- Search

Month: October 2015

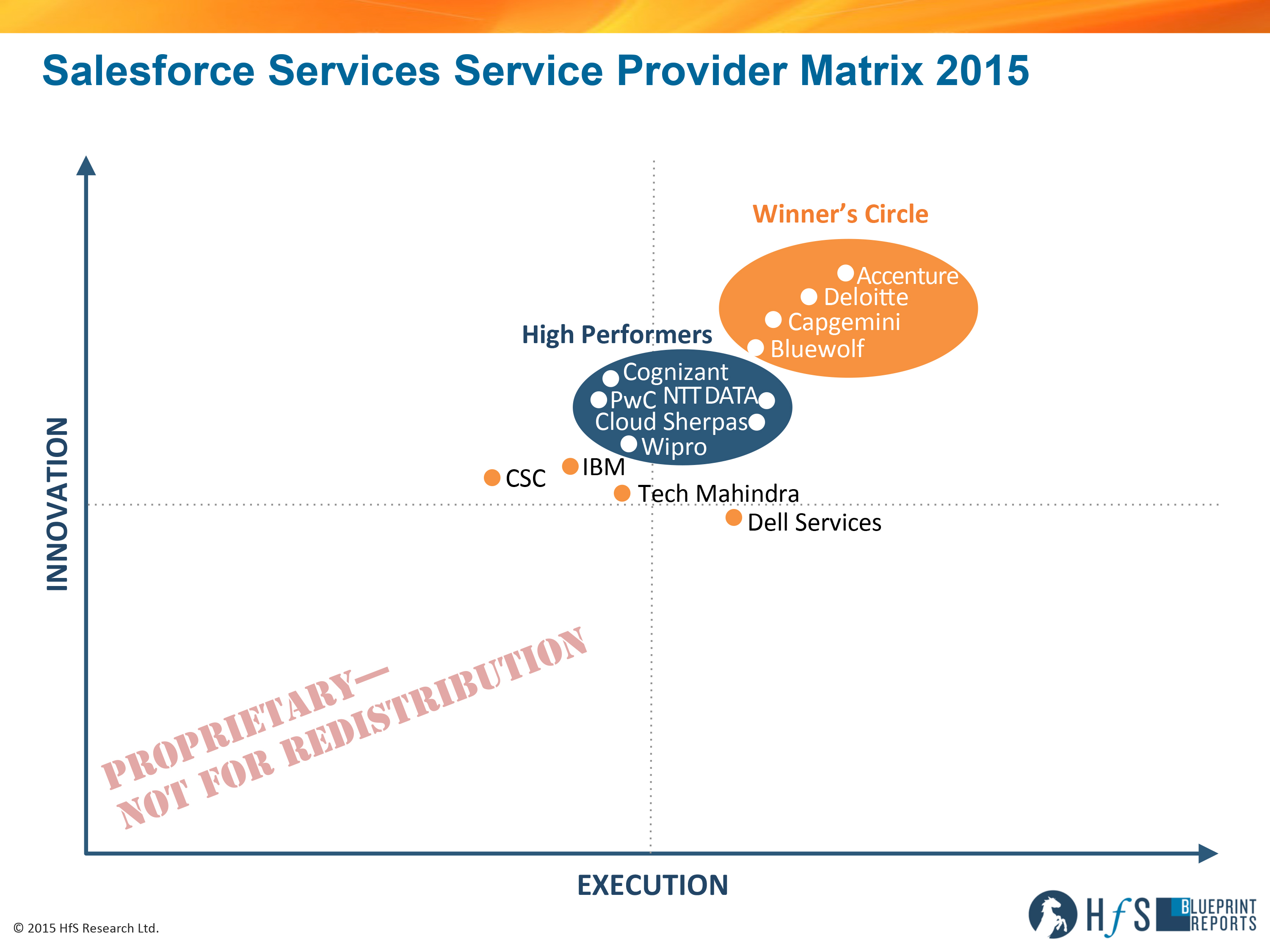

Accenture, Deloitte, Capgemini and Bluewolf lead the industry’s first Salesforce Services Blueprint

HfS Research unveils the industry's first Salesforce.com Services Blueprint analysisRead More

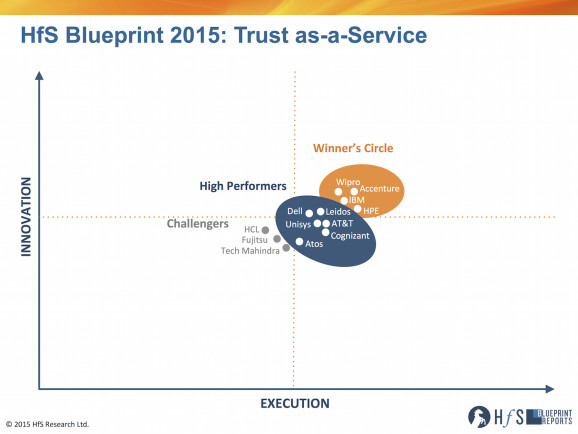

Provider, provider on the wall, who’s delivering Trust for Digital?

HfS unveils the first Trust-as-a-Service Blueprint Report assessing service provider capability in the Digital Security RealmRead More

Meet General Gary

Phil fersht talks to KPMG's Gary Novak and what he's learned being in China the last few yearsRead More

Cannibalize or face extinction (if you want to survive in the As-a-Service Economy)

Most service providers are not structured for success..... and the problem lies at the topRead More

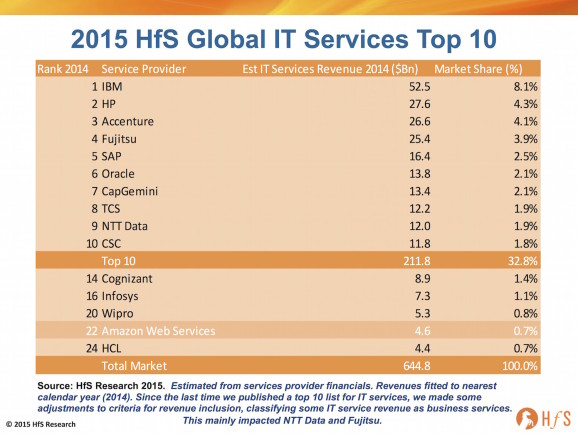

The 2015 HfS Global IT Services Top Ten. Here it is.

While the Indian-heritage providers continue to surge, here cometh AmazonRead More

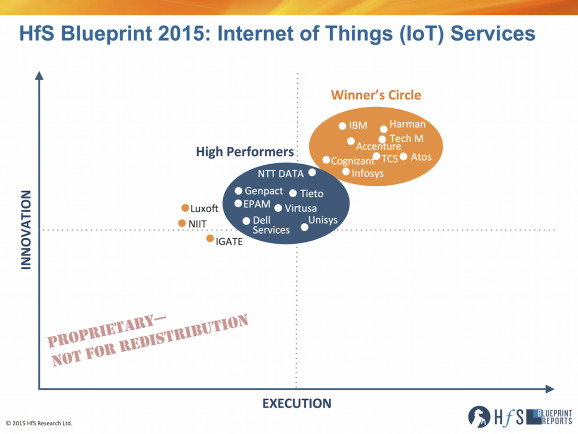

Harman, Tech Mahindra, IBM, Accenture and Atos leading the Internet of Things phenomenon

HfS Research unveils the first industry assessment of service provider performance and potential with IoTRead More

Thriving in a market that refuses to change? Then join us next month for the Analyst Relations Forum

Phil Fersht will be the keynote speaker at the Analyst Relations Forum, London November 5thRead More