – and can drive change with a little distance from the intense (and proud) history – is the right way to go. Again, this is a brave decision.

Salil Parekh: a pragmatic and sensible choice with the right experience-set

Salil Parekh ticks all the right boxes without upsetting the apple cart – it’s the external play, without the risky unknowns that a guy like Vishal brings. Firstly, Salil is not just a services man, but also a real consulting man. This is a sensible, pragmatic move that will help build and grow Infosys’ higher end consulting business. Salil has lived through two successful mergers – EY and Capgemini in the 2000’s, and more recently the Capgemini / IGATE merger, where there was very little client overlap and the two firms really complimented each other. Infosys has held back from opening the $6bn warchest – a lot of this was because they didn’t have the right guy at the helm whom the board trusted to make the biggest decisions that are still facing the firm: making the higher end consultative plays with the right acquisitions; making the right investments into its automation and AI capabilities; and positioning the firm as a true innovative and trusted partner in an uncertain world being ravaged by the seismic impact of Brexit, political instability and disruptive business models fuelled by digital tech and blockchain.

Yes, these are massive challenges, but the services winners of the last three decades have thrived on change, disruption, and uncertainty, which is exactly where the Infosys of 2018 and beyond needs to focus. Salil also has a career filled with cultural affinity across American, European and Indian business, which is so essential in today’s environment. Keeping Pravin Rao as COO helps maintain the best elements of Infy’s work ethic and culture, but Nilekani clearly wanted some new blood to inject a new direction for the firm. This is also a clear shot across the bow at Capgemini, a firm which Infosys can go after aggressively in the market.

So here’s a quick checklist of all the challenges and opportunities that must be urgently addressed

Immediate challenges:

Put forward an Infosys Brexit plan to support clients as panic starts to set in. With such a strong European presence, Brexit could be the biggest opportunity yet for Infosys to support global business in distress

Decide quickly which of Vishal Sikka’s initiatives to keep investing in, namely the Nia platform, the Design Thinking strategy;

Keep driving forward its localization investments, especially as DevOps increases the demand for immediate access to onsite resources;

Decide how much emphasis to put on EdgeVerve;

Evaluate the success and effectiveness of its BPO business and determine where to take that business;

Determine Infosys’ approach to “Digital” – is it worth playing the mimicry game, or is there a window to attack the market with a different approach? A lot of building blocks are there, but it is not as articulated and joined up, when compared to Accenture, Cognizant and Wipro;

Definitively nail-down Infosys’ approach to automation and AI (including AssistEdge and Nia) and set appropriate investment levels to make it work;

Assess current leadership team;

Identify its competitive set and determine who is wants to emulate and to compete with. Is Infy still the “Indian Accenture”, or time for a renewed focus?

Evaluate the recent investments in Californian talent and infrastructure.

Medium-term challenges:

Align the strengths of aligning Infosys’ DNA and culture with the future strategy and direction of the firm (without upsetting the Founders);

Ensure the right investments are made across industries based on Infosys’ strengths;

Continue to globalize the firm across North America, Europe and India;

Make significant investments in consulting, either through a major acquisition or a series of smaller tuck-in additions.

The Bottom-line: Infosys can correct-course, given the current market turmoil, but cannot afford another mess

If there is one saving grace that came out of Infosys’ annus horribilis of 2017: it’s the fact that everyone cares about them – and the firm is still chugging along as well as the rest of its competitive set. Just spend time with its executives and you’ll quickly see how proud its people are of their firm and their brand – you don’t get the same arrogance and complacency that some of its competitors give off. The firm has a big chance to make a big move in 2018 with the right man at the helm, but Salil must move swiftly and definitively – and keep these Founders in line – or we’ll just see history repeat itself… a fate not worth contemplating.

There is no doubt that several of its competitors have closed the gap on them (and some, arguably, are slightly ahead), but Infosys still stands proud and has a rare chance to learn from its own – and everyone else’s – mistakes. IT services is a savage business, but Infosys’ standing and financial resilience have gifted it a second chance to rise again.