- Search

Month: August 2016

Why is Gartner spewing such irresponsible and unsubstantiated data about “robobosses”?

Gartner's latest claim is that 3 million of us will be supervised by robots in 18 months' time. Great.Read More

Why An Outcome-Based Approach Can Shatter the Watermelon Effect of Outsourcing Contracts

What to do about that "feeling" that even if SLAs are Green, something feels Red!Read More

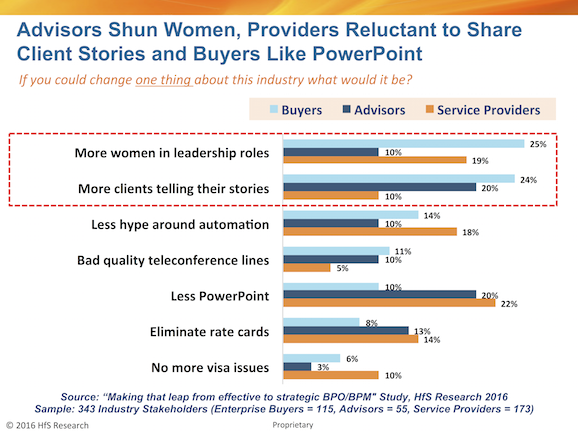

Beware men in gray suits: Clients want more senior women, more real client stories and less automation hype

Brand new data from the HfS-Nasscom 2016 BPO study has some revealing dynamics on the role of womenRead More

The testing community has to find a distinctive voice for the As-a-Service journey

Testing services have never fully mirrored the broader IT market in the way it was seeking to optimize its organizational models. So what are the innovations and models that are driving testing services forward?Read More

You can bet your mortgage-as-a-service on Accenture, Wipro, Cognizant and TCS

Mortgage As-a-Service Blueprint for 2016: The Evolving Service Provider LandscapeRead More

Who Are the As-a-Service Winners in Energy Operations? HfS’ inaugural Energy Operations Blueprint reveals frontrunners Accenture, EPAM, Infosys, Wipro and TCS

Who Are the As-a-Service Winners in Energy Operations? HfS’ inaugural Energy Operations Blueprint reveals frontrunners Accenture, EPAM, Infosys, Wipro and TCSRead More

Social media has turned us into a society of gibbering digital morons

It’s time to make things real again…Read More

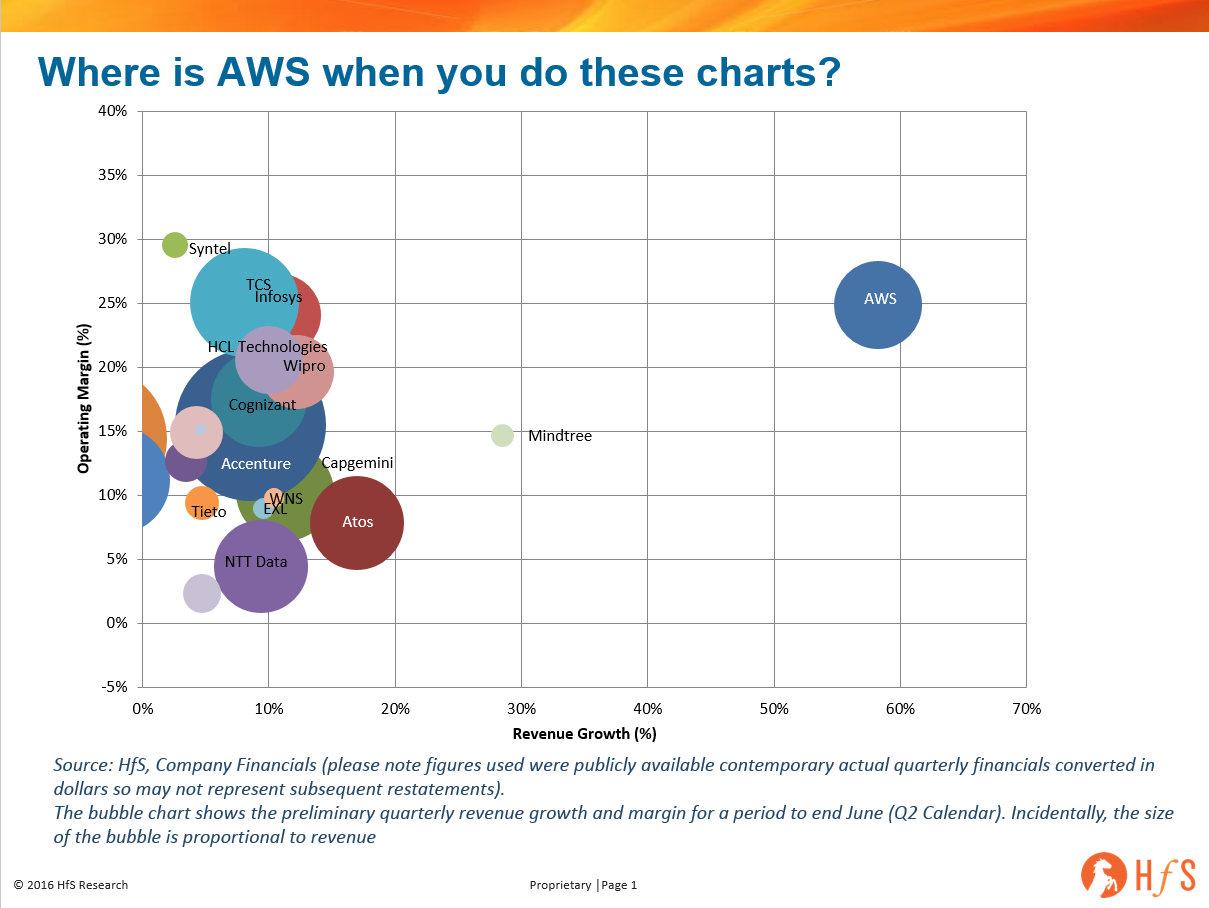

Where is AWS in relation to the other IT services players? And a sneak peek at Q2 provider chart…

Sneak peek of Q2 provider chartRead More

Gazing into the Automation Crystal Ball

Against this backdrop of a burgeoning and maturing market in Intelligent Automation what could be shifts in the provider landscape that could conceivably disrupt or accelerate the market? Four scenarios jump to mind.Read More

Meet the HfS team in Bangalore next month for NASSCOM BPM Strategy Summit!

HfS is sending a superstar analyst team to Bangalore next month for the 2016 BPM Strategy SummitRead More