It is that time of the quarter again; we are about to see a whole raft of quarterly results for Q3. HfS uses the results as a barometer for market performance, and we make decisions around the market sizing and forecasting from these numbers. The Q3 figures will give us three-quarters of the year’s results, so they start to give us a good idea of what the year is shaping up to be. We have already seen some important results from the early announcers, Accenture, TCS, Infosys, IBM, Wipro and WNS providing us with an indication of what is to come and speculate about the overall results.

As we mentioned in our recent analysis of the HCL / IBM partnership, the IT market has become much more complicated. For services buyers, it has impacted their ability to choose the right solution alignment for their businesses and for service providers in selecting the optimum places to make their investments. This is exacerbated further with the emergence of new disruptive competitors, both on client and provider sides, threatening the marketplace. In the past, we tried to simplify this market disruption by characterizing it as “two tier”, with service providers either being traditional or more “As-a-Service.” The theory, over the past 2-3 years, has been that growth will be slow, or non-existent, in the traditional services markets, while we will see emerging As-a-Service markets like cloud, BPaaS, digital and intelligent automation, growing in multiple double digits. Many of the traditional providers will experience revenue declines in this period as they burn through their backlogs of legacy contracts, particularly the large multi-tower outsourcing deals they may have. With most of these contracts morphing into As-a-Service delivery models or becoming increasingly cheap as the FTEs get reduced over time.

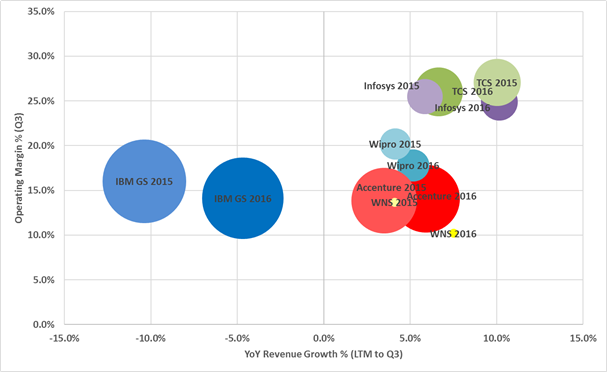

When we looked at the early announcers, at the start of the year, we predicted that the market would find renewed growth, as the market started to adopt the Ideals of As-a-Service, and growth in new business outweighing the decline of traditional spend. If you look at the performance of the early announcers in the chart, broadly this is true, with all the providers improving in revenue growth over the past four quarters, compared to the same four quarters last year. We use the twelve-month trailing data, as quarterly growth for individual companies can often fluctuate, and this gives a better direction of travel.

Bottom Line: Early signs are encouraging, but we need a consistent cadence of positive results over a sustained period

It is still early days – both with these secular changes to the market and in the results season for this quarter. However, if we see the rest of the market improve in a similar vain, we may well see growth rates improve for the IT and BPO services market, right across the board. This may be confined to more discretionary IT services markets like consulting and systems integration for the time being, and industry-specific BPO markets, such as insurance and healthcare. However, if this trend continues, we may see growth in infrastructure management spend in 2017. This is particularly significant for infrastructure as the market has been in decline for the last three years.

Over the next two months, as we digest all the results from the major IT and business services firms, we will form a viewpoint whether the market, as a whole, is seeing improvement and in what sectors. For example, whether the shift left of the offshore majors is set to continue in 2016 and beyond. We may also start to see signs that the IT and business services market might escape the low single digital purgatory it has been stuck for the last five years.

Posted in : Cloud Computing, IT Outsourcing / IT Services