Knowing full and well that predictions can bite you on the arse isn’t going to stop us making them! Particularly when the financial reports pour in from some of the biggest movers and shakers in the services industry confirm what we are thinking.

What do we know now?

Unlike the Trump-esque games of ‘I told you so’, we’re not going to pass off something everyone knows already as a prediction (and then immediately congratulate ourselves on doing such a good job at getting a prediction bang on the money).

First up, we need to talk about what we already know; most of the big providers have already posted their results and they make for interesting – and upbeat – reading.

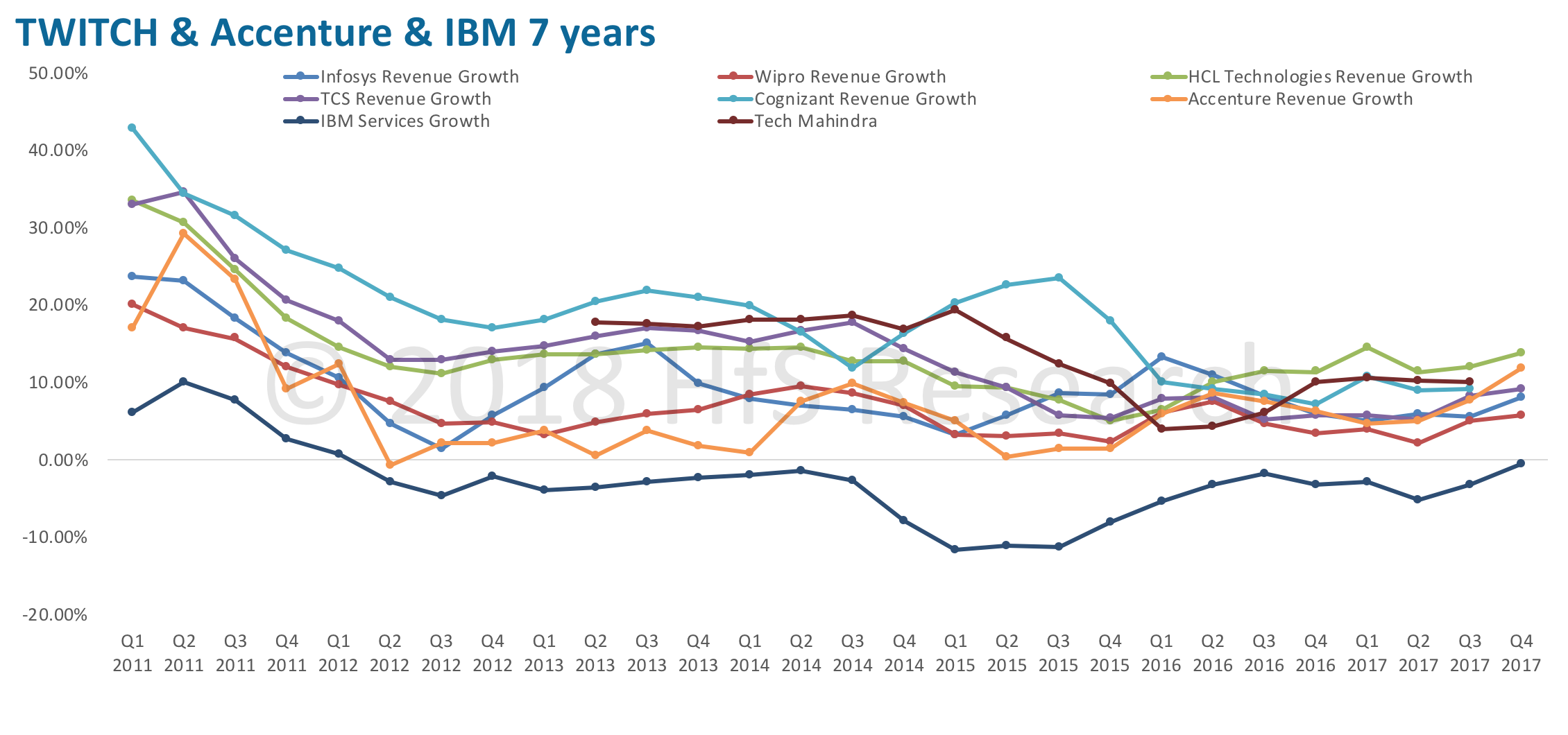

Let’s start by taking the TWITCH providers (Tech Mahindra, Wipro, Infosys, TCS, Cognizant, and HCL). By now, all of these providers, barring Cognizant and Tech Mahindra, have submitted their financial reports for Q4 2017. This gives us a decent picture of the state of the market in general—a topic tackled in greater detail in our latest 2018 market primer—but, suffice it to say, we are starting to look at the IT services market more optimistically – for the first time in years. Our expectations that all of the major providers would report reasonable growth figures have largely been met, a sure sign of the market finally reaching the tipping point. In short, we’re leaving behind much of the turmoil-ridden restructuring of the market from traditional and legacy services to the as-a-service and digital models enterprises now consume with increasingly insatiable appetites.

TWITCH is the winner?

Even so, there are winners and losers, and the pick up in market growth is not shared equally. Wipro, for example, is bucking the trend somewhat by reporting weaker growth than its contemporaries. Similarly, TCS is pushing a more consistent growth line, but the increase of a few percentage points doesn’t quite match the considerable spike other providers are seeing.

HCL’s continued growth has come as somewhat of a surprise to us. While the firm has a strong track-record as an IT services major, there were expectations that the emergence of increased digital uptake would leave the firm struggling to mirror its rivals. Central to this thinking is the fact that the firm has acquired digital capabilities less voraciously than some of its peers, and many of the larger acquisitions, such as Volvo IT, are now mature enough that we would not expect to see them contribute enormously to revenue growth. However, HCL’s continued growth—it is currently the fastest growing TWITCH provider—tells us several things about the firm. First, HCL clearly has the ability to grow digital capabilities organically to help pivot its products and services to meet new demand. Second, it has the leadership talent to keep the ship steady, even when dynamic market forces are making a significant impact, for better or for worse. In addition, HCL has smartly balanced its organic digital investments by focusing on reliable traditional market segments, such as its partnership supporting IBM Tivoli customers, which clearly has many years of profitable revenue to enjoy.

Infosys, too, reported a strong performance as 2017 closed, signalling the firm’s recently acquired ability to negotiate leadership crises with imperviousness. Expectations for the firm’s growth were somewhat muted as analysts and commentators took on a wait-and-see approach to observe if the firm’s revenue would be another casualty of the Infosys CEO sideshow. However, Infosys has continued to post solid growth, a testament to changing customer expectations (if the services are fine, who cares if the CEO changes?) and the firm’s investment in digital, its strong DNA for providing data driven support, and remodelling service delivery. The track-record of investment exemplified in both acquisitions of digital firms such as Brilliant Basics, and the upskilling and reskilling of staff, most notably the training of large chunks of service delivery teams in areas such as design thinking.

Finally, we have Cognizant, which is yet to report its Q4 2017 results. We expect no surprises, though, as the firm shows all signs of enjoying the uptake in the market with the other TWITCH providers. The firm is far from the dizzying heights of growth it became famous for in earlier years, but it continues to plug on and with recent acquisitions in analytics, digital, and design plus a strong narrative, we can expect the firm to fully enjoy the benefits of the expected tipping point from traditional to as-a-service and digital. However, the pressure is on, given the mark that Accenture has set with its 31 recent digital-esque acquisitions; expectations will be a return to double digits and anything falling short of this is bound to be a disappointment to stakeholders.

WITCH providers’ and Accenture’s revenue growth over seven years

Source: HfS Research. Click to Enlarge

Source: HfS Research. Click to Enlarge

Accenture’s enjoyed an unstoppable rise, but will digital continue to be the flavor in 2018, or is automation coming to the fore? And is this IBM’s time to seize back its throne?

Other firms are also revealing how they are handling the restructuring of the market—even IBM, which has finally arrested 22 consecutive quarters of decline in revenues, is approaching what could pass for growth. The latest financial reports from the firm place the decline in revenues as fractional as 0.6%. But the real standout provider is Accenture, which has reported revenue growth rates that actually exceed many of its TWITCH contemporaries. Given that its total revenues are double that of its nearest TWITCH rival, this is no mean feat.

If we were to categorise providers for their appetite for acquisitions and investments, then Accenture must have been famished. The firm’s list of acquisitions, particularly in digital, runs lengths longer than the combined total of major players in the space. Accenture’s reputation for delivering the goods—albeit with a premium price tag—has set the firm up to become the flagship of the digital services industry, assuming other providers remain on their current trajectory and we don’t see any furtive market leadership contest over the next few years. Conversely, IBM doubled-down on cognitive, before the market was ready, but should now find itself in a position to capitalize, with a compelling automation-AI suite of offerings coming emerging from its GBS division. Observing IBM versus Accenture over the next couple of years may boil down to a battle of two philosophies for clients: do they primarily need a services partner focused on the front end (digital), or transforming the middle-back end (automation). Having that OneOffice broad suite of skills to pull both together is where the real winning line is…

You were promised a prediction… here’s several

With all of that data at our fingertips and the recently published market primer giving us food for thought, it’s about time we started to make a few predictions about what we’ll see when all of the providers report their financial results. Foremost, it looks like we can expect to be more optimistic about the IT services market—something that IT services analysts are no doubt finding deeply unsettling. If, indeed, we are witnessing the market hitting rock bottom as posited in a recent blog, then it appears to be bouncing back with some vigour. It’s worth noting that growth in the global economy has been unexpectedly strong, which may be the cause of the improved growth rates. However, the growth seems more decided and uniform, which leads us to expect consistent positive results due to broader market restructuring rather than a macroeconomic fuelled one-off.

Here’s the clincher, though. While the spoils of increased market growth is being shared somewhat ubiquitously at the moment, it’s unlikely to lead to a utopian future, where all providers are winners. The best way to predict which providers will perform well in the new digital race and which will false-start is to take a look at the engine. While many providers have the capabilities and capacity to profit from the changing market initially, many don’t yet have the brake horsepower to gain enough momentum. Fewer still have the fuel needed to keep performance consistent and long-lasting.

So, here’s the next prediction: While we can be optimistic about the market generally, in the digital race not everyone will make it to the podium. Outside of the major providers we discussed earlier are a plethora of other IT service providers, some of which are set to outpace even the most entrenched and well-funded of the old guard. Beside these disruptors are the firms reluctant to make the jump to new delivery models, sticking to the safe harbours of legacy and tradition. These may be the first casualties that come sputtering to a halt well before sight of the checked flag. The upshot is, although things look rosy now, the change required to succeed in the new market is likely to be a step too far for many. Expect a frantic and bitter melee to ensue as legacy providers fight for relevancy in the new services landscape.

And, as a final prediction: Because these things are often best in threes and there hasn’t really been a strong prediction that we can really hang our hat on, we’re going to go out on a limb here and say 2018 might be the year we see IBM Services report actual revenue growth. There. We said it.

Bottom Line: Those providers that are investing during these transitional times will be the winners

While the biggest providers in the IT services space are validating a more optimistic market outlook, the picture is far from Utopian and while the first signs of the market finally reaching the tipping point marks the start of a positive decline for some providers, for others it signals the start of their decline. The new wave of OneOffice is forcing providers to invest further up the consultative chain to help clients move with technology. The tech is here and it’s easy to install and support – it’s being able to help clients use it and align it with their processes and business models, which is where the new spend is being created. It’s all about digitizing the front end and aligning those customer driven processes to an automated middle and back office… and, as we discussed, most of today’s motley crew of providers have pieces of the puzzle, but not all of it. Let’s face it, most will never be great at delivering everything, so clients will need to choose partners who can bring together the pieces and deliver to the outcomes they defined.

That requires real investment in your people, intense training and education, and establishment of an innovative culture to make the shift. Legacy providers will not get there with fancy marketing and a veneer of OneOffice—they need to establish it at their core, which is incredibly painful for firms that have never had this in their DNA. So the short answer to the question posed in the title of this blog is that many providers will fail to make the leap. There will be enough legacy business for years to come to feed these firms, but many will wither away as they reach the lowest common denominator of commodity value.

Posted in : IT Outsourcing / IT Services

Very good article – sums up this phase of services superbly.

James

Phil,

Fascinating to see this balance between digital and automation as the value levers. How do you see this one playing out?

Sumit

@Sumit: Most clients with very established BPO operations are looking to add RPA in to drive out the exceptions and scale down the FTE count. Automation-led deals will dominate the business process back/middle office, with elements of ML creeping is as the tech advances. Digital is very much at the front office where clients are looking to integrate customer interfaces and create more touchless environments. Most clients will look to both, but not necessarily as part of the same strategy / provider relationship. I actually see some providers being seeing as more "back-office" automation and others as more front "office digital." At some point these two need to blend together, but not necessarily in the short term for many clients,

Phil