Anthropic just announced a $1.5 billion joint venture with Blackstone, Hellman & Friedman, and Goldman Sachs to launch an AI-native enterprise services company. Service providers still debating whether this is a threat have already lost the first round.

Anthropic just announced a $1.5 billion joint venture with Blackstone, Hellman & Friedman, and Goldman Sachs to launch an AI-native enterprise services company. Service providers still debating whether this is a threat have already lost the first round.

The entire US economy has made a giant bet on AI, and Anthropic finds itself front and center

Just think about it: Anthropic propelled its revenues from $9bn to $30bn last year and is now projected to be valued at $1 trillion for its impending IPO. This firm is on, perhaps, the most unique rapid journey in tech industry history (and that includes NVIDIA), and while its technology is rewriting the rule book for knowledge work, the skills needed to keep pace with the adoption, the hype, and the insane sums of money propping up the stock markets are in a desperate short-fall. Hence, it’s little surprise Dario and co do not have the patience and confidence to bet all their chips on the traditional service providers to take them to the promised land.

I’ve been saying for a while that the real threat from Anthropic wasn’t whether they’d build a services arm. It was what happens when a model provider moves just far enough into execution to start shaping how the work actually gets done. Now we have our answer, and it came faster and with more firepower than most people expected.

What this confirms is the struggle many enterprises are having to move past pilots into full agentic deployments, and Anthropic desperately needs to drive execution itself with AI engineers, AI orchestrators, and deep data engineering skills. They clearly do not have the patience to deploy this 100% through SI partnerships. In addition, Anthropic wants access to PE portfolio companies that are some of the most aggressive adopters of AI technology, as it drives immediate value creation.

This is much more than a services play. It is a move to own the execution layer in enterprises

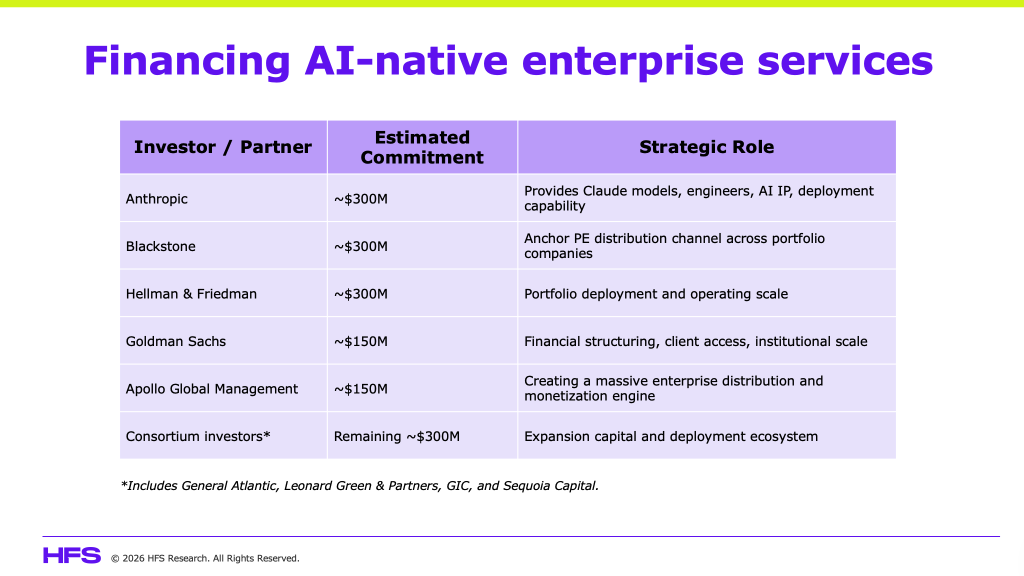

The new venture, backed by approximately $1.5 billion in committed capital and drawing additional support from General Atlantic, Apollo, Sequoia, and Singapore’s sovereign wealth fund GIC, is designed to embed Anthropic’s engineers and models directly into the core operations of mid-size businesses.

Anthropic has positioned this as additive to its existing service provider partnerships, and at the large-enterprise tier it largely is. But the real shift is the delivery model itself to being forward-deployed, model-lab-led, outcome-committed. That becomes the new reference point for services value, not just for Anthropic engagements, but for every provider engagement that follows. This is why the threat is so widely misunderstood. This is not a services land grab, but a play to own the execution layer before service providers understand what they are about to lose.

Anthropic takes inspiration from Palantir, but the ambition runs much deeper

The structure mirrors Palantir’s forward-deployment model, combining implementation capability with ownership of the underlying model in a single entity, which immediately undercuts the traditional consultant’s proposition of independent trusted advice. But no tech vendor willingly runs a labor-intensive services business at scale. Services margins are structurally inferior to software, and every operator in this industry knows it. The fact that Palantir had to build this model, and that Anthropic and OpenAI are now constructing the same thing with billions in committed capital behind them, tells you something fundamental: the current services model is not fit for proving agentic AI value in the enterprise. They are not entering services to compete with providers. They are entering services to replace the need for how services are currently delivered. And critically, they are building the channel they could not rent.

Stop telling yourself this is just a mid-market play. The playbook written there becomes the enterprise standard

Every service provider leadership team that reads this and tells itself this is a contained mid-market experiment is asking the wrong question. The threat was never whether Anthropic builds a consulting practice. The threat is what happens when the model stops being an ingredient and becomes the architecture. When Anthropic defines agent behavior, sets guardrails, determines task decomposition, and establishes execution patterns at scale, it is no longer supplying capability. It is defining how work gets done. That creates a platform dynamic, and platform dynamics concentrate value at the control layer while commoditizing everything else. This is the scenario service providers should fear most: not that they lose deals, but that they lose relevance in how value is defined. They risk being pushed down the stack into execution capacity while the model provider owns the orchestration layer, the IP, and ultimately the client relationship. HFS research already shows fewer than 10% of enterprises have scaled agentic AI beyond pilots. The mid-market is where that logjam breaks first, and once those delivery patterns are proven there, they become the benchmark for what good looks like everywhere else. That benchmark will not be built on effort. It will be built on outcomes.

This is not channel conflict. It is revenue compression arriving faster than incumbents can reinvent themselves

Calling this channel conflict misses the point entirely. This is a structural reset of the services value equation. When Anthropic delivers outcome-committed work with its own engineers embedded in execution, the expectation of value shifts for the entire market, not just for Anthropic engagements. Traditional services lines, particularly application development and maintenance, testing, support, and large-scale integration, begin to compress rapidly once that expectation takes hold. We are already seeing early evidence of 30 to 40% effort compression in certain workflows, and over the next several years, this translates into low-to-mid single-digit annual revenue deflation across commoditized services segments, with far steeper pressure in specific pockets. The market is not shrinking. But the labor-driven revenue pools are, and they are shrinking faster than most incumbents can reinvent themselves. Blackstone President Jon Gray described this as a shortage of engineers capable of implementing AI at speed, but that was not a talent statement. It was a power statement and tells you exactly who is repositioning to own execution, and once execution shifts, value ownership follows.

Targeted capability bets will beat scale every time in a disruption play

The joint venture structure reveals Anthropic’s strategy with unusual clarity. They are not acquiring large service providers because doing so would import the very inertia and structural complexity they are trying to disrupt. Instead, they will scale through targeted hires, forward-deployed engineers, and boutique acquisitions with domain expertise and workflow IP, which is a faster and cleaner way to build execution capability without inheriting legacy delivery baggage. OpenAI is already moving in the same direction with TPG and Bain Capital. That convergence should remove any remaining doubt about where this market is heading and how quickly the window for incumbents to respond is closing.

Bottom line: The services pie is expanding but ownership is being rewritten, and waiting is not a strategy

This is not about Anthropic doing services for the sake of services. It is about redefining what value in services actually is. Services-as-Software is expanding the total opportunity, but ownership of that opportunity is shifting toward those who control the models, the orchestration, and the execution patterns. Service providers that evolve into outcome-driven, agentic, forward-deployed operators will find themselves on the right side of that shift. Those that do not will not disappear overnight, but they will be steadily, irreversibly pushed out of the value layer that matters. The winners will own trust, integration, and accountability in complex enterprise environments. The losers will keep selling effort in a world that has stopped paying for it.

Posted in : Agentic AI, AGI, Anthropic, Artificial Intelligence, Automation, ChatGPT, Claude, Consulting, Digital OneOffice, GenAI, Generative Enterprise, OpenAI