A couple of months ago we wrote about meaningless data – the seemingly endless spew of pointless information that just starts to grate. Recently, we’ve started to see another related category of pointless crap – which is probably going to become more prevalent as organizations seek to increase the ease with which information is conveyed to a public that cannot be bothered to read anything anymore.

The category that is pointless crap visualization (PCV). Where an attempt is made to visualize something, often a relatively complex concept and it fails utterly to get the point across. But looks nice and gets attention because they drop some names of big vendors in there.

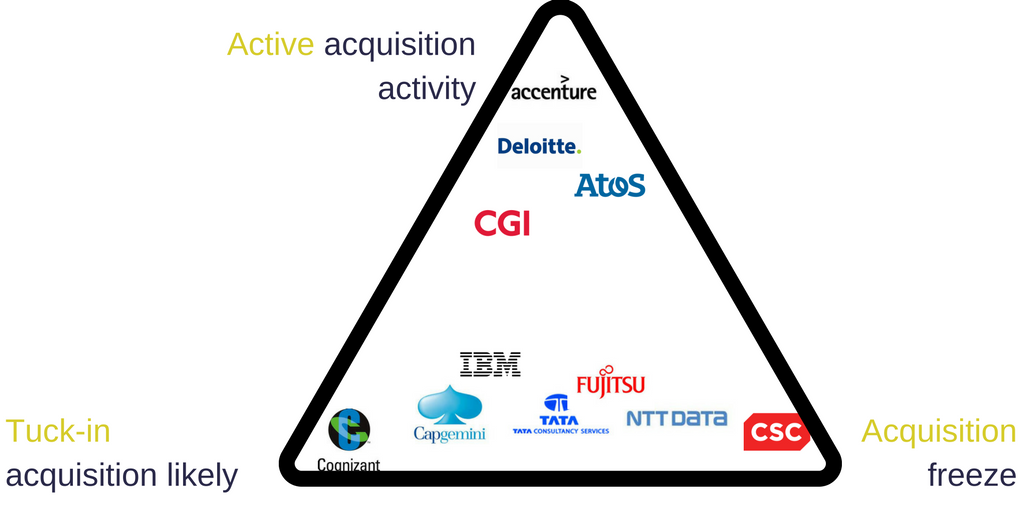

We recently noticed a thoroughly confusing diagram from one of our analyst colleagues, NelsonHall, that caused us scratch our heads in utter bewilderment:

The diagram is supposed to tell you something about the acquisition strategy of the companies in the triangle. We wrote down a couple of questions about what the chart meant, having not read the associated blog post.

It looks like Cognizant is more likely to make acquisitions than IBM? Really? Which seems highly unlikely given the huge difference between the two companies in the past – and the fact that Cognizant has a much smaller war chest for M&As, especially after its massive $2.7bn investment in Trizetto. We suppose you could limit to purely IT services – but a tuck-in acquisition is just as likely to be IP based as it is additional niche skills. Although even then we’d expect IBM to spend a great deal more – its Software group having notorious deep pockets for acquisition. Cognizant have made some significant acquisitions like Trizetto, but like all the offshore firms have been pretty gun shy when it comes to inorganic expansion compared to the big traditional technology firms.

Cognizant/TCS are more likely to acquire than NTT or Fujitsu? Mmmm… Fujitsu has been fairly quiet on the acquisition front for a few years, but you cannot count them out of the acquisition game – they made a few acquisitions in 2016 and made some very large purchases in the past. Given their cloud capabilities in Asia, it seems likely it would want to build on consulting capabilities particularly in Europe and the US. And NTT – certainly we may see a lull in activity as Dell Services gets absorbed, but NTT has been one of the most acquisitive of the services firms over the years, so this again seems slightly at odds. This seems much more likely than TCS, the least acquisitive of the already reluctant offshore providers.

The inclusion of CSC using the CSC logo… er seems a bit unnecessary. In fairness it may just be the choice of CSC as the logo – but CSC is part of HPE and no longer exists – so we do wonder how useful it is to know they won’t acquire…

Also, what is the difference between a “tuck-in acquisition” and active acquisitions? To say that IBM is not an active acquirer seems odd – again it may be a narrow view of just the IT services business, but we’re not sure that view really helps anyone considering IBM as a partner given that any software acquisitions bring IP which add to the richness of the services offerings.

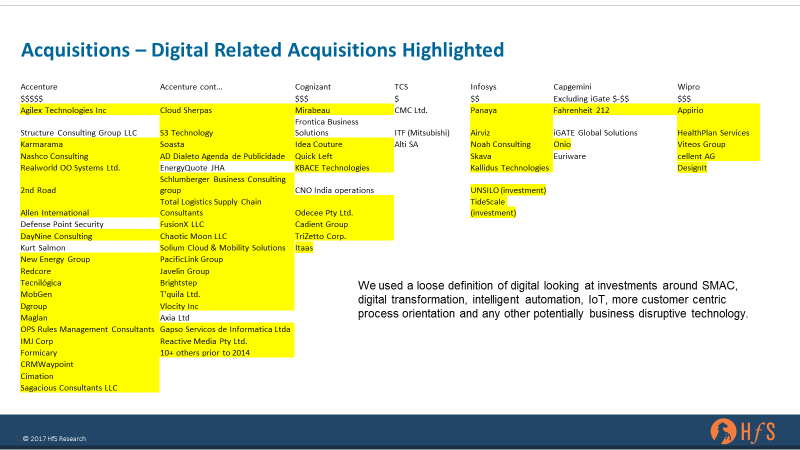

Again the distinction between active and tuck-in is not clear for Accenture – which is certainly the most acquisitive and has a very active strategy with an acquisition made seemingly every week, but some of these will be tuck-in, maybe half of them? You can judge for yourself and look at the list of Accenture acquisitions we tracked in the table below. We did some work on which providers are making digital acquisitions – not with the same list of providers, but it illustrates the scale of Accenture’s acquisition activity, compared with some of the providers on the NH diagram. So we’re not sure the visualization really captures the huge difference in acquisition trails between Accenture and the other pure services companies on the list.

It is a challenge to come up with good visualizations – that support data and summarize points being made. We have some way to go converting our list of contracts above into a statement about the different players – but I think if we do something around our acquisitions data we’ll probably convert into an index and visualize as a quadrant (oh no) or a simple bar chart. So in a way you have to applaud NH for trying something new.

To be fair the associated blog made a lot more sense – but the chart fails to reflect what is said or adds much to the understanding – it just throws names at you without any clear reasoning. What the diagram needs to do is illustrate a point or, ideally, provide a short cut to understanding. This doesn’t seem to do either. Frankly, it just obscured any of the valid points being made.

The Bottom Line – in this era of fake news and poor information, analysts have more responsibility than ever to reflect reality

This year HfS is making a clear commitment to visualizing our information better and trying to make our perspective in as clear and concise a way as possible. Like the above chart we may not always get it right – but hopefully, that is where our community comes into play and you will let us know what we get right and what we get wrong.

Posted in : Confusing Outsourcing Information, IT Outsourcing / IT Services

For those of us that know M&A approaches, "tuck ins" are one of four M&A integration strategies it isn’t a dimension.

And what would happen if they plottted someone in the dead middle?

*befuddled*

Yeah – I probably wouldn’t plot in the way they did.

If I was trying to do something like this maybe an arc rather than a triangle. With the depth of the arc being total value or some indication of total scale. With the position around the arc something like value per deal – this would give an idea of the type of acquirer… Although still not sure how much value would be, but at least would be more meaningful.