Our industry has become obsessed with building ever more capable AI models, while enterprises have become equally obsessed with gaining access to them.

Every week brings another benchmark, another frontier model, and another announcement that promises to reshape the AI landscape. Just last week, Moonshot AI’s Kimi 3 was the latest reminder that intelligence at the model layer is becoming more capable, more affordable, and increasingly interchangeable.

That’s great news for enterprises, but it also raises a more important question: If every enterprise rents increasingly powerful intelligence from the same handful of providers, from where will lasting competitive advantage actually come?

The answer is not yet another foundation model, but building intelligence that is unique to the enterprise.

Every organization possesses decades of accumulated expertise that no public model can replicate. It exists in the judgment of experienced employees, the way critical decisions are made, the nuances of customer relationships, industry-specific operating practices, and the battle scars and countless lessons learned through years of execution. That knowledge has always been the real differentiator, yet most organizations have never treated it as a strategic asset. Instead, it remains scattered across people, processes, applications, and documents, becoming increasingly difficult to capture, improve, and retain. As we recently researched, there is $18 trillion in trapped value just wasting away in our Global 2000 organizations. Are these really enterprise debts, or is this the value that needs to be unleashed that keeps them unique?

Services-as-Software™ defined: transforming human expertise into enterprise intelligence

This is precisely why HFS has evolved the concept of Services-as-Software™ (SaS). What began as a way for services and software providers to transform expertise into scalable digital capabilities has become something much broader:

Services-as-Software™ is the HFS operating framework that enables enterprises to build Sovereign Enterprise Intelligence by capturing and codifying human expertise, then continuously improving it through execution.

Net-net, SaS combines AI, business context, enterprise data, and governance to create continuously learning digital capabilities that remain owned by the enterprise rather than becoming part of someone else’s intelligence.

Three principles underpin the SaS approach

Capture and codify human expertise. Organizations must transform human expertise into reusable digital capabilities rather than allowing critical knowledge to remain trapped within individuals, documents, or consulting engagements.

Retain sovereignty over enterprise intelligence. AI should be informed by enterprise context without enterprises surrendering the knowledge, operating logic, and business expertise that differentiate them. Enterprise intelligence must remain an enterprise asset, not become part of someone else’s competitive advantage.

Continuously learn from execution. Every workflow, customer interaction, and business outcome should strengthen the enterprise itself. SaS creates a continuous learning cycle in which execution improves the operating model, enriches enterprise intelligence, and elevates the skills and judgment of the people who work within it.

Traditional software automates transactions, and traditional services apply human expertise. Services-as-Software™ continuously transforms that expertise into enterprise intelligence that grows increasingly valuable through execution:

Building Enterprise Intelligence requires a new enterprise operating model

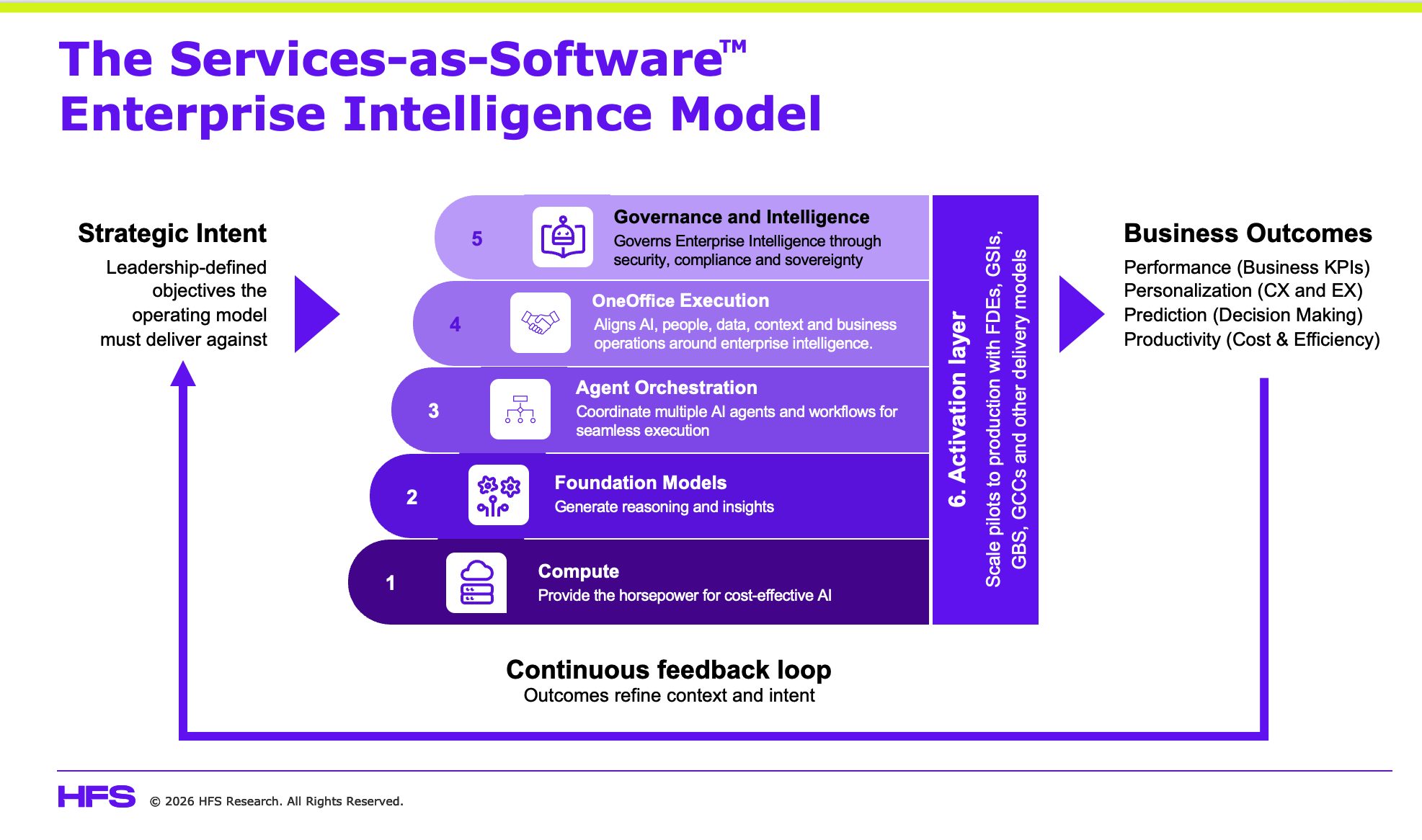

Our Services-as-Software™ Enterprise Intelligence Model connects leadership intent with business execution through six tightly integrated layers, all guided by a clear strategic objective. Every organization begins with an outcome it is trying to achieve, whether improving customer experience, accelerating product innovation, reducing risk, or transforming operational performance. That strategic intent becomes the organizing principle for every layer that follows.

Compute provides the infrastructure that powers enterprise AI, while foundation models contribute increasingly interchangeable reasoning capabilities. Agent orchestration coordinates models, workflows, and governance across complex business processes, ensuring intelligence is applied consistently rather than in isolated pockets across the enterprise.

At the heart of the model sits OneOffice Execution, where AI, people, enterprise data, and business operations converge into a single execution environment. This is where enterprise context is embedded in every decision, enabling AI to understand not only language but also the organization’s operating policies, customer relationships, regulatory obligations, commercial priorities, and institutional knowledge. Rather than automating individual tasks, OneOffice continuously aligns strategic intent with operational delivery while transforming every interaction into enterprise intelligence that remains under enterprise ownership.

Surrounding this execution layer is Governance and Enterprise Intelligence, which protects, validates, and continuously enriches the knowledge that differentiates the organization. Governance ensures AI operates securely, ethically, and in compliance with enterprise policies, while enterprise intelligence captures the insights generated during execution keeping them owned by the business, rather than becoming fragmented across applications or external AI platforms.

The Activation Layer then turns intelligence into organizational change. The activation layer bridges the gap between experimentation and production by combining Forward Deployed Engineers, Global Capability Centers, business leaders and services partners to industrialize AI across the enterprise. It is where isolated pilots become repeatable operating capability. This is where leaders, employees, and business functions adopt new ways of working, redesign processes, develop new skills, and embed AI into everyday decision-making. Without activation, even the most sophisticated AI operating model remains a technical capability rather than a business transformation.

Finally, Business Outcomes complete the learning cycle. Every customer interaction, operational workflow and business result feeds new knowledge back into the operating model, refining enterprise context, strengthening enterprise intelligence and continuously improving future execution.

Unlike traditional technology stacks, the Services-as-Software™ Enterprise Intelligence Model is designed as a continuous learning system. Strategic intent shapes execution, execution generates enterprise intelligence, activation embeds new capabilities across the organization, and business outcomes continually strengthen every layer of the model. The objective is not simply to automate work, but to create an enterprise that continuously learns, continuously adapts and continuously builds intelligence that competitors cannot rent, replicate or buy.

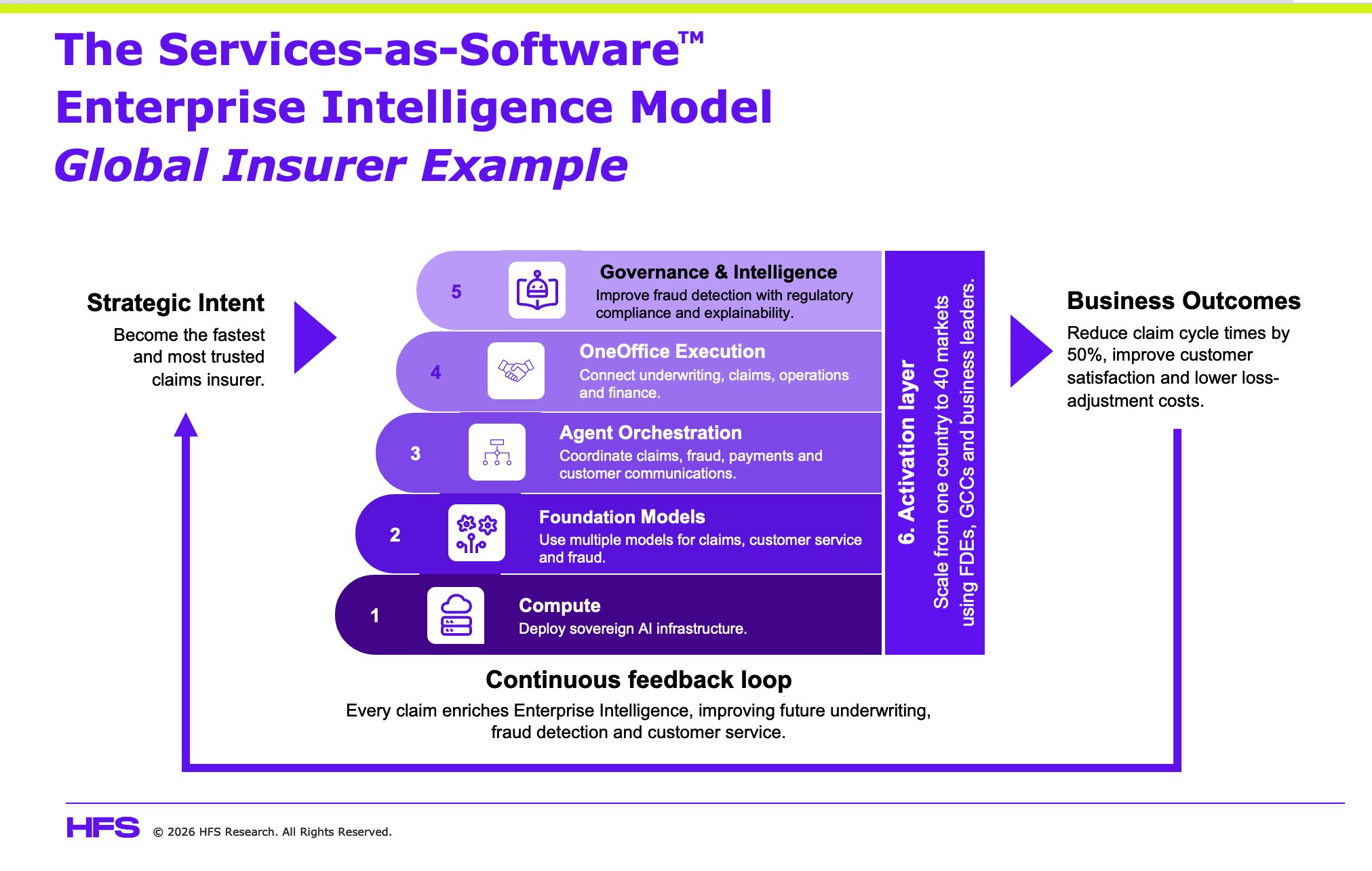

A smarter insurer illustrates how the model works

Consider a global insurance company seeking to reduce claims costs while improving customer experience.

Leadership begins with a clear business objective: settle claims faster, reduce fraud and improve customer trust. Compute provides the infrastructure to run AI at enterprise scale, while foundation models contribute reasoning capabilities for analyzing documentation, summarizing conversations, and supporting decision making. Agent orchestration coordinates specialized AI agents responsible for fraud detection, policy validation, regulatory compliance, and customer communications.

The real transformation occurs inside OneOffice Execution, where those agents operate with full enterprise context. Policy rules, customer history, underwriting practices, regulatory obligations and decades of claims expertise are combined into a single operating model that allows AI to make decisions consistent with how the insurer actually runs its business rather than relying solely on generic model knowledge.

Governance ensures every decision is explainable, compliant and aligned with enterprise policies, while every claim outcome feeds back into the operating model. Fraud patterns become easier to identify, customer interactions become more personalized, and underwriting decisions become more accurate because the insurer is continuously building enterprise intelligence rather than simply processing transactions more efficiently.

The technology improves, but more importantly, the business becomes smarter.

The real debate isn’t open versus closed AI… it’s rented versus owned intelligence.

Alex Karp recently ignited debate by warning that enterprises risk giving away the intelligence that differentiates their business as they increasingly depend on frontier AI providers such as OpenAI and Anthropic. His delivery was characteristically provocative, but the strategic issue deserves far more attention than the headlines it generated.

Every prompt, workflow and business process submitted to an external AI platform raises an important question. Is the enterprise simply consuming intelligence, or is it helping create intelligence that eventually benefits someone else?

This is why the growing focus on open models matters. The debate is not ideological. It is strategic. Open models give enterprises greater control over where inference runs, how models are tuned and how proprietary knowledge is protected. They reduce dependence on any single model provider while allowing organizations to combine multiple models within the same operating environment.

This is also why the Palantir-NVIDIA partnership is more significant than many observers realize. The announcement was never simply about combining GPUs with software. It reflects a broader shift toward enterprise-controlled AI environments where compute, models, orchestration and governance operate together while enterprise intelligence remains under the organisation’s ownership rather than becoming another external dependency.

As foundation models become increasingly interchangeable, the competitive advantage will no longer come from choosing the smartest AI model, but from building the smartest operating model.

Bottom line: Enterprise Intelligence is becoming the defining strategic asset of the AI era

The first generation of enterprise AI was about gaining access to intelligence. The new generation is about creating intelligence that competitors cannot buy because it is built from an organization’s own expertise, operating context, and continuous learning.

Services-as-Software™ provides the operating model for making that possible. It transforms human expertise into Enterprise Intelligence, protects the knowledge that differentiates the enterprise, and ensures every business outcome strengthens the organization rather than an external platform.

Every enterprise will soon have access to increasingly capable AI. The organizations that are already leading their industries are those that continuously build enterprise intelligence through Services-as-Software™, because that is the one asset their competitors can neither license nor replicate.

Main Street is operating in a very different reality to deliver on Wall Street’s lofty AI expectations, and it’s playing havoc with the current state of IT services.

Valuations are plummeting, many heritage services firms are suddenly looking like bargain-basement buys, and services firm leaders are under unprecedented pressure to convince the investor community that their firms are still relevant in the wake of the AI onslaught.

Moreover, many enterprises, seeing this carnage unfold, are greedily demanding increasingly cheaper rates from their services partners, citing AI as the new lever to deliver the same for even less, despite having little clue how to adopt AI themselves. All of today’s services firms are in full AI obsession mode, desperately positioning themselves as AI evangelists and technology implementers, when the reality is that they need to focus on being the foundation-fixers enterprises desperately need to avoid massive AI failure.

Net-net, Wall Street will soon feel the agony of this AI balloon bursting if today’s smartest services firms are not deployed to prepare Main Street for this AI future our whole economy is gambling on. Folks, services-as-software needs to be valued as the balance between success and failure.

The Wall Street Narrative: AI will replace the IT Services Sector

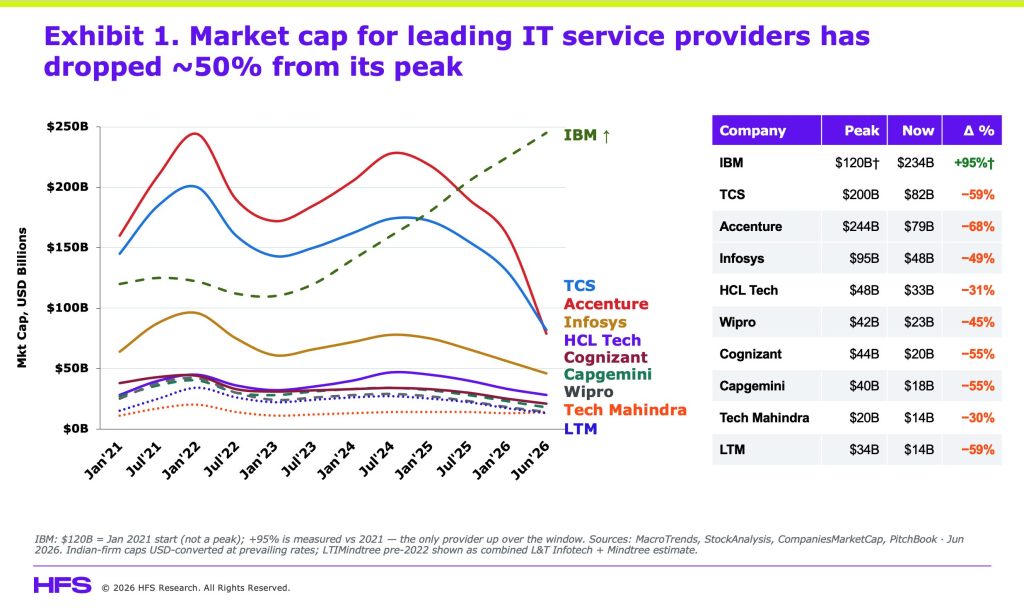

On June 18, Accenture reported what most companies would consider a solid quarter. Revenue grew 6%, EPS increased 9%, margins expanded, and the company generated $3.6 billion in free cash flow. Yet none of that mattered to investors, who sent the stock down almost 18% in its worst single trading day on record.

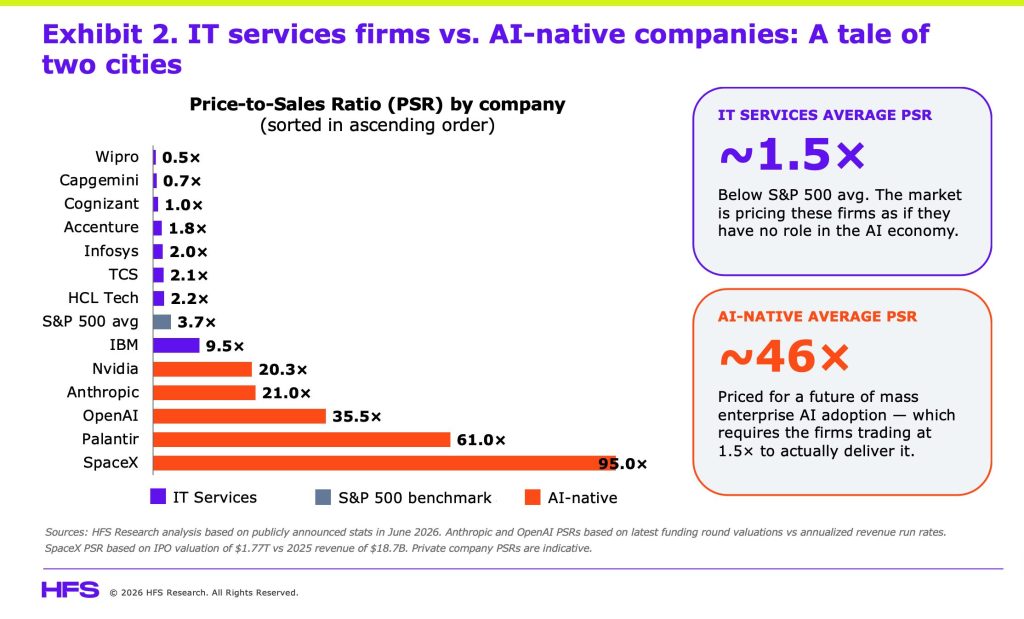

The selloff quickly spread across the sector, pulling down TCS, Infosys, Cognizant, Capgemini and every other major IT services provider. As a result, leading IT services firms now trade at roughly 1.5x revenue, while AI-native companies such as Anthropic, OpenAI, Palantir and SpaceX command valuations ranging from 20x to well over 100x revenue. Wall Street has clearly decided that IT services belong to the past while AI belongs to the future.

Despite all the excitement around generative AI, fewer than one in ten enterprise AI pilots make it into production because organizations remain buried under an estimated $18 trillion of accumulated technology, data, process and talent debt. Until that debt is addressed, the AI future investors are pricing into these companies simply cannot be realized at scale.

Ironically, the firms with the expertise to help enterprises overcome those barriers are the very ones the market is punishing today. That widening gap between Wall Street’s expectations and Main Street’s reality is becoming one of the defining investment stories of 2026, and unless those two worlds begin to converge, this could well be the year AI hype collides with enterprise execution.

Since reaching their peak in 2021, the world’s ten largest IT services firms have collectively lost more than $600 billion in market value. That collapse wasn’t triggered by a collapse in revenue, profitability, or cash generation. Instead, it reflected Wall Street fundamentally changing its view of the sector, re-rating IT services on the belief that AI-native companies represent the future while traditional services firms have become yesterday’s story (see Exhibit 1).

One company largely escaped that fate. While the rest of the sector saw their valuations steadily compress, IBM has roughly doubled its market capitalization over the same period, not because it suddenly started growing dramatically faster than its peers, but because it successfully repositioned itself as a hybrid cloud and AI platform company whose consulting business increasingly revolves around software, automation and proprietary assets rather than people. The market wasn’t rewarding IBM for what it had delivered. It was rewarding what investors believed it could become, a software and AI business that happened to own a consulting arm rather than a consulting business trying to sell AI.

That distinction matters because Wall Street no longer values IT services firms primarily on what they earn today. It is valuing them on whether investors believe they can become something fundamentally different tomorrow.

Wall Street is pricing two completely different futures

The numbers make the disconnect even starker. The largest IT services firms now trade at an average price-to-sales ratio of around 1.5x, less than half the S&P 500 average of 3.7x. Yet these are businesses generating tens of billions of dollars in annual revenue, serving the world’s largest enterprises under multi-year contracts, growing at roughly 5% a year, and consistently delivering operating margins in the 15% to 20% range. They are highly profitable, generate significant cash, and sit at the heart of the global economy. Wall Street is valuing them as though those advantages are rapidly becoming irrelevant.

The companies on the other side of the AI divide tell a very different story. Palantir trades at roughly 60x revenue, OpenAI’s implied valuation equates to around 35x, and newly public SpaceX commands close to 95x revenue. Across the leading AI-native companies, the average price-to-sales ratio now exceeds 45x. Investors aren’t buying today’s financial performance. They are paying for a future in which AI has moved beyond experimentation, every enterprise workflow is AI-enabled, and autonomous systems have become the operating model for business itself (see Exhibit 2).

The gap between 1.5x and 45x isn’t simply a valuation spread. It reflects two completely different beliefs about where value will be created over the next decade. One assumes today’s services model is headed for structural decline. The other assumes AI will scale seamlessly across the enterprise. The question this paper explores is whether both assumptions can really be true at the same time:

The Main Street Narrative: AI Is Hard to Adopt and Even Harder to Scale

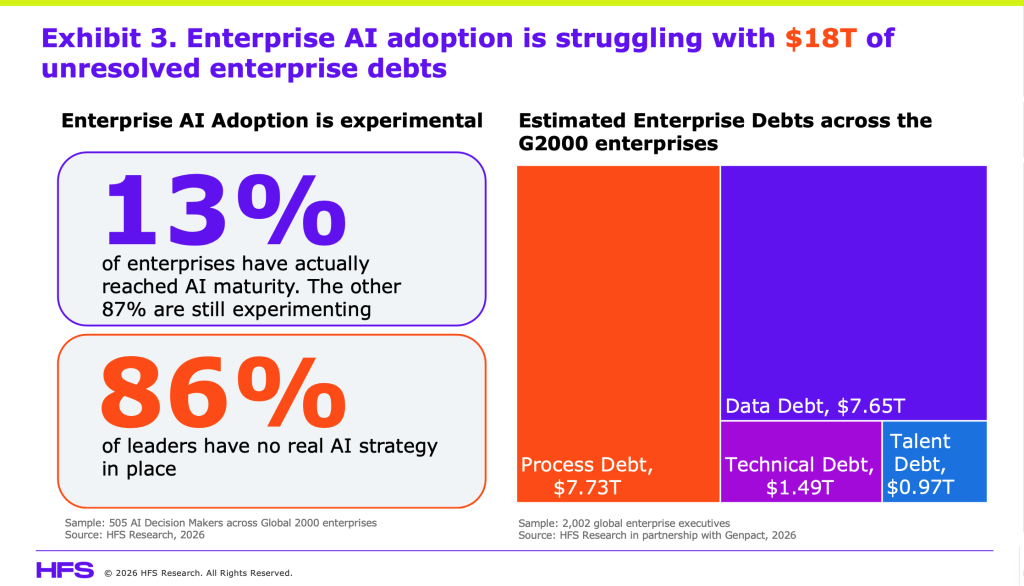

While Wall Street is pricing AI as though the enterprise transition has already happened, Main Street tells a very different story. Enterprises are enthusiastic about AI, but only 13% of Global 2000 organizations have reached any meaningful level of AI maturity, leaving the other 87% still experimenting. Even more telling, 86% of enterprise leaders admit they still lack a coherent AI strategy (see Exhibit 3).

In other words, the AI future investors are valuing at 20x, 50x, or even 100x revenue, which still exists largely in the lab for most enterprises. It hasn’t been deployed at scale, it isn’t fundamentally changing operations, and in most cases, it isn’t yet generating meaningful business value.

The technology isn’t the problem. Enterprise readiness is. Decades of accumulated debt have left organizations structurally unprepared to absorb AI at scale, and until that debt is addressed, even the most powerful models will struggle to deliver meaningful business outcomes. We see this debt falling into four distinct categories:

Technology debt: Aging infrastructure, technical complexity, and years of underinvestment leave enterprises maintaining legacy systems instead of building new capabilities. Many core platforms simply weren’t designed to support modern AI workloads.

Data debt: Critical information remains fragmented across disconnected systems, while weak governance, poor data quality and inconsistent ownership force employees to spend enormous amounts of time cleaning and reconciling data before AI can use it effectively.

Process debt: Too many organizations have introduced new technology without redesigning how work gets done. Siloed processes, inconsistent governance, and manual handoffs create friction that no AI model can remove on its own.

Talent debt: Many organizations still lack the skills, operating models, and leadership needed to embed AI into everyday work. Capability gaps, limited AI readiness, and shortages in critical roles continue to slow adoption even when the technology is available.

Taken together, these four forms of enterprise debt represent an estimated $18 trillion challenge across the Global 2000, which our deep research across more than 2000 Global 2000 enterprise leaders reveals. More importantly, they explain why AI adoption has stalled and this isn’t primarily a technology problem. It’s an implementation problem, a transformation problem, and ultimately a leadership problem:

So, Wall St, who resolves this adoption nightmare? We’ll give you a clue… it’s not the AI-native startups, the model providers or even the infrastructure hyperscalers. It is the Accentures, the TCSs, the Infosyses, the Cognizants, the Wipros and HCLs of the world. The firms that know the client’s ERP, the data architecture, the institutional processes, and the change management levers. The very same firms you’ve written off as irrelevant players from a bygone era where actual expertise mattered and humans needed humans to fashion solutions and outcomes.

The HFS Narrative: The lines between Services and Software are blurring giving rise to a new category we call Services-as-Software

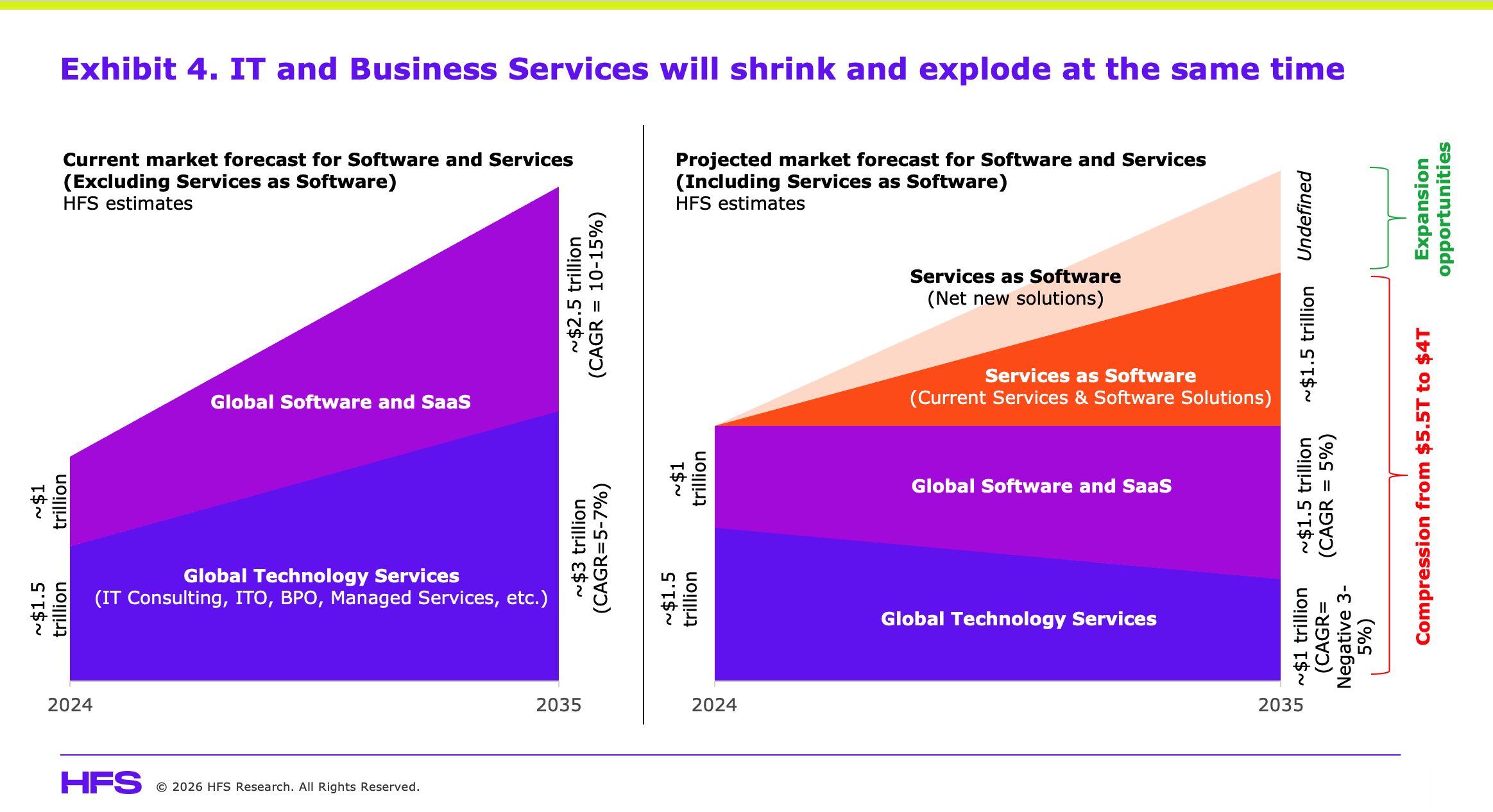

Wall Street isn’t wrong to expect disruption. More than a year ago, HFS forecast that the combined IT services and software market, which was on track to reach roughly $5.5 trillion by 2035 under the old delivery model, would instead compress to around $4 trillion as Services-as-Software fundamentally changes how enterprises consume both technology and services. That compression comes from eliminating value trapped in two legacy models at the same time, which are labor-intensive services that charge for effort and software businesses that continue to monetize static licenses rather than business outcomes.

In other words, the traditional billable-hour model will shrink, and so will the bloated SaaS licensing model that has dominated enterprise software for the past two decades. That part of Wall Street’s bear case is not only credible, but it is also already starting to play out (see Exhibit 4).

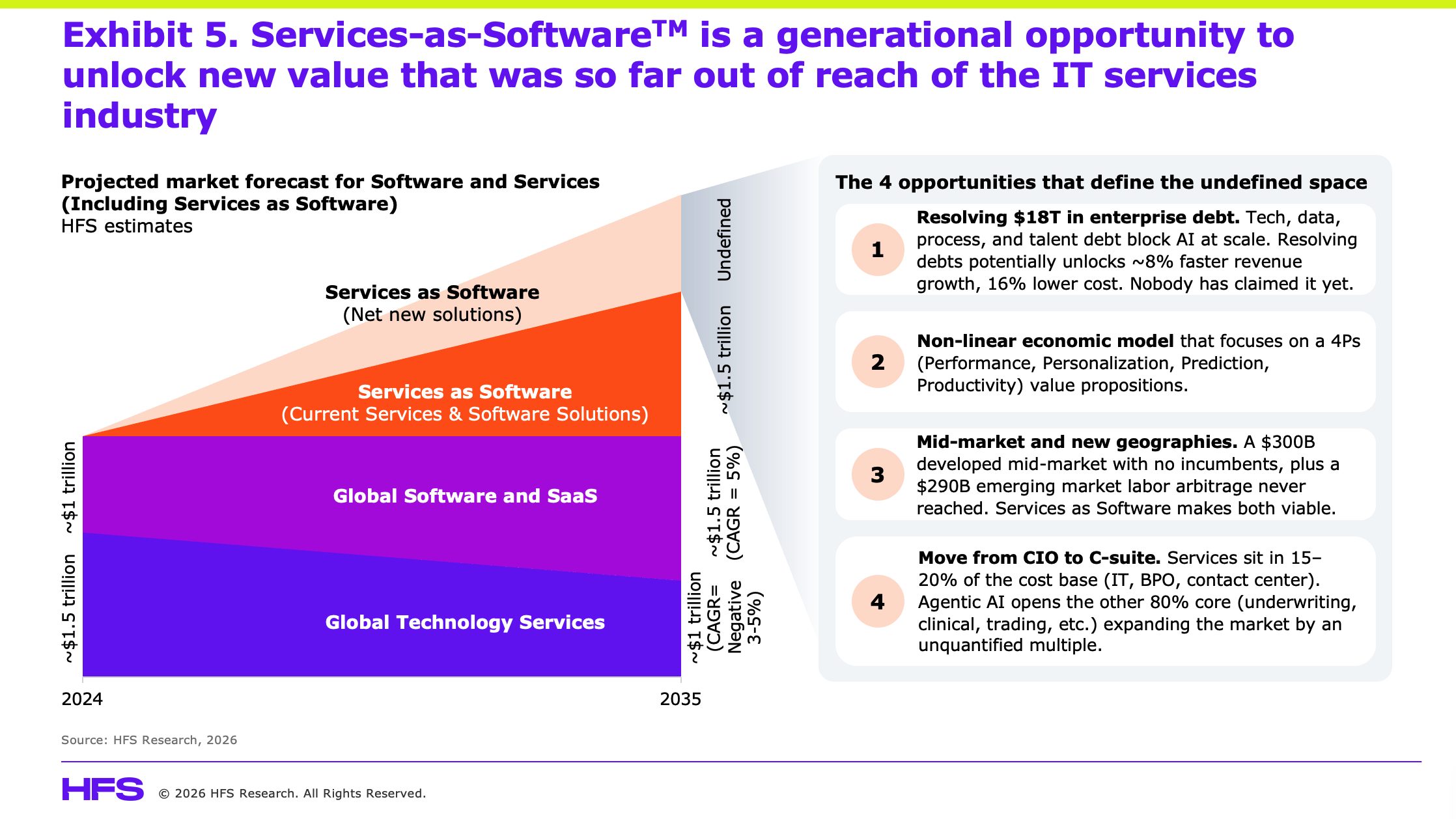

But that is only half the story. While Wall Street is focused on the value being destroyed in the traditional labor-based services model, it is largely ignoring a new triangle of value emerging above it. This is net new opportunity that the old headcount-driven model was never capable of capturing, and it falls into four distinct areas (see Exhibit 5).

Resolving $18 trillion of enterprise debt. Technology debt, data debt, process debt and talent debt are the biggest obstacles preventing AI from scaling across the Global 2000. Traditional FTE-based delivery keeps those problems under control but rarely eliminates them. AI-native remediation changes the economics completely, allowing providers to remove debt rather than simply manage it. The firms that combine AI with deep client relationships, transformation expertise and privileged access to enterprise systems will be uniquely positioned to unlock this opportunity. For enterprises, the prize is significant, with the potential for around 8% faster revenue growth and a 16% reduction in operating costs. Remarkably, no provider has yet established a clear leadership position in this market.

A non-linear economic model. For decades, IT services have priced effort by the hour, tying revenue directly to headcount. AI breaks that relationship because value no longer scales linearly with labor. The next generation of services will increasingly be priced around four sources of business value: Performance, Personalization, Prediction and Productivity. The providers that successfully monetize these four Ps instead of billable hours will build businesses with fundamentally different economics.

The mid-market and emerging economies. Traditional delivery models made it uneconomic to serve companies with revenues between $100 million and $1 billion, leaving a vast addressable market largely untouched. Services-as-Software dramatically lowers the cost to serve, opening a developed-market opportunity worth roughly $300 billion across the US, Europe, Japan, South Korea and Australia. Beyond that lies an even larger opportunity across emerging markets, from regional banks in India to manufacturers in Vietnam and logistics providers in Brazil. AI agents do not require visas or large delivery centers, making markets commercially viable that labor arbitrage could never profitably reach. Together, these opportunities represent an additional addressable market approaching $290 billion.

Expanding from the CIO to the C-suite. Most IT services firms have historically operated across only 15% to 20% of enterprise spending, concentrating on IT, business process services and customer operations. Agentic AI opens the remaining 80% by embedding intelligence directly into core business functions such as manufacturing, supply chains, underwriting, healthcare, finance and trading operations. That dramatically expands the addressable market beyond technology budgets into the heart of enterprise value creation.

The compression of the traditional market is real, but so is the expansion of the market that is replacing it. One opportunity is shrinking while another is only beginning to emerge, and the firms best positioned to capture that growth are the very ones Wall Street has decided to write off.

The Bottom-Line: AI and services need each other far more than Wall Street thinks

Wall Street has drawn a remarkably clear line between winners and losers, with AI-native companies representing the future and traditional IT services firms increasingly seen as part of the past. One side now commands price-to-sales multiples of 60x to 100x, while the other is steadily drifting towards 1x as investors bet that AI will replace the labor-intensive services model that has dominated enterprise technology for the last three decades.

The problem with that narrative is that it only works if enterprises can actually deploy AI at scale, and today they simply cannot. Until organizations resolve their technology, data, process, and talent debt, AI will remain trapped in pilots and proofs of concept rather than fundamentally changing how businesses operate, which means the AI balloon won’t burst because the models fail, but because enterprise adoption never catches up with the expectations already baked into today’s valuations.

This is precisely where Services-as-Software changes the equation, creating an entirely new category that sits between traditional services and enterprise software, blurring the distinction Wall Street still uses to justify a 60x multiple on one side and a 1x multiple on the other. Services firms are increasingly becoming software businesses, software companies are moving deeper into implementation and business transformation, and both are converging on the same outcome-based economic model, even if investors have yet to recognize it.

Ultimately, AI-native companies will have to come back to earth because their valuations depend on enterprise adoption that does not yet exist, while services firms have to convince investors they can escape the economics of selling labor and build businesses that scale through software, platforms and outcomes. Neither side gets where it wants to go without the other, and the companies that figure out how to combine AI innovation with enterprise transformation will define the next era of enterprise technology.

What should you do?

If you’re an enterprise leader…

Treat enterprise debt as a board-level issue. Technology, data, process and talent debt are now strategic liabilities, not operational inconveniences. Measure them, prioritize them and fund their resolution with the same discipline you apply to capital investments.

Stop celebrating pilots and start measuring business outcomes. If an AI initiative cannot demonstrate meaningful commercial impact within 90 days, question whether it deserves further investment. Every failed pilot delays the transformation you’re actually trying to achieve.

Buy outcomes instead of effort. Whether you’re purchasing software, AI or services, the conversation should begin with business value, not licenses, tokens or full-time equivalents. If a supplier cannot explain how they improve your P&L, they are selling technology rather than transformation.

Align your AI and services partners. The AI platform and the implementation partner are solving the same problem. If they are working independently, you will pay for the disconnect.

If you’re a services provider…

Stop selling labor and start eliminating enterprise debt. Clients don’t need more people. They need measurable improvements in performance, productivity and business outcomes.

Give investors a Services-as-Software story they can believe. Markets are no longer rewarding headcount growth. They are rewarding recurring platforms, proprietary IP and software-like economics. Show how your revenue mix is changing or accept that your valuation won’t.

Take the conversation beyond the CIO. AI is no longer an IT discussion. It is an operating model discussion that belongs with the CEO, CFO and business leaders responsible for growth and profitability.

Move aggressively into the mid-market. AI has fundamentally changed the economics of serving companies that were previously too small for global providers. This window will not remain open for long.

Stop talking endlessly about AI and refocus on yourself as a foundation fixer with Services-as-Software. Clients already know AI matters. What they need is a partner that can fix the foundations, preventing AI from delivering value. Become known for resolving enterprise debt through Services-as-Software, not for producing another AI presentation.

If you’re an AI-native company…

Sell business outcomes, not tokens. Enterprises don’t want to buy compute. They want faster decisions, lower costs and new sources of growth. Your commercial model should reflect that.

Get closer to implementation. A model working in a demo is very different from a model operating inside complex enterprise systems. The services firms understand those environments. Work with them rather than around them.

Earn trust before expecting scale. Every enterprise deployment that delivers measurable value strengthens your long-term valuation far more than another funding round. Sustainable enterprise adoption will ultimately matter more than benchmark scores or headline valuations.

The future doesn’t belong exclusively to AI-native companies or to traditional services firms. It belongs to the organizations that combine the strengths of both. That is the real opportunity emerging from this market correction, and it is why Services-as-Software may prove to be the most important category the enterprise technology industry creates this decade.

Box’s CEO reminds us that 88% of the economy runs on different rules, different budgets, and different constraints than the VC world…

If you want to understand why most enterprises are still stuck in AI pilot purgatory, you can do a lot worse than listen to Aaron Levie. The Box CEO recently delivered one of the most lucid, unsparing conversations I’ve heard on what agents actually mean for large organizations, and almost none of it matched the breathless narrative coming out of the labs and the VC echo chamber. He had to practically shake his interviewer, Harry Stebbings, to get some of it across.

So here is what enterprise leaders really need to hear about agentic AI…

Stop measuring AI’s impact on the 12% of the economy that already has it. The other 88% is where the transformation happens.

“Everybody is so myopic about this,” Levie said, and his point is that the tech industry represents 10-12% of GDP, while the banks, pharma companies, manufacturers, and industrial firms that make up the other 88% are not sitting on engineering surplus but are chronically under-resourced. AI-assisted development does not threaten Silicon Valley jobs but opens engineering-grade capability to the rest of the economy for the first time, meaning CS graduates no longer go to Google but to John Deere or Eli Lilly, and the profession expands rather than contracts.

The same logic applies to legal, because AI-generating contracts do not reduce the workload but flood the system with more work requiring qualified human review, and the bottleneck was never generation but courts, regulators, and approvals, which means there will be more lawyers in five years, not fewer. The real casualty is the junior pipeline, because when AI does the apprenticeship work, you lose the mechanism by which the next generation learns the craft, and every bank and law firm that built its talent model around that apprenticeship structure is facing that reckoning now.

The workflow needs to be redesigned for agents, not for people

Every large enterprise that wants meaningful returns from AI automation has to go through genuine change management. Data is fragmented across decades of employee-brought tooling, legacy document management systems, and network file shares. Agents will find the wrong contract, the wrong document, the wrong piece of customer data, not because the models are bad, but because the underlying data state was never organized with machine consumption in mind. People could navigate ambiguity by knowing where to look, which agents cannot. For example, a healthcare organization is using agents to automate patient referrals, which sounds like a win, but if the next available specialist appointment is still 18 months out, nothing has changed for the patient. The bottleneck was never the paperwork, but was the shortage of doctors as automation makes the queue move faster, but does not make the queue go somewhere. Every enterprise has a stack of constraints like this sitting behind the process they just automated, and agents surface them faster than any previous technology. You can automate the intake, but you cannot automate the shortage of doctors. Automation does not eliminate constraints, but reveals them faster.

Professional services firms are not being replaced by AI. They are about to get busier than they have ever been

Agentic is creating years of structural work for transformation partners. If a Fortune 500 company wants an agent to identify contract renewal risk, it might encounter ten systems holding contracts, half incompatible with modern API architecture, which means getting that data organized and context-aware is not a model problem but a decade of work for Accenture, Cognizant, or the next generation of specialized implementation partners. And there is one more dynamic that guarantees the services layer persists, which is that someone has to be accountable when it goes wrong, and as Levie put it, “you are not going to be able to blame Anthropic,” which means the moment you need liability you need ownership, and the moment you need ownership you need people, a structure that does not dissolve with better models.

Hire the agent operator now. Up to a million of these roles are coming and enterprises that wait will not catch up.

Levie floated a job title the industry is still workshopping, which is the agent operator, someone technical enough to understand MCPs, CLIs, and agent configuration files, but also fluent enough in business process to go into a marketing team or legal operations function and translate AI capability into workflow leverage, redesigning the process around the agent rather than the person who used to do it.

The second a new model drops your workflow probably breaks because the prompting syntax changes, which means this is not an IT role but a standing discipline sitting at the intersection of technical acumen and operational transformation. Levie puts the job creation at 500,000 to a million roles, with enterprises that build this capability internally seeing their AI returns grow and accelerate over time, because each workflow redesigned makes the next one faster and cheaper, while those that treat agent deployment as a one-time project will find themselves stuck in an endless cycle of pilots that nobody is equipped to sustain or scale.

Move AI spend out of the IT budget and into operating expense. Your CIO’s ceiling will never fund the transformation your business needs.

For the first time, technology providers can walk past the CIO and approach the line of business directly, offering a productivity return that justifies a share of operating budget, which is new, given that IT budgets have always been the ceiling. Levie’s view is that this probably doubles global enterprise technology spend by unlocking a new category of investment tied directly to workflow productivity. But what Silicon Valley keeps ignoring is that enterprises have EPS commitments and annual planning cycles, which means every dollar of AI spend has to justify itself against earnings targets.

So the practical discipline is to identify the 5-10% of your workforce doing the highest-value work, give them the best models with no capacity constraints, apply more efficient and cheaper models to the next tier of use cases, and let general productivity run on commodity AI, because treating every employee as equally deserving of frontier model access sounds inclusive but blows your budget and your earnings commitments in the same quarter.

Avoid single-vendor dependency in your AI stack. The enterprise AI platform race will end like cloud: multiple winners, massive market.

When asked to call the race between OpenAI and Anthropic, Levie gave the most pragmatic answer available, which is that in 2010 AWS had $500 million in revenue, Azure had just launched, and GCP had barely launched, yet today it is a multi-hundred-billion-dollar ecosystem where all three won, which is likely how AI ends up, with enterprises running multi-model stacks because no serious organization will accept single-vendor dependency in infrastructure this consequential.

Take your AI security risk seriously. Agents create attack surface faster than any human team can review it.

The moment you start generating code with AI you produce it at a volume that outstrips any human team’s ability to review it, with every feature shipped representing a potential vulnerability the agent introduced without anyone catching it. Meanwhile, the offensive side has exactly the same advantage and can scan for vulnerabilities at machine speed, leaving you with more surface area and faster attackers simultaneously. This is why Levie concluded that “agents are the solution to the problem that agents have caused,” a recursive dynamic that makes agentic security one of the few genuinely new infrastructure categories in this cycle.

Audit your platform stack for API depth, not UI richness. Agents do not care about your human interface… they care about your business logic.

Software built around dense interfaces designed for human clicking is genuinely at risk, because if agents are doing the work that humans used to do, that UI value simply evaporates. But software that embeds proprietary business logic in its API layer is a completely different story, because an ERP encoding two decades of supply chain rules is not just a database, and a platform enforcing FINRA retention at the API level is not just a file store. Agents actually need those capabilities more than humans did, which means the right question when evaluating any platform in your AI stack is not how good the interface is, but how deep the business logic runs and whether it was built to govern agent behavior rather than just enable human navigation.

Bottom line: Stop waiting for the technology to eliminate the hard parts. It will not.

As Levie put it, “we haven’t removed humans from the loop, we’ve just changed where they enter the loop,” and that single sentence should be on the wall of every enterprise transformation team. The real constraint is not model quality but workflow redesign, data readiness, change management, and accountability for when something goes wrong, and that work does not get automated away but gets more important with every agent deployed.

Enterprises that understand this will build a durable advantage, while those still waiting for the technology to eliminate the hard parts will still be waiting in five years as their competitors do the structural work that actually sticks.

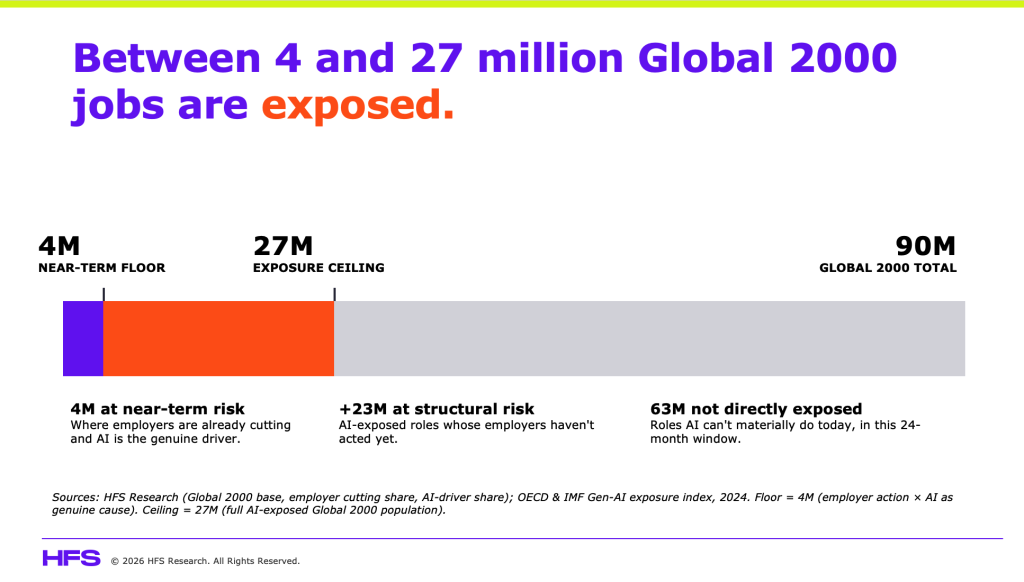

Twenty-seven million. That is the number of corporate roles across the Global 2000 that HFS Research identifies as meaningfully exposed to AI-driven elimination, displacement, or fundamental redesign over the next three years. Not factory-floor jobs or gig roles, but 27 million white-collar, salaried, benefits-eligible positions held by people who built careers on the assumption that their employer had a plan for the future.

Sadly, most employers do not, and the workers carrying the most exposure are the ones least likely to know it:

Credibility and trust of leadership are at stake when layoffs are made under a false AI narrative

Most of the organizations sitting on top of these 27 million exposures have no coherent plan for what they are doing with AI, let alone what happens to the people inside it. Our research across 505 AI leaders across the Global 2000 tells us only 14% have a clear enterprise AI strategy with defined goals and outcomes. The remaining 86% are split between strategies that are still developing and inconsistent (39%), AI activity that exists only in pockets with no enterprise direction (32%), and no defined strategy at all (15%).

Exhibit 1: Only 14% have a clear AI strategy. Everyone else is improvising.

“We’re restructuring for the AI era” sounds considerably better on an earnings call than “we spent two years in meetings about AI and have absolutely nothing to show for it.” Both announcements produce roughly the same stock reaction, but one of them is a strategy and the other is a prayer dressed up in a press release. At some point over the next few months, a CEO in your industry will announce a major workforce reduction and call it an AI transformation. The board will nod, and investors will reward the action. And somewhere in a conference room near you, someone is going to ask why your organization is not doing the same thing.

That moment is coming. For millions of workers across the Global 2000, it will not feel like a transformation. It will feel like they have sorely misplaced their trust in a leadership that is finally running out of road.

Enterprises are shrinking before they have figured out what they are rebuilding

AI is becoming the justification for decisions that were already forming, not the cause of them. The language will be about transformation. The reality will be a spreadsheet that was already open before the AI strategy was written, and a mounting leadership debt that is now being called in.

Because at the center of all of this is a simpler problem. There is no human accountability at the helm of AI, and enterprises are shrinking before they realize what they’ll need to rebuild. HFS Research estimates that between 17 and 20 million workers sit inside Global 2000 organizations with no clear AI strategy, no meaningful investment in their people, and no plan for what comes next. These workers are already living the consequences of decisions their leadership hasn’t made, and desperately need the training and resources they haven’t provided.

The current wave of layoffs is largely a smoke screen. The harder wave has not hit yet.

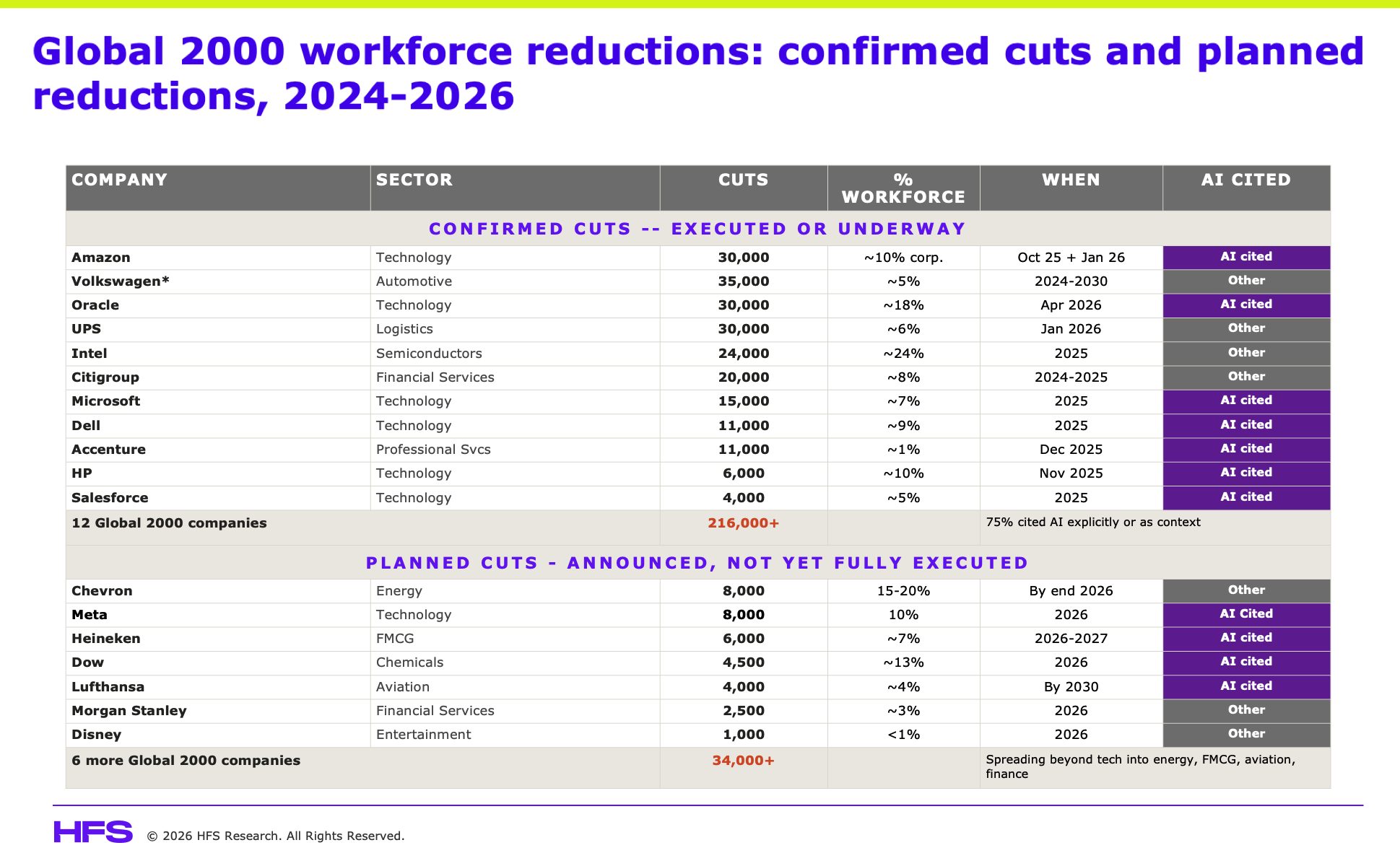

More than 216,000 roles have already been cut across just 12 Global 2000 companies since 2024, with 71% of those announcements citing AI as a driver (See Exhibit 2). But look a little closer at what those companies were actually doing. Oracle cut 30,000 roles while committing $300 billion to AI infrastructure. Amazon eliminated 30,000 corporate positions while investing $80 billion in AI in the same year. Microsoft reduced 15,000 roles in the same quarter it said AI was generating 30% of its code.

These are not distressed companies cutting from weakness. They are cutting with intent, removing what no longer fits while investing heavily in what comes next. The problem is that now everyone thinks they can do the same thing and the narrative travels faster than the capability behind it. No roadmap is required, no real AI muscle needed. Just the right language and a board that has been waiting long enough to want a number. As this spreads across the Global 2000 and the bandwagon forms, the trend will be mistaken for strategy. That is where we hit the danger zone.

Exhibit 2: Global 2000 workforce reductions: confirmed cuts and planned reductions, 2024-2026

The organizations feeling this pressure the most are the ones with the least to show.

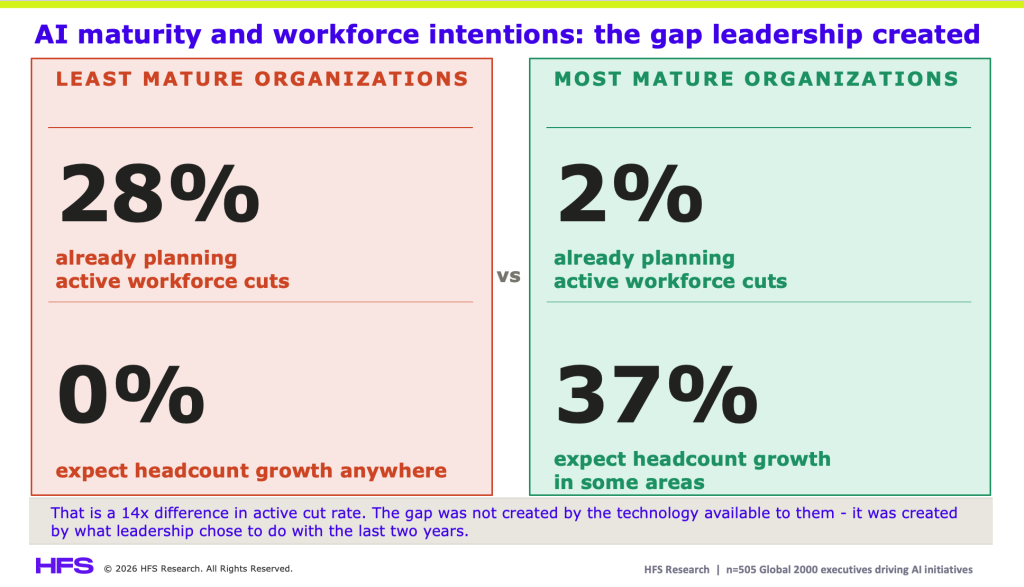

Cutting tens of thousands of roles while investing billions in AI infrastructure requires having billions in AI infrastructure to invest in. Most do not. The organizations heading toward the most damaging reductions the ones reacting through headlines without thinking through capabilities. In our latest study, we found that 28% of the least AI-mature organizations in the Global 2000 are already planning active workforce cuts. Among the most mature, 2%. Zero percent of the least mature expect to grow headcount anywhere. Among the most mature, 37% do.

The organizations in the 2% are cutting toward something. The organizations in the 28% are cutting because someone looked at the headlines, asked why we are not doing the same, and nobody in the room had a good answer. That is leadership debt.

Exhibit 3: AI maturity and workforce intentions

Across the Global 2000, a significant share of organizations still sit in low to mid levels of AI maturity. When you map that distribution against workforce exposure, the numbers become difficult to ignore: 17 and 20 million roles could be exposed to reactive reduction over the next two to three years, concentrated heavily in organizations that have not yet moved beyond experimentation (See Exhibit 4).

Exhibit 4: Of 90 million Global 2000 workers, where does the risk sit?

Leadership did not find the frozen middle. Leadership built it.

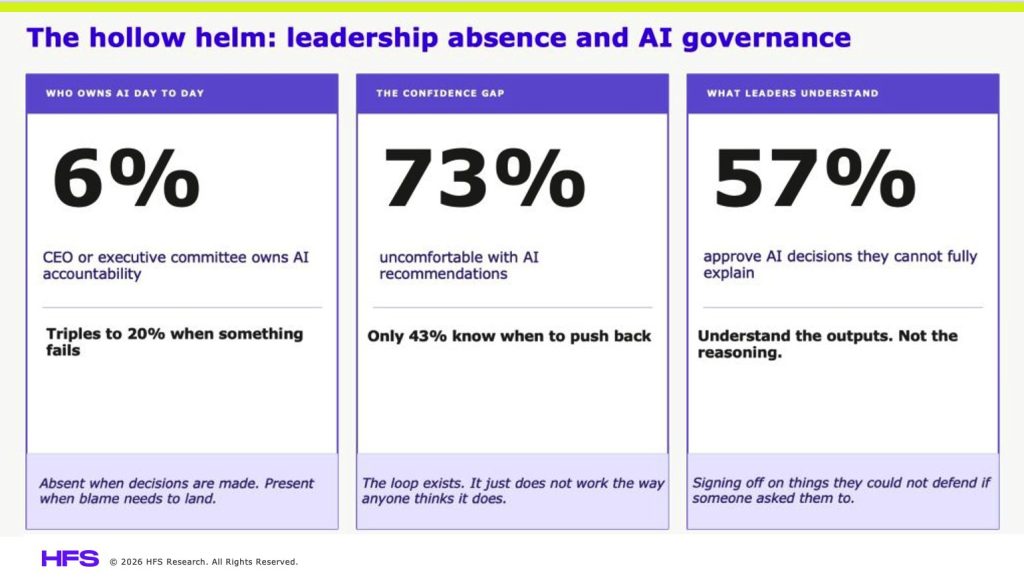

The organizations on the wrong side of that maturity gap ended up there because of choices that felt reasonable at the time and compounded quietly until the board ran out of patience. AI was delegated to the function best equipped to install it, not the function best equipped to lead it. The CIO got the roadmap, the CEO got the quarterly update, and somewhere between those two things, the actual decisions about what the organization was becoming, what work would change, and what the workforce needed to know never got made.

Our research puts a number on what that looks like in practice (Exhibit 5). Only 6% of CEOs own AI accountability day to day, though that number triples when something fails. 73% of leaders are uncomfortable with AI recommendations, but only 43% know when to push back, and 57% approve decisions they cannot fully explain. Nobody owns it, nobody can challenge it, and nobody can defend it when the board asks what two years of investment have actually produced.

That is the moment the conversation stops being about strategy, and someone opens a spreadsheet looking for a number, not because AI failed to deliver, but because leadership could never show that it had.

Exhibit 5: When it comes to AI in major enterprises, nobody owns it, few can challenge it, or defend it

Executives expect AI to eliminate the resource and skills constraints, but many are choosing to eliminate the resources first.

If this moment is being misread, it is because too many organizations are reacting to outcomes instead of defining them.

The companies getting this right are not moving faster and with intent. They know what AI is changing, where they are investing, and how their workforce is evolving as a result. Everyone else is still trying to reverse-engineer a strategy from someone else’s announcement.

This is the point where leadership either takes control of the direction or defaults to reacting to it. The difference shows up quickly, and the workforce is where it becomes visible.

Here is what needs to happen next:

Stop using AI as an explanation and start using it as a decision framework. If you cannot clearly articulate what AI is changing in your business, you are not ready to make workforce decisions tied to it.

Assign real ownership, not shared accountability. AI cannot sit across committees and still be directed with intent. One team, one leader, clear accountability for outcomes.

Move from pilots to irreversible decisions

If your AI efforts have not changed how core work gets done, you are still experimenting. Start redesigning workflows, not just testing tools.

Define what you are building before deciding what to cut. Headcount reductions without a clear future state will hollow out capability rather than build it.

Invest in people at the same level as you invest in technology. AI capability without workforce capability creates dependency, not advantage.

Resist copying what the market rewards. Other companies’ cuts are not your strategy. Without the same maturity and direction, the outcome will not be the same.

The Bottom line: You cannot shrink your way into an AI strategy

Align AI to growth by purposefully remodeling your workforce.

AI will reshape the workforce. The only real decision is whether leadership does it deliberately or whether the market does it for them. The leadership debt that’s been accumulating for two years is coming due; will it be repaid through strategy and capability, or will the workforce bear its burden?

Anthropic just announced a $1.5 billion joint venture with Blackstone, Hellman & Friedman, and Goldman Sachs to launch an AI-native enterprise services company. Service providers still debating whether this is a threat have already lost the first round.

The entire US economy has made a giant bet on AI, and Anthropic finds itself front and center

Just think about it: Anthropic propelled its revenues from $9bn to $30bn last year and is now projected to be valued at $1 trillion for its impending IPO. This firm is on, perhaps, the most unique rapid journey in tech industry history (and that includes NVIDIA), and while its technology is rewriting the rule book for knowledge work, the skills needed to keep pace with the adoption, the hype, and the insane sums of money propping up the stock markets are in a desperate short-fall. Hence, it’s little surprise Dario and co do not have the patience and confidence to bet all their chips on the traditional service providers to take them to the promised land.

I’ve been saying for a while that the real threat from Anthropic wasn’t whether they’d build a services arm. It was what happens when a model provider moves just far enough into execution to start shaping how the work actually gets done. Now we have our answer, and it came faster and with more firepower than most people expected.

What this confirms is the struggle many enterprises are having to move past pilots into full agentic deployments, and Anthropic desperately needs to drive execution itself with AI engineers, AI orchestrators, and deep data engineering skills. They clearly do not have the patience to deploy this 100% through SI partnerships. In addition, Anthropic wants access to PE portfolio companies that are some of the most aggressive adopters of AI technology, as it drives immediate value creation.

This is much more than a services play. It is a move to own the execution layer in enterprises

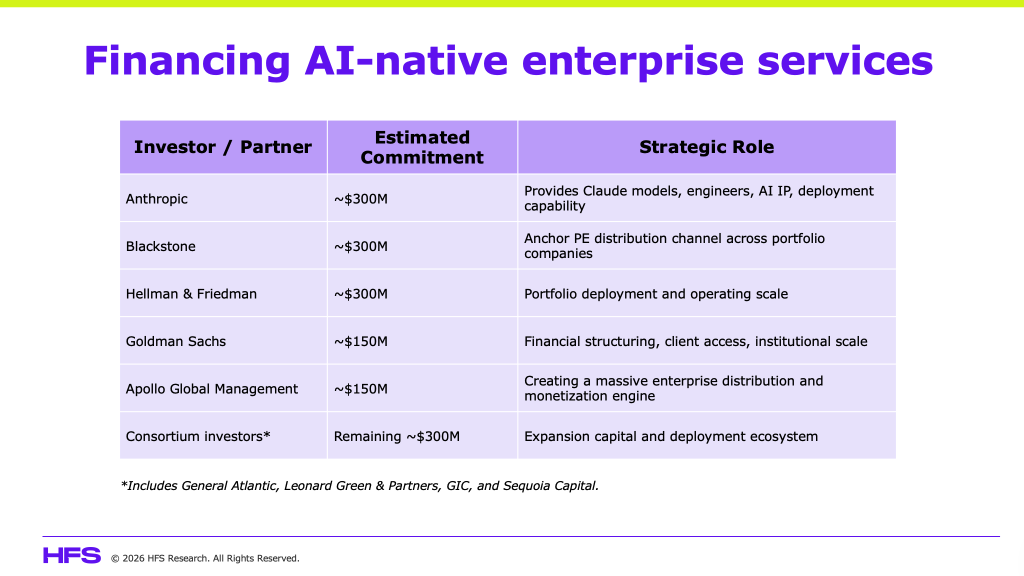

The new venture, backed by approximately $1.5 billion in committed capital and drawing additional support from General Atlantic, Apollo, Sequoia, and Singapore’s sovereign wealth fund GIC, is designed to embed Anthropic’s engineers and models directly into the core operations of mid-size businesses.

Anthropic has positioned this as additive to its existing service provider partnerships, and at the large-enterprise tier it largely is. But the real shift is the delivery model itself to being forward-deployed, model-lab-led, outcome-committed. That becomes the new reference point for services value, not just for Anthropic engagements, but for every provider engagement that follows. This is why the threat is so widely misunderstood. This is not a services land grab, but a play to own the execution layer before service providers understand what they are about to lose.

Anthropic takes inspiration from Palantir, but the ambition runs much deeper

The structure mirrors Palantir’s forward-deployment model, combining implementation capability with ownership of the underlying model in a single entity, which immediately undercuts the traditional consultant’s proposition of independent trusted advice. But no tech vendor willingly runs a labor-intensive services business at scale. Services margins are structurally inferior to software, and every operator in this industry knows it. The fact that Palantir had to build this model, and that Anthropic and OpenAI are now constructing the same thing with billions in committed capital behind them, tells you something fundamental: the current services model is not fit for proving agentic AI value in the enterprise. They are not entering services to compete with providers. They are entering services to replace the need for how services are currently delivered. And critically, they are building the channel they could not rent.

Stop telling yourself this is just a mid-market play. The playbook written there becomes the enterprise standard

Every service provider leadership team that reads this and tells itself this is a contained mid-market experiment is asking the wrong question. The threat was never whether Anthropic builds a consulting practice. The threat is what happens when the model stops being an ingredient and becomes the architecture. When Anthropic defines agent behavior, sets guardrails, determines task decomposition, and establishes execution patterns at scale, it is no longer supplying capability. It is defining how work gets done. That creates a platform dynamic, and platform dynamics concentrate value at the control layer while commoditizing everything else. This is the scenario service providers should fear most: not that they lose deals, but that they lose relevance in how value is defined. They risk being pushed down the stack into execution capacity while the model provider owns the orchestration layer, the IP, and ultimately the client relationship. HFS research already shows fewer than 10% of enterprises have scaled agentic AI beyond pilots. The mid-market is where that logjam breaks first, and once those delivery patterns are proven there, they become the benchmark for what good looks like everywhere else. That benchmark will not be built on effort. It will be built on outcomes.

This is not channel conflict. It is revenue compression arriving faster than incumbents can reinvent themselves

Calling this channel conflict misses the point entirely. This is a structural reset of the services value equation. When Anthropic delivers outcome-committed work with its own engineers embedded in execution, the expectation of value shifts for the entire market, not just for Anthropic engagements. Traditional services lines, particularly application development and maintenance, testing, support, and large-scale integration, begin to compress rapidly once that expectation takes hold. We are already seeing early evidence of 30 to 40% effort compression in certain workflows, and over the next several years, this translates into low-to-mid single-digit annual revenue deflation across commoditized services segments, with far steeper pressure in specific pockets. The market is not shrinking. But the labor-driven revenue pools are, and they are shrinking faster than most incumbents can reinvent themselves. Blackstone President Jon Gray described this as a shortage of engineers capable of implementing AI at speed, but that was not a talent statement. It was a power statement and tells you exactly who is repositioning to own execution, and once execution shifts, value ownership follows.

Targeted capability bets will beat scale every time in a disruption play

The joint venture structure reveals Anthropic’s strategy with unusual clarity. They are not acquiring large service providers because doing so would import the very inertia and structural complexity they are trying to disrupt. Instead, they will scale through targeted hires, forward-deployed engineers, and boutique acquisitions with domain expertise and workflow IP, which is a faster and cleaner way to build execution capability without inheriting legacy delivery baggage. OpenAI is already moving in the same direction with TPG and Bain Capital. That convergence should remove any remaining doubt about where this market is heading and how quickly the window for incumbents to respond is closing.

Bottom line: The services pie is expanding but ownership is being rewritten, and waiting is not a strategy

This is not about Anthropic doing services for the sake of services. It is about redefining what value in services actually is. Services-as-Software is expanding the total opportunity, but ownership of that opportunity is shifting toward those who control the models, the orchestration, and the execution patterns. Service providers that evolve into outcome-driven, agentic, forward-deployed operators will find themselves on the right side of that shift. Those that do not will not disappear overnight, but they will be steadily, irreversibly pushed out of the value layer that matters. The winners will own trust, integration, and accountability in complex enterprise environments. The losers will keep selling effort in a world that has stopped paying for it.

Accenture has 30,000 Claude-trained practitioners. Deloitte rolled out Claude to 470,000 employees while Cognizant deployed it to 350,000 more. Infosys signed its own major Anthropic deal last week, covering regulated industries. That is over one million practitioners already committed to Claude delivery, while most of their competitors are still reviewing governance frameworks and unsure where to place their agentic bets.

According to Menlo Ventures, Anthropic has already captured 40% of the enterprise AI market share, up from 24% at the start of 2025. The land grab is not coming, folks, it’s already happened. If your firm does not have a Claude delivery strategy built around trained practitioners, proprietary accelerators, and outcome-based pricing, you may already be on the scrap heap of labor-based services waiting for the incinerator.

Anthropic’s enterprise market share jumped from 24% to 40% in less than a year. That is not a trend… it is a takeover.

Claude’s ascent is not accidental. Four structural advantages are driving it:

First, Anthropic’s explicit safety and governance positioning unlocks regulated sectors like financial services, healthcare, and public sector where every other AI vendor is stuck in procurement limbo.

Second, Claude is increasingly agentic. It does not generate text and stop. It executes multi-step workflows, reasons across massive context windows, and acts as a participant in enterprise processes, not just a productivity add-on.

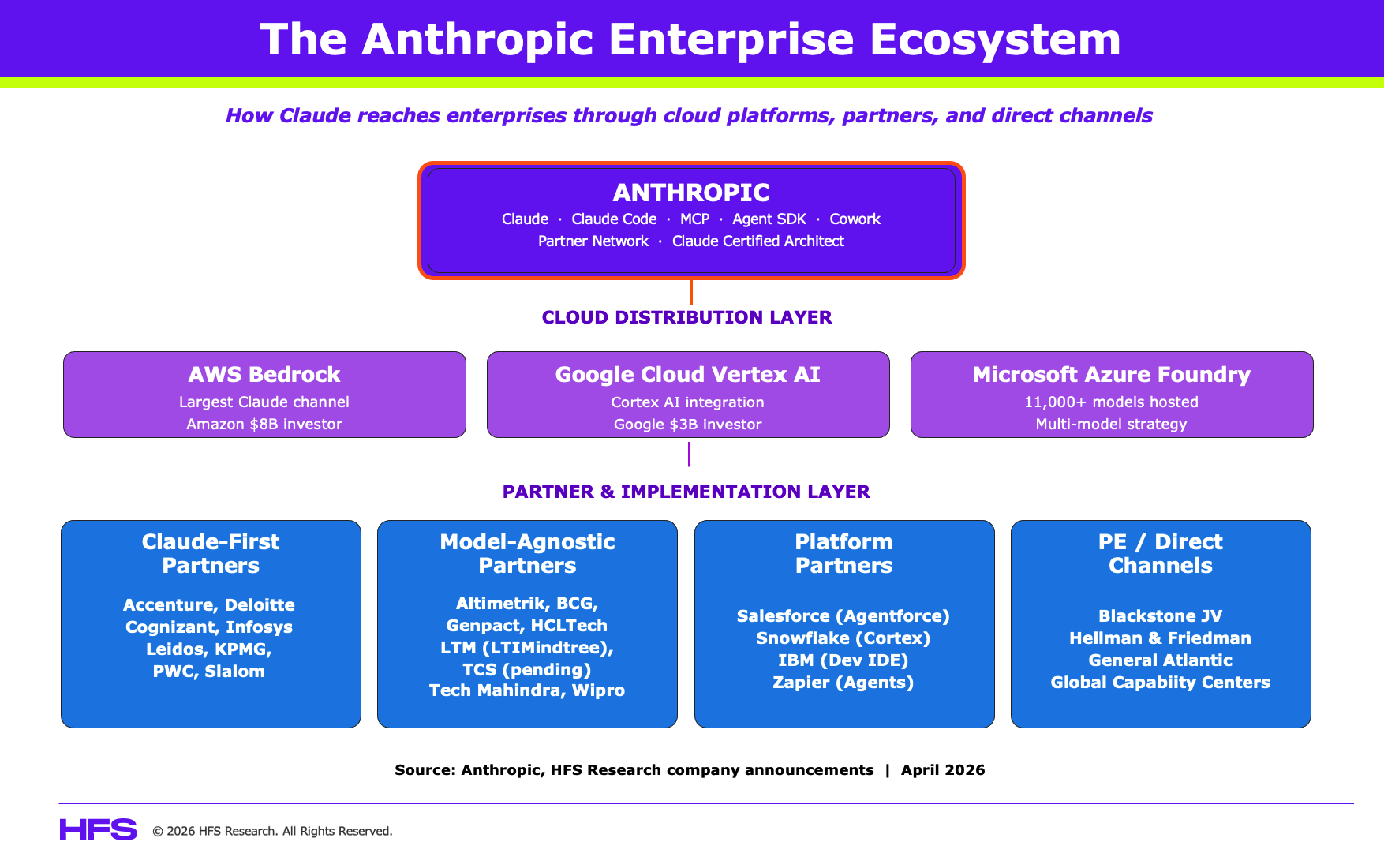

Third, Anthropic has distributed Claude through Amazon Bedrock and Google Cloud, making it available inside existing cloud relationships rather than requiring standalone commercial negotiations. That combination of trust, capability, and distribution is exactly what the services market needed to move from experimentation to scale. Not to mention Amazon is one of Anthropic’s investors.

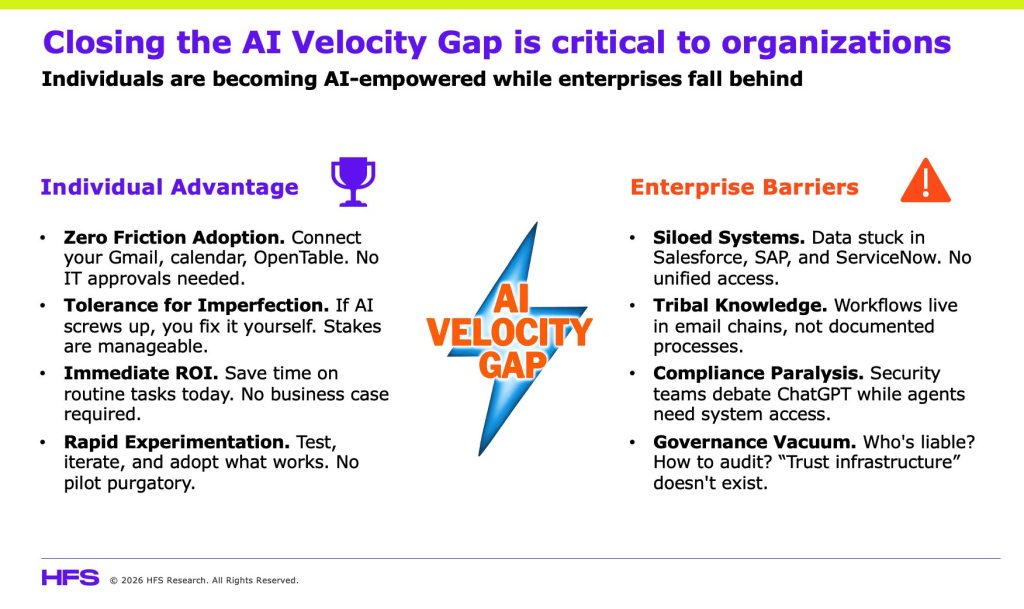

Fourth, Anthropic is becoming the most significant emerging AI Platform to close the Enterprise AI Velocity Gap. Our extensive research across the Global 2000 reveals that only 10% of enterprises deploy GenAI or agentic AI organization-wide today, and only a similar number report a cross-departmental rollout. We call this the AI Velocity Gap: individuals racing ahead with AI tools while enterprises remain gridlocked in governance committees, data silos, and change management debt. Claude, embedded into the delivery platforms of the likes of Accenture, Deloitte, Infosys, and Cognizant, is a significant mechanism through which many enterprises will eventually deploy to narrow that gap. The service providers that have embedded Claude deepest in their delivery models are positioning themselves to own the transformation budgets that follow.

Two camps are emerging in Anthropic professional services, but not in the clean, binary way many assume.

The first camp has moved decisively, building its own armies of Claude coders.

Accenture formed a dedicated Anthropic Business Group with 30,000 Claude-trained professionals, focused specifically on regulated industries where governance requirements are strictest. Deloitte deployed Claude to its entire global workforce of 470,000 across 150 countries in what became Anthropic’s largest enterprise rollout. Infosys integrated Claude into its Topaz AI platform and built a dedicated Anthropic Center of Excellence targeting telecom, financial services, and manufacturing. Cognizant has deployed Claude across 350,000 employees, aligning Claude models, Claude Code, MCP, and the Agent SDK with its core engineering platforms, and is developing vertical solutions starting with financial services through its Agent Foundry platform to embed agentic workflows into regulated enterprise environments. Slalom announced a formal partnership with Anthropic in November 2024 focused on ethical AI deployment on AWS and has a live case study with United Airlines, where Slalom used Amazon Bedrock and Claude to build AI-powered flight update customization.

Two additional consulting firms belong in this camp. PwC announced a formal collaboration with Anthropic in February 2026, focused on embedding Claude, including Cowork, Claude Code, Opus 4.6, and Sonnet 4.6, into regulated enterprise environments in finance and healthcare. PwC is developing industry-specific plugins, risk frameworks, and workflow redesigns around Claude, positioning it as more than a model-agnostic integrator. KPMG has partnered with Anthropic specifically on Claude for Life Sciences, helping clients integrate Claude into scientific research, clinical workflows, and regulatory processes.

These firms are not just offering clients access to Claude. They are building proprietary delivery infrastructure and repeatable assets around it. That is a fundamentally different competitive position.

The second camp is taking the hyperscaler path, embedding Claude via Amazon Bedrock alongside other foundation models, positioning as integration specialists rather than dedicated Claude practitioners.

Genpact, HCLTech, Wipro, Tech Mahindra, Altimetrik, LTM, and others fit here. The model-agnostic approach preserves flexibility but creates a real commoditization risk. When every provider can access Claude through the same cloud channel, differentiation has to come from proprietary accelerators, domain IP, and managed services layers. Building those assets takes time that is running out fast.

TCS, the largest Indian IT services firm with annual revenue of $30 billion, is notably absent from Camp 1 but moving fast. Its COO confirmed in April 2026 that TCS is working significantly with Anthropic and that a formal partnership announcement is expected soon. The parallel is striking: TCS and Anthropic now operate at roughly the same revenue scale, yet one sells human labor while the other sells the technology replacing it.

IBM represents a third path worth watching: productizing Claude inside enterprise development tools. That creates stickiness that project-based deployments cannot match and positions IBM to capture recurring revenue from AI-embedded workflows rather than one-time transformation fees.

A further competitive dynamic deserves attention: OpenAI’s push to formalize its ecosystem of services partners. Over the past year, it has deepened multi-year collaborations with firms such as McKinsey, BCG, Accenture, and Capgemini to scale enterprise adoption of its models and emerging agent platforms.

This creates a more nuanced competitive landscape. Large providers like Accenture are clearly hedging across both Anthropic and OpenAI, while strategy firms such as McKinsey, BCG, and Bain have built strong alignment with OpenAI’s enterprise roadmap. However, none of these partnerships are exclusive, and most services firms are deliberately maintaining multi-model strategies.

The reality is not a clean split between “Claude camps” and “OpenAI camps.” Systems integrators are increasingly supporting multiple model ecosystems, often shaped by hyperscaler relationships such as AWS, Microsoft, and Google.

Many Global Capability Centers (GCCs) are building direct Anthropic capability from inside the enterprise.

Many GCCs, particularly the 1,700-plus operating in India, are no longer back-office execution units. The most advanced GCCs are functioning as internal AI innovation labs, piloting Claude directly through Bedrock or enterprise agreements, and building proprietary workflow automation that bypasses the need for third-party services firms entirely (see earlier article). When a GCC at a major US financial institution can deploy Claude Code across its engineering team, build MCP integrations to its internal data stack, and redesign its own processes without engaging an Accenture or an Infosys, the addressable market for traditional services engagement shrinks from below, not just from above. Services firms must position themselves as the architects of GCC AI strategy, not just the vendors GCCs replace. That requires a fundamentally different client conversation than the one most account teams are having today.

A related disintermediation threat is emerging from private equity. Anthropic is in discussions with Blackstone, Hellman and Friedman, and General Atlantic to create a joint venture targeting up to one billion dollars in funding, with Anthropic contributing two hundred million. The venture would deploy Claude across PE-backed portfolio companies in a Palantir-style model combining software licensing with implementation consulting. If completed, this creates a distribution channel that bypasses traditional services firms entirely for a large segment of the enterprise market.

Microsoft is playing a different game entirely: hedging across every frontier model so it can ride whichever one leaps forward next.

Microsoft deserves its own analysis here because its strategy does not fit neatly into any of the camps outlined above. While services firms are choosing either deep Claude commitment or model-agnostic flexibility, Microsoft is building the platform layer underneath all of them. Its Azure AI Foundry now hosts over 11,000 models, including Claude through a direct Anthropic partnership, alongside OpenAI’s GPT family, Meta’s Llama, Mistral, Cohere, and Microsoft’s own emerging MAI models. Copilot itself is shifting from an OpenAI-only product to a multi-model architecture that can compare and cross-check responses across models. Microsoft is not betting on one model winning. It is betting that no single model will win permanently, and that the real margin lives in the orchestration, governance, and distribution layer that sits between frontier models and enterprise workflows.

This is a structurally sound hedge, and services leaders must understand Microsoft’s strategy to get the most from their relationship (and the services they’ll bring to market with Microsoft). When Microsoft makes Claude available through its Azure AI Foundry alongside its own MAI models, it commoditizes the model layer for enterprise buyers. This strategy will result in switching cost between frontier models dropping for everyone. Instead of models driving the value, the value migrates upward to whoever controls the integration fabric, the security and compliance overlay, and the agentic workflow design. In 4D chess, Microsoft is positioning itself to be that control layer across the entire enterprise stack, from Azure infrastructure to Microsoft 365 to GitHub to Dynamics. If it can execute, the services firms that built deep single-model practices will face a platform owner that can swap models underneath its customers without anyone noticing. That is the quiet threat inside Microsoft’s multi-model strategy: it turns model-specific expertise into a depreciating asset. (If you are a service provider leader read that last sentence again!)

But its not all rainbows and unicorns. The counter-argument is execution risk for Microsoft. Its Copilot adoption has underwhelmed, with only 15 million subscriptions against 450 million commercial seats, and Microsoft’s stock has pulled back sharply on concerns that its $100-billion-plus annual AI capex is not yet translating into proportional enterprise returns. Building your own MAI models while maintaining a $13 billion OpenAI partnership while also onboarding Anthropic and Mistral creates strategic complexity that no amount of Azure infrastructure can paper over. Services firms with deep Claude or OpenAI practices may find that their focused expertise is exactly what enterprise buyers want when the platform layer feels too broad and too uncertain to bet on alone.

The question for services leaders is not whether Microsoft’s hedge is smart (or necessarily a threat). It is whether your firm’s differentiation is deep enough to survive inside a platform that is designed to make your model-specific expertise interchangeable.

Claude is not in the lab anymore: it is already compressing costs and cycle times across financial services, healthcare, pharma, and software engineering.

The most important dynamics for services leaders is not the partnership announcements. It is what Claude is already doing inside enterprise processes. In financial services, Bridgewater’s investment research team is using Claude to draft Python scripts, run scenario analysis, and visualize financial projections, with the system designed to replicate junior analyst workflows and reducing time-to-insight by 50 to 70% on complex equity, FX, and fixed-income reports.

Data Studios in cybersecurity, HackerOne has reduced vulnerability response time by 44% using Claude. In pharmaceutical development, Novo Nordisk, the maker of Ozempic, was averaging just 2.3 clinical study reports per writer annually, with each report running up to 300 pages, and has used Claude to transform that bottleneck. In telecom, TELUS deployed Claude to 57,000 employees, giving them direct access to AI-powered workflows across developer, analyst, and support functions. In software engineering, Claude Code now holds over half of the AI coding market, enabling junior developers to produce senior-level code and onboard in weeks instead of months.

Several additional deployments reinforce the pattern. Brex automated 75% of expense transactions using Claude on AWS Bedrock, achieving 94% policy compliance and saving 169,000 hours monthly, equivalent to $56.5 million in salary. Snowflake integrated Claude into its Cortex AI platform, achieving over 90% accuracy on text-to-SQL queries across more than 10,000 customer organizations. Zapier deployed over 800 internal Claude-driven agents, achieving 89% employee adoption and 10x year-over-year growth in Claude-powered tasks. TELUS, beyond its 57,000 employee deployment, has built over 13,000 AI-powered tools internally, saved more than 500,000 staff hours, and realized over $90 million in measurable business benefits. Salesforce made Claude the foundational model for Agentforce 360, its autonomous AI agent platform that crossed $500 million in annual recurring revenue with 330% year-over-year growth. Cox Automotive integrated Claude via Bedrock to generate personalized communications, doubling lead follow-ups and test drive appointments.

Claude Code is not a productivity tool. It is a direct substitution mechanism for the junior-to-mid engineering workforce that anchors the Indian IT services delivery pyramid.

Unlike standard AI coding assistants that suggest completions line by line, Claude Code operates agentically. It reads codebases, plans multi-file changes, executes terminal commands, runs tests, and iterates on failures without human intervention at each step. A junior developer using Claude Code is not a faster junior developer. They are operating with the output velocity of a mid-level engineer. A mid-level engineer using Claude Code closes the gap on senior-level architecture decisions. The economics of the delivery pyramid do not bend gradually under this pressure. They break.

Cognizant has already moved Claude Code, MCP, and the Agent SDK to the center of its engineering practice. That is the right instinct, and it points to what a transformed software delivery practice actually looks like: fewer bodies doing rote implementation, more architects governing agent workflows, more domain specialists translating business requirements into agentic task structures, and more QA and oversight roles ensuring that autonomously generated code meets compliance and security standards. The headcount does not disappear. It reshapes. The firms that lead this transition will capture premium margins. The firms that resist it will lose application development mandates to competitors who can deliver faster, cheaper, and at better quality with smaller teams.

These are not proofs of concept. They are production deployments in some of the world’s most demanding and regulated environments. The compression of skilled labor hours is already measurable, and it is accelerating. The services firms that understand this are repositioning the human role toward oversight, orchestration, and domain judgment. The ones still debating whether to pilot will face a client base that has already moved.

The real battleground is not which firm has a Claude deal. It is who can govern, integrate, and redesign work around agentic AI at enterprise scale.

Three disciplines will determine which service providers win the next wave of AI transformation revenue. First, workflow integration: connecting Claude securely to enterprise systems across SAP, Salesforce, ServiceNow, and other data repositories that currently sit in silos. Most enterprises do not yet have the foundation for this, which means the integration layer provides significant service value. Second, AI governance and oversight: building monitoring, approval flows, and audit trails into AI-enabled operations. HFS data confirms that AI growth hinges on how effectively organizations strengthen security, governance, and data control. Third, workforce redesign: determining the optimal human-to-agent ratio across business functions and restructuring roles, incentives, and metrics accordingly. In practice, this means replacing entry-level execution roles with four new archetypes: AI Workflow Architects who design the agentic task structures that replace manual processes; AI Output Validators who govern quality, compliance, and accuracy of autonomous outputs; Domain Translation Specialists who convert business requirements into agent-ready instructions; and AI Operations Managers who monitor multi-agent systems and escalate exceptions. These are not theoretical roles. They are the functions that determine whether AI deployment creates durable enterprise value or just generates liability at scale.

Anthropic’s Model Context Protocol is significant here. Standardized connectivity lowers the integration burden for models but raises the design burden. Someone still has to architect how those connections work inside complex, legacy-laden organizations. That architecture work is high-value, recurring, and defensible. It will not be commoditized as quickly as code generation or document drafting. Cognizant has made MCP a core part of its Claude deployment, using it to give AI agents standardized access to developer tools and enterprise data rather than treating each integration as a bespoke project. That is the right instinct, and the providers that follow it will build more durable margin than those still quoting FTEs.

The revenue model shift is also accelerating. When AI reduces the hours required to deliver a given output, clients will not accept time-and-material pricing. HFS Research data shows agentic AI investment is set to surge 38% in 2026 alone, and enterprises are demanding outcome-based models, AI operations management services, and verticalized solution packages. The providers that have retooled their pricing and delivery models around these structures will capture that spend. The providers still quoting FTEs will lose it. This is the Services-as-Software inflection point. The firms that survive the transition are those that stop selling access to practitioners and start selling guaranteed business outcomes delivered by a combination of human expertise, proprietary IP, and AI agents working in concert. That is a fundamentally different commercial model, a different margin structure, and a different conversation with the CFO. The firms that master it will not just retain their existing clients. They will take share from competitors who are still explaining why their FTE count is a feature rather than a liability.

Bottom line:The Claude services land-grab is firmly underway for the early leaders.

Accenture, Deloitte, Infosys, and Cognizant have collectively committed over one million practitioners to Claude delivery and are building proprietary accelerators, governance frameworks, and vertical solution factories around it. Claude is already cutting research cycle times by 50 to 70% at Bridgewater, slashing vulnerability response by 44% at HackerOne, and transforming clinical documentation throughput at Novo Nordisk. This is not future potential. It is current competitive reality.

The financial trajectory reinforces the urgency. Anthropic’s run-rate revenue surged from nine billion dollars at end of 2025 to over thirty billion dollars by April 2026. Enterprise clients spending over one million dollars annually doubled from five hundred to one thousand in under two months. Eight of the Fortune 10 are Claude customers. Claude Code alone reached two point five billion dollars in annual recurring revenue in nine months. The Claude Partner Network, backed by one hundred million dollars in Anthropic investment, now includes a Claude Certified Architect certification and fivefold growth in partner-facing technical staff. The window for establishing a competitive Claude practice is not narrowing. It has nearly closed.

Service providers that have not matched that commitment are not just behind on a feature. They are ceding the transformation budgets that will define industry positioning for the next decade. Stop forming committees to evaluate AI strategy and start building the delivery capability to execute one. Every quarter you delay is a quarter your clients spend getting comfortable with your competitor’s Claude practitioners instead of yours.

The analyst and advisory industry is staring down its biggest existential moment in decades. When intelligence is instant, content is infinite, and influence is increasingly algorithmic, the old playbook of reports, briefings, and relationship-driven insight is breaking fast.

That’s exactly why bringing in someone who understands how influence really works in a digital, AI-saturated world matters.