- Search

Month: June 2017

What GBS leaders can learn from the Rise and Fall of Empires

There is no value in painting GBS as black or white. Like almost everything in life, it has shades of gray. The most important question is ‘how can we make it better?’Read More

The Dark Side of Shareholder Value: Its impact on the very people it’s designed to benefit

We need to rethink shareholder value and the integral link it has with the very element it seems to be bent on eliminating – people.Read More

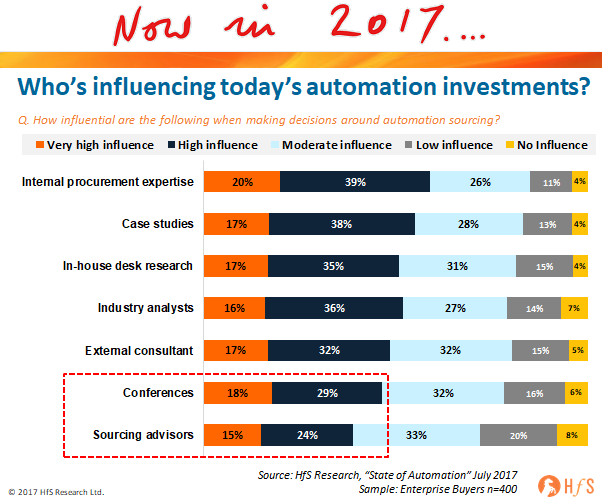

Why have so many sourcing advisors failed with automation?

New findings from HfS' "State of Automation 2017" study shows an alarming lack of influence from sourcing advisors in the automation spaceRead More

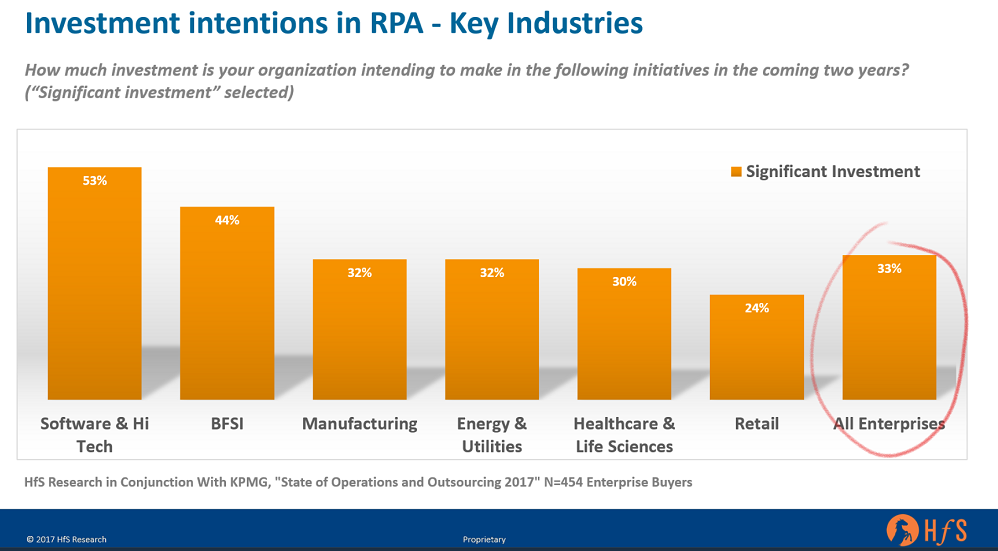

A third of enterprises are making significant investments in RPA

New research from the HfS/KPMG 2017 State of Operations and Outsourcing Study reveals a third of enterprises are fully invested in RPARead More

Off-Shore-Based Service Providers Look to Develop “Meaningful” Presence in the U.S.

Our research shows the there is a significant drop across the board in the move to “offshore” business and IT work – finance and accounting and HR, in particular.Read More

Microsoft Dynamics Gets Saas-y

HfS has just published its first HFS Blueprint Report: Microsoft Dynamics Services 2017.Read More

We are in the People Elimination business. How did it get this bad, and can we change course? (Rant warning)

Why are we on an inexorable nosedive to the lowest common denominator of creating and promoting business operations that no longer require people?Read More

Time to hangout with the real robo-bosses at the FORA Council this September

What happens when you put Alastair Bathgate, Mihir Shukla, Max Yankelevich, Daniel Dines, Tijl Vuyk in the same room?Read More

HCSC’s Sale of TMG Health to Cognizant Shows A Move to Focus – and Partner– for Better Outcomes

The changes in the healthcare market driven by consumerism and compliance are driving healthcare plans to “rethink” their business and operations strategy.Read More

Look into my eyes – I can see the future.

The future of outsourcing is linked very strongly to the future of technology and its use in the enterprise – often it’s very hard to distinguish between the trends of these two things.Read More