Yes, people, as we inch towards the dreaded singularity, we will continue to be bored silly with arrogant diatribes describing how “humans can stay relevant”.

Do we really need to hear this daily splurge of pontifications from business leaders in Davos about reskilling the workforce, without any real practical advice on what that reskilling is? I would argue this is more about culture and attitude, than training students to learn new programming languages and data analyst skills. The latter will come naturally as the needs of the workplace change, my view is that it’s the former which poses the real challenge: how can we enlighten people to change their working attitudes to make them much more valuable and irreplaceable to their employers? Anyone can fix a line of code within hours, or slam in some new software, it’s what you actually do with the tech that really counts.

It’s what you do when your boss isn’t looking, that makes you less predictable and more valuable

It’s not just about performing predictable tasks, it’s also about helping your firm devise new ways of doing things – that is the magic that makes staff valued. The truth is the singularity is a gimmick to jazz up advances with intelligent computing capability; the reality is the present and the future of the workplace are converging before our very eyes, and the survival of the digital worker depends on our ability to be looking constantly at where our firms are going, and being part of that journey.

The future of every type of ambitious commercial business, whether it’s a factory making products, a bank loaning money, an IT support shop helping users, a grocery store selling goods, a law firm prepping available information for its client cases, an analyst firm producing insight… is to perform its business operations with the optimum balance of talent, so it can maximise its immediate profits, with an eye on the future to stay ahead of the competition. As soon as someone’s output is predictable, taking inputs from various sources to produce outputs, you can start to figure out how to program software and machines to perform said tasks – and computers will always be cheaper than humans, once they are functional and can do the job. So our goal has to be about furthering our abilities, not only to get the basics of our jobs done, but to immerse ourselves into helping our colleagues and bosses figure out the what next. Because if we only focus on the now, we are eventually going to render ourselves predictable and replaceable.

Xerox and Zume: Two ends of the comfort/innovation spectrum

However, not all businesses are ambitious – some just want to milk what they have, squeeze as much as they can out of their current product and then exit. Just look at Xerox – the firm developed a tremendous product for many years (and was the most patented and innovative workplace technology alongside the emergence of the IBM computer back in Don Draper time), which literally dominated a market in such a way that their brand became a verb. However, Xerox just couldn’t find a way to become something else as copying documents became a commodity practise, and recently took its final payday before becoming part of Fujifilm.

Maybe some firms and some boards just aren’t destined to do anything else, and those who made millions and retired off their stock can sip their martinis and congratulate themselves on their success (and luck). However, for every millionaire, there will be a thousand mid-career folks rendered practically unemployable with a legacy skillset servicing a legacy product. So often we see people clinging onto the past with their careers, when it’s abundantly clear their train has left the station. Good money today doesn’t always mean a healthy long-term decision, and there are so many people facing that predicament. What of the bank teller facing branch closures and their role being BPO-ed? Or the insurance inspector being replaced by flying drones with webcams? Or the call center agent being phased out for an intelligent chatbot? Or the investment analyst being replaced by smart algorithms? We can just go on and on and on… and there are so many more examples, such as the case of Zume pizza.

Zume, a typical Californian disruptive business, makes its pizzas with robots, and can deliver up to 200 at a time thanks to remotely controlled ovens inside their delivery trucks, their patented “Cooking en Route” system. It’s secret sauce is literally automation (not tomato purée) which speeds pizzas to market more cheaply, efficiently and at scale (and delivered freshly cooked ant hot). Instead, it can invest its profits in hiring creative people to think of clever occasions with which to personalize and sell pizzas (i.e. during The Superbowl and Game of Thrones). In short, tasks that are automatable such as rolling out the dough, adding on the sauce and toppings and placing the pizzas into and out of ovens are much more cost effective to use machine labor. And when predictable intelligence is needed, such as forecasting weather conditions and popular events can benefit from a machine learning algorithm, the supply chain mechanism can be astutely optimized to get products to hungry customers quickly and profitably as possible. Hence, the human skills are being pushed further and further up the creative value chain, such as designing a Philly cheese steak pizza for Eagles fans, or a lobster roll pizza for new England fans (OK I just made those up, but you get the picture).

If you are an employer looking for creative talent, would you rather hire a successful Xerox executive who’s kept that beast trundling along for the last couple of decades, or someone who’s been immersed in the exciting growth of Zume over the past 18 months? Hmmm…

The secret sauce to an ambitious business lies in energizing its culture and mindset to focus on the now and the next

As we have discussed, predictable is not the secret sauce – the secret sauce is what you do when no one is looking, the less obvious tasks that make you irreplaceable. The key is to immerse yourself into the personable side of the business to become part of how the company drives value. This means making your value less simple to put on a spreadsheet – successful companies are those that create a culture that is unique to them, where its people are engaging in an enthusiastic way to find new sources of value for their firm, while enjoying being part of that journey. People who love what they do and energize those around them are rarely fired.

In the case of Zume, once you have your intelligent pizza supply chain perfected, the human differentiator lies in marketing the product to drive the customer experience, which means having teams of smart people who love the product and work enthusiastically to come up with ideas to win in their marketplace. It’s the same analogy with many insurance firms, where the whole process of managing an insurance process and developing smart algorithms to predict risk are increasingly digitizing (with the help of outsourced support), and the human edge lies with insurance firms out-marketing and out-thinking each other to offer the customer something that is more appealing to them? Do we really care whether Geiko or Progressive insures our cars? Probably not, but we will buy with whoever targeted us most effectively and made it easiest to get the transaction done. Or it may be as simple as which TV commercial appealed to us to the most – the frog with the British cockney access or the friendly Flo who just seems to trustworthy and nice. The simple reality here is as routine tasks become automated and the data becomes increasingly predictable with the use of advanced analytics and machine learning, the human skill lies in establishing the culture of a firm and the creativity in connecting and engaging as impactfully as possible with a customer base which just wants to be served as quickly and touchlessly as possible. Do we really care about talking to a pizza order-taker or an insurance customer rep on the phone, when we can just order something on an iphone app? I bet we’d hardly care if a drone rang our doorbell with a piping hot pizza at out front door, as long as it tasted great and was delivered quickly. And you wouldn’t have to tip either =)

The Bottom-line: Future workplace success is as much about attitude as it is skillset, where we need to focus on this convergance of the present and the future

If I have to hear yet another “we need to fix the skills gap” diatribe from some plastic HR analyst I am going to become a Belgian trappist monk and brew very strong beer all day. But I think you already knew that… so hear are some takeaways:

Get out of your silo. Get to know your colleagues and get them excited about what you do. Even if your work areas don’t converge that much, how hard is it to give up some time to get to know who you’re working with, and exploring how you can help each other. While we are all becoming digitally lazy with our social interactions (and many other activities) we need to focus harder on our people relationships to energize those around us. So get back to having lunch with colleagues… call them up to air ideas. Don’t be unafraid to get people to explain what the hell it is they actually do (because they are likely clueless whay you do also…).

Get to know some useful tech. Whatever you do, where are cool apps to enhance your job, whether its collaborative apps and social software, graphics and content packages, data visualization and analytics tools, CRM tools, RPA/RDA/BPM and easy-to-use process configuration software… you don’t need a computer science degree anymore to use this stuff. If you mastered that beast called PowerPoint, you can certainly use some of the sexier tools in the market and… and evaluating them is almost always free. If you’re not using some form of new tech in your job, then something is going amiss… or you’re just too busy selling your next photocoper to care.

Get to know your firm’s business better. Your bosses should be driving themselves nuts trying to get one over the competition and come up with new ideas for disrupting your market. Insert yourself in that conversation… everyone has a few good ideas in them somewhere. By showing you care about the business adds to your value and inclusion… and you’ll learn more about the business model and help people think through some clever options. If you just don’t care about the business your work in and really can’t be bothered to support your firm with its future, your current career track may be getting very limited…

Include others in what you do, even if it’s boring. Everyone loves being included in what others are doing… inclusion far out-trumps boredom. If someone enthusiastically shows you how he RPA-ed some workflows together, you’d just be happy he showed you how he did it, even though he may be dis-invited to your next pool party.

Being smart about data is no longer geeky, its career-critical. If you can’t automate and digitize your rudimentary processes, you will quickly run out of value to any organization. Plus, every siloed dataset restricts the analytics insight that makes you a strategic contributor to your business. You really can’t create value or transform a business operation without converged, real-time data. You don’t need to have a mathematics masters to understand your customers and the markets in which your operate – you just need to explain to your colleagues what you need and make sure it gets done.

Tune up your cross-cultural intelligence. We need to do a lot more than merely understand cultural differences – we need to adapt and modify our behaviors as the situation dictates as our workplaces and business environment continues to globalize. That means we need to get smarter about different senses of humor (and different sensitivities), widely differings levels of political correctness, different styles of engagement (most Americans tend to like to talk a lot more than most Europeans, for example and their meetings often last longer). Also be sensitive to time zones – the days of expecting people to take 4.00am calls are pretty much over. And be prepared to talk more about geopolitics – many people just want to talk about the big issues more openly these days (even Americans where political discourse has been taboo in days gone by). My only advice here is to try to listen, even if you are in violent disagreement with someone…

A lot has changed in the last year… especially when it comes to automation: it has now become the broadly-accepted efficiency tool for cost leverage with operations.

Every customer has RPA project managers and automation leads hungry for data, advice, and ideas. Every service provider has RPA embedded into their service delivery models, and every credible advisor has a practice that is working with multiple clients to make this happen. The Armageddon days of talking about robots taking our jobs are over – these are now the reality days where we can see exactly what’s going on with automation and AI, and accurately estimate how it’s going to impact the services industry in the next few years.

There will be impact, but it’s manageable provided we focus on new skills and value.

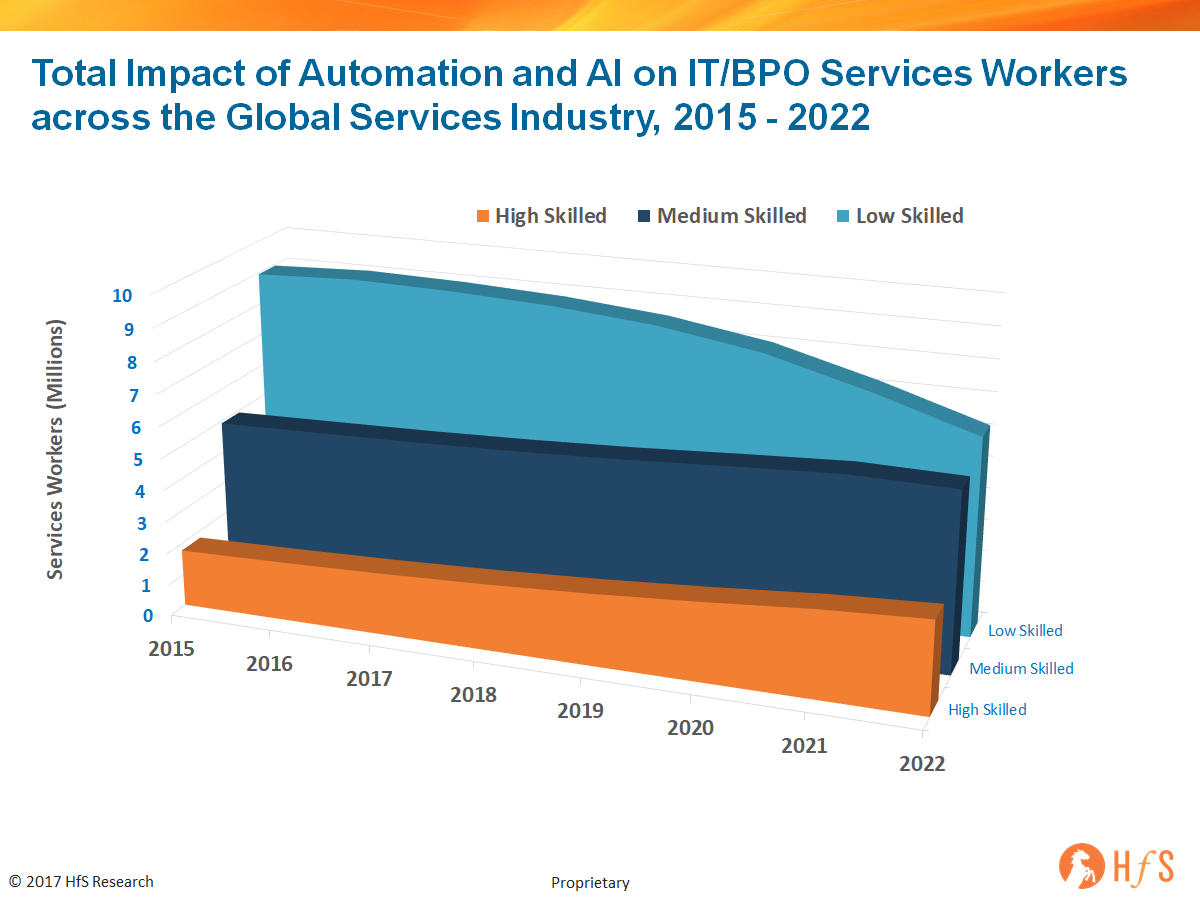

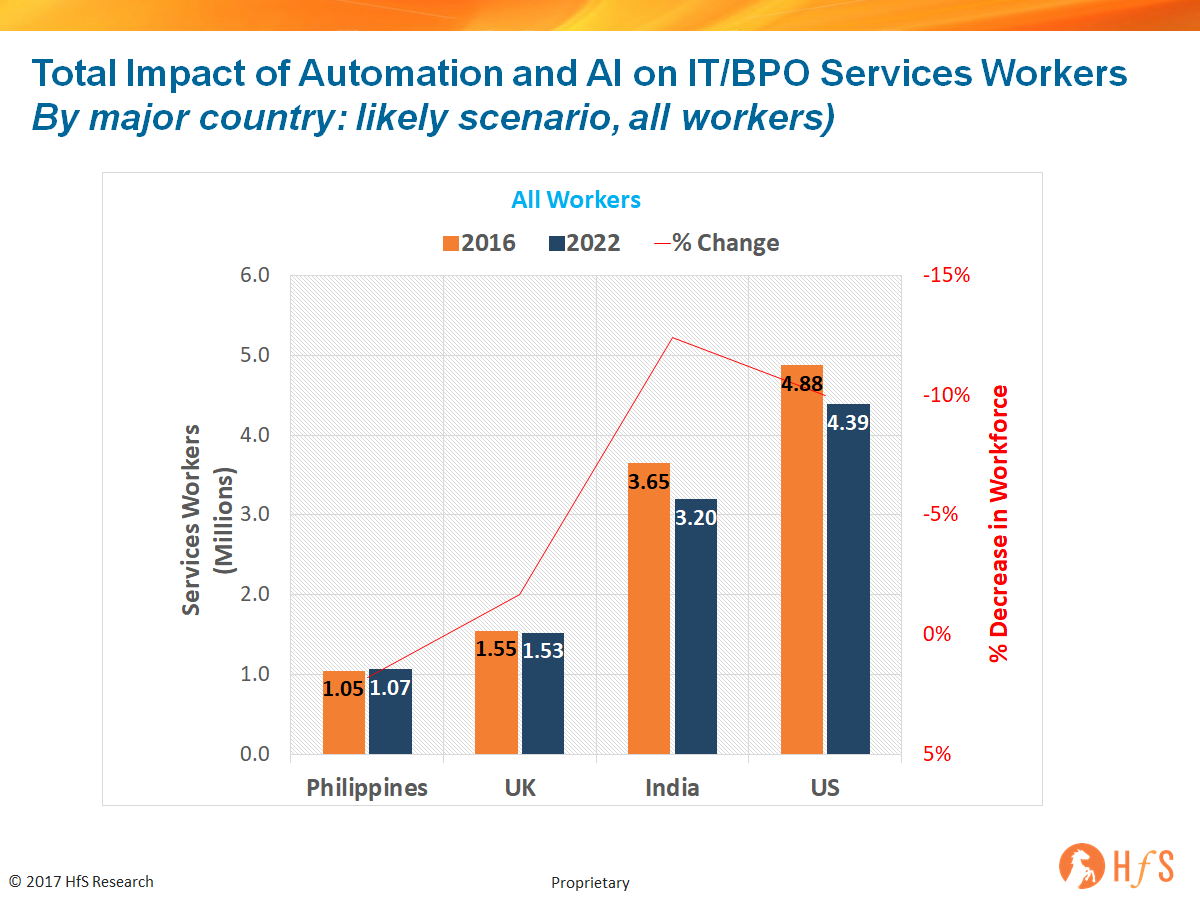

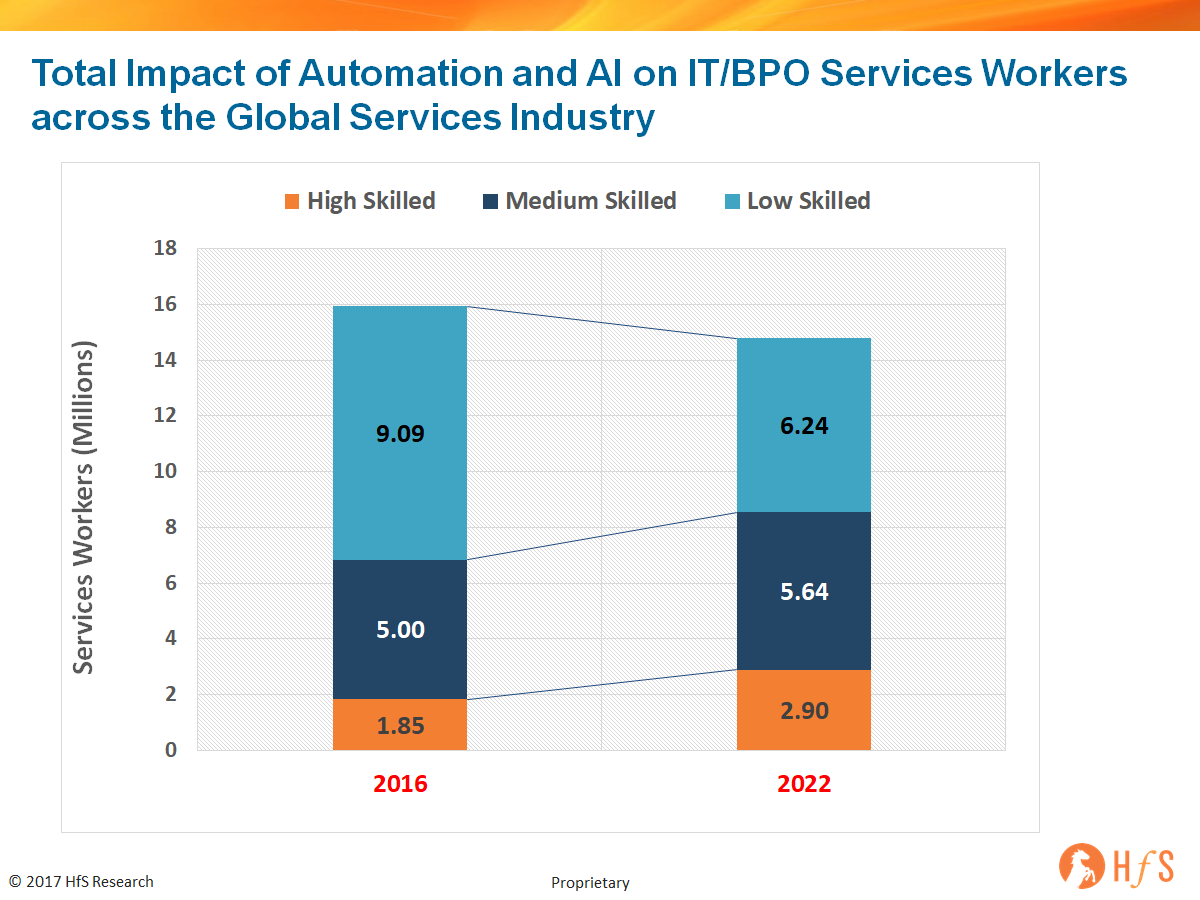

In short, the global IT and BPO services industry employs 16 million workers today. By 2022, our industry will employ 14.8 million – a likely decrease of 7.5%* in total workers (see our research methodology below). This isn’t devastating news – we’ll lose this many people through natural attrition, but what this data signifies is this industry is now delivering more for less because of advantages in automation and artificial intelligence. The new data also shows how job roles are evolving from low skilled workers conducting simple entry level, process driven tasks that require little abstract thinking or autonomy, to medium and high skilled workers undertaking more complicated tasks that require experience, expertise, abstract thinking, ability to manage machine-learning tools and autonomy.

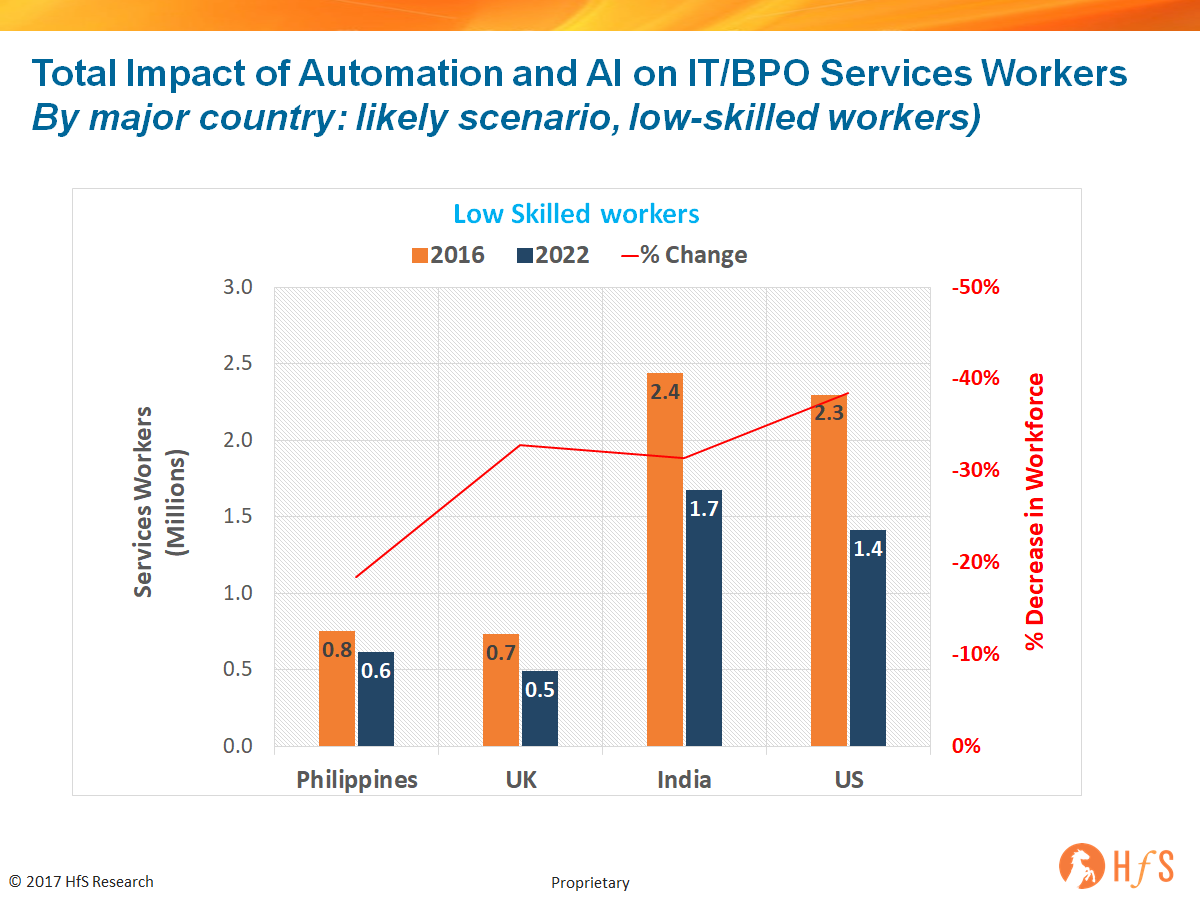

The low skill routine jobs are getting increasingly impacted, and our new demand data shows an acceleration in RPA tools (a 60% increase over the next year) where service providers are the largest adopters into their own service delivery organizations. We expect to see a more rapid impact on routine job roles which is most notable in 2022 as companies take time to build the impact of RPA into service contracts and figure out how to turn work elimination into hard savings than merely soft efficiency savings. With barely a 50% satisfaction level, this will take 4-5 years to see the real cost benefits in terms of job elimination. Most of the short-medium term benefits are being seen in increased efficiencies and more digital process workflows. All major service delivery locations are expected to be impacted at the low-end, but the higher the wage costs, the higher the expected role elimination (750,000 roles in India and a similar number in the US):

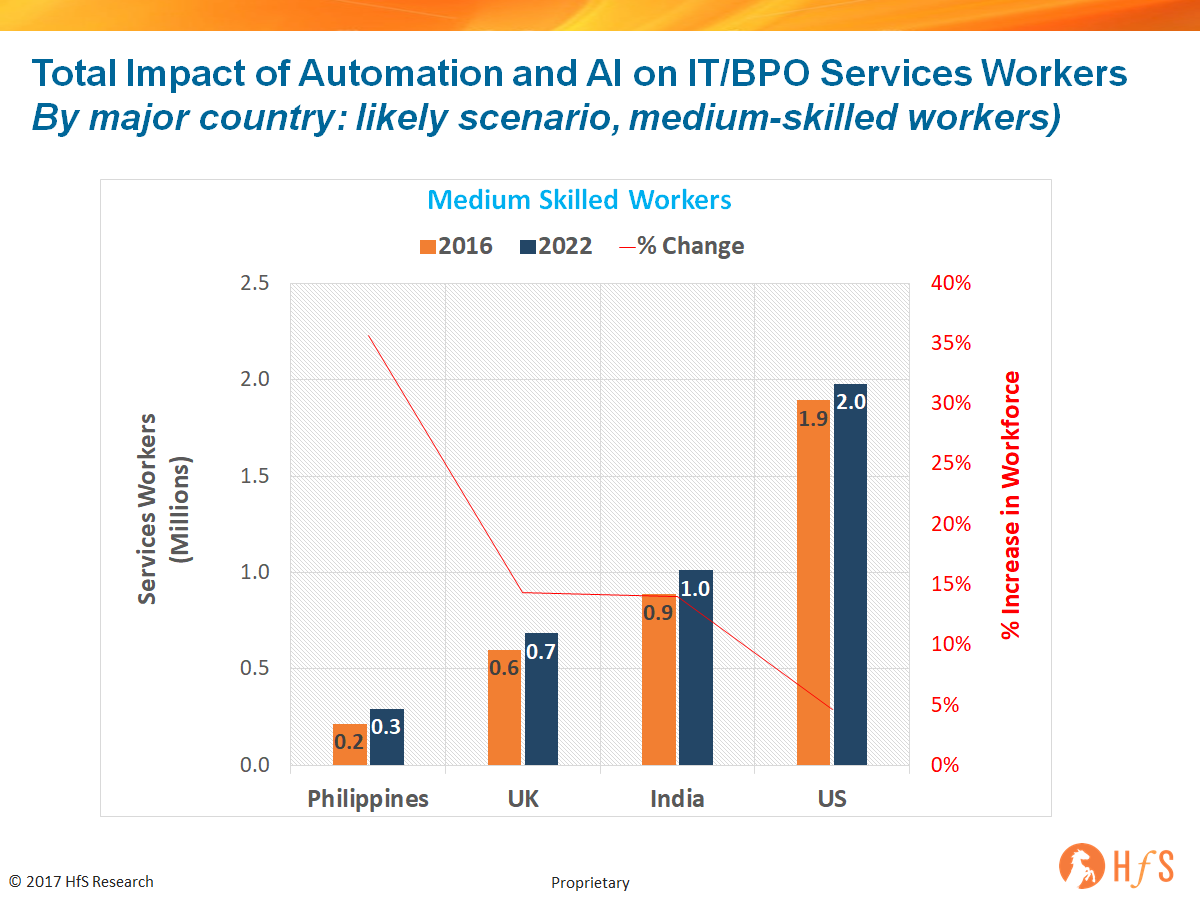

Medium skilled roles are picking up across the board, especially in roles that are customer/employee facing with the need for more customized support, the ability to handle basic customer and data queries, and more customized service work with virtual agent models in 2nd / 3rd tier escalations:

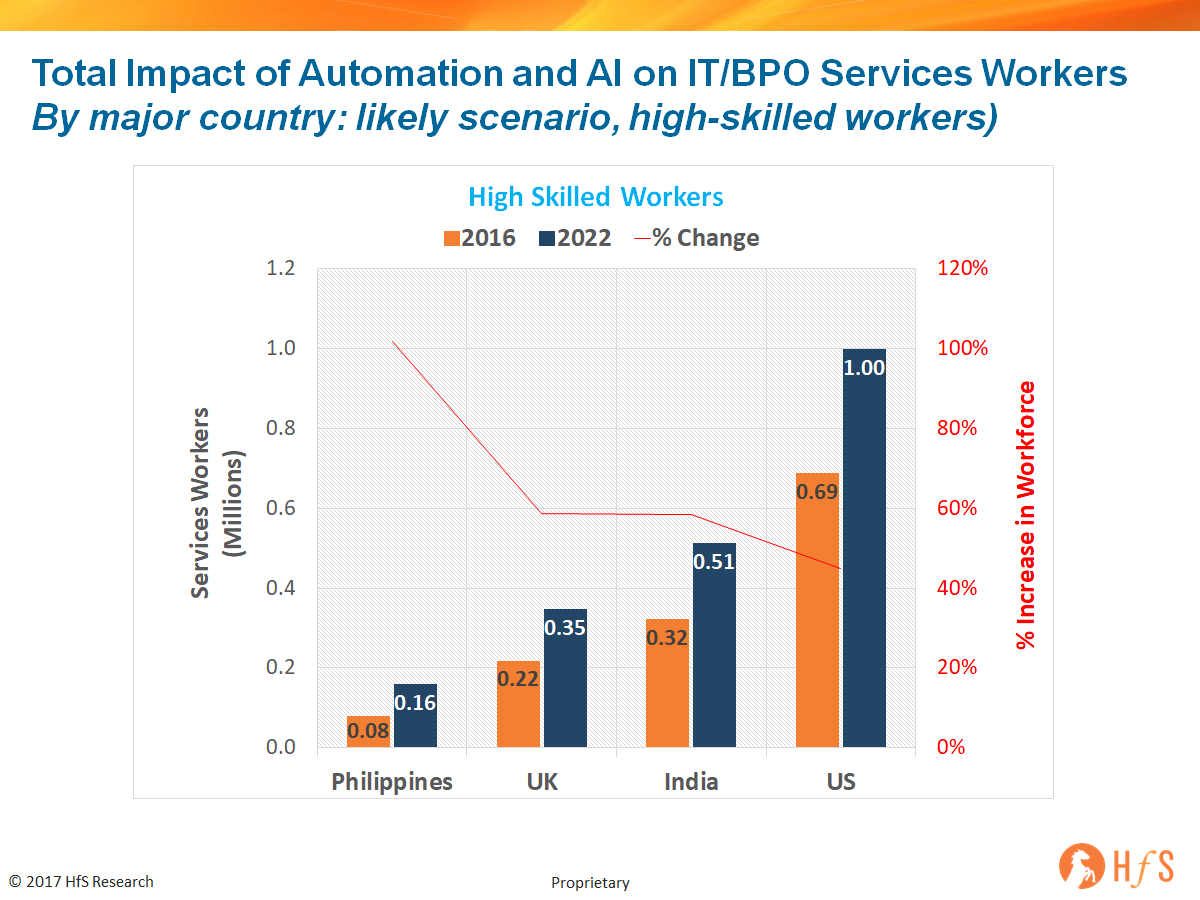

As this data illustrates, the more we automate and digitize, and the more we adopt human + machine technologies, such as machine learning and cognitive solutions, the more we need people to developing skills in managing automated workflows, machine learning mechanisms, being able to interpret data, and service increasingly complex customer and employee needs. So when we take into account the total impact of automation and AI on services jobs, the impact is not nearly as severe as so many of the hypesters and fear-mongerers are prophesizing:

Philippines should actually increase its service delivery population due to its dominance in voice and capabilities to support increasingly complex and personalized customer models, the UK should be flat, especially with the challenges of Brexit and the slowdown in low cost worker immigration, while both India and the US will see a total worker reduction estimated at the 10% level between by 2022. You can view the total impact on the global services industry – a worker population decline of 7.5% here:

The Bottom-line: The rote jobs are going to be eroded, but there is time on our side to develop the new skills we need

The big narrative here isn’t about what’s going away, but more about what is emerging in its place. The next fives years we can manage, it’s the five after that when the impact on labor becomes much more challenging. Transaction roles at the bottom of the value chain have been under threat for many years now – with the impact of low cost location delivery and better technology. Now the emergence of RPA is eventually going to sound the death knell for most high-throughput, high-intensity jobs, as both service providers and enterprises master the ability to apply these technologies effectively. The good news is this takes time and there is no huge burning platform to do this overnight from most enterprises.

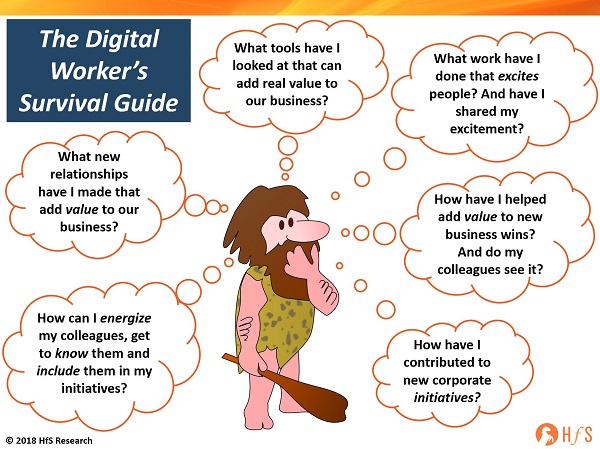

So our message to all stakeholders on operations and services is simply to get out of your comfort zones, accept that new skills are replacing old ones, and it’s critical we have a plan to train, develop and invest in changing what we have. I will leave you with six things to think about as you ponder your own value to this industry and your firm:

Which customers have you delighted recently?

What new relationships have you made that add value to our business?

What work have you done that excited people inside and outside of the business?

How are you helping energize your colleagues and exciting them with new ideas?

How have you helped add value to new business wins?

How have you contributed to new initiatives that improve productivity and effectiveness?

HfS has taken the following assumptions to form this size and forecast for the services industry:

A more aggressive uptake of RPA and Autonomic plus adoption of Cognitive in second half 2017 Leading stakeholders start to educate the market more realistically The adoption of RPA, RDA, Cognitive Computing and AI reaches exponential growth Visibility on impact through details in financial earnings calls and beyond Stronger impact on supply-side, more marginal on buy-side 30% Reskilling to medium and high skilled jobs, with 2/3rd to medium and 1/3 to high

HfS bases its data findings on the following sources:

HfS State of Automation survey (June 2017) covering the dynamics of 400 business operations and IT executives leading automation initiatives;

Market expertise of the HfS analysts across RPA, AI, BPO, IT Services and key industries;

Service provider interviews to understand their automation adoption across global delivery centers and emerging skills competencies with automation and AI solutions;

Government data and data published by industry associations, such as NASSCOM, US Bureau of Labor Statistics, IBAP, OECD Employment and Labour Market Statistics and Office of National Statistics, which provide data on IT industries and education – including specific information about job creation and the impact of automation;

HfS services contracts database, which provides analysis of service providers contracting activity;

Qualitative interviews with service buyers across different industries and company sizes;

Executive-level interviews with key independent advisors in the automation arena, such as KPMG, EY, Deloitte and Symphony Ventures to understand rate of adoption and other core issues related to automation and AI.

Having spent the last 15 years of my life in the US before recently returning to my British homeland to focus on the global expansion of HfS, I think I have earned the right to offer a view on how global innovation will evolve in the coming years. So let’s have a real State of the Union look into global battle for economic and digital supremacy.

For decades now, Silicon Valley has driven technology innovation, US corporates dominated business innovation, and US healthcare was the paragon of high-quality patient care. Everyone looked to the US for innovation, leadership and entrepreneurship. Hell, there was nowhere else in the world I could have founded and made HfS a success eight years’ ago… people in the UK used to sneer at new brands, ideas and anything that cut against the legacy business establishment. But Americans liked shiny new things, they embraced entrepreneurship and new ideas, and welcomed foreign talent. The US was the world’s innovator, the world’s entrepreneur… it was the place where ambitious people aspired to flourish. All good things happened in America – it’s where dreams were hatched and made real.

Fast-forward to present day and all this is changing before our eyes

Tech innovation is no longer confined to a politically exhausted, entitled and overpriced Silicon Valley. Israel is becoming a leading hub for security, blockchain and AI start-ups and talent. India’s startup scene is especially vibrant as ambitious IT talent grows frustrated with the monolithic outsourcers and seeks to join emerging tech firms and get involved with AI development environments such as Python, R, Caffe, Google TensorFlow, the Azure ML Workbench, Amazon’s Sagemaker etc. In China, real cooperation between the government and its tech giants is significantly positioning the country’s advancements as an AI leader. Meanwhile, Estonia is already putting its entire population database on a blockchain platform as part of its plans to build a digital nation, and even Dubai is declaring it will be a Blockchain city run by smart contracts by 2020.

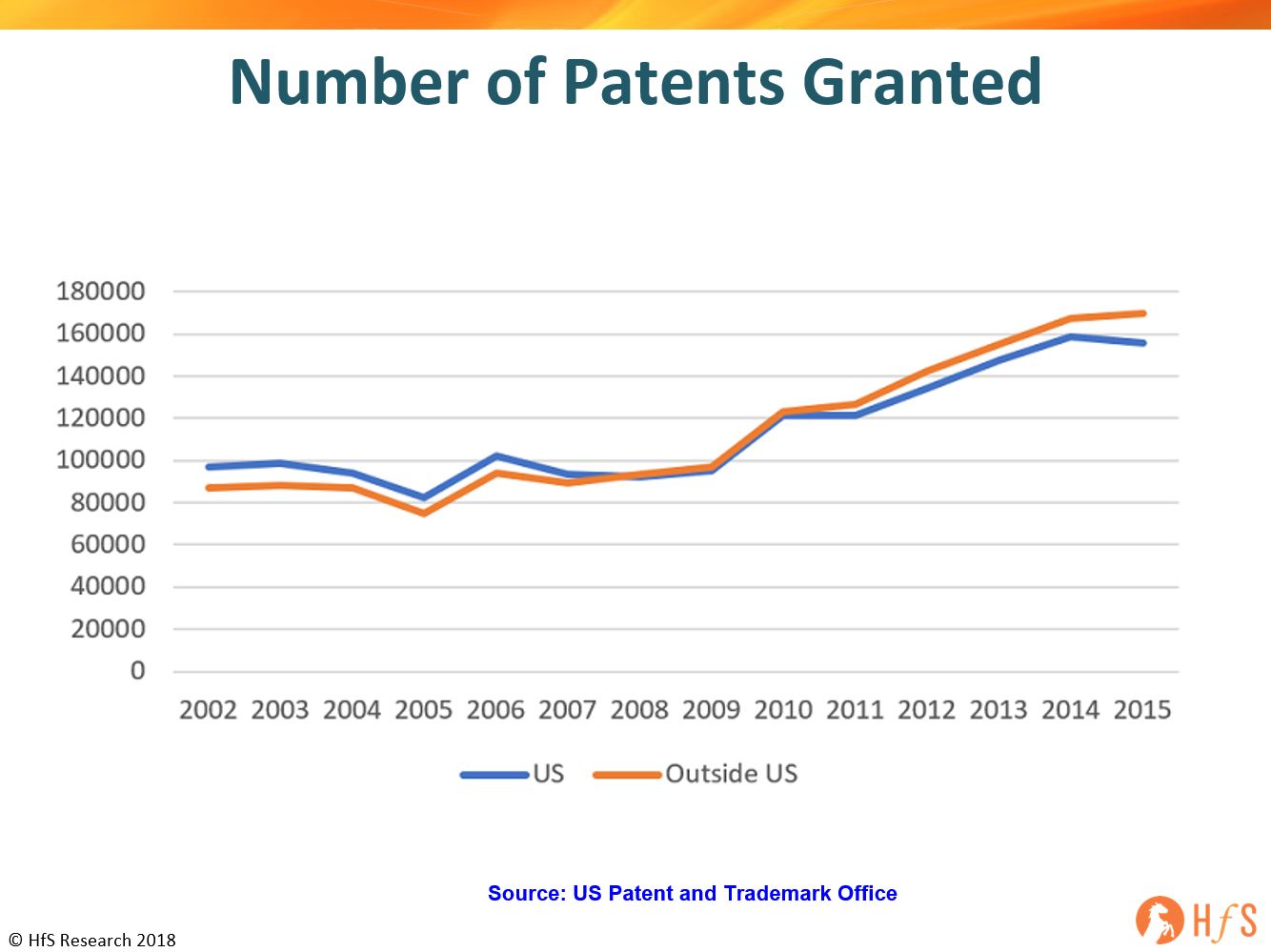

The abhorrent cost of talent in Silicon Valley, coupled with the extremely negative politics asphyxiating their once-dynamic firms is driving investors and valley firms to globalize their approach to talent access and their partnership ecospheres. US Patent and Trademark Office data shows that the number of patents granted to foreign countries (outside US) is now greater than US itself. Moreover, as tech power increasingly shifts to true global players such as Amazon, Alibaba and Google, and the establishment tech giants servicing legacy enterprises, such as Workday, Salesforce, SAP and Oracle become increasingly confined to a shrinking global 2000 (while ignoring the burgeoning small/mid-sized enterprise sector), the whole tech innovation industry will become increasingly globally distributed, as opposed to controlled from the entitled Californian epicentre.

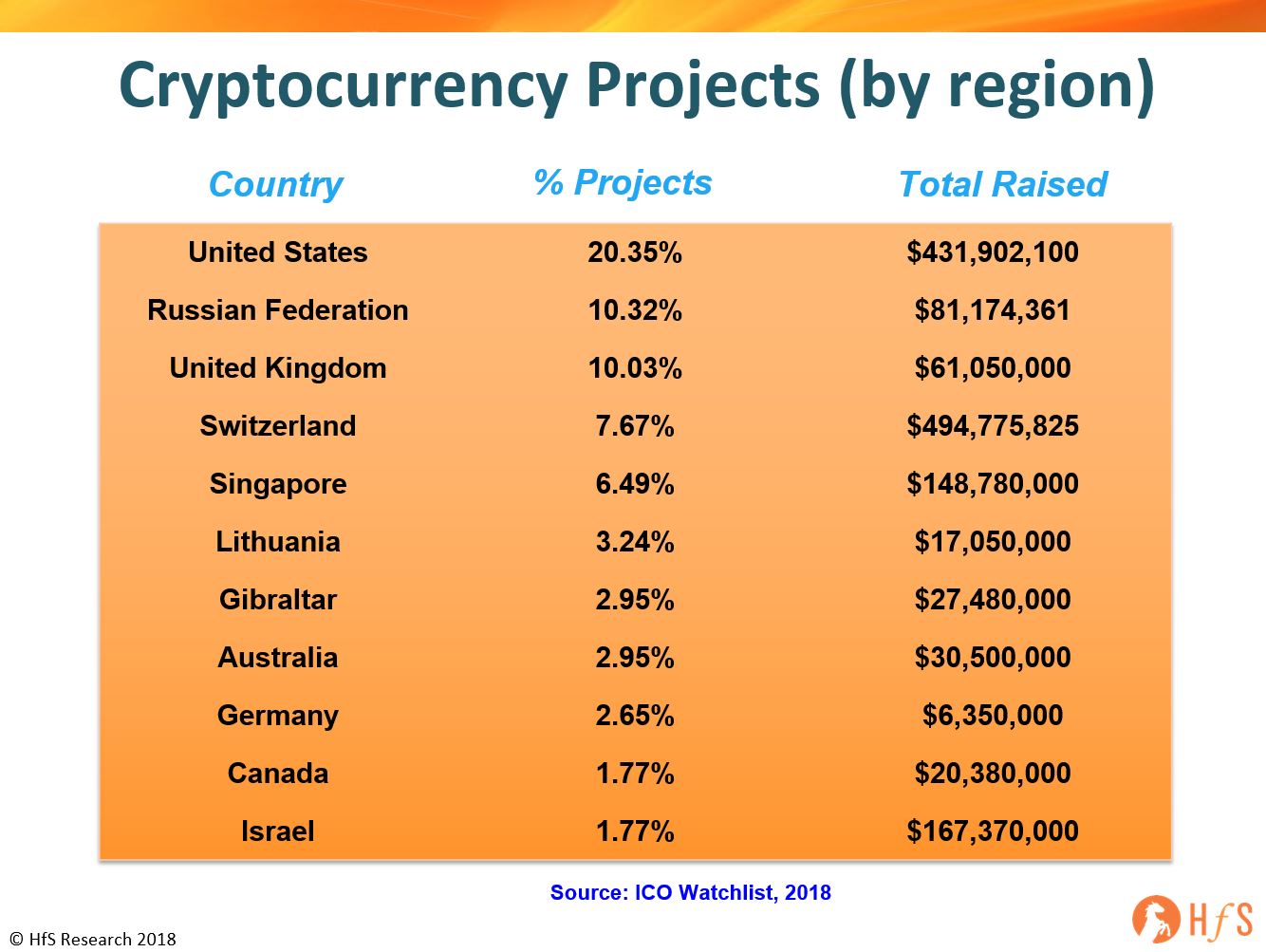

The crypto technologies and AI ecosystems will really start to blend, creating a whole new global tech economy. Use-cases around traceability through provenance and asset tracking, digitization of contracts leading to faster settlements, management of private data and digital identity will drive significant effectiveness gains in existing business models. Blockchain can also become a source of competitive differentiation in the medium term by re-imagining IT infrastructure that is shared and decentralized, re-defining transaction management that is transparent and immutable and driving additional trust in multi-party collaboration. Consequently, we’ll see AI developers increasingly involve themselves with this exciting combination of AI and blockchain. These areas include how to build together common collaborative data hubs to z the sharing of data, allow the sharing of emerging blockchain models, using distributed ledgers, blockchains and smart contracts for individual AIs to mediate their machine-to-machine interactions. As the stranglehold of the legacy US banks policing the world’s financial markets starts to loosen, we’ll see the global development communities come together to develop the new phase of crypto-intelligent tech for the AI economy. You only need to look at the spread of Initial Coin Offerings (ICOs) to see that the US only accounts for a fifth of global cryptocurrency projects:

Brexit is forcing new thinking and new ways of enterprise collaboration. While I have been honest about my views towards the negative aspects of Brexit, it has forced new thinking as Britain goes down it’s own path of looking within itself, not dissimilar to what Trump is doing in the US. The difference with Brexit is it’s highlighting the desire of British businesses and academia to embrace global talent and collaboration with other nations. The threat of losing its openness may have the longer term impact of driving British firms to work more closely with emerging nations, such as China and India, and not rely so much on its legacy business partners. It will be the same for the likes of economic powerhouses such as Germany and France, who are also being forced to look beyond the EU for their future commercial alliances. In short, outside of the US, most of the major economies are looking outward to grow, while the US is too busy navel-gazing and trying to figure out how to embrace its past, as opposed to the unraveling future.

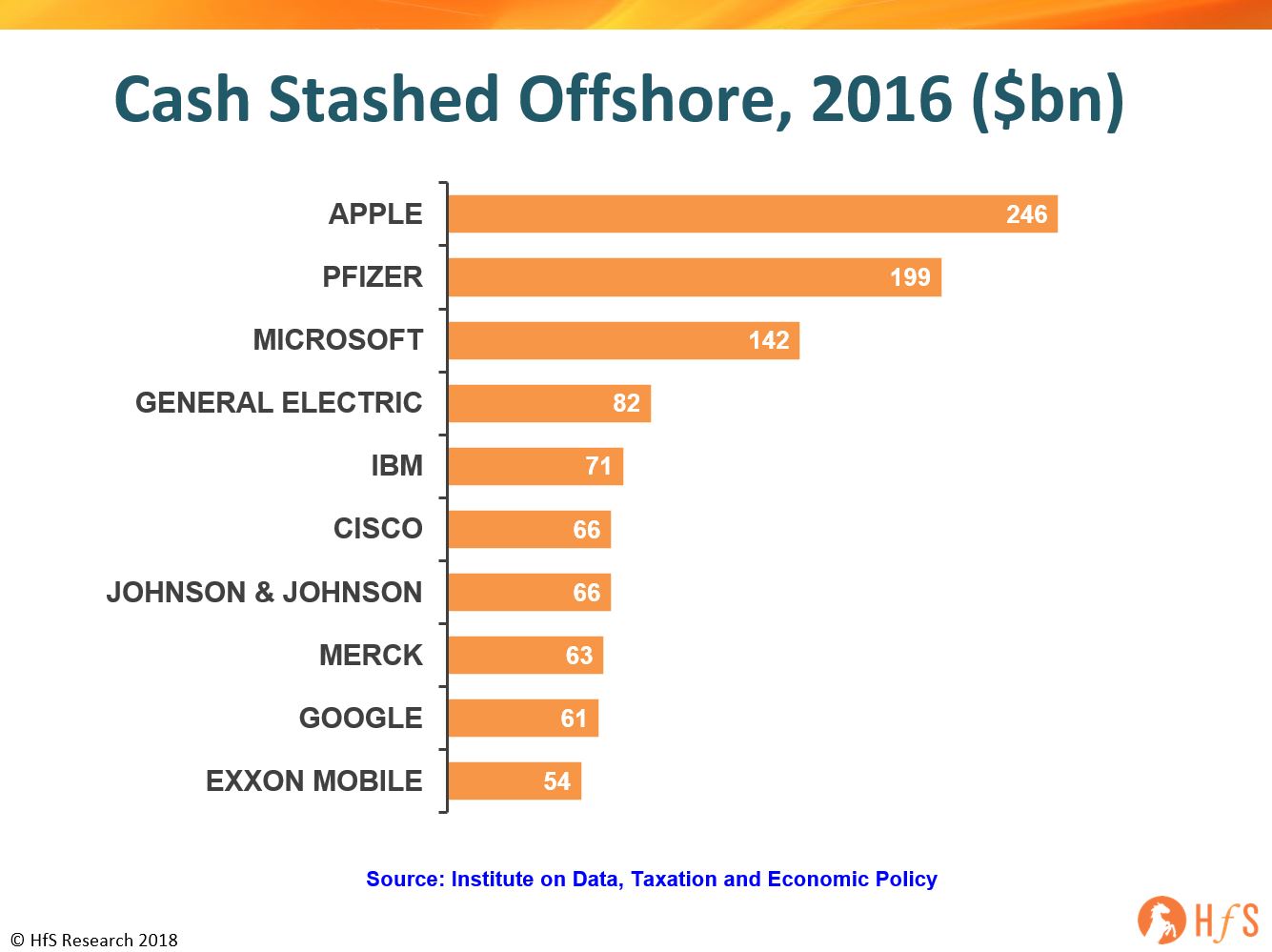

The global giants stash their cash offshore these days, creating a corporate versus government sovereignty war. While the massive US corporate tax cuts will bring some businesses back to the States, it’s pretty alarming when you look at how much money today is residing (and flowing) outside of the country, from the leading global enterprises. The global wealth is being truly spread around these days as the digital economy takes over and spreads across borders. This corporate-versus-government sovereignty war is well and truly in play, and it impacts every nation – and every business:

Digital means global, and there’s not much governments can do about it but become AI powerhouses, thus leveling the playing field. As the major corporates become increasingly global this is increasingly conflicting with governments’ desire to maintain control over their businesses to hire locally and maximize their tax revenue. A consumer in Bangalore is just as important as a consumer in Omaha to Jeff Bezos these days. It’s all one big global digital economy these days. In order for governments to stay ahead, they need to become fluent in AI to keep tabs on these data flows and maintain some sort of control over what is going on… from cyber-security, massive analytics to legislation and regulation. National AI policy and strategy will take center stage creating vastly different types of cooperation deals between governments and continual debate over data privacy and business licenses for firms where data crosses borders. Net-net, there is a new playing field being leveled for the next creation of wealth where data and AI is at the core.

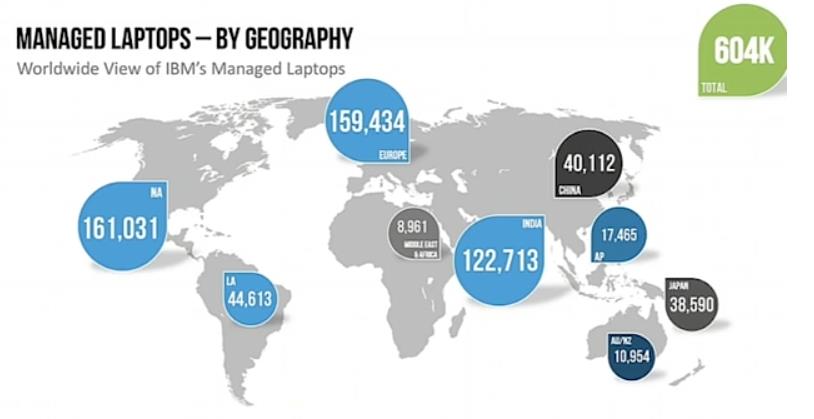

US no longer runs the global tech services game like it used to. The emergence of India as a technology services brand has been stellar over the past two decades, and even most US corporates prefer to work with a portfolio of Indian heritage firms, because of their quality and affordability – and flexibility. This is why “traditional” technology firms, such as DXC (HPE+CSC), Capgemini and Atos are finding it harder than ever to compete with the Indian heritage ower houses, who have all withstood the Trump anti-immigration policies impressively. Plus, America’s two tech powerhouses, IBM and Accenture are not really that “American” anymore – they have globalized themselves along with the digital economy – just look at the distribution of managed IBM laptops in 2016, as revealed by IBM’s CIO Fletcher Previn:

The Bottom-Line:There was only one bailout – and we’ve had that already. The new global economic war is being fought in data and AI

There is less tax revenue for the US government to boost its economy and reduce its massive $20 trillion debt. There won’t be a government bailout the next time the economy crashes – there is no more debt to be secured. Do we really think Amazon, Apple and Google will bail out governments? President Trump hopes corporate tax cuts will stimulate a massive reinvestment in the country, but the creation of new wealth goes a lot deeper, where access to talent with innovative and entrepreneurial mindsets is no longer confined to the blessed US of A.

Outside of the US, the recession of 2008 cut deep, and people know they cannot afford that happening again. Inside of the US, that massive Bandaid is still masking the inherent demise of the country’s core issues, as the rest of the world catches up. The next phase will not be about artificially propping up legacy banking systems and pumping borrowed money into infrastructure projects… it’s about taking the lead in a global digital economy by embracing, educating and possessing the best talent, the best homegrown companies to house that talent … and having the smartest leaders who understand the power data and AI.

Knowing full and well that predictions can bite you on the arse isn’t going to stop us making them! Particularly when the financial reports pour in from some of the biggest movers and shakers in the services industry confirm what we are thinking.

What do we know now?

Unlike the Trump-esque games of ‘I told you so’, we’re not going to pass off something everyone knows already as a prediction (and then immediately congratulate ourselves on doing such a good job at getting a prediction bang on the money).

First up, we need to talk about what we already know; most of the big providers have already posted their results and they make for interesting – and upbeat – reading.

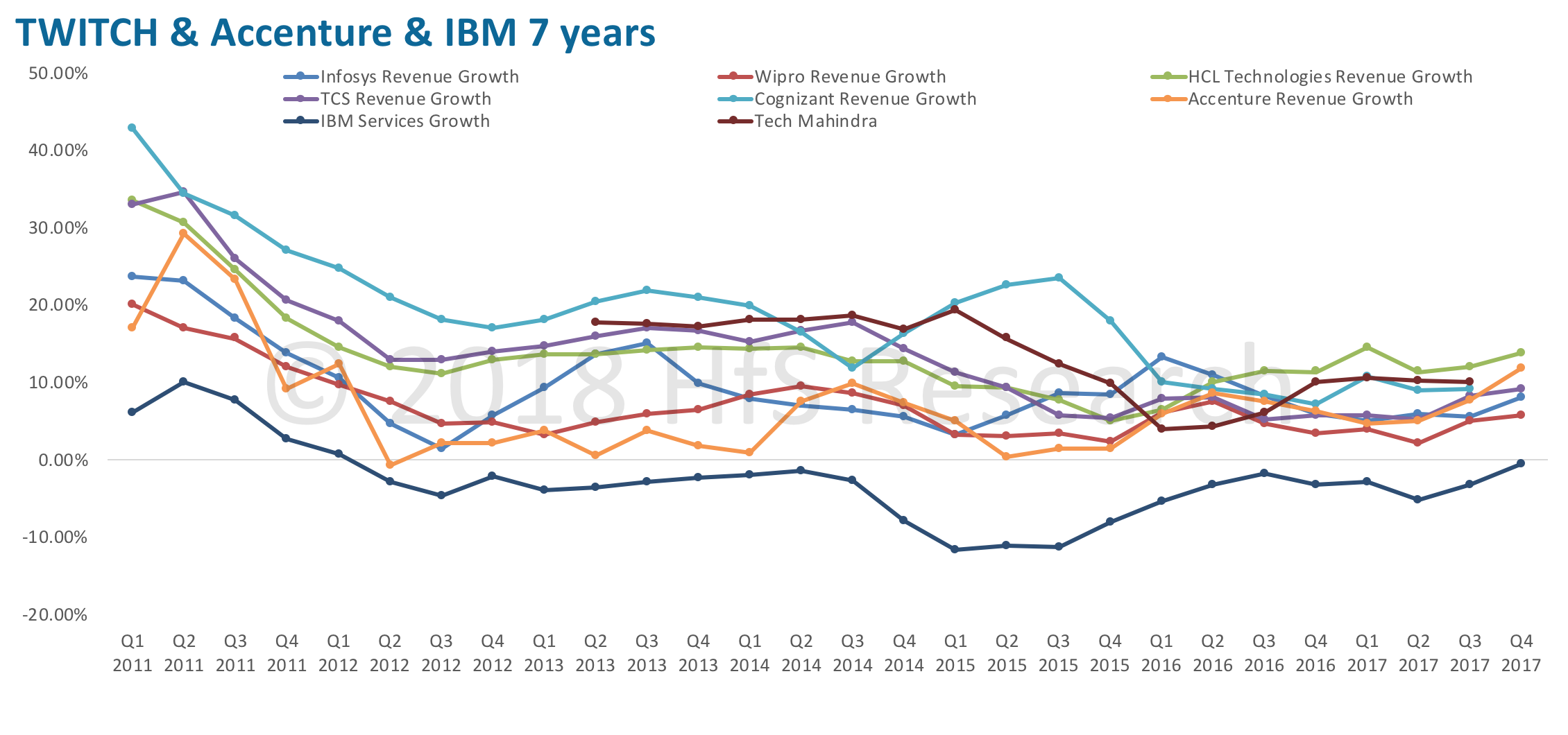

Let’s start by taking the TWITCH providers (Tech Mahindra, Wipro, Infosys, TCS, Cognizant, and HCL). By now, all of these providers, barring Cognizant and Tech Mahindra, have submitted their financial reports for Q4 2017. This gives us a decent picture of the state of the market in general—a topic tackled in greater detail in our latest 2018 market primer—but, suffice it to say, we are starting to look at the IT services market more optimistically – for the first time in years. Our expectations that all of the major providers would report reasonable growth figures have largely been met, a sure sign of the market finally reaching the tipping point. In short, we’re leaving behind much of the turmoil-ridden restructuring of the market from traditional and legacy services to the as-a-service and digital models enterprises now consume with increasingly insatiable appetites.

TWITCH is the winner?

Even so, there are winners and losers, and the pick up in market growth is not shared equally. Wipro, for example, is bucking the trend somewhat by reporting weaker growth than its contemporaries. Similarly, TCS is pushing a more consistent growth line, but the increase of a few percentage points doesn’t quite match the considerable spike other providers are seeing.

HCL’s continued growth has come as somewhat of a surprise to us. While the firm has a strong track-record as an IT services major, there were expectations that the emergence of increased digital uptake would leave the firm struggling to mirror its rivals. Central to this thinking is the fact that the firm has acquired digital capabilities less voraciously than some of its peers, and many of the larger acquisitions, such as Volvo IT, are now mature enough that we would not expect to see them contribute enormously to revenue growth. However, HCL’s continued growth—it is currently the fastest growing TWITCH provider—tells us several things about the firm. First, HCL clearly has the ability to grow digital capabilities organically to help pivot its products and services to meet new demand. Second, it has the leadership talent to keep the ship steady, even when dynamic market forces are making a significant impact, for better or for worse. In addition, HCL has smartly balanced its organic digital investments by focusing on reliable traditional market segments, such as its partnership supporting IBM Tivoli customers, which clearly has many years of profitable revenue to enjoy.

Infosys, too, reported a strong performance as 2017 closed, signalling the firm’s recently acquired ability to negotiate leadership crises with imperviousness. Expectations for the firm’s growth were somewhat muted as analysts and commentators took on a wait-and-see approach to observe if the firm’s revenue would be another casualty of the Infosys CEO sideshow. However, Infosys has continued to post solid growth, a testament to changing customer expectations (if the services are fine, who cares if the CEO changes?) and the firm’s investment in digital, its strong DNA for providing data driven support, and remodelling service delivery. The track-record of investment exemplified in both acquisitions of digital firms such as Brilliant Basics, and the upskilling and reskilling of staff, most notably the training of large chunks of service delivery teams in areas such as design thinking.

Finally, we have Cognizant, which is yet to report its Q4 2017 results. We expect no surprises, though, as the firm shows all signs of enjoying the uptake in the market with the other TWITCH providers. The firm is far from the dizzying heights of growth it became famous for in earlier years, but it continues to plug on and with recent acquisitions in analytics, digital, and design plus a strong narrative, we can expect the firm to fully enjoy the benefits of the expected tipping point from traditional to as-a-service and digital. However, the pressure is on, given the mark that Accenture has set with its 31 recent digital-esque acquisitions; expectations will be a return to double digits and anything falling short of this is bound to be a disappointment to stakeholders.

WITCH providers’ and Accenture’s revenue growth over seven years

Accenture’s enjoyed an unstoppable rise, but will digital continue to be the flavor in 2018, or is automation coming to the fore? And is this IBM’s time to seize back its throne?

Other firms are also revealing how they are handling the restructuring of the market—even IBM, which has finally arrested 22 consecutive quarters of decline in revenues, is approaching what could pass for growth. The latest financial reports from the firm place the decline in revenues as fractional as 0.6%. But the real standout provider is Accenture, which has reported revenue growth rates that actually exceed many of its TWITCH contemporaries. Given that its total revenues are double that of its nearest TWITCH rival, this is no mean feat.

If we were to categorise providers for their appetite for acquisitions and investments, then Accenture must have been famished. The firm’s list of acquisitions, particularly in digital, runs lengths longer than the combined total of major players in the space. Accenture’s reputation for delivering the goods—albeit with a premium price tag—has set the firm up to become the flagship of the digital services industry, assuming other providers remain on their current trajectory and we don’t see any furtive market leadership contest over the next few years. Conversely, IBM doubled-down on cognitive, before the market was ready, but should now find itself in a position to capitalize, with a compelling automation-AI suite of offerings coming emerging from its GBS division. Observing IBM versus Accenture over the next couple of years may boil down to a battle of two philosophies for clients: do they primarily need a services partner focused on the front end (digital), or transforming the middle-back end (automation). Having that OneOffice broad suite of skills to pull both together is where the real winning line is…

You were promised a prediction… here’s several

With all of that data at our fingertips and the recently published market primer giving us food for thought, it’s about time we started to make a few predictions about what we’ll see when all of the providers report their financial results. Foremost, it looks like we can expect to be more optimistic about the IT services market—something that IT services analysts are no doubt finding deeply unsettling. If, indeed, we are witnessing the market hitting rock bottom as posited in a recent blog, then it appears to be bouncing back with some vigour. It’s worth noting that growth in the global economy has been unexpectedly strong, which may be the cause of the improved growth rates. However, the growth seems more decided and uniform, which leads us to expect consistent positive results due to broader market restructuring rather than a macroeconomic fuelled one-off.

Here’s the clincher, though. While the spoils of increased market growth is being shared somewhat ubiquitously at the moment, it’s unlikely to lead to a utopian future, where all providers are winners. The best way to predict which providers will perform well in the new digital race and which will false-start is to take a look at the engine. While many providers have the capabilities and capacity to profit from the changing market initially, many don’t yet have the brake horsepower to gain enough momentum. Fewer still have the fuel needed to keep performance consistent and long-lasting.

So, here’s the next prediction: While we can be optimistic about the market generally, in the digital race not everyone will make it to the podium. Outside of the major providers we discussed earlier are a plethora of other IT service providers, some of which are set to outpace even the most entrenched and well-funded of the old guard. Beside these disruptors are the firms reluctant to make the jump to new delivery models, sticking to the safe harbours of legacy and tradition. These may be the first casualties that come sputtering to a halt well before sight of the checked flag. The upshot is, although things look rosy now, the change required to succeed in the new market is likely to be a step too far for many. Expect a frantic and bitter melee to ensue as legacy providers fight for relevancy in the new services landscape.

And, as a final prediction: Because these things are often best in threes and there hasn’t really been a strong prediction that we can really hang our hat on, we’re going to go out on a limb here and say 2018 might be the year we see IBM Services report actual revenue growth. There. We said it.

Bottom Line: Those providers that are investing during these transitional times will be the winners

While the biggest providers in the IT services space are validating a more optimistic market outlook, the picture is far from Utopian and while the first signs of the market finally reaching the tipping point marks the start of a positive decline for some providers, for others it signals the start of their decline. The new wave of OneOffice is forcing providers to invest further up the consultative chain to help clients move with technology. The tech is here and it’s easy to install and support – it’s being able to help clients use it and align it with their processes and business models, which is where the new spend is being created. It’s all about digitizing the front end and aligning those customer driven processes to an automated middle and back office… and, as we discussed, most of today’s motley crew of providers have pieces of the puzzle, but not all of it. Let’s face it, most will never be great at delivering everything, so clients will need to choose partners who can bring together the pieces and deliver to the outcomes they defined.

That requires real investment in your people, intense training and education, and establishment of an innovative culture to make the shift. Legacy providers will not get there with fancy marketing and a veneer of OneOffice—they need to establish it at their core, which is incredibly painful for firms that have never had this in their DNA. So the short answer to the question posed in the title of this blog is that many providers will fail to make the leap. There will be enough legacy business for years to come to feed these firms, but many will wither away as they reach the lowest common denominator of commodity value.

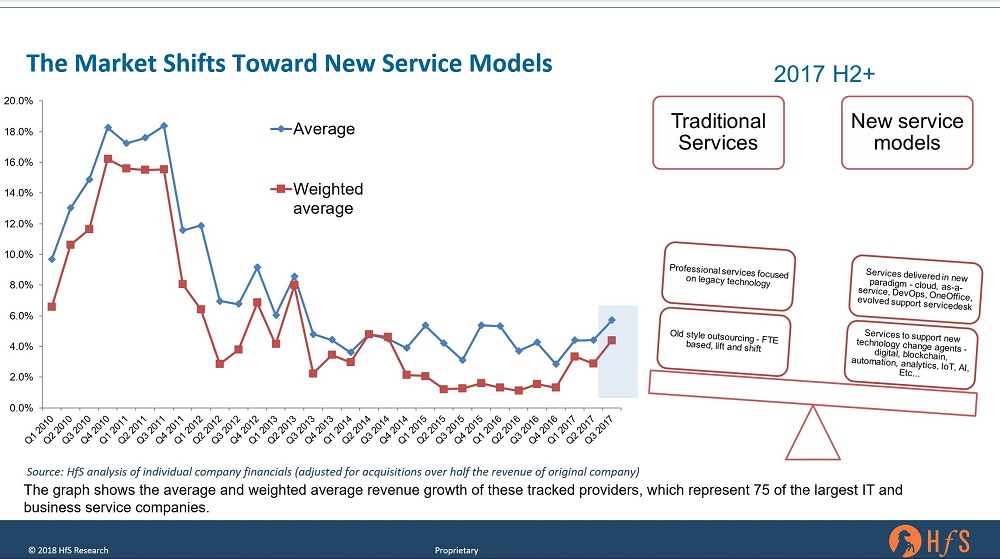

Surely not, folks… but did the flagging IT services business finally find rock bottom… and we’re now working our way back to something resembling (gasp) growth?

According to our latest market size and forecast, Q3 2017 showed real signs of genuine improvement in the services business. It is consistent with the gradual upward trend we’ve been monitoring over the past 8 quarters (with the exception of Q4 2016), when the market dipped due to concerns around Brexit and Trump. We’ve been observing an increasingly significant number of Digital OneOffice type deals, and it seems we may have finally reached an inflection point where these “OneOffice style” engagements are driving more growth than the legacy is sucking out of the market.

How we define OneOffice IT Services

The OneOffice framework is all about collapsing the barriers between front and back office to create OneOffice with unified outcomes, centered around customer impact. OneOffice IT supports this framework. As such, OneOffice IT Services is split into two main components – operational services and professional services:

The difference between traditional operational services and OneOffice operational services is the business model of the services itself and the manner in which the service is delivered. Operational OneOffice services can include both application management and IT Infrastructure focused services. OneOffice services use an evolved service delivery model that shifts the business model towards outcome realization and consumption, so would include hybrid and cloud infrastructure as-a-service, application management in SaaS and DevOps environments, and evolved enterprise wide managed services service desk support. OneOffice framework is all about collapsing the barriers between front and back office to create OneOffice with unified outcomes, centered around customer impact. OneOffice IT support this framework.

ii) Professional Services

The shift in professional services is less about changes to the business model of the service itself, but more about the technology being implemented or consulted about. HfS includes all the services used to support the new technology change agents, namely cloud, digital, analytics, blockchain, process automation, IoT, and AI. Importantly, this includes consulting that changes clients’ businesses as part of this new technology adoption.

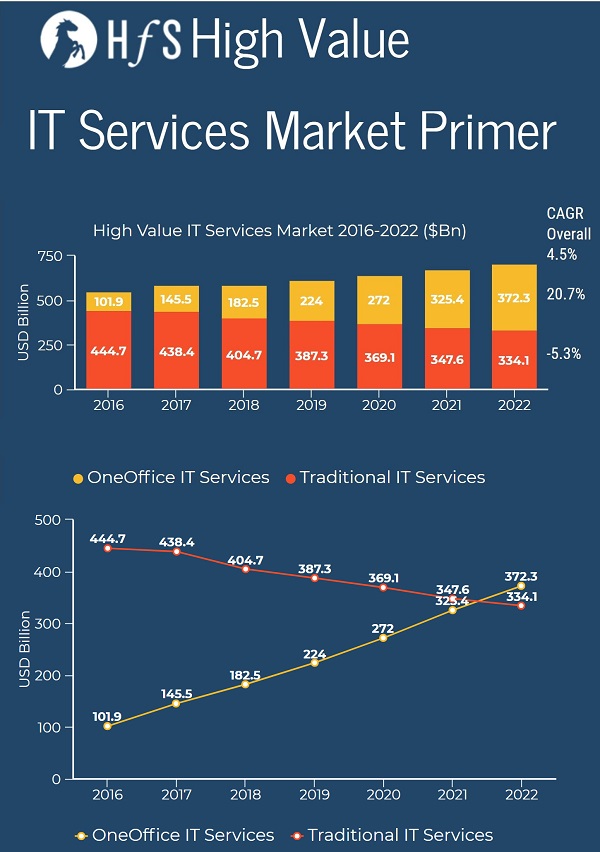

We are translating this optimism into our market forecasting and are starting by making the first adjustment to the IT Services forecast which you can see in the 2018 market primer infographic:

Why OneOffice IT is driving the IT services rebound

The market primer provides our latest size and forecast for the high value IT Services market – this market excludes support services and training and education services. Its main constituents are applications development and management, IT infrastructure management services and professional services. We have provided a split between the new style of IT Services – what we are calling Digital OneOffice IT Services – and traditional IT Services. With the former a combination of newer engagement models and services directed at the implementation and running of the new technology change agents.

Although we do expect the old and new worlds to coexist for some time to come, the distinction between the two will become harder, and less relevant – particularly as the market overall starts to accelerate its growth. We have increased our forecast for IT Services overall to 4.5%, with OneOffice services growing at 20.7% and the traditional markets declining at 5.3%. We expect 90% of professional services growth to come from the emerging change agents (namely digital tech, automation, AI and eventually blockchain), as the consulting and implementation services for traditional IT shrinks.

We can see traditional (or “legacy”) IT outsourcing being impacted by big price dips in traditional infra and apps work – and general cost impetus – and a falling out of love with outsourcing as a deliverer of real business value. There is still too much focus on legacy deals – even with the shift towards asset light, as-a-service and cloud taking operating costs out of larger contracts – and the upside of new technologies not compensating. However, we can see some of this changing as growth in cloud services becomes enough to offset these declines.

The application development and management market is still growing faster than the market as a whole. Due to new methodologies like DevOps and the increased “cloudification” of business infrastructure, the lines between IT Services towers continue to blur. This means applications become more front and center and the infrastructure that supports them becomes less important. We have seen more deals and more RFIs where applications and the infrastructure supporting the apps is combined.

Crucially, traditional application management is now largely commoditized, with new growth areas stemming from systems integration, application engineering, and design, enabling the adoption of new IT and digital technologies. Indeed, SaaS adoption is set to grow almost five times faster than traditional software product delivery, with many large businesses showing a preference for the As-a-Service model instead of capital investment.

In 2016, the number of contracts for Custom Application Development (CAD) and Maintenance accounted for 25% of the total market activity, whereas the application maintenance share reduced to 18%. In 2017, we expect customization to be the second service in demand under ADM, after SaaS services.

The Bottom-line: As the line between traditional IT services and OneOffice services continues to blur, we’ll see some traditional offshore-centric providers making the smart investments begin to reap the benefits

The professional services market has been kept buoyant with new technologies and digital. However, the pricing for professional services is increasingly at odds with pricing for operational IT services – with operational services becoming cheaper and more efficient over the past decade, through the use of cloud, better development platforms, standardization, automation and, offshore. This disparity between the perceived value of professional services and operational services is starting to show in customer attitudes toward consulting. This also creates significant opportunities for the offshore-centric service providers moving up the value chain to cater for broader transformations over longer team deals – such as the recent slew of TCS wins over the past few weeks.

While it’s been a “sluggish” couple of years for the likes of Wipro, TCS, Cognizant, HCL and Infosys (sluggish in the sense of only single-digit growth), we expect many of the investments these firms have made in their delivery capabilities to bear fruit over the course of 2018 and beyond – such as Wipro’s Holmes, TCS’s ignio, Cognizant’s BigDecisions, HCL’s DRYiCE etc. While uptake of many of these investments has been slow, we are now seeing many of them being embedded into longer, higher risk engagements, which should ultimately lead to more profitable, higher value delivery. On top of this, we are seeing Accenture lead the way with its concerted focus on digital solutions, but not every enterprise is ready to pay Accenture prices. And with IBM’s 23 consecutive quarters of negative growth finally came to an end, this may signal the firm is managing to balance its OneOffice capabilities with its struggling traditional business to better effect. On the flip side, those that fail to convince their shareholders they have to make the smart investments, will shrink and wither away like many of the monoliths of yesteryear (several of whom still limp along on life support).

All in all, we may finally be emerging from a confused couple of years, where the industry struggled to make the switch from the old to the new. Now the blurring if the lines is bringing higher value IT to the forefront and forcing many of the traditional service providers to up their game and provide more value. Expect more investments to follow and some erosion of profit margins to fund this next wave of IT service development… but ultimately renewed growth, which ultimately leads to a healthier, more buoyant and innovative industry.

Yes, folks, that was one of the key takeaways one of the delegates pointed out at the FORA Summit in London last month, where a very mature conversation took place about the real future of operations in this lovely robotic age (download your full copy here).

This packed-out event was attended by 120 senior executives, the majority being senior buyside enterprise clients, joined by the CEOs of the leading automation solutions vendors, practice leaders across the leading service providers and global advisors. and the HfS analyst team. This was a chance to get beyond that deluge of wooden marketing and sales hype that is murdering our sanity… and get to the real nub of the of the issues plaguing a confused – and fumbling – industry.

Ten Big Takeaways from the Discussions

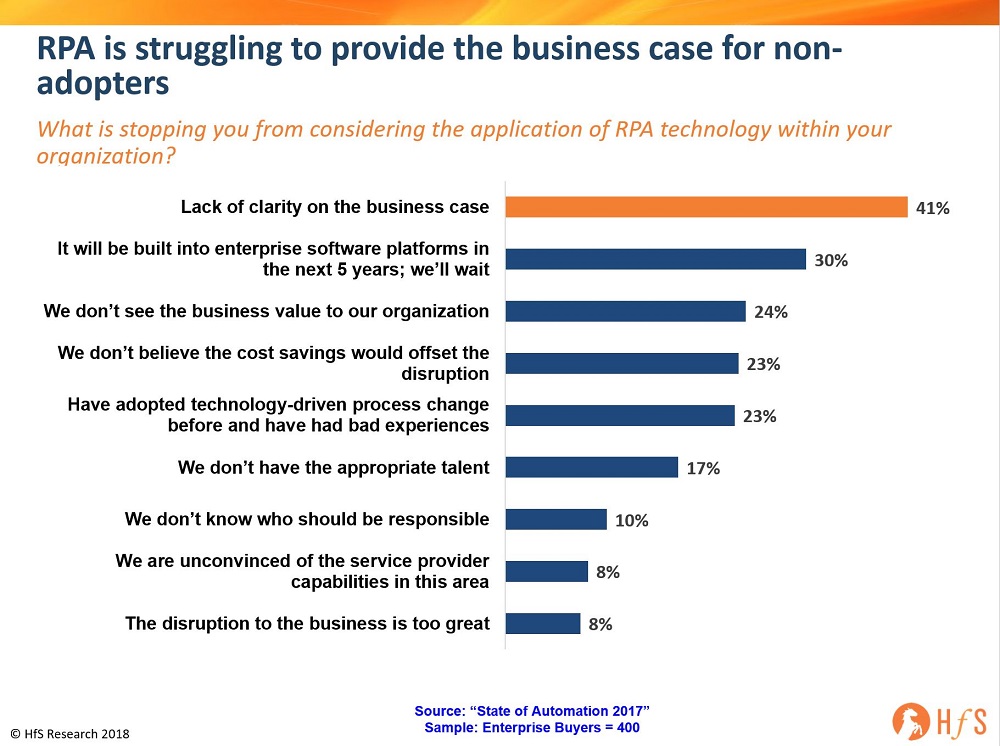

1. RPA needs to move beyond the teenage romance stage. One delegate pointed out that RPA often started out like a teenage romance – a lot of fumbling around with enthusiasm that ends quickly, often leading to disappointment. Past events have focused on the importance of change management to the process, however, our recent study of 400 automation buyers shows that a lack of clarity around the business case is the major barrier to RPA adoption (change management rears its head after all the fun and games of implementing the software):

2. RPA hype is over and it’s nearing time to retire the term in favor of Digital Operations and the emerging Digital Workforce. Hype needs to move from replacement to enablement. The benefit of automation and AI are not reducing the workforce, but enabling machine to human and human to machine interaction. Helping enterprises and governments make better decisions with data. Building a more virtuous cycle with automation, decision making and data.

3. The Pace of Change Cannot Be Slowed – If You Aren’t Disrupting You Aren’t Surviving. Companies that view disruption as an opportunity and are not complacent are the most successful. Paranoia about the world ahead is your friend – driving staff to innovate and disrupt. Technology in this circumstance is a tool not a solution. Our customer panel said that there are ‘burning platforms’ already being created and businesses are going to have to come to a decision at some point soon to adopt. The supplier panel were agreeing that automation is surviving for big businesses and large enterprises have less than five years to sort this out.

4. The biggest challenge for Automation is the shift to scale. It’s not a technology problem, but an organizational change issue and how to achieve a broad set of outcomes at scale. Currently many implementations are sub-scale – tens or hundreds of bots instead of thousands they could potentially be.

5. Ultimately the world needs to shift its economic measure from effort to outcomes – where value is linked to achievement rather than the effort to achieve. The value of relationships need to be more interactive than ever, to make the shift towards outcome-based engagements, and away from effort-based.

6. The C-Suite is paranoid about the future and eager to make changes, while middle management is complacent and resistant to change. Culture is a major impediment to changing this dynamic. This requires a number of changes –change in the way companies operate, change in the skills that companies value, change in the incentives and the training that enterprises offer staff.

7. To adapt we need to constantly learn. This means better understanding of new technologies, better understanding of underlying processes and what can be improved. But ultimately it is about the best way to drive outcomes within the business.

8. We still need more use cases – especially as we look to Cognitive/ML/AI. As the hype shifts to higher forms of automation the need for use cases for all automation expands. There needs to be clearer understanding of where the value lies and where the process should begin. RPA is being passed over even when it offers 80% value for 20% cost and should be recognized as a valuable tool in an enterprise’s arsenal.

9. The purpose of digital is to bring humans and technology together. One of the panellists made the comment that digital was not about specific technology or about a transformation. “Digital” is about the bringing together of humans and technology. It is the interface, closing the gap between the two.

10. Change management remains a vital component of automation strategies. The difficulty in delivering at scale is exacerbated by poor change management and planning. It’s clear from our event in Chicago and in London that enterprise customers and service providers need to spend more time on planning to get automation to work effectively. One senior buyer representative said “change is not like flipping a light switch… more like a dimmer where it comes to full light over time and every new leaders is a new start.” So there needs to be a clear outcome and commitment – one of the main topics of conversation during the event was around the need for better change management to ensure that nothing is left behind in the race to transform. With important advice that “change management is about educating people slowly toward what the world will look like tomorrow”.

The Bottom line: Here are the anti-fumbling themes taking the conversation to New York this coming March…

To conclude the London summit and take the narrative onto our biggest and baddest FORA summit yet, the following four themes will steer the next phase of this industry mandate:

The Technology – a means, not an end. Data is the currency of transformation

Like with many new technologies, analysts, consultants and industry practitioners become obsessed with definitions and the demarcation between automation variants: in this case RDA, RPA, AI, Machine Learning, Cognitive, and all their permutations and combinations. Whilst this might be important for market sizing and positioning – many of the conversations in London reinforced the point that technology is a means, not an end – deemphasizing this definitional obsession. All these pieces of tech are tools, not solutions themselves. Without a coherent, end-to-end business transformation strategy, “dabbling” with automation technologies frequently does more harm than good, at best yielding only meagre results. Given the amount of potential disruption to legacy work practices businesses are facing, a deeper transformation strategy is required which will take automation at scale – “you need to go big,” as one participant put it, to get real benefit from automation. But first, organizations must map out the path to understand where they’re going. This brings with it another crucial part of the transformation recipe – data. Understanding the centrality of data to the digital enterprise – how to acquire, structure, interpret and act on it – is essential

The Value – shifting the metrics from effort to outcomes

Much of the discussion during the event focused on the outsourcing services industry, in part because that’s where the prevailing labor-arbitrage business model is under existential threat, and in part because that’s where automation technology is already being deployed at scale. During his keynote Phil Fersht observed that “Transactional outsourcing’s death throws began in 2012” – dating its demise to the rapid emergence of RPA. However, there is a new, business model within reach. Providers have meaningful experience with automation technologies and valuable know-how, while buyers desperately need expert help with design and implementation. What’s needed is a new value proposition – one that separates effort and time from cost and revenue, and shares risks and gains. “Clients will have to contribute value to their suppliers,” as one participant put it, and providers will have to become more innovative and willing to expose their balance sheets – in short, being less transactional and more consultative.

The Talent – taking the robot out of the human and putting insights back into the process

As has been discussed at the FORA and HfS Summits in the past – and as noted by Professors Leslie Willcocks in London, automation is not about replacing humans, automation “takes the robot out of the human.” Taking the mundane and process-centric tasks to free up employees to engage in more meaningful activities. Artificial Intelligence, on the other hand, augments and extends the human mind, empowering humans to make more consequential decisions. Together, they fundamentally change human behavior and workplace management paradigms. In the digital future, all employees will need skills in data analysis and interpretation, and middle managers in particular will need to be able to connect the work they supervise with the outcomes the business requires. Both must be granted what one participant called “permission to change” the way they have traditionally operated, and business must invest to equip them with new skills to succeed.

The Change Imperative – the way operations support the business itself needs to be redesigned

There is a growing awareness that we are at a step-change – a discontinuity – in business history. The challenge presented by digital and automation technologies can only be met successfully with a commitment to transformational change; incremental, tactical approaches will only yield limited results and risk failure. As never before, senior executives in every industry face existential decisions about the future of their enterprises, and will need to “make themselves uncomfortable,” as one participant put it – to re-imagine their businesses based on the centrality of data and digital relationships (see Technology above). They will need to shed the constraints of the “as is” and articulate the journey to the “to be.” Success will be measured not on beating last quarter’s results but on the ability to see and grasp the scale of change required and create a viable and compelling digital vision for what one participant called the “journey to improvement.”

Our Chief Strategy officer, Saurabh Gupta has been pioneering new research and vision across distributed ledgers, blockchain and smart contracts. In his latest POV, entitled “The Blockchain Reality Check. Where are we, and what can we expect in 2018?” Saurabh dives into what we describe as “Blockchain Six-Pack”, which describes six built-in features of blockchains that manifest into a disruptive potential over the long run for enterprises, when leveraged intelligently in relevant business use-cases. Net-net, the Blockchain Six-Pack is changing the way we think about business transactions, data storage, and even industry value chains and associated revenue models:

Distributed shared data over Peer-to-Peer (P2P) network reduces single points of failiure. The most fundamental difference between DLT and the way we store data today, is that Distributed Ledgers do not have a central administrator. A distributed ledger is replicated, shared, and synchronized digital data geographically spread across multiple sites, countries, or institutions. This allows information to be available across the network in a fully transparent and autonomous way, reducing single points of failure and enabling far better collaboration.

Consensus-driven trust cuts out the middle-man. In blockchains, there is no need to trust the middle-man as you don’t have one. Trust is driven by consensus algorithms such as proof-of-work (PoW) or Proof-of-Stake (PoS) or some variation of these. As a result, we don’t need to worry about unreliable, inaccurate, dishonest or overpriced intermediaries.

Immutable transactions ensure trust. Each block in a blockchain contains a timestamp and a link to a previous block. By definition, blockchains are inherently resistant to modification of the data. Once recorded, the data in any given block cannot be altered retroactively without the alteration of all subsequent blocks and a collusion of the network majority creating a single source of truth.

Hashing-based data ensures integrity and security. All records are individually encrypted. Blockchains use cryptographic hash codes to verify data that drives up integrity and creates strong resilience to cyber-security concerns

Automated smart contracts promote touchless interactions across process chains. Several blockchains also offer ‘Smart Contract’ functionality. These are computer protocols that facilitate, verify, or enforce the negotiation or performance of a contract, or that obviate the need for a contractual clause. This allows contracts to auto-execute based on pre-set conditions or triggers and allows for much higher levels of straight-through It can even allow the millions of IoT devices to work autonomously

Permissioned and permission-less flavors give enterprise users flexibility. Much like public and private clouds, blockchains can be private (permissioned), public (permission-less), or somewhere in between (hybrid). These flavors give enterprises the flexibility to choose their solution based on their needs and preferences. Permissioned blockchains enhance privacy and take less computational power (so have higher throughput) but lack the Utopian trust that permissionless blockchains, such as Bitcoin, can bring.

Blockchain’s inherent features give it the potential to drive new touchless business models and disrupt existing ones by removing the need for intermediaries in the long-run. This results in significant increases in the speed, security and reliability of executive processes, transactions and interactions on both micro and macro scales. The potential is enormous, provided blockchains are adopted, sensibly regulated and executed effectively. However, HfS expects a five to seven-year horizon for blockchain to delivery fully, given the nascency of the technology and associated challenges. In addition, media hype and fake news, in addition to negative activity from threatened legacy stakeholders and other economic impacts, could impede adoption.

What can we expect from blockchain in 2018?

In the near term, we do expect blockchain initiatives to drive significant business impact and create a frenzy of excitement as ambitious businesses jump on the potential of new technology developments like never before. Use-cases around traceability through provenance and asset tracking, digitization of contracts leading to faster settlements, management of private data and digital identity will drive significant efficiency and effectiveness gains in existing business models. Blockchain can also become a source of competitive differentiation in the medium term by re-imagining IT infrastructure that is shared and decentralized, re-defining transaction management that is transparent and immutable and driving additional trust in multi-party collaboration.

We might not see the true disruptive potential of blockchains over the next 12-18 months, but we will see it become much more than a conversation topic with several use-cases that are generating tremendous business value for its constituents. And let’s not discount the levels of hype that tend to drive our industry in new directions, especially when the tech works. While digital, AI and automation have been the flavors of 2017, blockchain is gearing up to lead the hype in 2018, as enterprise leaders search for new levels of value that have genuine, proven business applications.

So don’t sit back and assume that the world is not changing, because very soon this funnel is going to flip. Go ahead and investigate blockchain!

HfS subscribers can click here to download our new POV: “The Blockchain Reality Check. Where are we, and what can we expect in 2018?”

The tech is here and is being proven, but are we really, truly ready to disrupt our underlying corporate DNA to exploit it to its full potential? Can we really change how we operate, think, collaborate and focus to embrace the new wave of data-driven transformation that is engulfing us? In true ballistic HfS style, we are bringing together some of the finest minds from enterprise buyers, academia, technology and BPM services to share how change can be realized – and how to venture outside of our comfort zone to get there. As always, this is a non-salesy sharing of best practices and research between the key industry stakeholders. No cardboard cutouts, plastic booths or dodgy salesmen… honest!

The new “rules” of the workplace are being defined as computers are frantically being programmed to take the lead in the workplace, when it comes to judgment and intuition. We humans need to be the idea generators, the motivators, the negotiators, and the trouble-shooters to fix computer errors, if we want to govern our emerging digital environments. In short, we need to get closer to our firms, be more tightly integrated and intimate with work performance than ever before… which means the role and tenure of the much-derided middle-manager in the Dilbert Cartoons could be taking on a whole new potential twist – and a whole new (potential) level of relevance.

I would go as far as declaring 2018 as a new beginning of the value of the full-time employee – where alignment with the mission, spirit, culture, energy and context of an organization has never been so important. We are seeing the value of contract work diminish as so much “outsource-able” work is so much easier to automate and global labor drives down the cost of getting things done quickly and easily. Business success is more about investing in the core than ever – and that core includes the people who are the true pieces of human middleware to hold everything together.

The onus is circling back to the value of being a full-time employee, who needs to value the fruits of having a predictable income and adapt to the changing balance of how humans need to work with computers.

Remember when the rise of the gig worker was supposed to revamp how so many of us worked, as we escaped the shackles of the “evil employer”?

Almost two decades ago, the internet was creating the independent worker, as exemplified in Dan Pink’s timeless book “Free Agent Nation: How America’s New Independent Workers are Transforming the Way We Live” became the seminal guide for what is now known as the “gig worker”.

Furthermore, unless recent research from McKinsey of 8000 workers can now be categorized as fake news, 162 million people in Europe and the United States—or 20 to 30 percent of the working-age population—engage in some form of independent work today. And a recent study from freelance site Upwork (which undoubtedly wants to hype the impact of gig world) cranks up the numbers even further, claiming that a staggering 50% of US millennials are already freelancing, before declaring the freelance sector will comprise the majority of the US workforce within a decade. Wow.

So are the days of being gainfully employed really disintegrating before our very eyes? Or is the gig hype beginning to atrophy for many people?

The gig economy is becoming a tough place to craft a living if many of the new reports are to be believed. And it’s not just about driving Ubers, delivering food orders and contracting for logistics firms – i.e., working for businesses that exploit the gig economy to drive down labor costs and improve services. It’s the freelance gig economy where people forge a living writing code, supporting content development, delivering consulting work on-demand etc. Even that lovely Upwork research admits: “While finances are a challenge for all, freelancers experience a unique concern — income predictability. The study found that, with the ebbs and flows of freelancing, full-time freelancers dip into savings more often (63 percent at least once per month versus 20 percent of full-time non-freelancers)”. So even if the most biased of sources admits most gig workers can’t cover their living costs, we can conclude that those “Free Agents”, which McKinsey describes as the gig worker sector using gig work as its primary income, are not in a sustainable earning situation.

Today, it’s a buyer’s market for gig work

You only need to spend a little time on LinkedIn to observe just how many people are now marketing their wares as solo free agents, or as part of a company bearing their name. It’s abundantly clear that so many people have decided to set themselves up as independents, that the market for gig talent is saturated and it’s become a “buyers’ market” for gig work. Whether I want to commission a crack consultant to validate some RPA software, hire an analyst to endorse my product, commission a writer to produce a white-label assessment of an emerging market, produce a go-to-market strategy for my business, redesign my website, my logo, or just have someone support my business on a part-time basis… today, I am spoiled for choice. I barely need to hire fulltime employees these days, unless they are truly core to keeping my business ticking along – and I can create real competition to get the work done for much lower costs than a few short years ago.

On top of the risks of commoditizing gig work, we have to contend with the impact of automation and Machine Learning to stay relevant and worthy of earning a paycheck

We’re not in a world rejecting human work, but a world where work is rapidly changing – and the skills of the dynamic middle manager has never been so important. In short, the increasing availability of computing power to crunch massive amounts of data, coupled with advancing tools to tag and label data and workflow clusters with breakthrough programming in languages such as Python for syntax and R for data visualization, are the game-changers that will increasingly impact how we get work done, as we develop continually smarter algorithms to keep teaching computers to do the work of the human brain.

What’s more, the rapid development of Machine Learning (ML) environments such as Google’s TensorFlow, the Microsoft’s Azure Machine Learning Workbench, Amazon’s Sagemaker, Caffe and Alibaba’s Aliyun are becoming the new environments driving armies of coders and developers to align themselves with ML value – desperate to stay relevant (and well paid) against the headwinds of commoditization of legacy coding and app development.

As ML takes over judgment and (eventually) intuition, the human-value onus moves to interaction, agenda-setting, problem defining and idea generation

In short, the disruptive ML techniques are teaching computers to do what comes naturally to humans: to learn by example. Today’s emerging ML tools use massive amounts of data and computing power to simulate neural networks that imitate the human brain’s connectivity, classifying data sets and finding patterns and correlations between them.

Net-net, pattern-matching jobs are increasingly being affected by ML – vocations such as radiologists, pathologists, financial advisors, lawyers, procurement executives, accountants etc. are all being challenged as judgment work is (gradually) being replaced by smart algorithms. However, as elements of these types of jobs are being affected, other job elements become even more important, namely interacting with other humans, creating, setting the agenda, defining and finding the problems to go after. They motivate, they persuade, they negotiate, they coordinate. They are the dynamic conduits of driving information and ideas in an organization and will be increasingly in the driving seat as Machine Learning advancements increasingly take hold. The digital middle manager who can bring a team together and lead people in the right direction does not exist and likely never will…. I’d be amazed if we saw one emerge soon.

Fulltime employment is now becoming a premium situation

Having predictability of income, healthcare costs covered, guaranteed paid vacation time – and a constant supply of work to do – is fast becoming the dream scenario for the disgruntled gig worker. So here’s a thought – go get a JOB. Or if you’re in a job and wanted to try the gig work thing… spare a thought for what your ideal situation looks like, because last time I looked, most firms are doing everything they can to avoid hiring well-paid staff… especially if they can get the work done much cheaper from desperate gig workers.

The Bottom-Line: Five steps to keeping your job:

i) Become the conduit of ideas and information that is irreplaceable right across your organization. So we’ve now come full circle, where the value of having people really close to the business is becoming more important than ever, as computers perform more and more of the routine and judgement based tasks. To the point, the value of the full-time employee goes both ways: companies need people who really understand their institutional processes, their quirks and ways of getting things done… who are onhand to troubleshoot mistakes, but also there to keep the ideas flowing to keep the business ahead of its competition and close to its customers. “Human middleware” is becomimg the real OneOffice glue to break down those siloes and help govern a slick business operation from front to back office.

ii) Develop a positive attitude by finding aspects of your job you do like. Your full time job is likely the best gig-work you will probably ever get, so even if you hate your boss and most of your colleagues, ask yourself if you’d prefer scrapping around for the boring work other companies prefer to outsource. Focus on the interesting stuff you can do and keep reminding yourself that the grass is rarely greener elsewhere. Unless you are a whizz at Python development, the chances are your job-hopping days are numbered and you need to figure out how to stay put and make it better for yourself.

iii) Motivate yourself and become a real motivator. Being motivated – and helping to motivate others – is probably the least computerizable trait of all. If you aren’t motivated, you are placing yourself at risk when your leadership assess which of their team then want to take them forward into the future. If you really can’t get yourself excited about what you do, or your company just demotivates you in such a way you can’t dig yourself out of your rut, then you may need to take that Python course and brush up your resume…

iv) Let the computers take the lead and become the controller to fix mistakes double checking, intervening when the computers do something dumb. Humans and computers make different kinds of mistakes, so we really need to bring humans and computers together intelligently to cancel out each other’s mistakes. Fighting automation and ML is a lost cause, especially when your firm is completely bought in to the concept and it rolling out bots and working on developing smart algorithms. Just let these things take the lead and them figure out how to make them functional and monitor their errors, ad computers will always keep making them. You can’t fight innovation, but you can nurture it, manage it and troubleshoot it.

v) Find your pareto balance and stop whining. Nothing in life including your current or prospective employer will be perfect. Focus on the 80% that is right, versus making yourself (and others around you) miserable by the other 20%. There is rarely a perfect fit where workers only get to focus 100% on all the things they love to do… there has to be this 80/20 compromise, or you will be forever hopping around trying to find a workplace nirvana that doesn’t exist. And it today’s social world your reputation follows you around like never before… and employers are steering clear of the whiners at all costs.

Source: HfS Research.

Source: HfS Research.