The revelation that Deloitte submitted a government report filled with AI-generated fake references and fabricated court quotes is not just embarrassing – it is a $290,000 lesson in what happens when professional judgment is replaced by blind trust in AI.

Australia’s Department of Employment and Workplace Relations said Deloitte will return part of the AU$440,000 fee after errors including a fabricated court quote and non-existent references were uncovered by academic Chris Rudge. A corrected version disclosed use of Azure OpenAI GPT-4o after the scandal broke. AI without verification is not innovation. It is professional malpractice waiting to happen.

GPT-4o did not malfunction. Deloitte’s process did.

Deloitte was hired to review a welfare compliance framework and IT system. The report went live, and a single diligent reader exposed fake sources and a bogus court quote. Deloitte then refunded the final payment and disclosed its generative AI use after the fact.

The model did not fail. It produced fluent, plausible text exactly as designed. What failed was process and accountability. Someone generated content, skipped verification, and submitted it to a government client whose decisions affect millions of citizens and billions in welfare payments. The stakes were too high for shortcuts, yet shortcuts were taken.

Enterprise leaders already know the risks, but they’re buying the services anyway

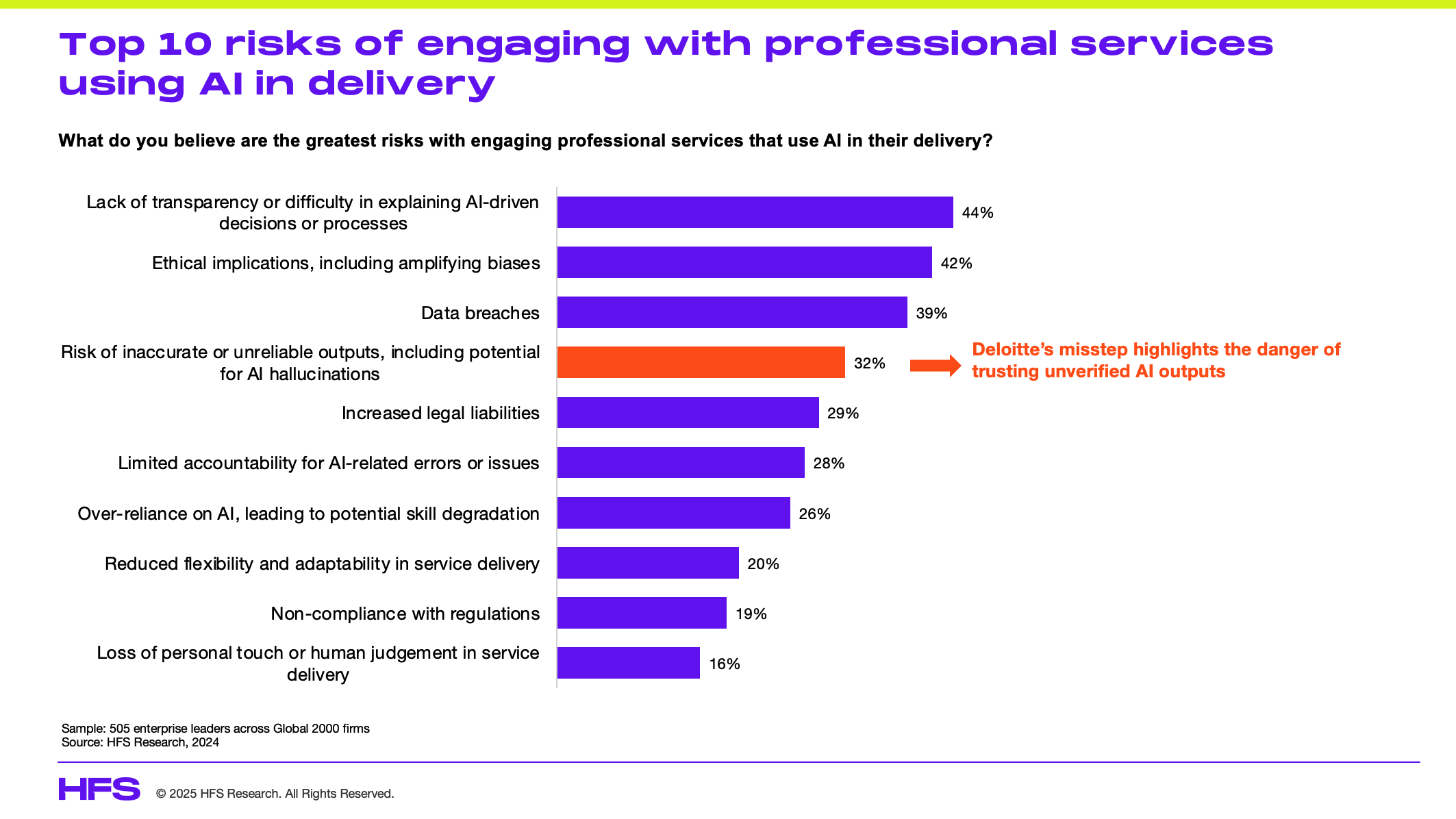

The irony is almost painful. When HFS Research surveyed 505 enterprise leaders across Global 2000 firms in 2024, 32% identified “risk of inaccurate or unreliable outputs, including potential for AI hallucinations” as one of their top concerns when engaging professional services that use AI in delivery. That’s nearly one in three buyers explicitly worried about the exact problem that just cost Deloitte a contract and its reputation:

Yet those same enterprises keep signing deals with firms racing to automate their deliverables without building verification into workflows. The Deloitte scandal isn’t revealing a hidden risk, it’s confirming what enterprise leaders already feared. Even more telling, 44% cited lack of transparency in AI-driven decisions as their top concern, and 28% worried about limited accountability for AI-related errors. The market knows the problem exists. The difference now is that Deloitte’s $290,000 refund puts a price tag on ignoring it. When nearly half of your potential clients are already worried about whether you’re being transparent about AI use, hiding GPT-4o in your methodology until after you get caught isn’t just bad practice, it’s commercial suicide.

Buyers ranked “ability to balance AI with human expertise” as their fifth most important selection criterion

When HFS Research asked 1,002 enterprise leaders across Global 2000 firms what matters most when selecting an AI-powered consulting firm in 2025, the results expose exactly where Deloitte failed. “Ability to balance AI with human expertise” ranked fifth out of ten criteria, sitting between proprietary IP differentiation and track record of delivering outcomes:

This isn’t a nice-to-have buried at the bottom of the list. It’s a top-five dealbreaker. Yet Deloitte’s approach to the Australian welfare report suggests they treated AI as a replacement for human judgment rather than an amplifier of it. The ranking also reveals something critical about buyer expectations: deep industry expertise still matters most, but the ability to use AI responsibly is now more important than customization, change management capabilities, or vendor ecosystem collaboration. Enterprise leaders aren’t rejecting AI in professional services. They’re demanding that firms prove they can deploy it without sacrificing the human insight they’re paying premium rates to receive. Deloitte’s scandal shows what happens when a firm optimizes for speed and margin while ignoring the one thing clients ranked in their top five priorities.

Your vendors are using AI right now whether you know it or not

If you buy consulting, strategy reports, audits, or any expertise-driven service, assume AI is already in your supply chain. The question is not if vendors are using it, but how responsibly they are doing so.

Make AI disclosure non-negotiable in every contract starting today. Every agreement must spell out which tools are used, for what purposes, and how verification occurs. “We use GPT-4o for initial drafts, followed by human fact-checking” is accountability. “AI-assisted workflows” is a loophole.

Verify before you act on any deliverable that matters. High-stakes work requires qualified human review of every claim and citation. Do not assume plausibility equals truth. Deloitte was caught by one diligent academic. How many unchecked reports are sitting in your systems right now?

Rewrite acceptance criteria because your current standards assume human work. Add explicit checks for fact accuracy, citation integrity, and full AI disclosure to every statement of work before you sign it.

Create escalation protocols before the next crisis breaks. When a fabricated quote surfaces, who investigates? Who notifies the client? How do you remediate within hours, not weeks? Deloitte’s response was reactive PR. You need prevention built into operations.

The race to automate is hurting service provider credibility

One unverified deliverable cost Deloitte both money and trust. The economic temptation is obvious: use AI to draft faster, bill the same, and pocket the margin. But that margin gain is being bought with a credibility deficit that compounds with every careless report.

This is the dark side of the Services-as-Software era. AI can enable services to behave like scalable platforms, but that only works when the underlying workflows are validated, explainable, and consistently coded for quality. Without these controls, Services-as-Software collapses into Services-as-Spin.

Make verification mandatory for every single AI-assisted output. Every piece of content must undergo human expert review before it leaves your building. Treat verification as a professional obligation, not an optional cost.

Default to transparency because clients will find out eventually. Discovery happens through audits, detection tools, or leaks. Early disclosure builds trust. Concealment destroys it permanently.

Separate creation from review immediately. The person prompting AI cannot be the same one validating its results. Fresh eyes catch errors invisible to the drafter who anchored on what they expected.

Price for integrity, not just AI-enabled margin expansion. If AI improves efficiency, reinvest some savings in stronger validation. Competing on AI-driven speed while starving quality control is reputational suicide.

Most AI transformation programs fail because they optimize for speed over verification

This problem is now systemic across sectors. New York lawyers were sanctioned in Mata v. Avianca after filing briefs with non-existent cases generated by ChatGPT. UK High Court judges have warned lawyers that citing fake AI cases can trigger contempt referrals. Air Canada was held liable after its website chatbot gave a passenger false policy guidance. Media outlets including CNET and Sports Illustrated faced backlash and corrections for AI-generated content riddled with factual errors and fake bylines. Academic publishers have retracted thousands of papers amid papermill and AI-fabrication concerns, with Wiley confirming over 11,000 retractions tied to Hindawi and Springer Nature retracting a machine-learning book after fake citations were exposed.

LLMs can be transformative when they amplify human expertise. Deloitte’s failure was not using AI. It was abdicating accountability by treating AI as a substitute for analysis rather than a partner in it.

This is exactly where Vibe Coding matters. Enterprises that succeed with AI are already teaching their people to code the “vibe” of quality into every workflow. That means aligning how data is validated, how context is shared, and how collaboration flows across the OneOffice. You do not scale trust with technology. You scale it through consistent cultural coding of how technology is used.

The fastest results come from fixing one broken process at a time

Do not try to govern AI everywhere at once. Start where the blast radius is biggest.

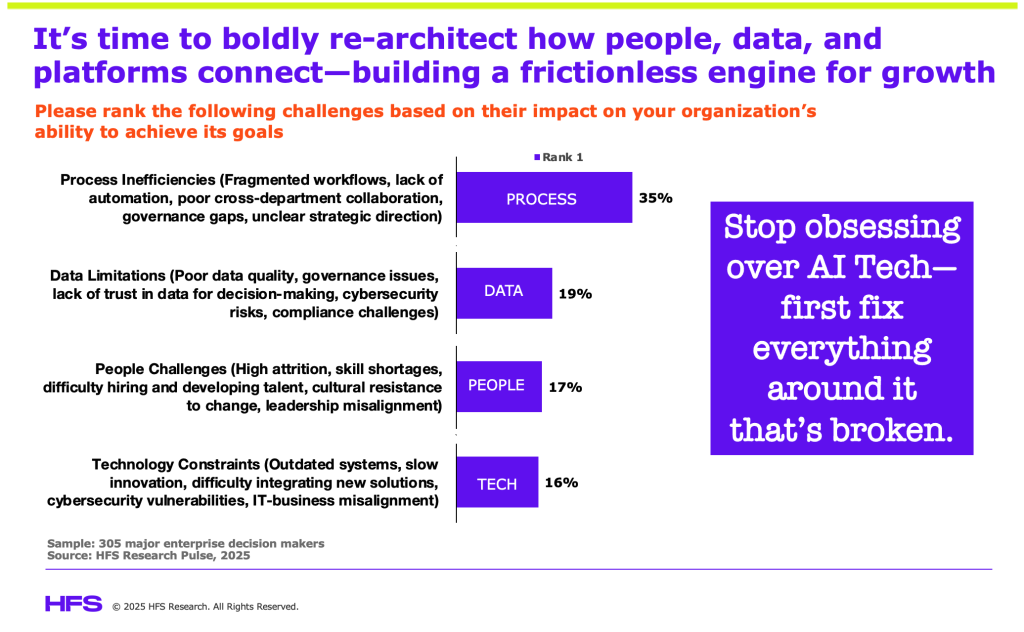

As our recent research across the Global 2000 reveals, the issue with AI transformation isn’t the tech, but the archaic processes that are failing to create better data to make decisions. It’s also the failure of leadership to train their people to rethink processes and be aware of the real business problems they are trying to solve. While so many stakeholders obsess with technical debt, the real change mandate is to address process, data and people debt to exploit these wonderful technologies:

For enterprises: Pick one high-stakes category such as government reports, regulatory filings, audit outputs, or financial models. Build airtight disclosure and verification there first, then scale the approach.

For service providers: Target practices using AI heavily. Make documented verification an essential mandate to client delivery. Track error types and use them to improve prompts, retrieval methods, and quality checklists continuously.

The leaders separating progress from scandal are those who embed quality control at the start, not those scrambling to bolt it on after public failure.

Regulatory crackdowns are coming and 60% of firms have no AI governance plan

Courts are already adjusting. US judges have begun issuing standing orders that require lawyers to certify whether filings used generative AI and to verify any AI-drafted text. The UK High Court has warned that submitting fictitious AI-generated case law risks contempt or referral to regulators. At the policy level, NIST has published its Generative AI Profile as companion guidance to the AI Risk Management Framework with concrete control actions organizations can adopt now.

Governments burned by AI blunders will introduce binding standards. Professional associations will issue mandatory guidelines. Clients will add AI clauses to every contract with real penalties. The firms that move now, investing in transparency, training, and verification, will win trust and market share. The rest will be litigating their way through the next cycle of embarrassment.

We are in a period where AI capability has outpaced corporate discipline. Old QA checklists miss AI-specific failure modes like hallucinations and fake citations. Old pricing models ignore the real cost of verification overhead. Old disclosure norms hide behind marketing language that protects no one.

Bottom line: AI without verification is outsourcing judgment to a system that confidently invents facts.

Deloitte’s scandal is not an outlier. It is the first major warning shot of a much larger credibility crisis coming for every industry. The shift to Services-as-Software and Vibe-Coded enterprises is about replacing legacy human-only workflows with intelligent, accountable, and transparent ones that combine machine efficiency with human integrity. Build this discipline into your operating model now or explain the next scandal later when your name hits the headlines.

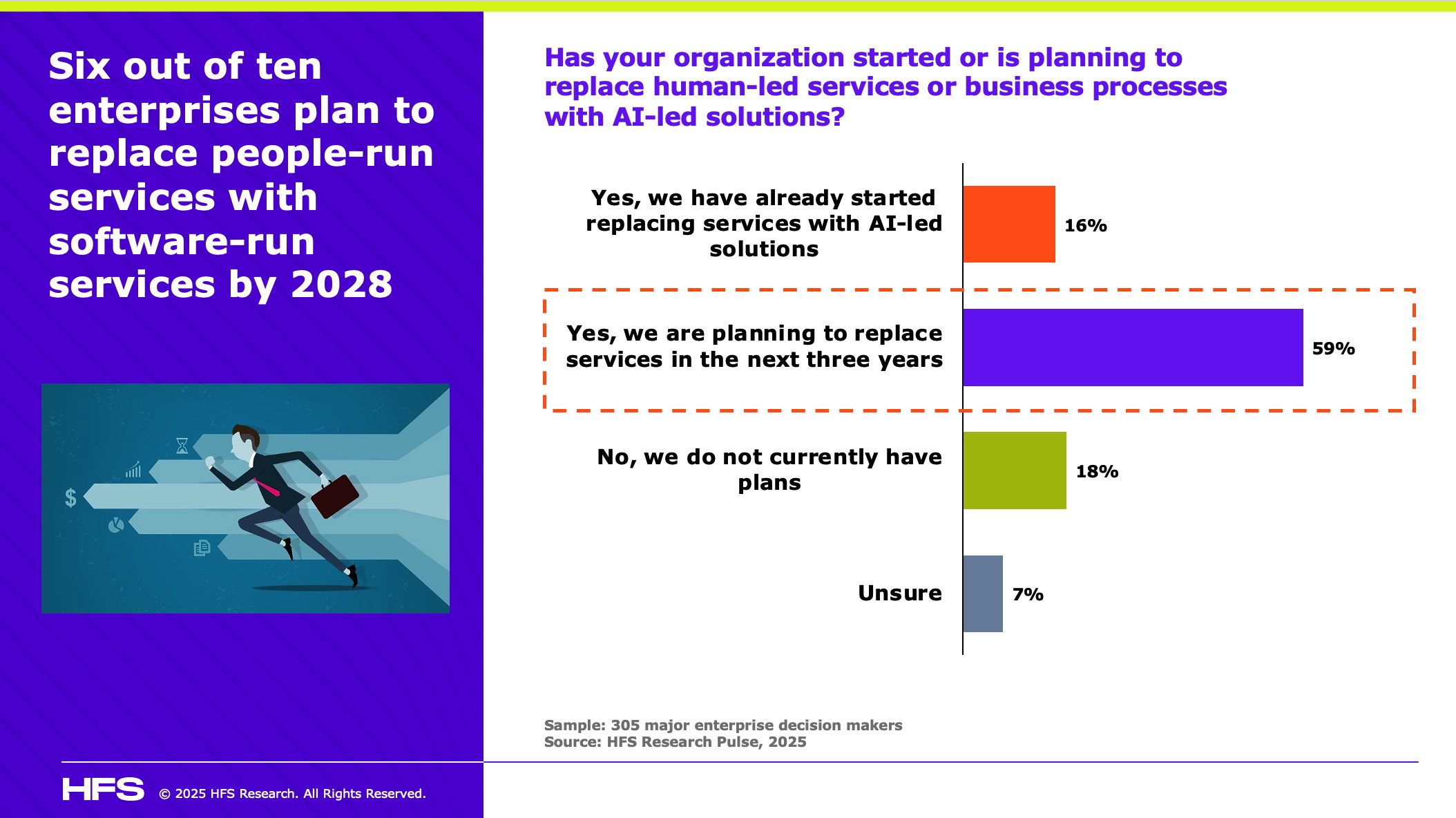

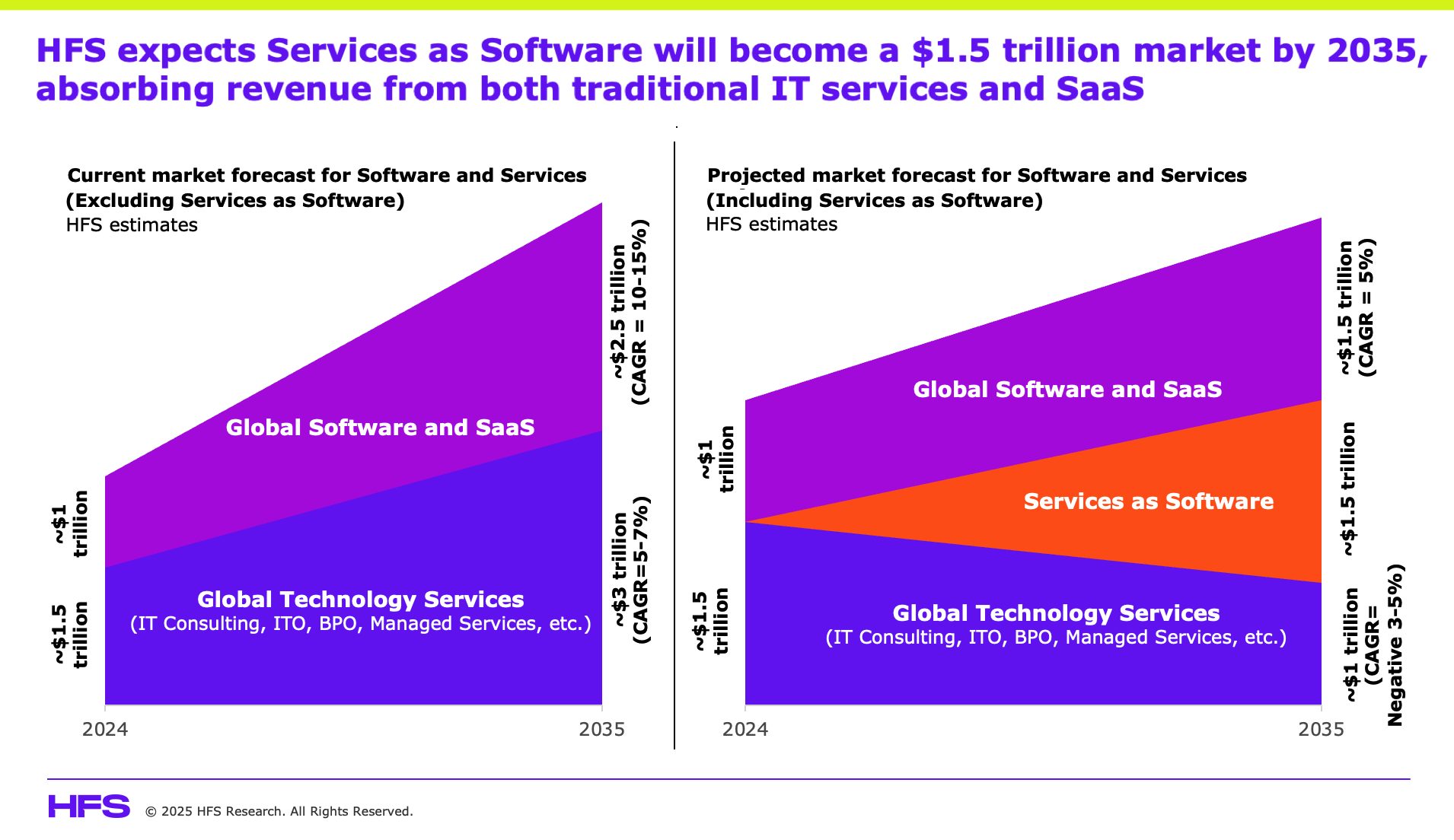

Within three years, two-thirds of Global 2000 enterprises intend to replace human-heavy IT and BPO services with AI-driven delivery. At HFS, we are terming this Services-as-Software (SaS) and view the rapid progress of AI Agents, Large Language Models (LLMs) and, ultimately, Vibe Coding as the three technological catalysts to make this happen:

Why Services-as-Software will render many traditional services and software providers obsolete

Services-as-Software (SaS) is the fusion of software and services into AI-powered, outcome-driven platforms that continuously learn and adapt. SaS replaces static SaaS and labor-heavy consulting with autonomous digital service layers that deliver expertise and execution in real time. SaS will eventually render traditional labor-based professional services and traditional SaaS providers obsolete, replaced by scalable AI Agents that deliver outcomes, not hours or licenses.

SaS is an emerging enterprise model where human-delivered services are redesigned as intelligent, automated, and continuously adaptive software entities. Instead of buying static SaaS licenses or paying for labor-intensive services, enterprises consume AI-native service layers that blend automation, reasoning, and execution into outcome-based solutions.

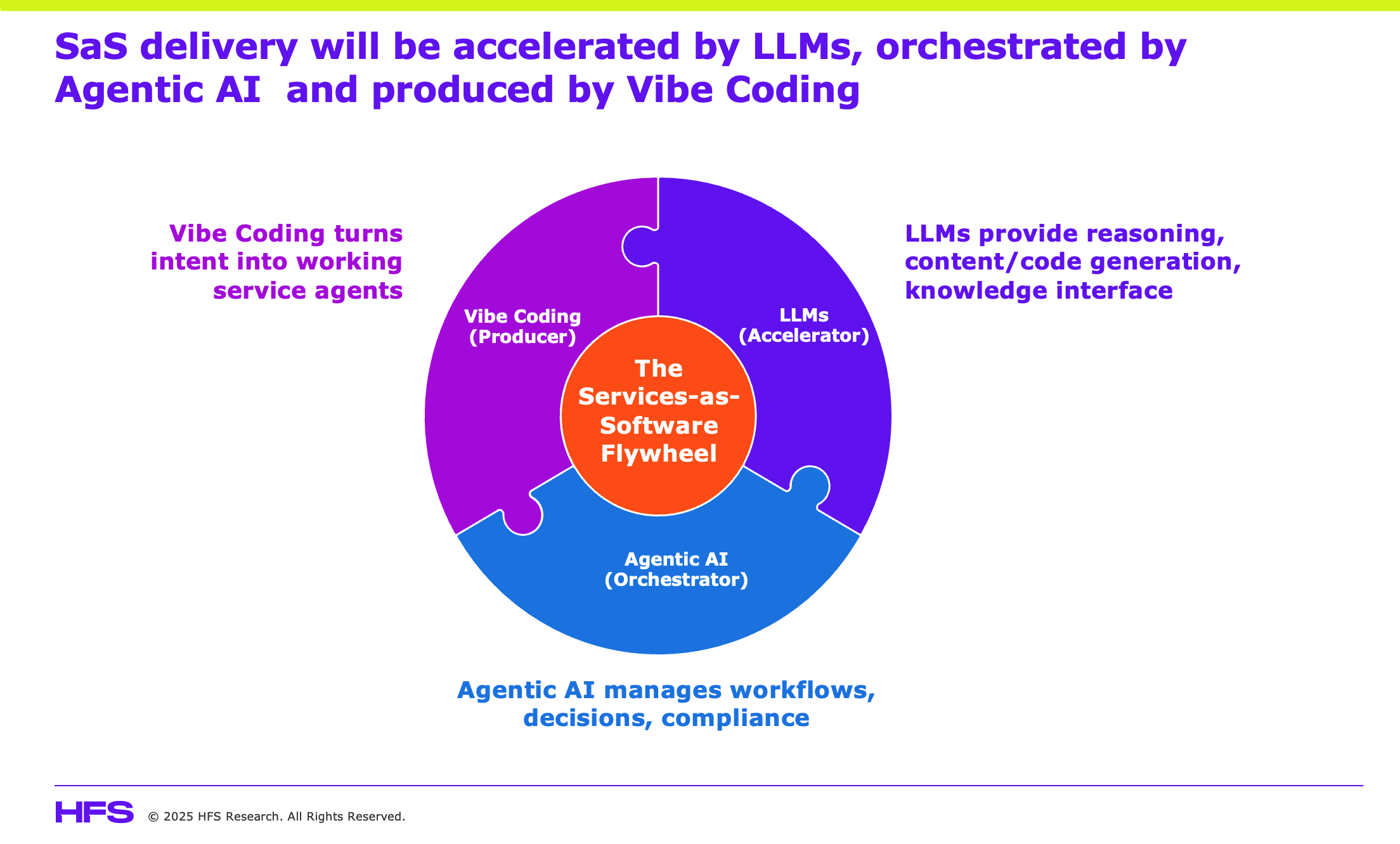

SaS delivery will be accelerated by LLMs, orchestrated by Agentic AI, and produced by Vibe Coding

Services scaled in the past by combining talent with common tech platforms. In the SaS era, the same principle applies, but talent now needs deeper business context to unlock the value of common AI platforms.

Vibe Coding provides speed and intent, but it is the fusion with LLMs and Agentic AI that makes SaS sustainable:

LLMs are the accelerator. It automates content, code, and workflow generation. Customers are already using it to shrink delivery cycles, generate reusable IP, and cut the cost of software testing.

Agentic AI is the orchestrator. Multi-agent systems manage tasks, test outputs, retrain models, and monitor compliance. We see banks piloting agent-based compliance checks and insurers using them to orchestrate claims processing without armies of analysts.

Vibe Coding is the production engine. It anchors intent-driven builds that can be refined, secured, and deployed like products. Large retailers are now expecting working demos within days of an engagement, driven by Vibe Coding copilots.

Together, these three AI constituents are replacing traditional FTE billing with subscription-based services, predictable costs, and outcome-linked value:

SaS blurs the line between software and services to form a $1.5 trillion industry

Like services, SaS delivers expertise and decision-making. Like software, it is automated, scalable, and subscription-based. But unlike either, it is dynamic, self-learning, and outcome-driven. This new category will absorb spend from both traditional SaaS and IT services, creating a $1.5 trillion market over the next few years, where enterprises stop paying for headcount or static tools and instead subscribe to AI-powered, adaptive outcomes:

Vice Coding is a new programming style that emphasizes rapid, intuitive and low-ceremony development. Developers and business stakeholders co-create with AI copilots through natural language, moving directly from intent to working code. It’s fast, conversational, and adaptive, designed for a world where software and services are fusing into dynamic, AI-driven outcomes. At HFS, we believe Vibe Coding will become the production engine behind the emerging Services-as-Software model, and we won’t even be calling it “vibe coding” in the future. It will all be about writing syntax to frame problems and design solutions. Let’s investigate further…

Vibe Coding offers the opportunity to realize the HFS OneOffice vision

For decades, business and IT have operated in silos — business leaders drafting requirements, IT translating them months later into code. This gap has slowed innovation and reinforced the divide between the front, middle, and back office.

Vibe Coding offers the opportunity to realize the HFS OneOffice vision. By enabling business stakeholders and developers to co-create with AI copilots in natural language, it collapses the wall between business intent and technology execution. Instead of handoffs, enterprises move in real time from idea to outcome. This is where business and IT finally come together as OneOffice: a unified, adaptive enterprise where technology and talent co-orchestrate value creation.

Those enterprises that simply think they can bolt on agentic technologies to their existing processes are quickly learning that this adds minimal value. It is like bolting a Tesla battery pack onto a lawnmower, where you can brag about the tech, but it will not cut the grass any faster. To gain the maximum benefits from AI technologies, business executives must work closely with their IT counterparts to design processes that generate the right data, make smarter decisions, and train people to use the technology effectively. The way we work is changing, both in terms of how processes function and how our roles need to broaden, as so many of our current tasks are improved or even replaced by AI.

Vibe Coding is not a lab experiment

Vibe Coding emphasizes speed, intuition, and iteration over rigid, process-heavy development. By reducing dependence on upfront design and exhaustive documentation, Vibe Coding enables teams to move directly from intent to working code in a conversational, adaptive way that aligns with the fast, fluid needs of modern enterprises.

Start-up funding organization Y Combinator reported that a quarter of its Winter 2025 startups had codebases that were 95 percent AI-generated. Production-ready components are now being built in hours instead of weeks. Governance, compliance, and security can be embedded into the codebase from the outset. Services, like software releases, can be built once and reused across multiple customers instead of bespoke projects. The consequences for service providers are profound.

Vibe Coding is the production engine that turns Services-as-Software from vision to reality

Services operated in the past by combining talent-at-scale with common tech platforms. In the SaS era, the same principles apply, but the talent needs deeper business context to unlock the value of common AI platforms.

Vibe Coding provides speed and intent, but it is the fusion with LLMs and Agentic AI that makes SaS sustainable:

LLMs are the accelerator. It automates content, code, and workflow generation. Customers are already using it to shrink delivery cycles, generate reusable IP, and cut the cost of software testing.

Agentic AI is the orchestrator. Multi-agent systems manage tasks, test outputs, retrain models, and monitor compliance. We see banks piloting agent-based compliance checks and insurers using them to orchestrate claims processing without armies of analysts.

Vibe Coding is the production engine. It anchors intent-driven builds that can be refined, secured, and deployed like products. Large retailers are now expecting working demos within days of an engagement, driven by Vibe Coding copilots.

Together, these three AI constituents are replacing traditional FTE billing with subscription-based services, predictable costs, and outcome-linked value.

Enterprises mustn’t approach SaS as another outsourcing wave.

SaS is a new operating model and ambitious enterprise customers now expect working demos early in engagements, are exploring outcome-based contracts, and demand transparency on AI governance and intellectual property. This is the SaS vision coming to life in real time.

Smart enterprise leaders must stop measuring value in FTE counts and start anchoring contracts to speed, reuse, and reliability. That means asking providers for subscription-style pricing and demonstrable reuse of code and IP, not endless custom builds. It also means insisting on AI governance frameworks that explain how models are trained, how code is validated, and how intellectual property is protected.

CIOs must pivot their own talent strategies too. Developers and architects need to work with Vibe Coding and agentic systems rather than compete with them. Enterprises that invest in prompt engineering, AI-era architecture oversight, and code validation will extract the most value. Those that do not risk being locked into black-box services they cannot control or trust.

A global bank recently shifted from a traditional outsourcing contract to a SaS model for customer onboarding. Instead of hundreds of developers coding workflows, the provider now delivers an AI-powered onboarding service on subscription. Vibe Coding enables rapid iteration of new compliance checks, GenAI auto-generates the documentation, and Agentic AI monitors process accuracy. The bank gets faster releases, lower costs, and auditable governance, without the FTE treadmill.

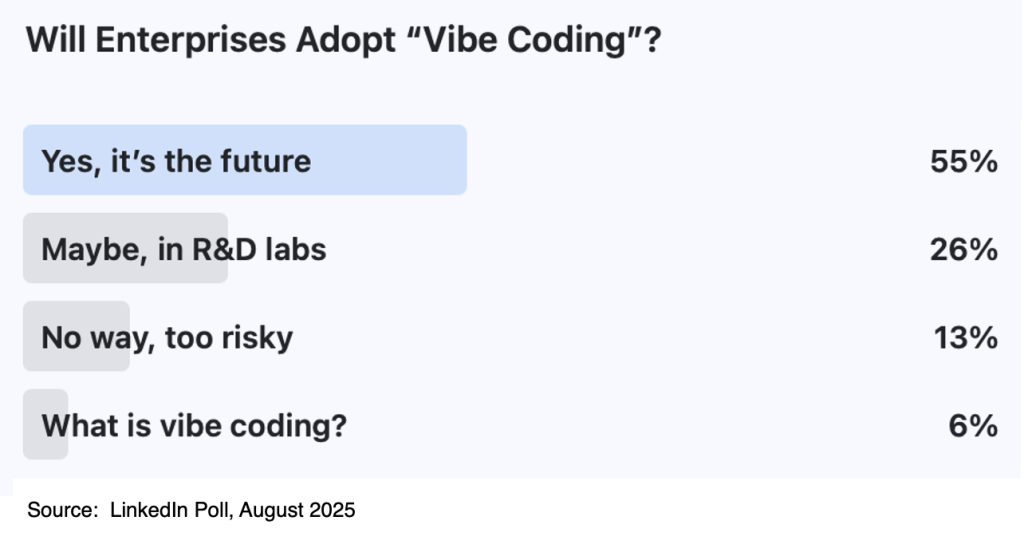

Is vibe coding ready for prime time? Or stuck in lab?

To test the waters, we recently ran a LinkedIn poll asking: “Will enterprises adopt Vibe Coding?”

The results highlight both momentum and hesitation. The majority clearly see Vibe Coding as inevitable, drawn by its speed, adaptability, and ability to turn ideas into working code in days instead of months. Younger developers in particular are energised by its low-ceremony, conversational style, which plays to their comfort with AI-first tools.

But there is a tale of caution in the poll as well. Those who view Vibe Coding as risky because of:

Governance & compliance gaps. Regulators and enterprises worry about how to audit code that is 95% AI-generated.

Black-box outputs. Without explainability, enterprises fear vendor lock-in and an inability to validate outcomes.

Talent disruption. Senior developers may resist low-ceremony, AI-first practices that threaten traditional roles.

Security concerns. Copilots and LLMs trained on broad datasets raise questions about vulnerabilities and IP leakage.

Cultural inertia. Shifting from documentation-heavy processes to conversational coding requires a new mindset that not all enterprises are ready for.

These concerns don’t negate the momentum, but they underline that adoption will depend on embedding governance, explainability, and trust at the core of Vibe Coding practices.

Recommendations for Enterprise Customers

Shift contracting models. Move from FTE billing and static SaaS licenses to subscription-style, outcome-linked services.

Invest in talent. Build new skills in prompt engineering, AI-era architecture, and code validation. Encourage younger talent to lead experiments with Vibe Voding, since they adapt fastest to conversational, AI-first ways of building.

Demand transparency. Require providers to demonstrate AI governance frameworks, data lineage, and intellectual property protection.

Push for reuse. Ask providers to deliver modular service components that can be reused across the enterprise, not bespoke one-offs.

Pilot fast, scale faster. Expect working demos in days, not months, and measure providers on speed, reuse, and reliability.

Recommendations for Service Providers

Retire the labor pyramid. Replace headcount-heavy delivery with AI-first, productized service agents built through Vibe Coding.

Embed governance at the core. Bake compliance, security, and auditability into AI services from the outset.

Industrialize Vibe Coding. Make copilots standard for all delivery teams and use young developers as the frontline to accelerate builds and generate reusable IP.

Rewire pricing. Shift to subscription-based models that monetize outcomes, not hours.

Partner widely. Team with hyperscalers, LLM vendors, and AI-native startups to co-create SaS offerings.

Recommendations for Traditional SaaS Firms

Move beyond licenses. Static SaaS will be cannibalized. Pivot toward adaptive, AI-powered service layers that evolve continuously.

Fuse with services. Collaborate with service providers to create co-delivered SaS platforms.

Embrace Vibe Coding ecosystems. Open your platforms so developers, especially younger talent, can use AI copilots to extend and customize products in real time.

Differentiate on trust. Put governance, privacy, and explainability at the center of your value proposition.

Accelerate open platforms. Build marketplaces where Vibe Coding, Agentic AI, and LLM-powered agents extend your applications with speed and creativity.

Bottom line: Embrace vibe coding. Don’t fear it.

Vibe Coding is the production engine that makes Services-as-Software real, and it will decide the winners of the next decade. Enterprises can no longer afford to treat AI as bolt-ons or outsourcing-lite. SaS is a new operating model where AI agents, LLMs, and Vibe Coding collapse the gap between software and services, shifting the economics of IT from people and licenses to reusable, outcome-based digital service layers.

The real risk isn’t that Vibe Coding will fail; it’s that enterprises will fear it and do nothing, clinging to incremental improvements that are only slightly better, faster, or cheaper. Those who adapt now will own the future $1.5 trillion SaS market. Those who don’t will be stuck optimizing the old world, while others reinvent the new one.

To conclude, Vibe Coding is a new mindset that energizes young talent and accelerates the shift from human-run services to software-run outcomes. Enterprises, providers, and SaaS firms that embrace this culture will define the $1.5 trillion SaS market.

The future of the analyst industry is here, but most of its stakeholders are simply not ready. You only need to see the stock price carnage of Gartner and Forrester to realize the analyst and advisor industry are in grave danger of being runover by AI.

The Futurum Group CEO, Daniel Newman, and I take a hard look at the future of the analyst industry in the era of ChatGPT-5 and agentic AI.

We discuss how AI is dismantling legacy models built on slow inquiry processes, paywalled reports, and expensive AR programs, replacing them with instant, on-demand insights. Analyst firms, especially the large, entrenched players, must reinvent themselves fast, shifting from rear-view research to forward-looking influence, proprietary data, and authentic personal brands.

➡️ Our conversation covers:

*Why AI is making traditional analyst deliverables (Magic Quadrants, long reports) less relevant

*The need for speed, authenticity, and personality to stand out in a market drowning in AI-generated content

*How smaller, nimble firms can outpace large incumbents by moving faster and building direct influence

*The decline of AR’s traditional role as a concierge between vendors and analysts

*The genuine risk of irrelevance if the industry fails to adapt within 18 months

Bottom line: The analyst business has arrived at its “Blockbuster moment.”

Adapt quickly, embrace AI, and build genuine influence or be replaced by faster, cheaper, and better alternatives. Enjoy!

Layoffs are accelerating again, but this time AI is becoming the cover story, offering a convenient narrative to justify long-delayed changes under the guise of technological progress.

Microsoft, Amazon, Citigroup, UPS, Google, McKinsey, Deloitte, PwC, and many others have all recently laid off staff under the AI smokescreen. The headlines say it is about automation and AI readiness, but that is not the whole story… not even close.

What we are seeing is not just automation-led efficiency, it is a structural shakeout triggered by board pressures to cut costs, eliminate underperforming middle layers, and move away from legacy talent strategies. The corporate world has also experienced high-wage fatigue, where many staff have had significant wage growth, especially since the inflationary pandemic years, and it’s simply very expensive to maintain staff on these high salaries and other benefits.

Many of these firms have been waiting for an excuse for years to trim their fat, and now they have it. We will, however, give some credit to TCS’s CEO Krithi, who positioned their recent “restructuring initiative as being aimed at transforming the company into a future-ready organization.” At least there is some admission here that many staff at mid-senior levels were no longer delivering value in a challenging market environment, and it was time to trim the fat. Not one mention of AI…

You can run from your past, but it will catch up with you if you can’t change your habits

Companies are making moves they have postponed for years. Cuts labeled as future-proofing are often strategic resets that should have happened long before AI showed up. Yes, some AI deployments are proving valuable. But not at the scale required to displace tens of thousands of roles overnight.

In fact, we were having exactly the same conversations when RPA was hyping markets a decade ago, but the technologies couldn’t scale up and deliver like what we are witnessing with GenAI and agentic. It is easier to blame emerging tech than to admit to dysfunctional processes, poor-quality data, bloated hierarchies, poor skills development, or misaligned workforce structures.

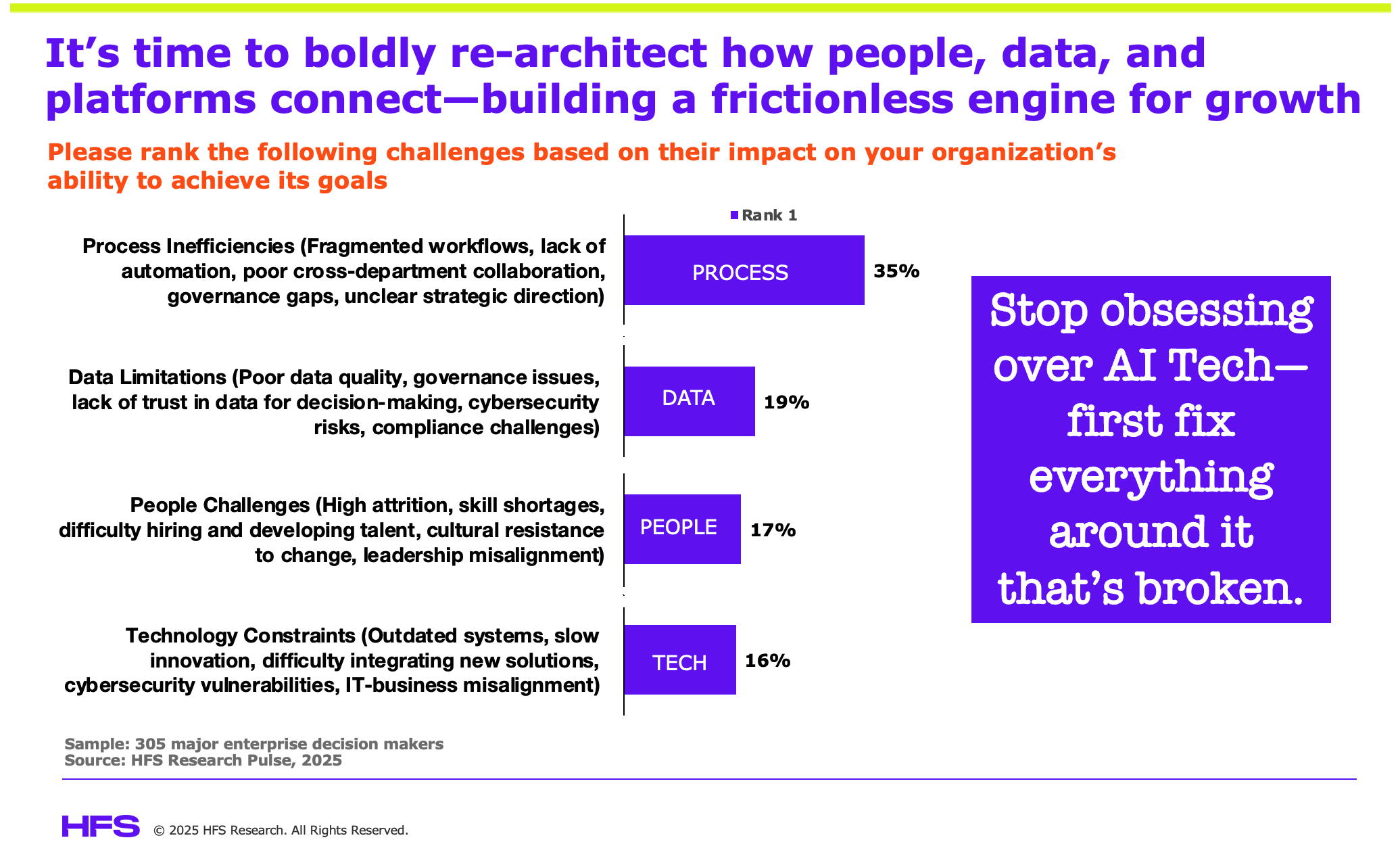

Recent research (below) clearly shows that the issues plaguing major enterprises in achieving their goals are not technology constraints but all the non-technical areas that are blocking the ability to exploit AI:

Leaders need to stop pretending all of this is an AI transformation. This is not an overdue cleanup… it is a premature dismantling of work structures without the foundations for what comes next. What is clear is that you will fail with AI if you do not focus on your processes, data, and people first.

Cutting early-career talent creates long-term fragility and trashes your culture

Some of the clearest signals are coming from the firms that once defined the pyramid talent model: the big four. Deloitte, EY, PwC, and KPMG have sharply reduced graduate recruitment, with cuts as high as 44 percent compared to last year. At the same time, mid-level roles are being protected, senior compensation is climbing, and administrative tasks are being offshored to lower-cost hubs.

The rationale? AI can automate a lot of entry-level work. But AI is not ready to own this work at scale, and many of these roles were not just about task execution, they were about long-term capability building. Cutting them removes a foundational layer of growth, learning, and leadership development. It weakens succession pipelines, institutional knowledge transfer, and creates brittle organizations with no buffer to absorb future shifts.

This pattern is not limited to the big four. The US government is accelerating generative AI pilots while significantly cutting civil service positions. Media organizations like Business Insider are adopting AI-first strategies while laying off large portions of their newsrooms. B2B companies are reducing headcount in marketing and sales functions in anticipation of productivity gains that have yet to fully materialize.

Yet few of these decisions are supported by robust evidence of AI delivering sustainable value at scale. Instead, many are driven by cost-cutting mandates, simplification goals, and boardroom pressure. AI is being positioned as a convenient explanation for broader organizational shakeouts.

Crucially, early-career roles are not collateral damage, they are a deliberate target. Firms are pulling back on graduate and entry-level hiring, assuming that AI will render those jobs unnecessary. But AI can only automate fragments of work, not own entire workflows. These junior positions were never just task execution lanes—they were foundational to future leadership development, capability building, and institutional continuity. Eliminating them puts long-term organizational stability at risk. We are not just trimming headcount, we are erasing the scaffolding of future expertise.

Smart enterprise leaders are leaning into both young talent and emerging AI opportunities together

Enterprise leaders should proactively invest in young talent by aligning graduate recruitment with evolving skill requirements, emphasizing continuous learning, and developing pathways that enable graduates to work creatively and effectively with AI tools. Lean into both by creating roles that complement AI—focusing human effort on critical thinking, creativity, ethics oversight, process and systems governance, and innovation management.

The US, for example, has several robust training initiatives underway to support AI workforce development. These include NSF-funded National AI Research Institutes focused on sector-specific skills, the Department of Labor’s AI Apprenticeship Program emphasizing practical AI training, the Department of Commerce’s AI Centers of Excellence facilitating industry partnerships, and Workforce Innovation Grants aimed at boosting AI education in community colleges and regional institutions.

The work has not been redesigned, only reduced

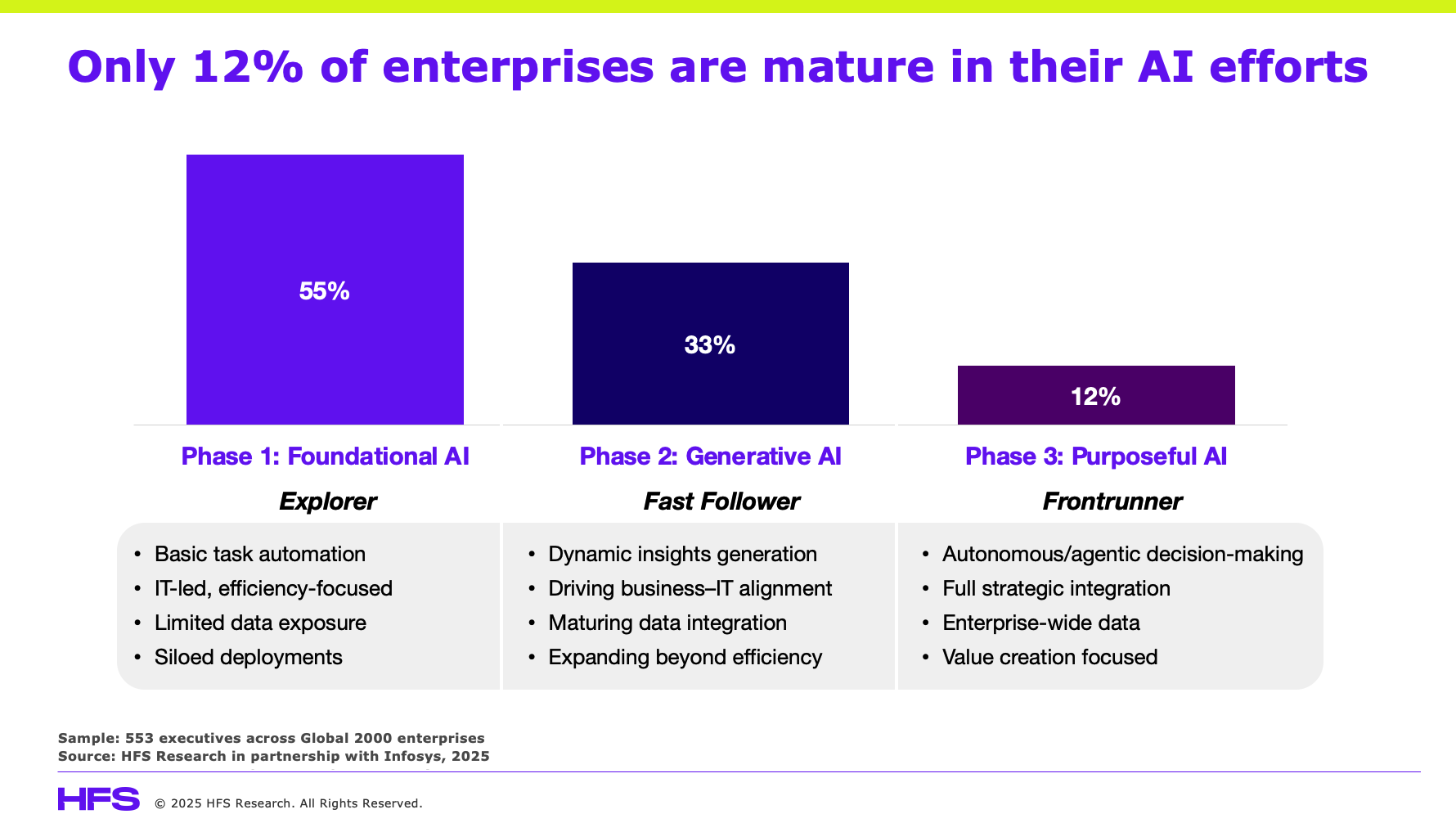

Here is the real risk. Enterprises are shrinking their workforce without reshaping the work. The assumption is that AI will simply fill in the gaps. However, only 12 percent of organizations report a somewhat mature level of AI readiness, and most of them acknowledge that they have a long way to go (see exhibit below). That makes the scale of workforce cuts hard to justify on the basis of actual deployment.

Most of the AI used today still relies on human orchestration, supervision, and refinement. Few enterprises have established clear handoffs between agents and people, and even fewer have rearchitected workflows to reflect new levels of autonomy or human-AI collaboration:

We are clearing out talent faster than we are designing the next delivery model, and that creates exposure, inconsistent outcomes, and over-reliance on immature systems. Fragile operating models are held together by duct tape, not by design.

This is not the AI revolution most leaders say they are preparing for. It is a pause on hiring disguised as foresight. A reversion to old cost takeout habits, rather than a step toward adaptive work models.

Where enterprise leaders now need to focus

If you are an enterprise leader watching this unfold, it is time to move beyond reactive cycles. Here is where to focus instead:

Map the work, not just the roles. Understand what outcomes your teams are responsible for and where AI can assist rather than own it. Decompose the work before deciding who or what should do it.

Stop hollowing out your future talent. Reducing early-career roles may create short-term savings but also destroy long-term agility. Invest in hybrid learning environments where new talent can collaborate with AI systems and senior mentors.

Redesign for orchestration. Do not just implement AI tools. Build systems around them that define how work is triggered, handed off, evaluated, and evolved. Think beyond productivity into reliability and resilience.

Ground your decisions in data, not buzz. Track what AI is actually delivering, where it saves time, reduces errors, or enhances quality. Make staffing decisions based on this evidence, not aspiration.

Challenge your narrative. If you are using AI as the justification for layoffs, be honest about what is really driving the shift. Employees, customers, and shareholders are watching and expecting more than spin.

This is not about being anti-AI. It is about building enterprise systems and workforces that are designed for what is coming, not just shedding what is familiar. AI may be the accelerant, but the redesign is still up to us.

Bottom line: Stop optimizing for a future you have not yet built

Enterprises are rushing to cut headcount for AI efficiency without having done the work to understand what good looks like. Most have not redesigned roles, workflows, or orchestration layers. They are simply hoping that fewer people plus more tech will equal progress. That is not a strategy; it is a gamble.

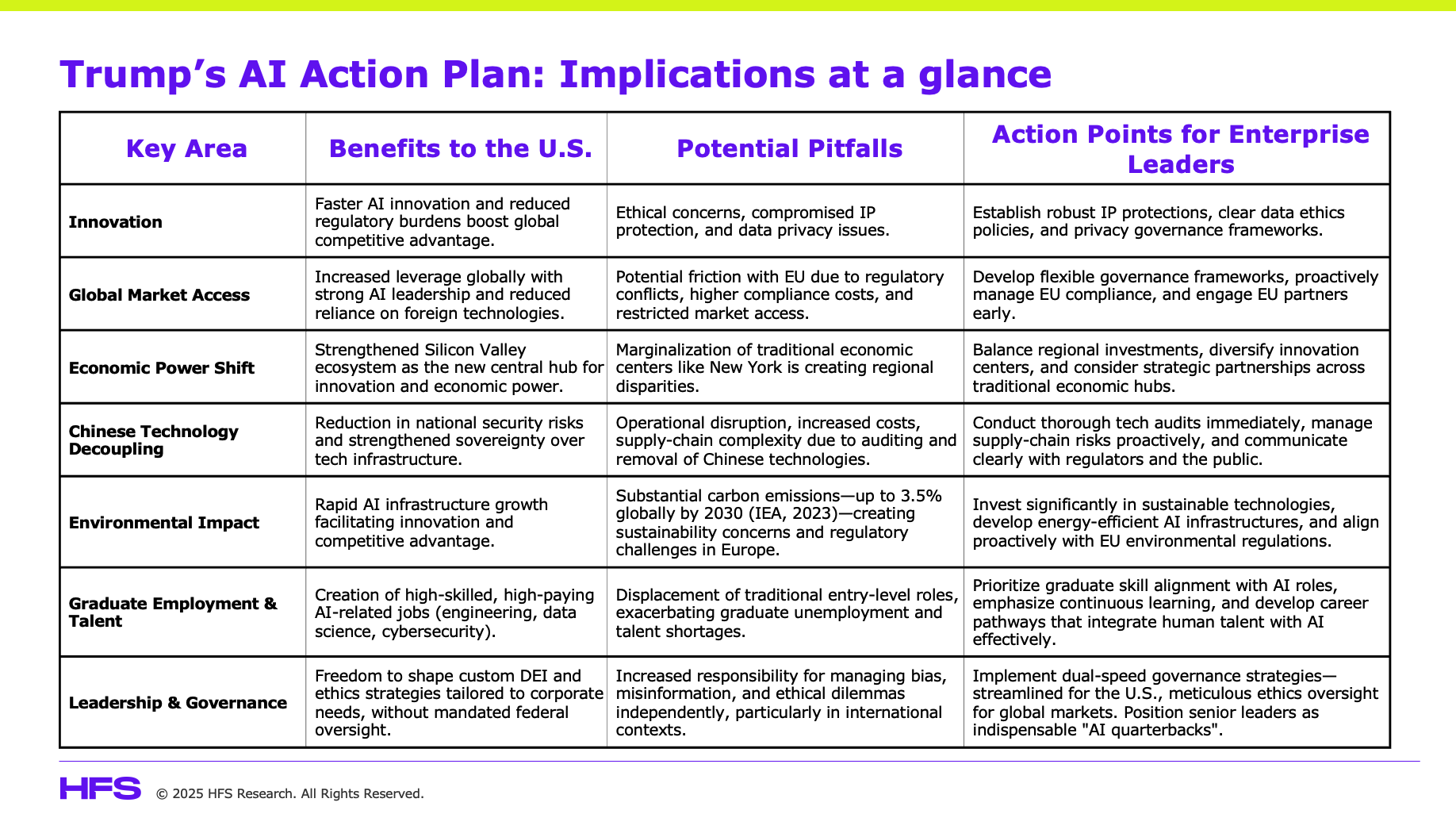

Love him or loathe him, let’s be clear… President Trump’s new AI Action Plan isn’t just political theatre, it’s a strategic sledgehammer aimed at reshaping the global AI landscape in America’s favor. This is your wake-up call, whether you’re leading a tech firm or steering an enterprise. Align with the American AI stack, or prepare for a long ride in the slow tech lane.

Accelerating innovation and removing regulatory shackles

America is taking its foot off the regulatory brakes, although this could amplify ethical risks, reduce content protection, and potentially compromise data privacy as it seeks to become the undisputed AI leader. Trump’s vision is simple: remove barriers, build massive infrastructure, and force global alignment with US-controlled AI tech stacks and data centers. Forget subtlety, this is an aggressive, competitive manoeuvre driven by Trump’s showman antics!

Silicon Valley becoming America’s power center

With copyright protections sidelined and regulations slashed, the Valley is primed to dominate this AI-fuelled gold rush. However, this raises critical concerns, namely uncontrolled content exploitation by AI bots that could severely damage intellectual property rights, trigger extensive copyright litigation, and create significant ethical dilemmas related to data privacy and fairness. Additionally, this push reinforces a significant power shift toward Silicon Valley and away from traditional economic hubs like New York, further consolidating influence around tech giants at the expense of traditional finance and media sectors.

America’s free-for-all approach is in stark contrast to Europe’s regulatory quagmire

Europe’s AI Act emphasizes caution, human oversight, and sustainability, which could prove to be deadly slow in the AI arms race. Trump’s strategy couldn’t be more opposite by promoting innovation, accelerating infrastructure, and accepting (or just ignoring) inherent risks. For ambitious enterprises seeking to drive AI-first business and talent strategies, the choice is stark… bet on the fast-moving, albeit riskier, American stack or struggle through Europe’s costly and stodgy compliance maze.

This AI Action Plan could also create challenges for American firms dealing with European firms, in terms of meeting their compliance requirements, potentially increasing operational complexity and legal risks. Also, with Europe tightening controls and potentially imposing import taxes on tech services from countries not complying with its regulations, American enterprises might face higher costs, restricted market access, or increased scrutiny when serving European customers.

To mitigate these issues, American enterprises should proactively develop flexible, robust governance frameworks capable of adapting to both markets, clearly communicate compliance and ethical strategies, and engage directly with European partners to address potential concerns early.

Audit your tech stack immediately for Chinese influence

With Trump’s renewed emphasis on national security, enterprises must urgently audit their tech stacks. Firmware, data sources, and LLMs originating from China, such as DeepSeek, ERNIE Bot, Manus Tongyi Qianwen, 360 Zhinao, SenseFace, and Tencent, will be considered toxic. Be ready to answer regulators’ tough questions or face uncomfortable public scrutiny. Keep in mind, however, that auditing and removing Chinese technology can present significant operational challenges, including service disruptions, increased costs, and potential supply-chain complexities.

Take charge of your DEI and ethics strategy independently

The Trump administration is explicitly stripping DEI and ethics mandates from federal frameworks. This gives enterprises both freedom and responsibility, where US firms must now manage their own bias and misinformation risks, especially when operating internationally. Prepare for a dual-speed governance approach that tackles streamlined security for the US market with meticulous ethics and compliance for Europe.

Address the environmental cost of rapid AI expansion

The global environmental impact of AI infrastructure growth is immense. AI data centers alone could account for up to 3.5% of global carbon emissions by 2030 (source: International Energy Agency, 2023), which is even more than the emissions from the global aviation industry today. Enterprises racing to expand their AI capabilities must grapple with sustainability concerns as energy consumption and environmental footprints skyrocket.

American firms relying heavily on carbon-intensive AI infrastructure could struggle to comply with EU sustainability requirements. This scenario could raise operational costs significantly, making American solutions less competitive or less attractive to European partners who prioritize sustainability compliance.

Lean into both your developing human talent and AI ambitions to create a unique company culture and identity

The AI Action Plan presents significant implications for graduate employment and entry-level jobs in particular. On the positive side, increased investment and rapid innovation in AI technology will likely create new categories of high-skilled, high-paying jobs, particularly in AI engineering, data science, and cybersecurity. Graduates who acquire specialized AI-related skills will have considerable advantages in the job market.

However, there’s also a downside. Automation and AI could displace entry-level positions traditionally filled by recent graduates, potentially exacerbating graduate unemployment rates and creating a gap in career pathways. Enterprise leaders should proactively invest in young talent by aligning graduate recruitment with evolving skill requirements, emphasizing continuous learning, and developing pathways that enable graduates to work creatively and effectively with AI tools. Lean into both by creating roles that complement AI—focusing human effort on critical thinking, creativity, ethics oversight, process and systems governance, and innovation management.

The US has several robust training initiatives underway to support AI workforce development. These include NSF-funded National AI Research Institutes focused on sector-specific skills, the Department of Labor’s AI Apprenticeship Program emphasizing practical AI training, the Department of Commerce’s AI Centers of Excellence facilitating industry partnerships, and Workforce Innovation Grants aimed at boosting AI education in community colleges and regional institutions.

Become an AI quarterback and an indispensable leader

Business leaders must proactively position themselves as indispensable AI quarterbacks within their organizations. This involves developing a deep understanding of AI capabilities, limitations, and strategic implications for your business. Act as a bridge between technical AI teams and broader organizational strategy, effectively translating complex technical details into clear business insights.

Leaders should prioritize AI literacy, invest in executive education, and champion AI-driven initiatives across all departments. Foster a culture of curiosity and agility, encouraging your teams to experiment and iterate quickly. Your ability to lead AI transformations, manage risks, create smart governance frameworks, and leverage technology strategically will make you essential to your organization’s future success.

Bottom line: Invest hard, move fast, and exploit this AI freedom

Trump’s AI Action Plan signals permission to innovate aggressively. Push the limits, break the mold, and stop waiting for global consensus. This is your moment to place your big bets on AI with Uncle Sam’s backing, which means speed and boldness trump caution and inertia. Hesitate now, and you risk irrelevance.

Today’s analysts and advisors love talking about how the speed of AI advancements is turning every industry on its head, but most conveniently ignore the fact that their own industry is getting rewired faster than they can say “disrupted.”

The analyst and advisor industries, reliant on IP and research to market their products, are in serious trouble, and many firms will cease to exist in a couple of years. I mean, whatever happened to the likes of Omdia or 451? They already seem to have melted away into insignificance under some analyst firm roll-up scheme, smashing together mediocre events, marketing, and “research”.

I’ve been fortunate to be part of the analyst and advisory industry for three decades. I can only say it’s been a privilege to be paid to learn, to engage with so many smart people, and to build many, many relationships over the years based on trust, mutual respect, and friendship.

However, there have been warning signs for a long while that the comfortable status quo is already getting very rocky (as already witnessed by Forrester’s dramatic decline). And what’s really worrying is the recent speed of development with AI platforms, agentic software, and LLMs, which is, quite frankly, making the use of analysts and advisors increasingly irrelevant.

The issues are staring us in the face:

Generative AI platforms are fast replacing the need for analyst support. Routine research tasks, such as reports summarizing trends, market sizing, vendor comparisons, or basic scenario analysis, are increasingly being automated by generative AI.

Analysts are just too slow to deliver insight. The sheer speed of GenAI is challenging analysts to justify their premium pricing and timelines. Why pay for information that sometimes takes weeks to access, or even set up a call with an analyst? We are operating in a world of immediate decision-making, and many analysts are simply not adapting.

Cost Pressures will focus many firms to prioritize their GenAI platforms: GenAI significantly lowers barriers to basic insight, and many clients are already pushing analyst firms harder to justify their obscene subscription costs. In addition, the cost of enterprise tokens for GenAI platforms is pushing many CFOs to look at offsetting against legacy research costs. If you’re spending $500K+ a year on your enterprise OpenAI access, you’ll want to offset this against existing information costs, which will likely include analyst subscriptions.

Analysts are losing authenticity. So much analyst output today has become so jargonized that many research consumers are simply switching off. Who wants to hear the constant regurgitation of meaningless words like “orchestration” and “transformation”. Analysts using GenAI to craft their narrative immediately lose touch with a human audience who wants to hear something real, not more recycled nonsense.

Many analyst/advisor relations professionals are killing the analyst industry. Most tech and services firms persist in relying on prehistoric analyst relations professionals who have forgotten what “value” analysts provide to their firms. They live in a world of checking boxes for administering their executives’ briefings and justifying their large salaries by claiming they somehow drive influence and new business for their employers. I personally can’t remember the last time analyst/advisor relations professionals proactively called up analysts to understand their research agendas and craft an engagement model to get the most out of the relationship. These roles will likely get phased out in the next couple of years as the whole concept of analyst value deviates away from these transactional relationships that are becoming worthless in this age of LLMs.

In short, the whole concept of the value an analyst provides is changing very fast…

How the analyst industry can save itself

Stop cheating with ChatGPT. Now. As MIT scientists have discovered, do not use ChatGPT for your writing if you want to avoid accumulating Cognitive Debt. So if you are genuinely using ChatGPT to write your research for you, stop now. One, it will rot your brain, and many smart people can tell they are not reading the work of a human. Too many bullet points, obvious capitalization of titles, overuse of em dashes, articles that start with “in today’s challenging world…In today’s fast-paced environment” or some variation of it, overuse of short lists with bold titles. I’ve also started seeing ChatGPT-generated charts and diagrams, which don’t really make sense. Plus, some of these analyst articles sound like some corny American journalists in some blah magazine.

Dig deeper – don’t just skim the surface. Too much analysis feels like it’s been written after a quick skim of a press release and a glance at LinkedIn – too much seems generated. If you want to say anything of interest, you must get beyond the obvious. Ask the difficult questions. What’s really going on behind the trends? What are the implications people aren’t talking about? The best analysts cut through the fluff and reveal the real story – not just what happened, but why it matters and what to do about it. Bring insight, not just information. That’s how you earn trust and deliver value.

Be authentic. The one thing good analysts bring to the table is a human voice that should rise above the AI-manufactured cacophony of bullshit. They need to talk plain English to their subscribers. People are turned off by AI-generated content and the same old buzzword bingo, so rise above it, folks! Pretend you are explaining agentic AI to your Mom or the immigration officer who asks what you do for a living…

Lose the attitude. I hate to say it, but people don’t like assholes anymore. They want to like the voice they are hearing, to identify with the analyst, to learn from them, to empathize with them. They don’t want to be lectured and preached to constantly. If they identify with the analyst, they may actually pay to engage with them and get support and ideas from them. Why would you pay for a human being you don’t care about when you get your information from ChatGPT?

Just get to the bloody point. No one has time to read paragraphs of preamble these days. They need to know immediately what you are writing. The days of the waffling intellectual analyst are over. You have a tiny piece of attention-time to make your mark these days, and you need to scream to your audience why you are declaring something profound for their insight pleasure.

Invest in personal relationships – and not just with vendors. The most effective analysts today are those who have invested in their networks and relationships across their ecosystem. I can attest to the fact that you can gain from a lifetime’s knowledge from a person in an hour. Great analysts get to know the people buying technology and services, not just the ones who are marketing themselves to the buyer. You will be such a better analyst for being able to convey real buyer experiences than one who is merely parroting vendor marketing jargon. Great analysts tend to be great people with great personalities and relationships.

Use AI as an ally, not a competitor. The old saying that you won’t lose your job to AI, but to someone who can use AI better than you is VERY true with analysts. Use AI as a research assistant and sounding board, but NOT as your brain.

The Bottom-line: Be honest with yourself if you really want to stay relevant

Analysts need to accomplish three things if they want to avoid being replaced by agents and LLMs:

Influence people. You need to convince people that your experience and views matter, and that they actually follow you.

Advise people. You need to convince people that your research and wisdom matter, and they actually listen to you.

Connect people. You need to prove to people you have a great network of stakeholders across your value ecosystem, so they actually want to know you and spend time with you.

The traditional lines between CPG brands and retailers are blurring, with brands engaging consumers directly and retailers elevating private-label products to international rivals. The global supply chain instability is pushing them toward diversification for greater resilience. These firms are battling multiple fronts—margin pressure, shifting consumer preferences, operational complexity, and a relentless technology drumbeat. While the noise around GenAI, automation, and omnichannel disruption is deafening, executives are shooting sharper questions: What investments actually matter? Where should we double down now? What’s worth betting on for the future?

The lion’s share of tech budgets remains anchored in traditional strongholds: cloud computing (26%) and analytics (21%), which collectively command nearly half of all enterprise tech spending. But the real surprise lies in the swelling appetite for new-age AI: GenAI (10%) and agentic AI (7%), which now outpace traditional AI (6%) and underscore a dramatic pivot in enterprise AI adoption narratives. RPA and intelligent automation are still much alive (9%). Meanwhile, emerging tools such as blockchain and digital twins hover at the margins, but their moment may be approaching.

90% of IT and business services outsourcing spend maps to the eight domains of the HFS retail and CPG value chain. Over 56% is concentrated in just four areas: Data-driven product innovation, omnichannel CX, resilient operations, and immersive marketing and customer engagement.

Investments that clearly demonstrated business value and are now ready to scale include:

Personalization, driven by AI recommendation engines and GenAI content creation, is delivering a double-digit revenue uplift per user. Retailers using tools such as Salesforce Einstein or Adobe Target are driving higher conversion rates and increased loyalty.

Omni-fulfillment strategies—including BOPIS (buy online, pick up in store), curbside pickup, and ship-from-store—are now foundational, supported by cloud-based inventory management and AI-driven demand forecasting. Enterprises mastering this coordination enjoy 30% higher customer lifetime value.

Micro-fulfillment centers are helping to meet the growing demand for same-day delivery in urban markets, while bonded warehouses are improving global cash flow and customs agility.

Data-fueled product innovations, such as private-label SKUs based on trending ingredients or unmet category demands, is cutting time-to-market and improving launch success rates.

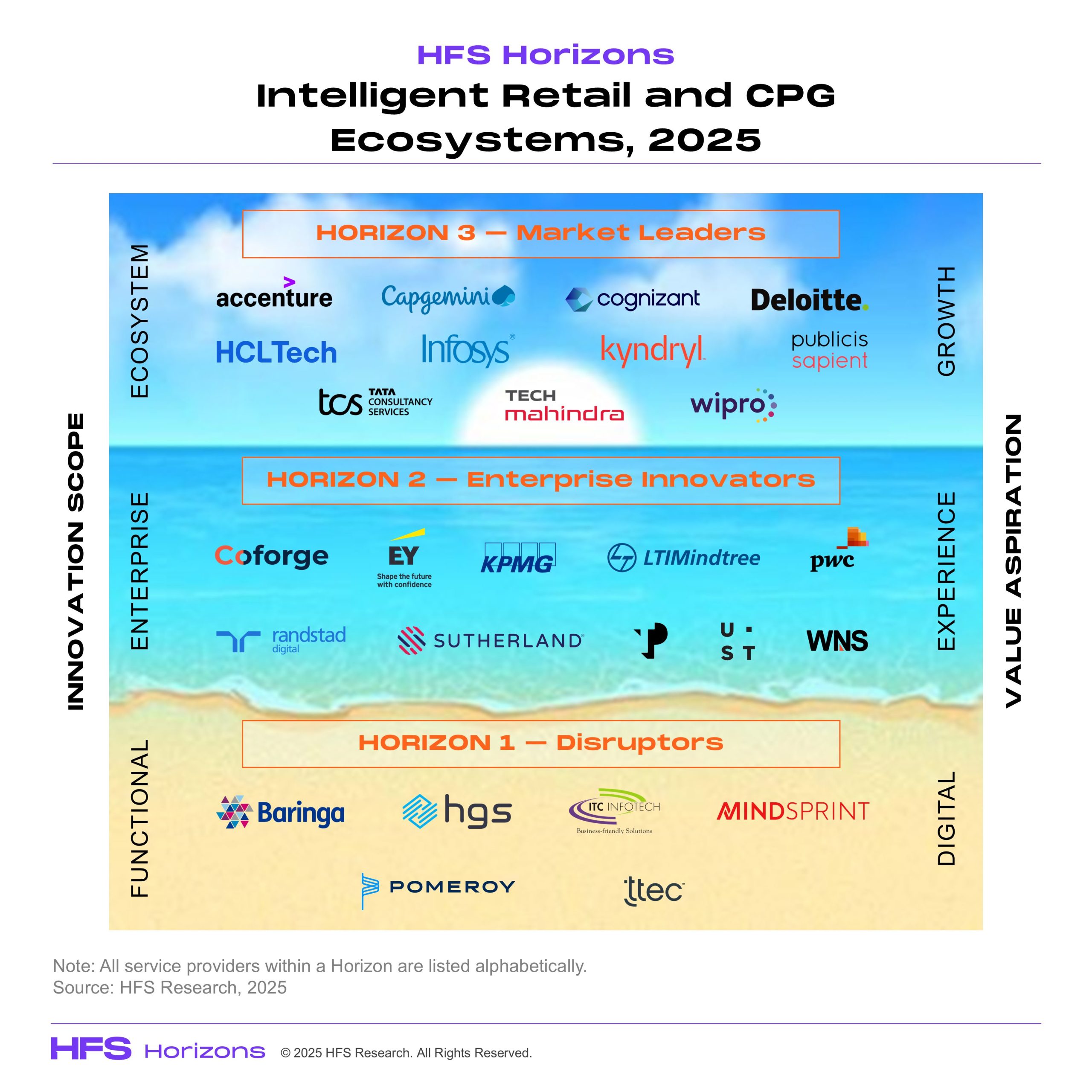

The report evaluates 27 retail and CPG service providers. Of these, 11 are classified as Horizon 3 Leaders, 10 as Horizon 2 Innovators, and 6 as Horizon 1 Disruptors. The evaluation included inputs from 44 enterprise reference clients and 36 reference technology vendors.

Horizon 1 represents Disruptors laying the foundation for digital efficiency by leveraging technology to drive cost reduction, speed, and operational efficiency in specific functions across the value chain.

Horizon 2 represents Innovators delivering end-to-end experience transformation i.e., Horizon 1 + elevating the entire value chain by creating integrated, customer-centric experiences through data unification and seamless interaction across touchpoints.

Horizon 3 represents Leaders showcasing ecosystem synergy and new value creation i.e., Horizon 2 + building ecosystems that unlock new business models, foster co-innovation, and create entirely new revenue streams, with an emphasis on sustainability and collaboration.

The Bottom Line: Retail and CPG leaders should prioritize investments in data-driven product innovation and omnichannel CX with cloud as the enabler, analytics as the propeller, and AI as the value generator.

Service providers that are rising beyond traditional services and capturing value through futuristic value-capturing models such as services-as-software are best suited to cater to the business expansion demand of the retail and CPG ecosystem.

My analyst colleague Saurabh Gupta has shared our viewpoint about what’s going on with Accenture in 2025 and it’s big re-org around Reinvention Services under the leadership of Manish Sharma.

Saurabh lays down the challenges ahead for our 800,000 services King Kong, namely several recent leadership changes, its sheer size, its huge plethora of acquisitions, its client culture, and the simple fact that AI is levelling the playing field. He also calls out the company’s huge breadth of capabilities to reinvent its clients with the subtle nuance that it now needs to prevail with its largest reinvention challenge: itself.

I am personally excited for my good friend Manish Sharma taking on the challenge of bringing together Accenture’s crown jewels of Strategy, Consulting, Song, Technology, and Operations to spearhead its Reinvention Services capability. Manish has been one of the bastions of global services ever since I can remember (which is a long time), and I can’t think of too many people who generally “get” the need to simply offer services to enterprises and bring together business needs scaled by technology. And in today’s era of AI fluff, the need to bring together front and back offices to exploit the blurring of lines between software and services, between people and machines, has never been more prominent.

Accenture’s been a step ahead reinventing the services market for many years

This is a significant rejigging of the services world from the global leader, which has clearly reached its own reinvention moment. The firm invented the term digital with its practice launch in 2013 and proceeded to acquire ~50 media/ad firms to become the global powerhouse in martech and digital advertising. The following year, it brought its BPO and managed IT services together under the Accenture Operations banner to transform “multi-tower” outsourcing. It then went full throttle Cloud First as we hit the pandemic, as the enterprise world desperately groped around to become genuinely virtual, organized, and scaled in the cloud. And as GenAI hit the big streets in late 2022, Accenture made sure it was at the forefront of building a billion-dollar pipeline. Then, when GCCs started competing directly with service providers for the offshore outsourcing work, Accenture smartly acquired a major stake in the GCC consulting leader ANSR to ensure it could balance its consulting and outsourcing portfolios to stay ahead of the disruption to global services. At the heart of this acquisition was Manish Sharma, the king of services reinvention himself, who sits on the ANSR board.

But can it keep reinventing with reinvented services in this volatile climate?

One of the secrets of growing, growing, and growing is having well-designed business units that can compete aggressively in the market, feeding off a common brand and pool of resources. However, with the unbelievable speed of development of agentic AI, generative AI, and machine learning, we have reached a greater need than ever to fix the same quagmire of issues plaguing enterprises for decades: processes, people, data, and tech.

However, what people don’t often realize is that the tech isn’t really the problem with AI. It’s fixing all the process mess, bad data, and skills deficiencies that are holding back enterprises. As our Pulse data across the Global 2000 dramatically illustrates, processes are the biggest, hairiest mess, and we need open-heart surgery to even consider sampling the forbidden fruits of AI:

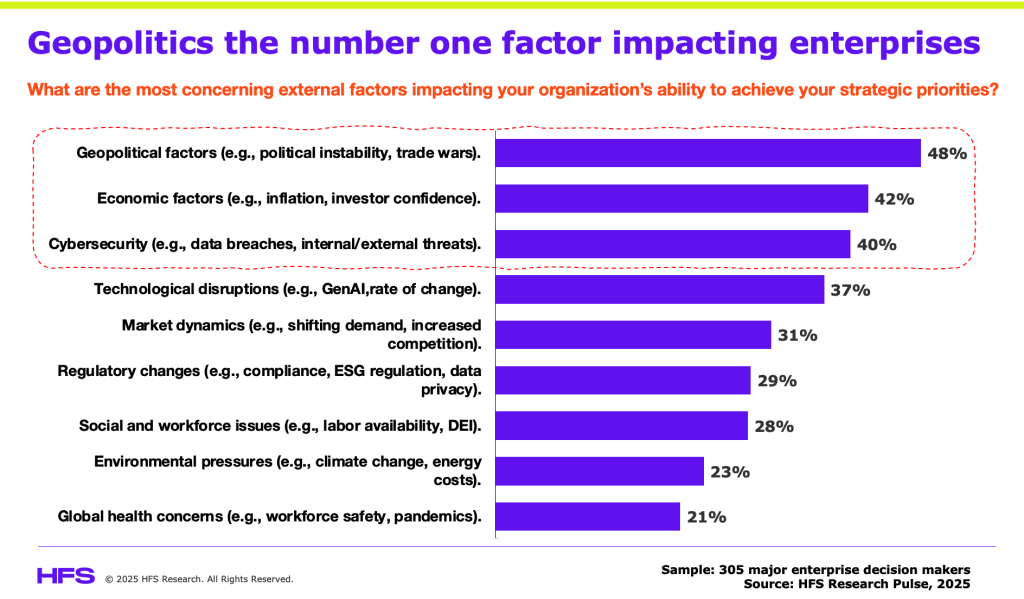

Coupled with our legacy debts, we also need to get ahead of all the instability posed by geopolitics, economics, and cybersecurity, as these dominate the minds of troubled ambitious enterprise leaders looking to invest in the core infrastructure of the businesses to insulate themselves from macro-instability and exposure to debilitating cyberattacks:

Net-net, the need for businesses to reinvent themselves to define such an array of problems and somehow fashion a way forward in this world has never been so poignant.

Bottom Line: Accenture has always stayed ahead of the game, but this time presents their biggest challenge

As we’ve discussed, Accenture has done a brilliant job over the last two decades reinventing itself and forcing the rest of the industry to follow its lead. However, they were able to do this with several business lines working fairly independently of each other. Their corporate branding, their deep relationships across the C-Suite (and not just IT) have enabled the firm to grow with a lot of smart acquisitions, incredible marketing, and an aggressive culture of “high performance” that was very distinct to the Accenture brand and culture.

However, today’s services playbook is changing radically and all the leading providers have no choice but to practice what they preach and take themselves through painful bottom-up change, where they need to focus on repaying their legacy debts of the last two decades to reinvent their own cultures, break down their silos and create distinct value for their clients. Being a true services-as-software provider necessitates a completely integrated company operating under one mission, one culture, one brand and one united leadership team energized by working together. But if anyone can pull this off, Manish can…

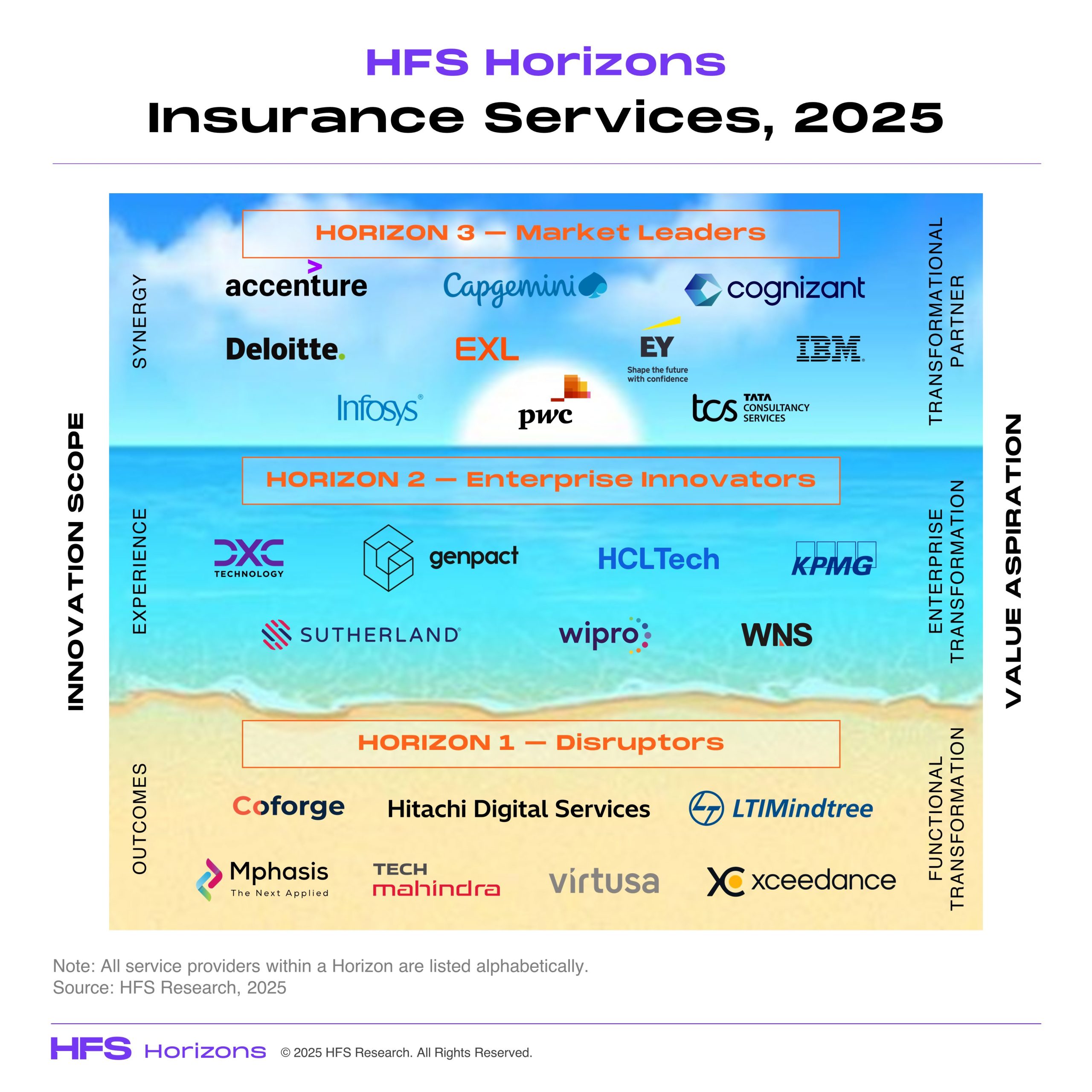

The insurance industry has spent the last decade digitizing its core in the form of claims, policy servicing, and back-office operations. But in 2025, modernizing won’t cut it. The real challenge is shifting from functional transformation to enterprise orchestration and ecosystem-led growth.

Our HFS Horizons: Insurance Services 2025 study evaluates 24 leading service providers across the insurance value chain. The verdict is that winners aren’t just automating; they’re unlocking new forms of value through GenAI, smarter underwriting, personalized CX, and ecosystem co-creation.

Exhibit 1: The Insurance Horizons framework captures the transformative shift from operational efficiency to ecosystem-driven, experience-led enterprises

Key study findings:

Functional transformation is the foundation and not the future: Many service providers have been successful in reducing expense ratios, streamlining workflows, and bringing regulatory clarity to complex insurance operations. Providers in Horizon 1 are driving measurable outcomes in speed, cost, and compliance, especially across claims, policy servicing, and legacy modernization.

But while functional execution earns providers a seat at the table, it doesn’t guarantee long-term relevance. Insurers are now expecting more flexible APIs, GenAI-powered insights, predictive risk engines, and cloud-native ecosystems that don’t just fix problems but prevent them from occurring.

Ecosystem orchestration is moving from slideware to real revenue: The most forward-looking providers (recognized as Horizon 3 Market Leaders) are co-creating with insurers, InsurTechs, data providers, and cloud platforms to reimagine entire insurance journeys. These firms are embedding intelligent agents in underwriting, activating ESG-linked product design, and orchestrating API-first platforms that connect distribution, policy, and claims into a single flow.

What separates these players isn’t just innovation but their ability to operationalize it at scale. They’re building modular offerings with clear business cases and aligning their delivery to customer, broker, and employee experience KPIs.

Underwriting is emerging as the next transformation battleground: Underwriting is the new frontier. Buyers want AI-driven triage, real-time risk scoring, and faster quote-to-bind cycles. Yet many providers still treat underwriting as off-limits. Leaders such as EY and EXL are deploying modular, data-rich solutions. Insurers should prioritize partners that bring speed, intelligence, and transparency to the front-end, not just clean up the back office.

The GenAI gap between hype and impact: Most GenAI pilots in insurance (chatbots, claims summaries, FNOL) haven’t scaled yet as they are bolted on and not embedded. Domain-specific tuning, deep API integration, and governance maturity are still lacking. Until GenAI is wired into core delivery without being stitched around it, enterprise leaders will see potential, not value.

Experience integration is the next mandate: Enterprises seek connected experiences, not point improvements. Whether it’s agents, policyholders, or employees, users are tired of jumping across portals, systems, and processes. Service providers that can’t deliver seamless journeys across underwriting, claims, and service will lose out to those that can.

The Bottom Line: Enterprises today have no shortage of service providers, but their true transformation lies in enabling a future-ready business model. Service providers that can’t make that shift will be replaced by those that can.

Insurance providers have modernized, but now they need to orchestrate. Leaders in this space aren’t just fixing workflows; they’re building modular, intelligent, and experience-aligned ecosystems that insurers can monetize. The ask has shifted from automation to alignment, tech showcases to scalable orchestration, and functional delivery to growth-anchored impact.

GenAI won’t matter unless it’s embedded. Underwriting won’t scale unless it’s intelligent. And journeys won’t stick unless they’re connected. To stay relevant in Horizon 3, insurers must move beyond just transforming operations by reinventing their business models.

Aren’t you just sick and tired of people waxing on about AI job destruction but clearly assume they are just going to be fine because they are just so damn important and irreplaceable? Oh, wait, you’re not also guilty of this, too, are you?

The harsh reality is that we all have a price on our heads to be replaced. As long as we are employed by someone else, we’re running the risk of pricing ourselves out of our jobs, because we’re just not worth the cost to our employers anymore.

We’ve always been walking costs to our employers. AI has just exposed us more than ever

Let’s cut through the noise and face our brutal truth head-on: we’re all vulnerable to AI, not just “them,” but you, me, everyone drawing a paycheck. It’s time we stopped comfortably pontificating about AI’s impact on other industries and professions, while conveniently ignoring our own glaring susceptibility. The harsh reality? Fail to evolve our work habits and embrace AI, and we’re setting ourselves up for irrelevance—fast-tracked straight onto the scrapheap of once-talented dinosaurs.

Here’s a simple litmus test: we can spot an executive bluffing about their AI knowledge in under two minutes. The buzzwords flow freely, but practical application? Hmmm… And guess what? Most people in your organization are quickly becoming adept at identifying the AI fakers. Authentic understanding—real competence—is becoming the gold standard that separates valuable assets from costly liabilities.

Leaders have avoided getting their hands dirty for decades, until now

For decades, people have survived on weaving their wonderful bullsh*t without getting their hands dirty. I remember once interviewing the RPA practice leaders across all the leading services firms and asking them to share their insights into the product functionality of the leading software tools. All of them failed to demonstrate any actual understanding of what these automation products actually did, beyond the usual rhetoric about “automating the enterprise”, infusing terms like “hyper” and “intelligent”. And they undoubtedly were dealing with clients who possessed equally scant knowledge of what these products did. In both cases, the leaders were dumping the real work down into the trenches of their organizations, where it inevitably faded into a series of insignificant pilot projects.

Let’s tackle the elephant in the room: the delicate balance between your cost, your value, and your replaceability

Here’s the cold, hard truth about employment today—we’re judged by one ruthless metric: how much we cost versus how much value we deliver. With AI reshaping expectations, the tipping point where our value fails to justify our price tag is frighteningly closer than most of us will admit.

The future of labor isn’t complicated—it’s about raw economics. For example, if you’re earning $200K+ annually, you’d better deliver exponentially greater value than someone at $75K with better AI chops. AI isn’t just another workplace tool—it’s an economic reset button that’s forcing every one of us to justify our salaries like never before. Young professionals, take note: this is your golden opportunity. If you can deliver equivalent or greater value at a fraction of the cost through adept AI integration, the future is yours to claim.

The Bottom-line: Don’t be part of the corporate hedgerow

Costs are like hedgerows – if you don’t keep trimming them, they keep growing back. But this time, many of these legacy hedgerows aren’t ever going to be replaced as enterprise leadership seems to eradicate legacy costs once and for all with their AI investments.

In this unforgiving AI economy, your salary isn’t just compensation—it’s a number continuously scrutinized, weighed, and measured against the value you’re delivering. But this really shouldn’t be about fear; it must be about clarity and being self-aware of our value. Justifying our price point has never been harder, but making ourselves irreplaceable AI warriors has never been more rewarding.