We all know that Blockchain has emerged as the world’s leading software platform for digital assets, however, new research is demonstrating its value could go even further than merely digital assets. Blockchain can reinvigorate parts of your infrastructure that have been under-performing for years to have a dramatic increase on the satisfaction of your partners, your customers and possibly even your employees…

HfS research’s new findings indicate that many enterprise back offices are in dire need of a complete transformation in order to come close to achieving the desired outcomes of their partners. Yes, folks, the impact of blockchains is causing many flagging enterprise assets to stand to attention, desperate to reclaim their former splendor and glory. According to one automation governance lead from a major consumer products firm, “Why rip and replace legacy assets when you still have plenty of mileage to glean from your trusted old systems? Ever since we got on the Blockchain Program, we’re rediscovering the ability to perform in a manner I’ve not experienced for at least twenty years.”

As with every technology magic bullet, the conversation always reverts to “hammers finding nails”, as many executives long to revive the glory days of shaving more off their bottom line in order to achieve more attractive results.

To this end, a financial controller of a FORTUNE 20 bank declared, “I had practically given up on ever meeting the demands of my various partners. Every time we were asked to perform, we just couldn’t connect the pieces. We tried every solution on the market, every tool off the shelf, even some special robots… we were a hammer trying to find a nail, but the nail just wouldn’t find the hole. Until we were introduced to blockchain, and suddenly everything changed…”.

There’s something about the nature of a distributed ledger that enables even the most seasoned of industry executives to re-live the days of their youth, a revelation that has put the wind up Pfizer, whose market is the latest to be on the verge of disruption. According to one disgruntled Prizer executive, “We are very concerned about the impact of Blockchain on our business lines. We have been warning customers of the serious side effects a Blockchain is going to have, with its sheer processing grunt depleting energy resources to an alarming extent. We advise affected customers to call their on-demand service provider for urgent support, especially after more than four hours of vigorous non-stop blockchain activity that is showing no signs of slowing down.”

HfS analysts also caught up with a leading executive from IBM, John Holmes, who added, “Thanks to blockchain, there is a huge opportunity to get our firm back on course for some serious straight line growth.”

And when we managed to get Accenture blockchain guru, Peter North, on the phone who revealed, “Blockchain promises high performance delivered and we aim to deliver that high performance. Delivered.”

Even President Donald Trump has confirmed the future potential of Blockchain in a recent series of tweets where he argued ‘It’s the best. The greatest. Just great. I’m so glad I came up with idea before Cambridge Analytica and Facebook. But seriously, Ivanka, is there any way we can delete some of the data on there? Yes those blocks called Stormy, delete them.’

And of course… this was an:

Please, please don’t tell me you fell for this again for the ninth year in a row! …And I know some of you did =)

And while we’re reminiscing about falling for April Fools’ gags, here is 2017’s classic:

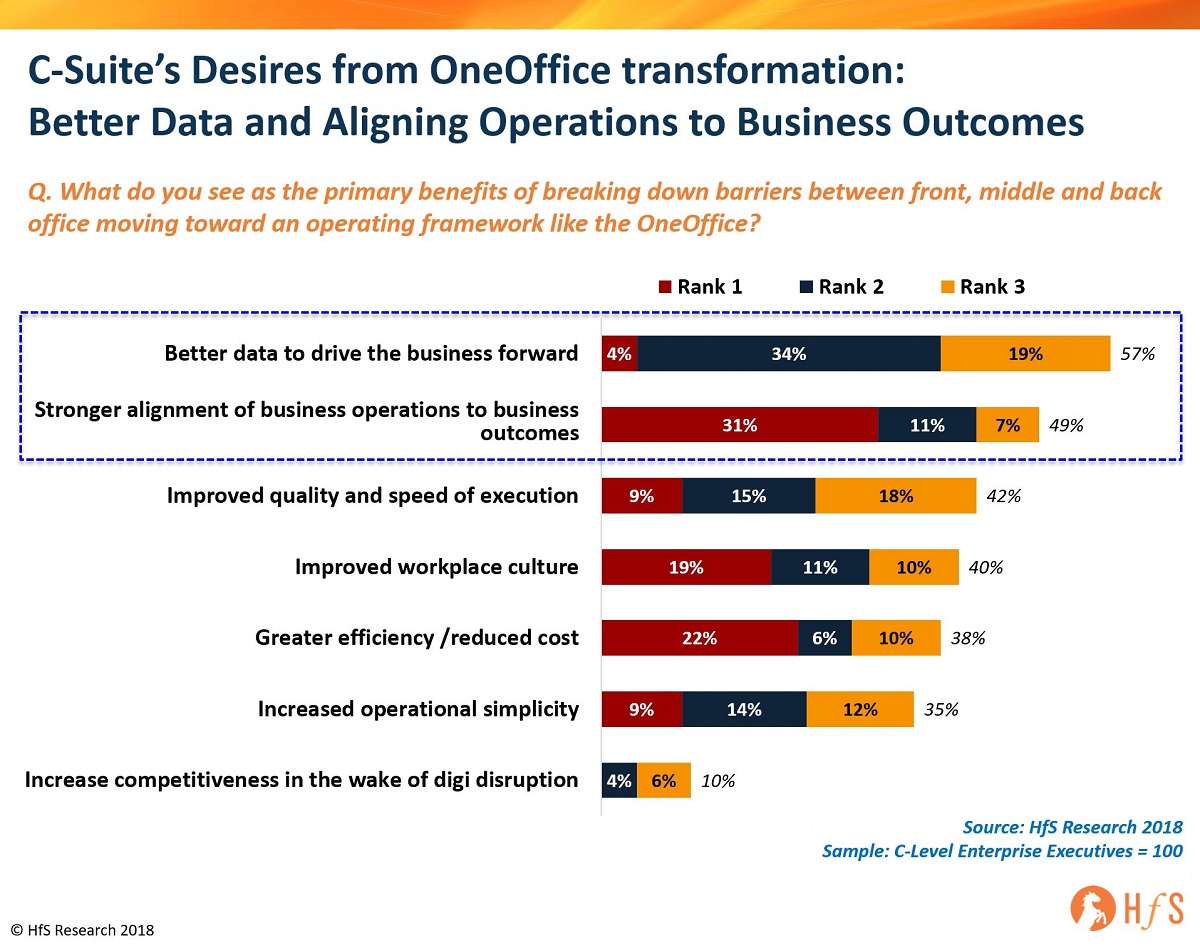

The biggest issue with most companies, when it comes to planning their operations, is that most do not have an ideal endstate in mind. They struggle to define success beyond finding some shiny new activity that will get them from where they are today to a state of greater productivity and/or lower operating cost. However, our new research with 100 C Suite execs reveals that their real goals are to get better data to drive their businesses forward while aligning their operations to their business goals. Technology solutions are enablers to achieve these goals, they provide a means, but they do not provide the outcome, which is where so many enterprises are going wrong these days.

Without a defined OneOffice endstate, automation strategies will always run out of steam

Even with offshore outsourcing, the endstate was rarely defined – it was simply to meet the next set of metrics before figuring out the “what’s next”. Were companies really envisaging running their operations in a similar way as before, merely with lower cost resources and some standardization of processes? But at least outsourcing was relatively predictable – it was defining how much work to move to the service provider and how many staff were needed to keep the operation ticking along to meet a desired set of metrics. With automation, entirely new metrics are in play, and it’s currently a random crapshoot how most companies are dealing with this. From manhours per year eliminated, to processing time reductions, to actual headcounts being removed, and even improvements in compliance and data accuracy, the “new metrics” that enterprises are toying with to find that next piece of “success” are becoming foggier than ever to decipher… and trust. And if you can’t trust the metrics, the whole thing starts to fall apart.

The reality is, once certain productivity measures have been achieved, the focus from the C-Suite quickly shifts to the next set of initiatives to achieve an entirely new level of productivity metrics. This is why the emergence of automation has been so significant – it is providing that next stage of productivity improvement that C-Suites are craving, and why RPA is now the leading investment focus to reduce costs in 2018 among Global 2000 firms:

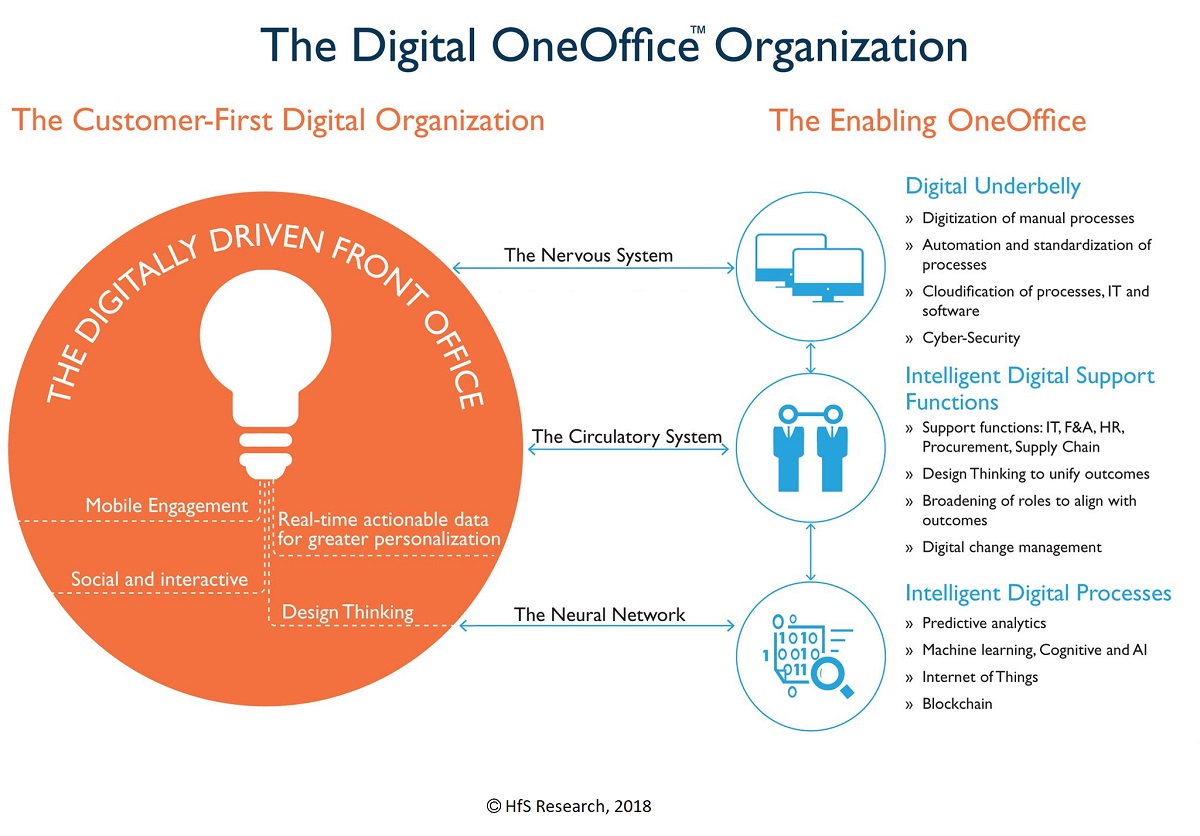

The end-game is about getting better data and aligning operations with the business goals. The end-game is OneOffice, where front, middle and back offices will cease to exist

Emerging technologies like automation and ML are not the “end”, they are just a “means” to get us from one state to the next. Enterprises need to define what is their real endgame, otherwise they are stuck in a perennial loop of finding short-term fixes and losing focus. This is why we have developed the Digital OneOffice Framework, where the organization’s people, intelligence, processes and infrastructure come together as one integrated unit, with one set of unified business outcomes tied to exceeding customer expectations. OneOffice is where teams function autonomously across front, middle and back office functions to promote broader processes with real-time data flows that support rapid decision making, based on meeting these defined outcomes. Hence, emerging technologies like automation and AI are significant enablers in helping enterprises meet their ultimate goals, where front, middle and back offices will cease to exist: They will be, simply, OneOffice:

In a new study we are soon releasing that tests the OneOffice endstate with 100 C-Suite executives, we asked them about the primary benefits of breaking down internal silos between front, middle and back offices – i.e. making them think more about what their real end-game is versus merely how to dig out more cost. And it’s not really all about cost, it’s much more about getting the data they need to stay ahead of the game and to align their operations with the front end of the business. In short, the endstate if about simplifying the business around the needs of the customer and having the data to stay ahead of the competition:

The Bottom-line: Without a defined OneOffice endstate in mind, enterprises are forever meandering from one silver bullet to the next, where the only metric of success is eking out further reductions in headcount to keep their operations functioning

The real key is to define where you want to be, and create a path to get there. In most cases, this endstate is all about enterprises becoming conduits of the data they need to satisfy their customers’ needs in realtime, with a team of smart people who know how to manage these data flows and make smart decisions to keep ahead of the competition. The broader processes become between the customer and the enabling operations, the faster companies can satisfy their needs, and stay ahead of the game. The future is all about simplifying data complexity and having talent that can make creative and intelligent decisions, based on the availability of this data and understanding the customer. This is the very essence of OneOffice – simplifying data flows, bringing the customer and the operation together and aligning your talent with achieving defined outcomes that keep you ahead of your competition.

Now most of you have finally realized that blockchain means something more than some weird disruptive currency you completely avoided buying when it could have netted you millions, we need to get much more familiar with the actual enterprise platforms being developed, where the true potential of this ledger technology can be unleashed on our enterprises, supply chains and industries.

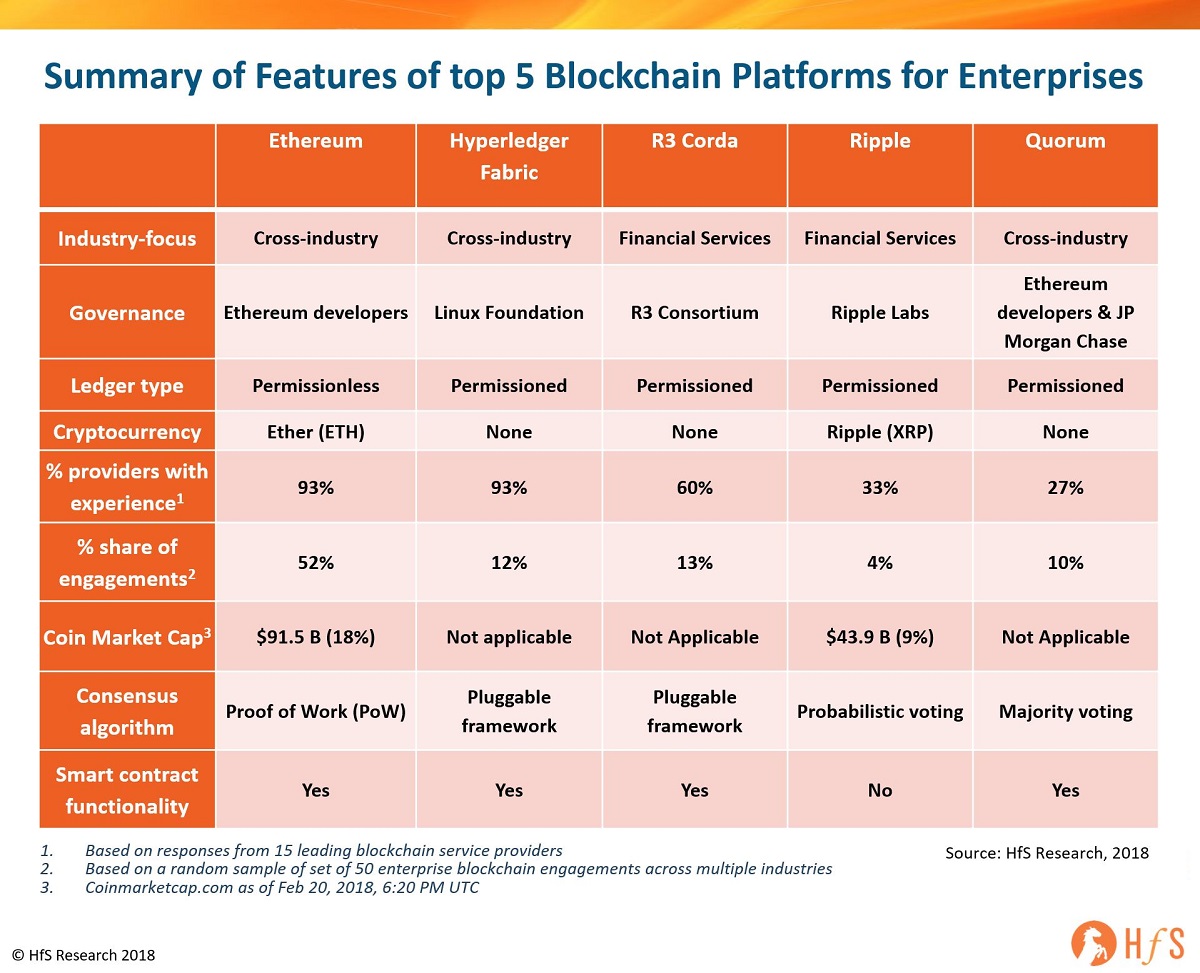

So we asked our blockchain boffins Saurabh Gupta and Mayank Madhur to take a deeper look at the top 5, namely: Ethereum, Hyperledger Fabric, R3 Corda, Ripple, and Quorum. Please note that Bitcoin does not make it to our list of top 5 platforms. In fact, it does not make the top 10 list when we talk about enterprise application of Blockchain.

The objective of our research is to understand blockchain platforms that show promise in solving complex business problems:

“Ethereum is a platform that makes it possible for any developer to write and distribute next-generation decentralized applications.”

– Vitalik Buterin, Co-Founder, Ethereum

Founded by the 22 year old Russian-Canadian Vitalk Buterin, Ethereum is one of the most mature blockchain platforms available today. Known for its robust smart contracting functionality and flexibility, it is used widely across multiple industry use-cases. It has the largest number of use-cases available today (50%+ in our sample set). Along with Hyperledger Fabric, Ethereum has developed a large online support community as well has frequent product updates and enhancements.

The Ethereum Enterprise Alliance (EEA), a non-profit organization is now over 250+ members strong and connects Fortune 500 enterprises, startups, academics, and technology vendors with Ethereum subject matter experts. Despite its widespread adoption in enterprise use-cases, it’s important to realize that Ethereum is essentially a permissionless (or public) platform that is designed for mass consumption versus restricted access (typical requirement for privacy requirements in enterprise use-cases). It is also PoW (proof-of-work) based which is not the fastest (resulting in potential latency issues) and is an energy-sucker. Though it might change its consensus algorithm to the fast PoS (proof-of-stake) in future versions.

“As new technology develops, there is a call for standards. Participants want to focus on time and effort and investment to build solutions versus worrying about the framework. This is the rationale for open standards…we are pulling together the most exciting portfolio with a multi-lateral developer and vendor community. It’s similar to the benefits that Linux brought to the world of operating systems.”

– Brian Behlendorf, Executive Director, Hyperledger

Hyperledger, hosted by Linux Foundation and launched in 2016, is an open-source collaborative effort to advance cross-industry blockchain technologies. One of its key goals is to create enterprise-grade distributed ledger frameworks and codebases. Hyperledger boasts 185+ collaborating enterprises across finance, banking, Internet of Things, supply chain, manufacturing and technology. Hyperledger Fabric is one of the 8 ongoing Hyperledger projects that was initially contributed by IBM and Digital Asset. It is an attractive blockchain framework for enterprise solutions, given its modular architecture, as it allows plug-and-play components around consensus and membership services. It recently announced the release of Hyperledger Fabric 1.0 that claims to be production-ready for enterprises.

#3. R3 Corda. New Operating System for Financial Services

“Corda has been developed to service the specific needs of financial services with generations of disparate legacy financial technology platforms that struggle to interoperate, causing inefficiencies, risk and spiraling costs.”

– David E. Rutter, Founder and CEO, R3

Launched in 2015, R3 is a consortium of some of the world’s biggest financial institutions that has created an open-source distributed ledger platform called Corda. It’s partner network has grown to 60+ companies. While Corda was designed with banking in mind, other use cases in supply chain, healthcare, trade finance, and government are emerging. There is no built-in token or cryptocurrency for Corda, and it is a permissioned blockchain as it restricts access to data within an agreement to only those explicitly entitled to it, rather than the entire network. Its consensus system takes into account the reality of managing complex financial agreements. It is also known for its focus on interoperability ease of integration with legacy systems.

#4. Ripple. Enterprise Blockchain Solution for Global Payments

“Global payments are undeniably going through a sea change, led by financial institutions adopting blockchain to fix their customers’ broken payments experience. Now more than 100 financial institutions are looking to Ripple as the solution to the problem…”

– Brad Garlinghouse, CEO of Ripple

Ripple was founded in 2012 and was renamed fromOpencoin in 2015. It aims to connect banks, payment providers, digital asset exchanges and corporates through RippleNet, with nearly-free global transactions without any chargebacks. It enables global payments through its digital asset called “Ripples or XRP” that has become one of the most popular cryptocurrency just behind Bitcoin and Ether. XRP is touted to be the faster and scalable than most other blockchains (4 seconds payment settlement versus 1+ hour in Bitcoin with the ability to 1,500 transactions per second compared to 3-6 for Bitcoin). It has 100+ customers with 75+ clients in various stages of commercial deployment across three primary use cases namely: cross-border payments (xCurrent), minimizing liquidity costs (xRapid), and to send payments across various networks (xVia).

#5. Quorum. Enterprise-focused Version of Etheruem

“J.P. Morgan has long used open source software and we are excited to have this opportunity to give back to the community. Quorum is a collaborative effort and we look forward to partnering with technologists around the world to advance the state of the art for distributed ledger technology.”

– Lori Beer, CIO, J.P. Morgan Corporate and Investment Bank

Developed by J.P. Morgan leveraging Ethereum since 2015, Quorum is designed to handle use-cases requiring high-speed and high-throughput processing of private transactions, with a permissioned group of participants. It does not use the Proof of Work (PoW) consensus algorithm but uses vote-based and other algorithms enabling it to process hundreds of transactions per second, depending on how smart contracts and networks are configured. Quorum is designed to develop and evolve alongside Ethereum. It only minimally modifies Ethereum’s core, thus Quorum is able to incorporate the majority of Ethereum updates quickly and seamlessly. Just like Etherue, Quorum is also open sourced, free to use in perpetuity and encourages experimentation.

The Bottom-line: Blockchain Platforms will Consolidate and Collaborate as Enterprise Adoption Increases

The blockchain world moves at a frenetic pace of innovation with emerging new platforms, additional new features, and new releases, while ambitious enterprises are eager to get ahead of the curve with its disruptive potential

Meanwhile, enterprise adopters face challenges with a lack of standards and inter-operability issues, especially as they try and upgrade from pilots and PoCs to real production-grade environments. The whole development of the blockchain ecosystem is no dissimilar to the Internet for permissionless networks and cloud for permissioned ones, where blockchain is almost akin to TCP/IP as the architectural technology.

Like with any hyped, exciting new technology development, enterprises do not need 1,500+ different platforms and we will quickly see a handful of real players start to dominate and investors get focused and the ecosystem fleshes out. This PoV highlights the current top 5 platform players, but given the nascency of blockchain (almost all of these are merely a few years old), this will continue to evolve. and we will start to see greater collaboration between leading platforms given the market push and pulls. For example, we are already starting to see some evidence of this, with Hyperledger, Sawtooth, and Hyperledger Burrow working together to run the Ethereum Virtual Machine (EVM). The Blockchain Interoperability Alliance was also created in November 2017 to collaborate on researching interchain transactions and communications. Like with every new concept, blockchain is also going through these growing pains.

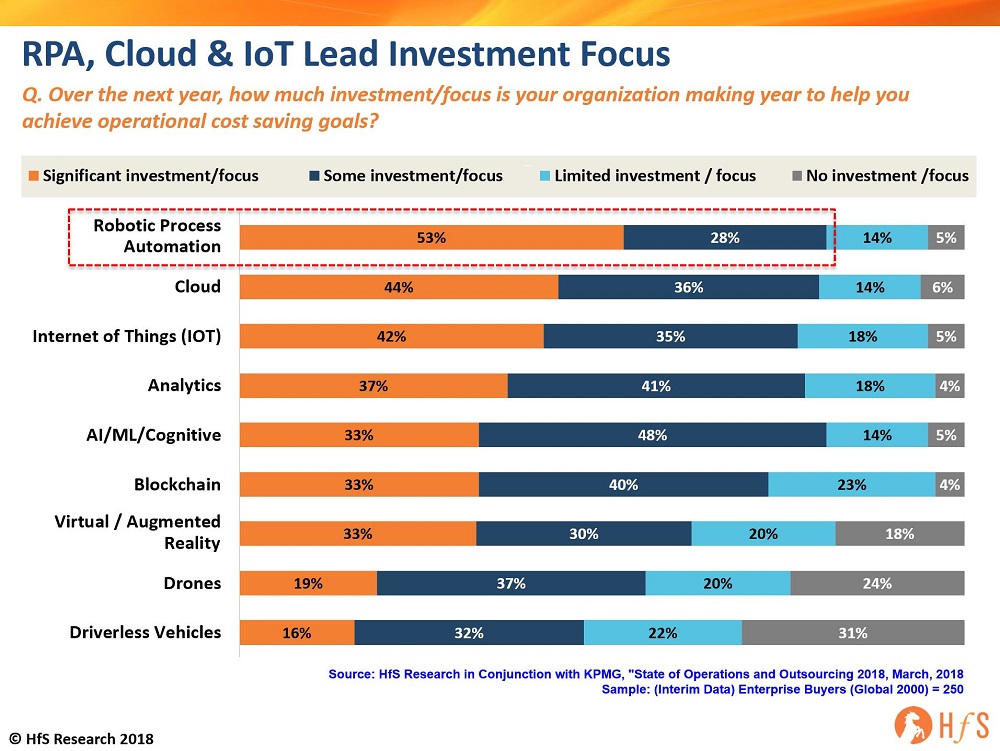

While we were discussing the confusing realities of the RPA hype at the HfS FORA Summit, we got a sneak preview of the interim data from the 2018 State of Operations and Outsourcing Study, conducted in conjunction with KPMG, where 250 interviews with Global 2000 operations leaders have now been completed.

We asked them where their investment priorities were currently lying when it comes to 2018 cost reduction:

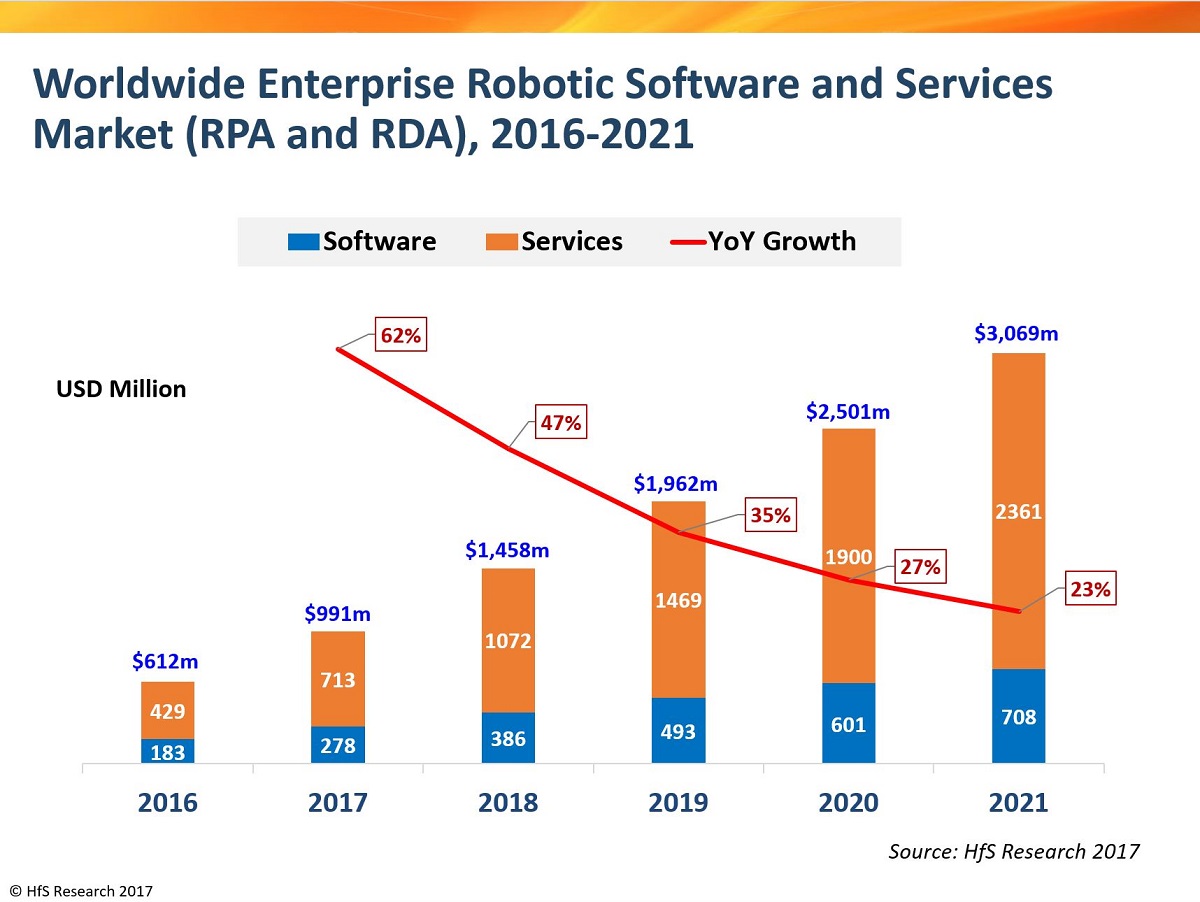

So it’s abundantly clear all the hype about rampant adoption has been warranted, and we can hang our hats on our recent enterprise robotics software and services forecast, which now appears conservative, increasing with 47% growth to $1.46bn this year (click here for full forecast):

The Bottom-line: RPA has succeeded in being positioned as the “easiest silver bullet to target that next wave of cost take-out”. Now let the real fun and games begin…

The real issue, here, is that the majority of enterprises are taking the plunge and investing the dollars, with 81% actually taking RPA seriously, and 53% very seriously. So what’s going to happen in a few months when those ambitious CIOs and CFOs ask to see real, tangible demonstrations of the resultant cost takeout? Can C-Suite leaders quickly learn to love metrics that are tied to growth, value and effectiveness, as opposed to a simple reduction in operating expenses to feel rewarded for those expensive bot licenses? Are operations leaders generally going to be ready to quantify the value effectively? Can they really convince their superiors that there is true value impact beyond merely offering up headcount elimination?

What’s more, what if headcount reductions were promised to offset investments, and adopters have failed to free up the workload that can enable them? And can they reward the staff, who cooperated in the automation work, by getting them “retrained”? Is there really a plan? While the “one human to oversee every 10 bots” is becoming the latest robo-governance rule-of-thumb, how real is this? Or are we just all bull*****g ourselves about the future, and merely circling the hype to stay relevant today? Do we really care about our companies anymore, or are we more obsessed with adding big sexy initiatives to our CVs? Is this really anything different to yesteryear, where you needed to have an SAP rollout on your CV to be a credible CIO, or oversaw a 1000 FTE outsourcing deal to prove you were worth that $1.2m/ year GBS salary (yes, that’s what some get…). In this world of #fakenews, does anything really matter anymore, when we can spin our realities into whatever shiny new thing is out there?

One thing is clear is that the back office needs to be submerged into the value end of the organization. There is little more headcount elimination to be had for most companies – sure, there are still many areas that have too many people working on too few valuable tasks, and technologies like RPA are terrific tools for breathing new life into legacy systems and creating digital process flows, where before there was only spaghetti code, manual workarounds and swamps of data polluting the corporate underbelly.

One thing is clear, it’s very murky out there, and all we can really do is hatch a semi-realistic plan and try and stay on top of it as the future unravels in front of us…

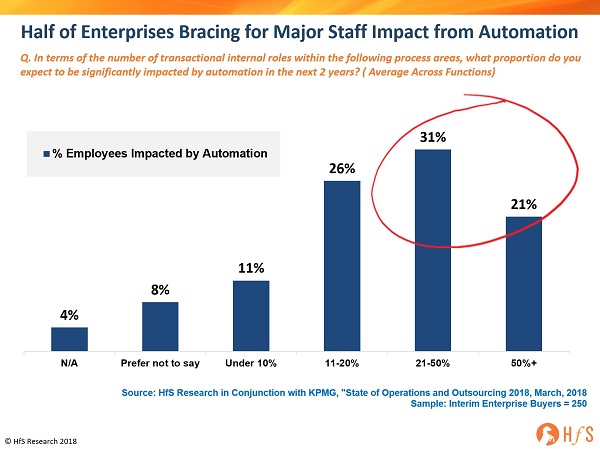

So here’s the biggest issue facing enterprise operations in the next couple of years: what to do with staff impacted by automation. Our brand new 2018 State of Operations study, conducted with KPMG, over half the Global 2000 firms surveyed believe transactional roles will be significantly impacted by automation within just a two-year timeframe:

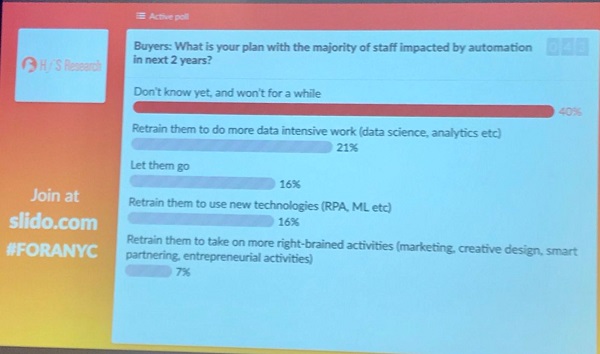

So we thought we’d poll the 120 buyers at the new York FORA summit this morning as we asked them what they intended to do with their impacted staff:

While a good portion are already thinking about “retraining” their impacted staff to take on analytics work (21%) and help manage new tech such as RPA and ML (16%), the vast majority (40%) are just honest and reveal they just don’t know.

Bottom-line: We have to plan for automation better

As automation fever takes over business operations (and we’ll reveal that data next), my one plea to industry is to plan this better. CFOs and CIOs investing $ millions in bot licenses and consultants to implement them will be expecting a return on their investment, and if operations leaders do not have a concerted plan to use the freed up man hours, you can be sure there will be intense pressure to reduce even more heads than may have been in the initial plan.

Have you ever mixed business with romance? Oh dear, that could be taken the wrong way, but our keynote speaker next week at the HfS FORA summit New York, Tim Leberecht, has literally written the book on the subject. Tim’s session next week is one that will breathe new energy into our narrative, and the title “How to Thrive in the Robotic Age Without Losing Your Humanity” just about says it all!

So let’s hear a bit more from Tim about why he’s such a sought-after speaker and visionary on the future of work and the impact of AI…

Phil Fersht (CEO, HfS): Tim, we’re very excited to have you as one of our keynotes in New York. So maybe you can give us some insight into how you have become a “Business Romantic.”

Tim Leberecht (Founder of The Business Romantic Society): Education-wise, my background is in the humanities and professionally, in marketing. Initially, I set out to write a book about meaning, and specifically the power of brands to serve as one of the few remaining arbiters of meaning in our societies. As I was looking into the principles of meaning-making, I realized that they were all, in effect, romantic principles: keep the mystique, foster intimacy, embrace solitude, seek adventure, suffer (a little), and so on. I had this epiphany: “Wow, I am a romantic!” In fact, I realized that romance had been the defining quality of my career—I just hadn’t been able to articulate it. The term “Business Romantic” nailed the tension I had felt all my professional life, and since the book came out in 2015, it has proven to be provocative and fruitful. Opposites attract, or as one of the interviewees for my book said: juxtaposing opposite poles make each of the poles more attractive. I haven’t met anybody yet who hasn’t had a strong reaction to the word “romance:” people either oppose it or aspire to it.

Phil: So the theme of the conference is “Learning to Change in the robotic era”… what’s your view on how we humans must adapt with all the technological change occurring? Is it more about attitudes that skillsets?

Tim: It’s both, Phil. There are some grim reports out there, such as Bain’s recent study that predicts 30 percent of all US jobs will be automated by 2030, with the rewards of automation going mostly to the top 20 percent of earners or savvy AI investors. McKinsey estimates that 30 percent of 60 percent of all tasks in existing jobs can already be automated. Futurist Gerd Leonhard proclaims that “if you can describe your job in one sentence, chances are you might get automated,” referring to the high likelihood of process-oriented, linear, routine-based work being automated.

Entire professions will feel the consequences: not only factory workers or call-center agents but also legal research assistants, accountants, notaries, investment managers, or management consultants. While exact estimates are still disputed, clearly, massive changes to work and society are underway, and we are just beginning to grasp them. AI will dramatically alter both process and offerings in almost every industry. Every profession will have to evolve and embed AI and robotics in their processes. AI and co-bots will become our new co-workers, and those parts of our work that can be done more efficiently will be taken over by them. Many of us will lose traditional employment, the rest of us will have to get used to hybrid work environments and collaborating with AI (and perhaps even having AI’s as bosses).

We’re definitely in a race with the machines, and it’s not one we can win unless we remind ourselves of our inherently human qualities that AI isn’t able to emulate yet: vulnerability, imagination, and character. We are elusive, inconsistent, elastic, and often erratic beings—we remain unpredictable and can change our beliefs and emotions. That makes us hard to deal with but also constitutes the very engine of progress. It’s not technology, it is our changing hearts and minds, our ever-evolving values, that is the source of innovation.

We will need to acquire not only new technical skills, but also new emotional ones, as we’ll be facing an increasing loss of control, of agency in the traditional sense. Deloitte says that 63 percent of businesses need leadership skill development for the digital future, and that many of these skills are “soft skills.” Our identities and interactions will become more fluid, as boundaries between man and machine, internal and external reality, digital and physical world continue to blur. To thrive in this age of machines, we will have to learn (again) to appreciate beautiful work and how to our work beautifully—with heart, character, and intuition. This what romanticism can teach us.

Phil: And what’s your view of this “singularity”? Is it real, Tim, or just hype? What is the real pace of change and disruption, as you see it?

Tim: Let’s say it is a real possibility Phil. AI is already capable of solving complex problems or performing analytical knowledge work such as legal research or content analysis. It can now learn on its own (e.g. Baidu’s Deep Speech technology can acquire a new language in a couple of hours virtually without any human oversight) and even be creative. For example, AI can compose and perform entire symphonies based on musical patterns it has studied. Or take the phenomenon of fake video created by deep learning algorithms that superimpose faces and audio on real recordings—with disturbing use cases in porn as well as politics. In architecture and design, too, it is becoming harder, if not impossible, to distinguish man-made from machine-made creations, whether it is the kind of computational design used for buildings like Amazon’s new HQ or the Shanghai Tower, or Airbnb developing an AI-based product design service that converts design sketches into prototypes without any human oversight. Amazon has even developed an AI-based fashion designer. Plus, AI can now create and train its own AI, as Google recently announced.

Just last week, a collective of leading AI researchers and civil society organizations sounded alarm about the accelerated development of AI and urged human regulation and common standards. Much of the immediate doomsday scenarios may be overstated, but AI is certainly on a fast track to morphing into Artificial General Intelligence that could potentially overpower humans—not because it outperforms us in every single dimension of our intelligence, but because it may disrupt enough of our social fabric and humanity to throw us into catastrophic turmoil.

We will need to find a way to redistribute wealth to avoid growing social divides and unrest, as well as the phenomenon of a new class of dispensable workers (many of them, as recent study by the World Economic Forum has shown, will be female workers) – a new “useless class,” as Yuval Noah Harari calls them. Universal Basic Income is a promising policy idea to allow for the decoupling of income from prosperity and wellbeing and to reduce economic anxiety.

Phil: So what can we expect you to talk about in Manhattan next week? What do you hope enterprise operations leaders can take away from your session?

Tim: With transaction costs lowered by digital technology, and technologies like AI and Blockchain democratizing and virtualizing transactions, the role of the traditional corporation will diminish. We’ll witness the continued rise of the freelance/gig economy (the fastest growing part of the labor market in the US and Europe), with ever more flexible work structures, alternative currencies (cryptocurrencies like Bitcoin, but also an appreciation of intangible assets such as identity, reputation, personal brand, relationships, etc.), as well as growing volatility and fragmentation of work. There will be more project-based work or so-called “flash organizations” that assemble ad-hoc and only for a specific, temporary purpose.

I am a romantic and remain optimistic about the future, but I want business leaders to realize what’s at stake: not just our jobs, our very humanity. Now is the time to explore new paradigms and tools of value creation, to (re)define success on human terms. Operations leaders, in particular, bear an enormous power and responsibility: many of the jobs that will be automated are in their domain, and they need to find ways to reskill workers and help them prepare them for the new world of work—technically, intellectually, and emotionally. They will have a lot of big decisions to make in the next few years, and I hope that they will make them not only with an eye on the bottom line but on the prolonged health of their businesses and our societies.

Phil: Terrific discussion, Tim. Can’t wait to hear you next week at the big summit!

One character who will light up our New York HfS FORA Summit next week (and not just with a cigar) is the irrepressible Lee Coulter. While Lee could have hung his hat on leadership roles at GE, Kraft and Ascension Health (where he still oversees their shared services as his day job), he has taken it upon himself to become one of the leading voices behind the Intelligent Process Automation (IPA) movement, as Chair of the IEEE’s working standards group on IPA and Founder of Agilify, a newly launched automation services business, already boasting 32 clients.

With so much going on in Lee’s world, I thought it high time to catch up with him before we hear his dulcet tones next week…

Phil Fersht, CEO and Chief Analyst, HfS Research: You’ve been the self-styled Godfather of Intelligent Process Automation, brandishing a cigar, as opposed to a Kalashnikov… why did you take on this mantel, how did this evolve during your recent years with Ascension into this new firm, “Agilify”?

Lee Coulter, CEO, Ascension: That’s quite an image. I think my role chairing the IEEE Working Group on Standards in Intelligent Process Automation was probably what did it. We started over five years ago on our automation journey. The hype and confusion was literally driving me batty. So instead of getting into a war of words, I decided the best answer was to get the competitors to not want to be left out of a standards effort. It was in everyone’s best interest to work together. That first standard (IEEE 2755-2017) was really a hallmark and the next one (P2755.1), coming this year, will have a far greater impact. That work has created great relationships across the continuum that have been helpful in bringing automation to Ascension.

The idea for Agilify came about during a conversation with a GBS colleague when he wanted to bring his team on site for a third full day to meet with my team. I told him, “Hey, I think you’ve gotten automation help about as much from us as can be had from long top-to-top meetings and if you really want some help, let me send a couple of my people on site for a few days and really give you some help.” He said that would be awesome. I said, however, I can’t do that for free and asked if he would be willing to pay for it. Without hesitation, he said yes! At that moment I knew we could help other folks. Word spread and this turned out to be the first in a long line people just asking for help. We had no sales people, no marketing, nothing. As more walk up business arrived, I knew it was time to give it a life of its own.

Phil: Lee what is your role with Agilify and how will this dovetail with your role at Ascension? And your role with IEEE? Are you going to be working harder than ever, or taking a deserved break from life and confusing the hell out of people what you actually do?

Lee: I guess the best answer would be board chair and strategic advisor for Agilify. My role at Ascension continues being a digital disrupter As the largest customer of Agilify’s, we have a significant interest in their future. The demand pipeline Ascension has assembled for Agilify really helps drive their capability development and delivery. We are now doing some really clever stuff mixing different Intelligent Process Automation stuff with ML.

My work with IEEE is going forward uninterrupted. Actually very excited about progress there. The current standard under development P2755.1 is the Taxonomy for Intelligent Process Automation Products and it is coming along very well. It will be a game changer and I am excited to still have the support of the working group to continue as Chair.

As to taking a break, heck no! There are a ton of exciting things going on.

Phil: So why launch a firm, and what’s its purpose in life? And why is it called “Agilify”?

Lee: Agilify has a lot to offer. They have some of the deepest capabilities technically across multiple technologies and what most others are not really offering, which is how to embrace enterprise adoption. The training and consulting spans far more than just building bots, but addresses strategy, risk and control, business analysis, change management, and operations resilience. The experience Agilify has gained comes from building an Automation Practice from the ground up and having to live with the outcomes.It really is a journey, and it turns out that Agilify is very good at meeting people where they are and helping them along their journey. All of the engagements are tuned to deliver what’s needed rather than a canned set of fixed-price consulting packages.

So Agilify’s purpose is helping others. Some customers are just starting out, and some are three years down the road. Our slogan is unleashing human potential through automation (http://agilifyautomation.com/about.php) and it is not just for marketing. We work with others to hit what I call the four “Es” of automation. We provide technology agnostic automation platforms and services driving the “4 Es” of automation: Efficiency (cost), Effectiveness (business result), Experience (customer) and Engagement (associate). What’s more is this journey extends far beyond RPA into RDA, and ML and advanced analytics.

Agilify is a great name that brings to mind agility, life, and technology and this is at the heart of it.

Phil: Which type of firms do you see Agilify partnering and competing with as you build up your business focus?

Lee: I see Agilify working across the spectrum. They are one of just a handful of pure-plays out there and it is a remarkably respectful community. It is quite conceivable, that we might see some cooperation within the competition. The Agilify differentiator is truly being a full spectrum provider focusing on successful enterprise adoption of automation. So in addition to the panel of technology partners, there are a number of other partnerships in place and more under development that will expand their reach and capability. Due to the strength of the Agilify Automation Academy, there are some surprising customers in the pipeline. More to come on that as these deals conclude and can be shared.

Phil: So what’s the direction of travel for the Intelligent Process Automation industry? Is this truly sustainable?

Lee: First of all, it makes me really happy to hear Intelligent Process Automation as the term. We worked really hard to get folks to understand that there is more in the automation field than RPA and we are seeing that play out. I think it’s conceivable in the future that the separation between RPA and RDA and ML will disappear and Intelligent Process Automation will be used. I say that because as we are seeing, the products are rapidly evolving to embrace features and functions that cover the spectrum. Whether it’s ML embedded in a server-based runtime environment or desktop automation now including ML and server-based features, the trend is all heading toward the Intelligent Process Automation moniker.

I think it is sustainable for the foreseeable future. It is unrealistic to think that large companies are going to abandon their very expensive systems-of-record. So how can we treat multi-system processes and present them as if they were a single system with a single interface? That is where Intelligent Process Automation comes in. I do think we will see a broadening of native automation capabilities like this coming from the new breed of heavy IT systems. However Chrome still doesn’t play well with java and that isn’t likely to change any time soon and crossing 10 or 15 apps with low-code-no-code automation is going to be around for as far out as my crystal ball can see.

Phil: And what’s the winning strategy for the tools providers – is it direct selling to the clients, or through smart partnerships? We keep hearing that having a strong consulting partner is the way to go versus trying to establish your own CoE – what’s your take on that?

Lee: For the makers, it’s all about the partners. Likewise, finding a consulting partner that can take you from where you are to three years from now is critical. In a recent paper (https://www.ssonetwork.com/reports/global-intelligent-automation-market-report-h2), I talk a lot about COE structure and governance. I think the future will see COEs pretty much everywhere, particularly as folks move from RPA to IPA.

Phil: And what’s the future of BPO and shared services in this automation age? Is this a gradual evolution towards more touchless environments, or are we truly in for some “shock and awe”. What’s your advice to process and operations leaders scratching their heads trying to figure out where their careers are heading?

Lee: Shared services will continue to be a place that businesses send any operation that exists at scale with reasonably standard processes. The tools, the mix of digital and human labor, the complexity of the work and the performance expectations are changing and in large part increasing. GBS and hence BPO are still going to be looked to drive improvements year over year. Like we are seeing elsewhere, the pace of change and the pace of disruption are likewise increasing. I can conceive of a day in the future where by and large, ML enabled Intelligent Process Automation manages multi-system processing. I think GBS will need to get comfortable with a bigger “more for less” expectation. My advice to service operators is lead these transformations, don’t wait to be told or it might already be too late. Your company and your career may depend on it.

Phil: And finally, what are your realistic expectations for Agilify over the next two years? What does success look like?

Lee: Agilify is now one of a small handful of Intelligent Process Automation pure-plays out there. I think the best work is coming from the pure plays so I expect Agilify to grow quickly. There is a lot to do with RPA still, but the larger opportunity is with Intelligent Process Automation and that is where Agilify has some distinct advantages. There are also some offerings that are a bit under the tent still that will be a game changer. More on that next time.

Lee will be taking part in the The Great Intelligent Automation Debate and the Family Feud Face-Off next week at HfS’ flagship FORA Summit, Times Square Manhattan.

Stability and modest growth should be the best thing that has happened to this industry: companies can plan for the future with greater predictability and make smarter investment decisions. Instead, we’re suffering from a culture of endless hype, copycat marketing and an addiction to hypergrowth.

NASSCOM’s annual India Leadership Forum is always a good bellwether for testing the temperature of the global services industry – and the 2018 rendition this week in Hyderabad served up some real pearls of wisdom (yes, Hyderabad is the world’s leading refiner of pearls).

Getting to the point, the services industry has never found itself in a worse state of bewilderment and confusion. After last year’s sense of looming disaster with President Trump’s proposed Visa reforms, at least the industry has something collective to hang onto – a common fear of being politicked out of business. However, with that panic pretty much diluted, what has been left is a conflicting range of moods, ranging from confusion to depression to uncomfortable modest growth, alarmingly untrue #fakenews, and a never-ending plethora of meaningless buzz words, which have become so deepset in the fabric of our industry, most of us are resigned to using them, as it’s the only language left to communicate basic sentences to each other.

So let’s try and shed some light on the confusion, based on some of the terrific conversations we had this week:

The Indian IT industry is struggling to cope with “modest growth”. With NASSCOM bravely predicting something in the 7-9% range, most credible analysts are predicting 4-5% for the short, medium and long-term. The reality is, the whole DNA of Indian IT has been borne out of hyper-growth, offering genuine riches to ambitious executives who could project-manage their way to a very nice condo in Bangalore or Gurgaon. The gravy train has now firmly ground to a halt, and most of the lovely folks remaining are still coming to terms with their salary increases slowing down, or disappearing altogether. And many are just pleased to cling to their jobs. The level-headed executives have accepted they are now looking at a more modest outlook for their firms and their own futures, and are making some adjustments, while others are still clambering around trying to find the next hype bandwagon to hitch to their next career move (and payrise). Did I hear the words AI, Blockchain, or RPA anyone?

“Digital” provides a sugar frosting for restating revenues as something that is not traditional IT. While we managed to have about 30 structured meetings with service providers, GICs and tech firms, the term “digital” has become so meaningless, it now ceases to be used in any coherent sentence. It seems to be purely a term now for convincing investors and Wall St analysts that, somehow, traditional services revenues have become something mysterious and new that will set services firms on a new pathway to returning to hypergrowth… and very soon. In reality, “digital” is all about designing new revenue channels for customers using emerging interactive technologies. It’s all about collapsing internal silos within business operations to service customers’ emerging digital needs. If you’re telling me that 50-75% of IT services revenues are now “digital”, then please tell me where all the billions of dollars of app testing, app management and IT infra revenues mysteriously disappeared?

Services has fallen hook, line and sinker for its own #fakenews. Suddenly, every services provider has developed the industry’s leading competency for delivering automation, artificial intelligence and blockchain… overnight. While, barely a year ago, exactly the same firms were the industry’s leading maestros at serving up “digital transformation”. Amazing how they could source thousands of experts, and convince so many clients to make this all possible in barely a few months. Until recently, most providers declared they were adopting a “wait and see” attitude to approaching some of these areas, but now are in there fully-fledged and firing on all their lovely blockchain cylinders. Puhlease ladies and gents! At least, in days gone by, most providers would be relatively honest about their core areas of focus and expertise. Now it seems perfectly acceptable for many just to stare you in the eyes and just lie… what on earth has driven us to this place?

DXC continues to baffle everyone. Can someone please explain what DXC is supposed to be doing? I love the Accenture-esque TV ads, but I am still clueless as to what this firm is actually doing to be the next big thing in the industry. While I was very happy with the DXC branded gifts for writing notes and charging my phones, I would rather just get a little postcard explaining what on earth this new-fangled services business is supposed to be doing that is so special…

Sourcing advisors have just fallen off a cliff. Yeah – they just weren’t present. Barely a couple of years ago they still trawled these halls with their promises of big deals (or would try and sell you some “research” to make a few bucks). Now they have all but disappeared from the equation. Maybe their absence is the most notable sign that the good ol’ days are firmly gone forever, and it’s high-time to wake up to something approaching a normal, stable industry?

The Bottom-line: There are some seriously cool things going in in the world of technology services; we just need to unearth them and change the narrative

There is a lot of goodness this industry is capable of achieving if we can just get out of our own way.

For starters, we’re seeing the fastest revenue growth from several middle-tier providers who are big enough to go after some large complex deals, small enough to work on new concepts with clients and lack the legacy business to focus on going after greenfield disruptive opportunities that the big guys cannot consider. We are seeing some of the major providers unearth new gold by taking ambitious clients to new places of business value, with a high-risk / high value mindset, using technology that is here today and working with them as a trusted long-term partner. We’re seeing real advances in automation, machine learning and digital enablement that are here today – they are now a reality, not some future innovation that is still some years away. We are also seeing a feverish desire from many clients to experiment with blockchain, despite the fact it’s still a long way from providing many meaningful business applications today.

The present is now the future and this should be the most exciting time ever to be innovative, courageous and entrepreneurial. So let’s stop trying to pretend to be something we’re not and focus on the real potential that is staring us in the face. Everyone’s tired of the #fakenews… it’s time to change the channel!

The good old customer BPO business has taken quite a battering in recent years, where the same old usual suspects have embarked on selling predominantly the same old voice services, with most choosing to compete with ever-cheaper global locations to prop up their fragile profit margins. While many of the services majors have chosen to steer clear (or quietly exit the market), the importance of creating an amazing customer experience has never been so critical to customer-facing businesses. Something has gone sorely wrong here…

In an era where every firm aims to be “digital” (and has a Chief Digital Officer to boot), the focus on engaging customers with both digital and voice communications has taken center stage… yet, these legacy call center practices continue to hound the services industry as most of the call center firms continue to fight it out to the lowest common denominator: who can delivery average customer service as cheaply as possible? But you can’t just blame the service providers alone for this behaviour: many of the FORTUNE 500 propagate this behaviour by playing everyone off to squeeze every last drop of cost (and subsequently value) out of their delivery capability… preferring to talk a big digital customer experience game than truly investing in one.

One leader in the space who has taken it upon himself to declare war on these legacy practices is Concentrix President Chris Caldwell, who has masterminded the impressive growth of the firm over the last 12 years, which has included some major acquisitions, notably, the IBM contact center business, BPO firm Minacs and the Australian digital outfit, Tigerspike. The company today boasts annual revenues greater than $2bn with over 100,000 employees globally. Having observed this rapid rise, I thought it high time to invite Chris on here to share a bit more about his story and his views on why this industry needn’t be an FTE hell any longer…

Phil Fersht, CEO and Chief Analyst, HfS Research: Good morning Chris. It’s great to finally get you here on HfS. I would love to hear about your journey on how you wound up running the Concentrix business.

Chris Caldwell, President, Concentrix Corporation: Of course, Phil, It’s bit of an interesting story. I’m not sure if anyone starts out saying that they are going into a career to beat your business, or a call center business. But I worked for a parent company, SYNNEX where I was looking after M&A and the diversification of their business model from the core distribution business. One of the businesses that we bought, very small at the time, was a BPO business, about 30 people which was barely doing over $1m a year and had begun to lose money after some time. And my boss who was the CEO of the other company, said to me, ‘you bought it, you fix it.’ That was the start of the BPO business and that’s when I took over Concentrix at the time. I then had to learn the call center business very quickly; figure out how to grow it and do something with it, which happened in approximately 2005.

Phil: Chris, you then went through this much, much larger acquisition of the IBM call center business in 2013. Can you talk a bit about how Concentrix got to that point, the relationship with SYNNEX, and how things have really progressed since you made that major acquisition?

Chris: Sure, It’s interesting. When we originally invested in Concentrix it was to provide additional services to SYNNEX vendors. SYNNEX is an IT distributor and I can still remember our first services for lead generation for some of the IT vendors, which were very basic offerings.

What became clear very quickly was that the vendors of SYNNEX alone weren’t going to be able to grow us. And so, we had to develop a service offering for new clients and discover something that was compelling for the marketplace.

At the time we looked at doing renewals for vendors, technical support and various other things. We developed this philosophy around how to drive lifecycle management for our end customers and our clients, which was successful. This enabled us to expand in the Philippines and in Latin America. We bought some software technology that covered renewals to drive our value and we grew the business up to about $200 million over several years. Just before the acquisition, we reviewed the marketplace, where we felt that ‘we are too small to be big, and too big to be small. And we either need to double down in this business, or we frankly need to get out.”

We therefore looked at a lot of different companies, and one of the businesses that was coming in the market was the IBM CRM and BPO business. It was a massive undertaking. But when we looked at, it was clear that it would allow us to get into verticals that we would have a very hard time to break into just by ourselves. It had a lot of capabilities that we thought we could exploit. It had a blue-chip client base that would have taken us years to develop. So, we decided that this was the way to go and really grow the business and we went ahead with the IBM acquisition.

It was a huge task. We went from having a business of approx. 12,000 people to bringing on board an extra 35,000 overnight. The business changed from covering 10-11 countries up to 24 countries at the same time. Suddenly we went from primarily servicing smaller banking, consumer electronics and IT types of clients to significant banks and insurance companies around the world This really changed the dynamic of our business, which gave us a launching pad to grow from approx. $1bn dollars 4 years ago, to $2bn this year.

The acquisition clearly allowed us not only to grow our existing client base but also expand into new verticals. It really was a big change for us, but it was a part of this strategy of ‘how do we become a significant player in the BPO business’. Where we see the market going, it was certainly something we had to do to stay relevant in the market.

Phil: That’s a good background, Chris and it’s great to see the effort, and the impact that has gone into this. When we look at where the industry is going, there’s been a lot of sort of noise in the market, in the last couple of years. Firstly, we had the ‘Digital’ bandwagon. Now it’s evolving more around Automation, and AI. How would you say this is impacting the contact center business, in terms of the way the clients are behaving, the way that you are behaving?

Chris: So, I think that there are few things here. For example, we were primarily voice 5-6 years ago. We now are almost 50-50 between voice and non-voice. And our belief is that, and we talk about this a lot in one-office, the reality is that you no longer can segregate voice and non-voice. It requires them to come together, and I see that happening increasingly, where our clients are asking us to take over an entire process or solution, which requires you to pull bits and pieces together to make that happen.

While that’s happening, the reality is that, you’ve got these change elements saying, okay, now that you are doing both voice and non-voice, how can we digitize some of this; now let’s figure out how to put RPA on that. When you look at AI, it has got a lot of sex appeal to it, I am not sure if it has got a lot of meat to it yet. But driving a better process, better efficiencies, and really taking the cost out of the equation for our clients, I just see that continuing. I see the development of tools and technology continuing to try and work out the process to enhance the customer experience – that’s clearly key. I think the brands that will survive will create a much more engaged and personalized customer experience regardless of what they do. And that’s really where we want to see our market growing, where we want to be present.

Phil: Chris, we are seeing a convergence of the traditional and the emerging businesses, in terms of business models and technologies. And I’ve noticed you’ve made acquisitions that seem to approach both markets. You bought Minacs a couple of years ago, and then Tigerspike more recently. Can you sort of expand a little bit on where you are doubling down?

Chris:We will never be an Information Technology Outsourcing player. However, our belief is that we need to have technology integrated into our solutions, some of which will be proprietary technology that we will develop ourselves by our large development team. Then a part of that will be an ‘off-the-shelf’ customization that we will add to finish off the solution. I think just going to the market with a labour solution or a cost solution is irrelevant now. There’s still some business for it, but over the coming months and years, it is likely to diminish.

So, the investments we’ve made in Minacs were about Internet of Things (IoT), Connected Car and Automotive. Our investments in Tigerspike are about driving a superior UX and UI design, as well executional mobile enterprise and mobile applications. We see the needs from our client base and then we also see where the market is going and needing more of these types of services. We really want to be a leader around how to deliver this and frankly disrupt our competitor’s businesses by going to their client’s and saying, ‘not only can we take up this work, we can develop a much better customer experience. We can measure that customer experience differently. We are going to create a very flexible workforce model that allows you to really manage your peaks and valleys at a much more variable cost solution versus a conventional FTE type of solution, which historically has been sort of where a lot of our competitors continue to focus.

Phil: Right, and do you see more opportunity going after tired competitive deals and trying to offer something more disruptive, or by targeting green-field clients which might be in the emerging markets and needing a contact center solution? Where do you see the bigger growth opportunity in the short to medium term?

Chris: So, it’s interesting. We have two very focused directions for these types of clients. One is the larger clients that are in our vertical industry that we are focussed on, where we are coming together with a complete solution. We also invest in the ‘unicorns’, the ‘up and comers’ where we know that out of five or six, a few will perish, but one or two might become the ‘next best thing’. That’s been a very successful model for us for several years. We don’t basically go to market via the contact center. In fact, we are almost 50-50 in terms of voice / non-voice. It’s more about what type of solution that the client is trying to drive; what customer engagement are they trying to achieve? And then building a solution around that wholesome technology, as well as services, and a global footprint, and then everything else that goes along with it. That’s a more compelling thing.

We stay away from industries that are just body shop industries. We tend to stay away from clients who are “most common denominator” procurers and really focus on the people who are trying to differentiate their brand in the marketplace.

Phil:Okay. You mentioned at our Chicago conference a few months ago that you are very tired of these buying practices where many clients are still trying to buy in the old-fashioned procurement way, where the focus remains purely on cost and labor. You made it very clear you wanted to see a shift in how these services are positioned, delivered and managed, where the onus switches to value metrics and business outcomes. I don’t think it’s just the fault of the buyers, as most of the contact center service providers propagate that model… simply because they are comfortable with it as well. What do you think really needs to happen to change this attitude and approach and get some real shifts in a different direction?

Chris: That’s an interesting question, Phil. I see the shift coming when consumers procure services in a different manner. And that tends to kind of permeate all the way through the organization or the company providing those services. ‘We can’t do it in the same old way. We need new innovations. We need to change that up.’ They go back to their vendor partners, and the vendor partners go, ‘we are not going to work with you to procure or deliver these services in the old methodology.’ And we are seeing a bit of that.

I think it’s also particular in our industry, where we see new arrivals taking share from the incumbents by being a very disruptive force in the marketplace. And then they come back to us, and say, ‘we need something different.’ And we say, ‘well, you are not going to be able to procure it the way we normally procured it.’

I think that’s what’s really going to be a driver for change. There’ll still be some companies who want to do everything through procurement, and that’s fine. But I see it as a very big competitive disadvantage to what more nimble companies are doing. And we are seeing very large companies who are incredibly successful in the States now totally change how they are procuring services. Because you are having an end-to end business conversation where you are talking about the solution, the end-customer goal, different types of deliverables and then you are talking about the total cost of delivery execution around these solutions by ending with focusing on how is that better than what their current cost structure is. That’s a different conversation.

Then what tends to happen is procurement comes in, and handles the contract administration, and compliance, which are very important things. However, the difference is that they do not get into how much you are going to charge for this transaction, or how much your FTE rate is etc. and that’s where we see real changes happening in the industry.

Phil: Okay. So, if I could anoint you as the Emperor of Contact Centers for the next year and you could have one wish to change this industry, what would that wish be?

Chris:Ah! Umm. People stop making claims about AI that are completely wrong, irrelevant, and lies!

In all seriousness, I think from my standpoint it’s about having real business discussions around the solutions they need versus trying to procure these types of services through a lowest cost RFP discussion. That I think would up-the-game and would make a healthier business because you find some providers couldn’t compete anymore, and would just fall off the radar, which would then enable the others to drive more innovative solutions. So, a lot of things that people talk about would then start to get baked into these solutions rather than just talked about, which seems to happen a lot in our industry.

Phil:Yes, the blurring lines between hype and what’s actually possible, right? And I agree with you on the AI stuff, we need to have a more realistic conversation about the business. And I like some of the things you’ve been saying around this shift towards an outcome type conversation and less of the administration stuff. This has been really refreshing. Hopefully, we’ll get to see you soon in one of our summits and engage again. It’s been great catching up.

Chris: Yes, for sure. It’s funny, I’m used to saying it a few times over the last week. I love your line about ‘AI is like your first teenage experience where there is a lot of excitement; It happens very quickly, and then a lot of disappointment, and missed expectations’. And I’ve used that a lot to describe the hype in this business. I keep attributing it to you, so you might get a few emails about it. I thought it was brilliant.

Phil: Yes. I seem to have got away with that one! I really enjoyed this and thanks again for your time today.