- Search

Month: June 2013

Welcome to the Six Tenets of Sourcing 2.0 – where a “lights on” approach might just get you fired

Big and clunky is ugly, lean and scalable is the new corporate sexy.Read More

Replay of “Outsourcing is DEAD! Long Live Outsourcing…”

Click here for the replay & Click here for the slides. Enjoy!Read More

Our hearts are with you Nelson

Has anyone inspired the world more in the last half a century than Nelson Mandela? Peace be with you during this time old friend...Read More

It needn’t be marketing hell, with EXL

One example of an Indian-centric provider which is setting the standard for many others to follow is up-and-coming BPO provider EXL, which has not only invested heavily in local delivery resources, but has also put significant resources into developing its corporate, sales and marketing leadership in the United States. Read More

Just incase you missed all those riveting Visa Reform webinars…

Missed yesterday's record-breaking webinar on the proposed Visa Reform? Or, were you one of the 870 registrants who enjoyed the discussion so much, that you've come back for more? Either way, we have what you're looking for...Read More

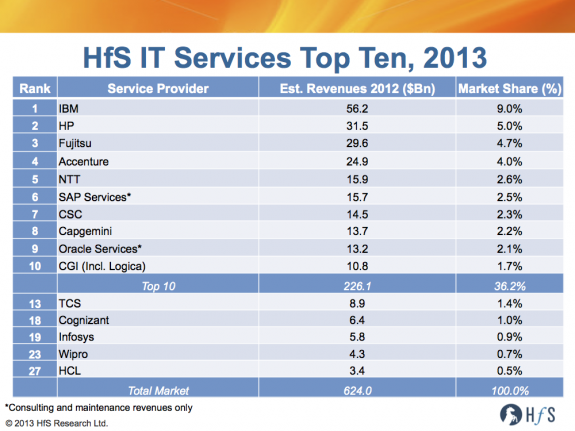

Why the Indian W-I-T-C-H providers have yet to break the IT Services Top Ten

It would be easy to forgive anyone for assuming that the Indian services majors Wipro, Infosys, TCS, Cognizant and HCL (aka the "WITCH" providers) are dominating the global battle for services supremacy, given the hype that surrounds India’s dynamic IT outsourcing economy. However, In spite of their impressive growth over the past ten years, none of the WITCH providers have yet to make the HfS Top 10 of global IT services firms, despite dominating the application development and management businesRead More

HP and CSC beware: Dell is quietly becoming a major threat to the traditional IT services providers

It is my personal belief that the likes of HP and CSC will be sweating from the oncoming threat from the Austin-based firm's $8.5 billion services arm in the not-too-distant future, not to mention some of the flagging Indian firms struggling to rediscover their mojoes.Read More