Main Street is operating in a very different reality to deliver on Wall Street’s lofty AI expectations, and it’s playing havoc with the current state of IT services.

Valuations are plummeting, many heritage services firms are suddenly looking like bargain-basement buys, and services firm leaders are under unprecedented pressure to convince the investor community that their firms are still relevant in the wake of the AI onslaught.

Moreover, many enterprises, seeing this carnage unfold, are greedily demanding increasingly cheaper rates from their services partners, citing AI as the new lever to deliver the same for even less, despite having little clue how to adopt AI themselves. All of today’s services firms are in full AI obsession mode, desperately positioning themselves as AI evangelists and technology implementers, when the reality is that they need to focus on being the foundation-fixers enterprises desperately need to avoid massive AI failure.

Net-net, Wall Street will soon feel the agony of this AI balloon bursting if today’s smartest services firms are not deployed to prepare Main Street for this AI future our whole economy is gambling on. Folks, services-as-software needs to be valued as the balance between success and failure.

The Wall Street Narrative: AI will replace the IT Services Sector

On June 18, Accenture reported what most companies would consider a solid quarter. Revenue grew 6%, EPS increased 9%, margins expanded, and the company generated $3.6 billion in free cash flow. Yet none of that mattered to investors, who sent the stock down almost 18% in its worst single trading day on record.

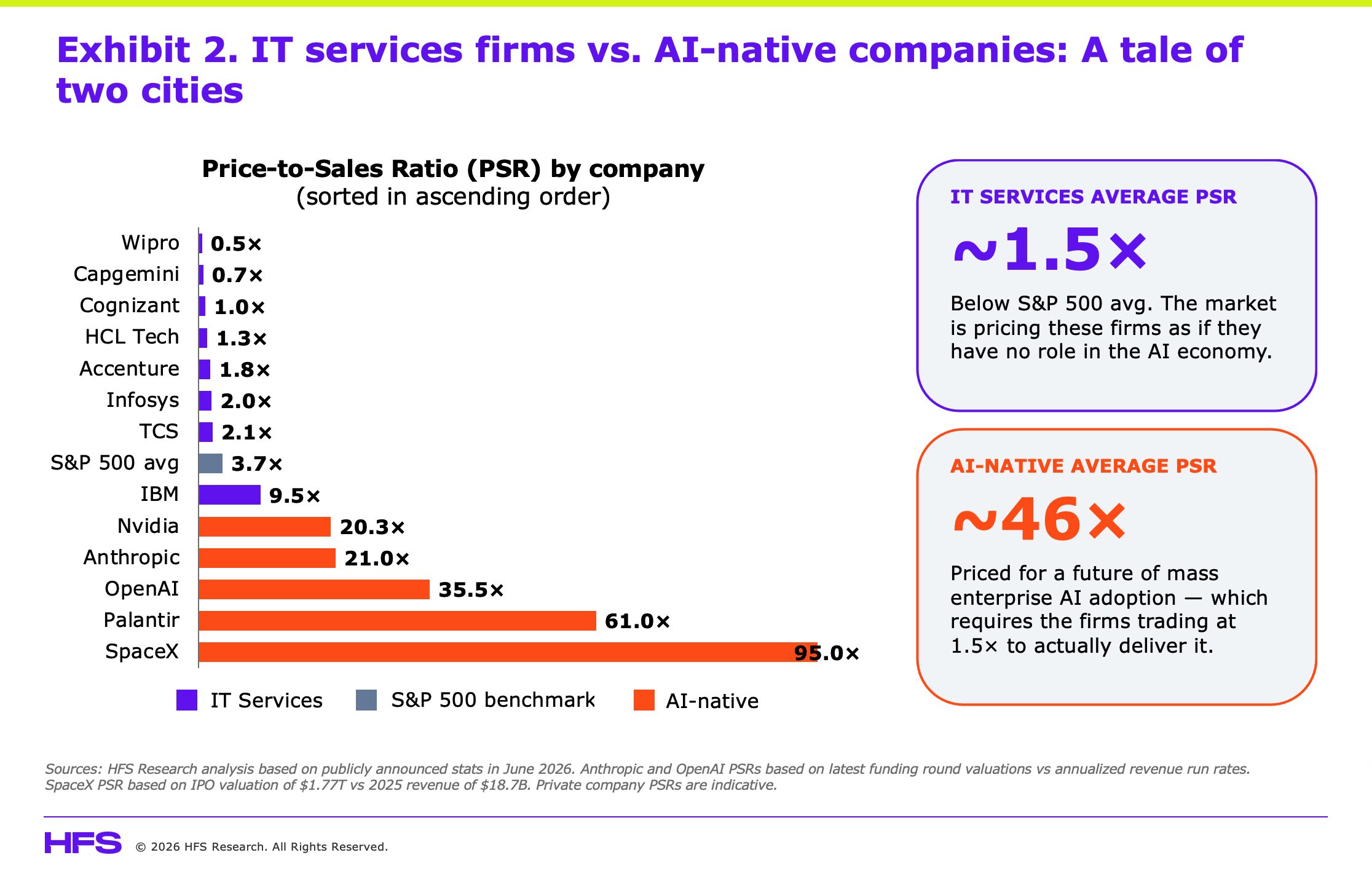

The selloff quickly spread across the sector, pulling down TCS, Infosys, Cognizant, Capgemini and every other major IT services provider. As a result, leading IT services firms now trade at roughly 1.5x revenue, while AI-native companies such as Anthropic, OpenAI, Palantir and SpaceX command valuations ranging from 20x to well over 100x revenue. Wall Street has clearly decided that IT services belong to the past while AI belongs to the future.

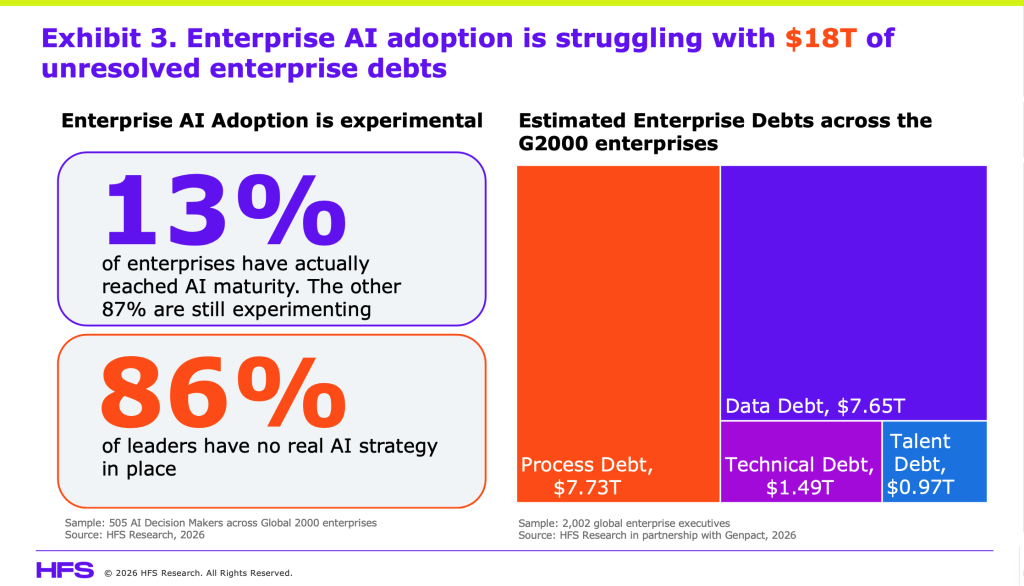

Despite all the excitement around generative AI, fewer than one in ten enterprise AI pilots make it into production because organizations remain buried under an estimated $18 trillion of accumulated technology, data, process and talent debt. Until that debt is addressed, the AI future investors are pricing into these companies simply cannot be realized at scale.

Ironically, the firms with the expertise to help enterprises overcome those barriers are the very ones the market is punishing today. That widening gap between Wall Street’s expectations and Main Street’s reality is becoming one of the defining investment stories of 2026, and unless those two worlds begin to converge, this could well be the year AI hype collides with enterprise execution.

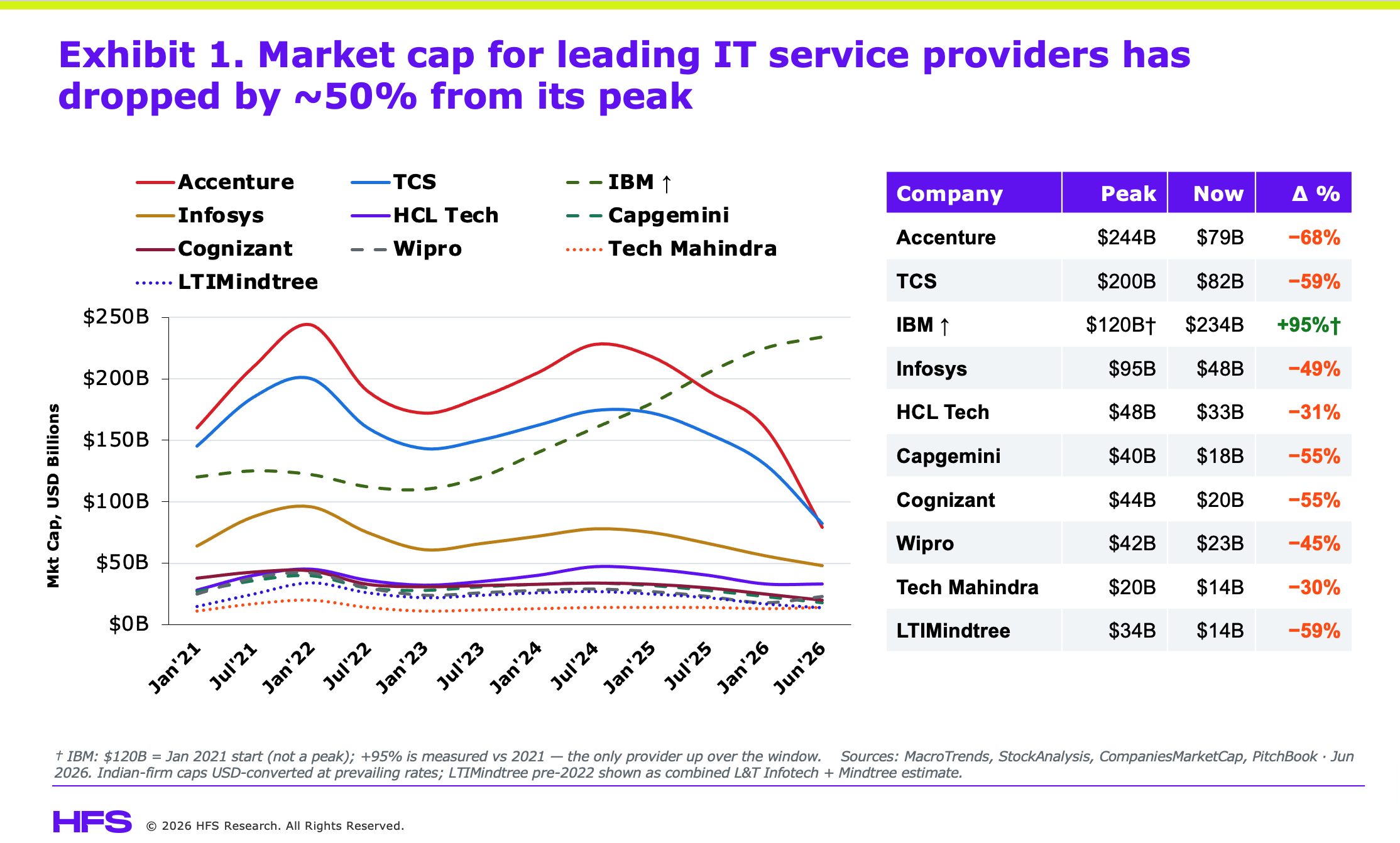

Since reaching their peak in 2021, the world’s ten largest IT services firms have collectively lost more than $600 billion in market value. That collapse wasn’t triggered by a collapse in revenue, profitability, or cash generation. Instead, it reflected Wall Street fundamentally changing its view of the sector, re-rating IT services on the belief that AI-native companies represent the future while traditional services firms have become yesterday’s story (see Exhibit 1).

One company largely escaped that fate. While the rest of the sector saw their valuations steadily compress, IBM has roughly doubled its market capitalization over the same period, not because it suddenly started growing dramatically faster than its peers, but because it successfully repositioned itself as a hybrid cloud and AI platform company whose consulting business increasingly revolves around software, automation and proprietary assets rather than people. The market wasn’t rewarding IBM for what it had delivered. It was rewarding what investors believed it could become, a software and AI business that happened to own a consulting arm rather than a consulting business trying to sell AI.

That distinction matters because Wall Street no longer values IT services firms primarily on what they earn today. It is valuing them on whether investors believe they can become something fundamentally different tomorrow.

Wall Street is pricing two completely different futures

The numbers make the disconnect even starker. The largest IT services firms now trade at an average price-to-sales ratio of around 1.5x, less than half the S&P 500 average of 3.7x. Yet these are businesses generating tens of billions of dollars in annual revenue, serving the world’s largest enterprises under multi-year contracts, growing at roughly 5% a year, and consistently delivering operating margins in the 15% to 20% range. They are highly profitable, generate significant cash, and sit at the heart of the global economy. Wall Street is valuing them as though those advantages are rapidly becoming irrelevant.

The companies on the other side of the AI divide tell a very different story. Palantir trades at roughly 60x revenue, OpenAI’s implied valuation equates to around 35x, and newly public SpaceX commands close to 95x revenue. Across the leading AI-native companies, the average price-to-sales ratio now exceeds 45x. Investors aren’t buying today’s financial performance. They are paying for a future in which AI has moved beyond experimentation, every enterprise workflow is AI-enabled, and autonomous systems have become the operating model for business itself (see Exhibit 2).

The gap between 1.5x and 45x isn’t simply a valuation spread. It reflects two completely different beliefs about where value will be created over the next decade. One assumes today’s services model is headed for structural decline. The other assumes AI will scale seamlessly across the enterprise. The question this paper explores is whether both assumptions can really be true at the same time:

The Main Street Narrative: AI Is Hard to Adopt and Even Harder to Scale

While Wall Street is pricing AI as though the enterprise transition has already happened, Main Street tells a very different story. Enterprises are enthusiastic about AI, but only 13% of Global 2000 organizations have reached any meaningful level of AI maturity, leaving the other 87% still experimenting. Even more telling, 86% of enterprise leaders admit they still lack a coherent AI strategy (see Exhibit 3).

In other words, the AI future investors are valuing at 20x, 50x, or even 100x revenue, which still exists largely in the lab for most enterprises. It hasn’t been deployed at scale, it isn’t fundamentally changing operations, and in most cases, it isn’t yet generating meaningful business value.

The technology isn’t the problem. Enterprise readiness is. Decades of accumulated debt have left organizations structurally unprepared to absorb AI at scale, and until that debt is addressed, even the most powerful models will struggle to deliver meaningful business outcomes. We see this debt falling into four distinct categories:

- Technology debt: Aging infrastructure, technical complexity, and years of underinvestment leave enterprises maintaining legacy systems instead of building new capabilities. Many core platforms simply weren’t designed to support modern AI workloads.

- Data debt: Critical information remains fragmented across disconnected systems, while weak governance, poor data quality and inconsistent ownership force employees to spend enormous amounts of time cleaning and reconciling data before AI can use it effectively.

- Process debt: Too many organizations have introduced new technology without redesigning how work gets done. Siloed processes, inconsistent governance, and manual handoffs create friction that no AI model can remove on its own.

- Talent debt: Many organizations still lack the skills, operating models, and leadership needed to embed AI into everyday work. Capability gaps, limited AI readiness, and shortages in critical roles continue to slow adoption even when the technology is available.

Taken together, these four forms of enterprise debt represent an estimated $18 trillion challenge across the Global 2000, which our deep research across more than 2000 Global 2000 enterprise leaders reveals. More importantly, they explain why AI adoption has stalled and this isn’t primarily a technology problem. It’s an implementation problem, a transformation problem, and ultimately a leadership problem:

So, Wall St, who resolves this adoption nightmare? We’ll give you a clue… it’s not the AI-native startups, the model providers or even the infrastructure hyperscalers. It is the Accentures, the TCSs, the Infosyses, the Cognizants, the Wipros and HCLs of the world. The firms that know the client’s ERP, the data architecture, the institutional processes, and the change management levers. The very same firms you’ve written off as irrelevant players from a bygone era where actual expertise mattered and humans needed humans to fashion solutions and outcomes.

The HFS Narrative: The lines between Services and Software are blurring giving rise to a new category we call Services-as-Software

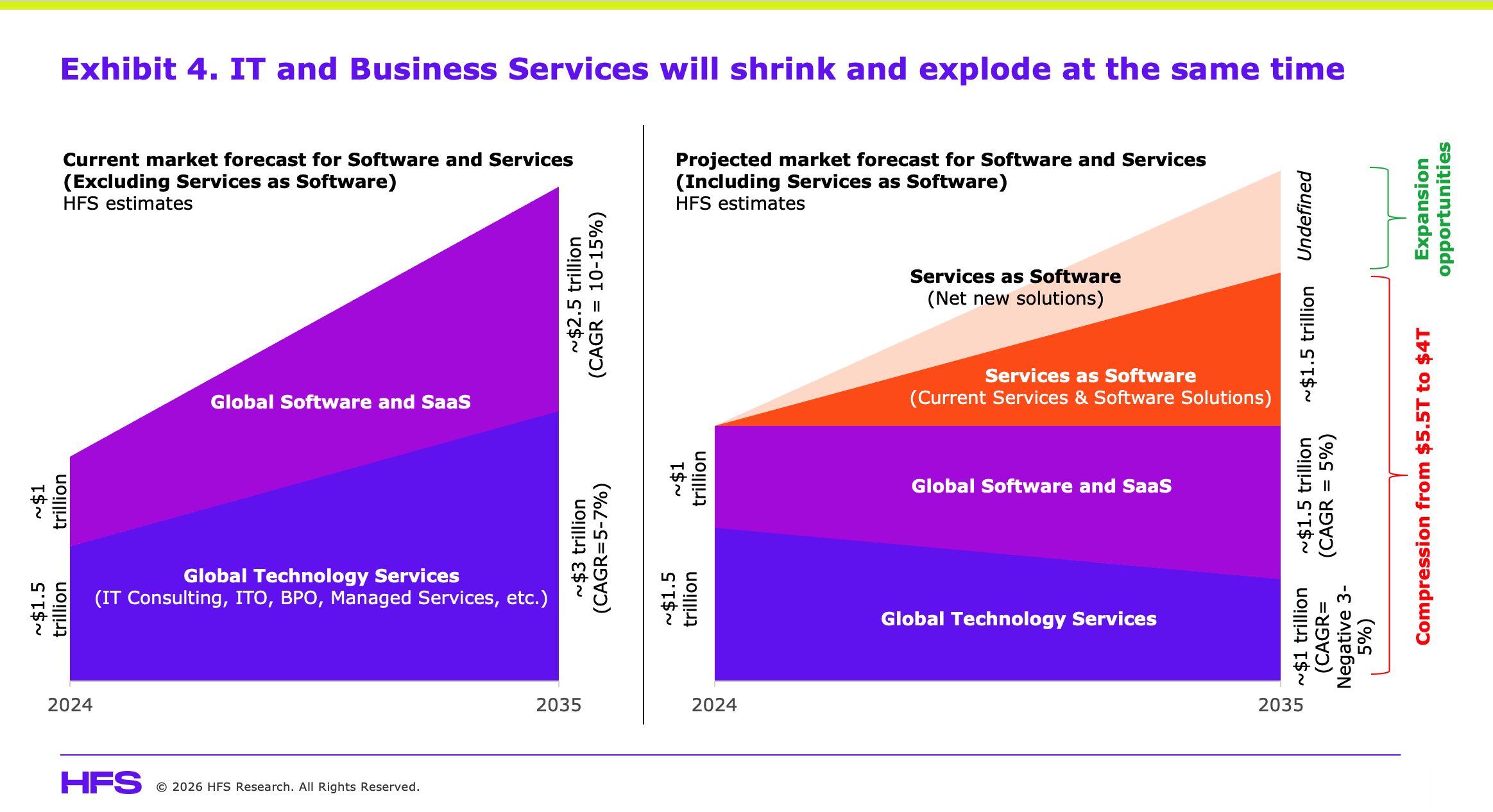

Wall Street isn’t wrong to expect disruption. More than a year ago, HFS forecast that the combined IT services and software market, which was on track to reach roughly $5.5 trillion by 2035 under the old delivery model, would instead compress to around $4 trillion as Services-as-Software fundamentally changes how enterprises consume both technology and services. That compression comes from eliminating value trapped in two legacy models at the same time, which are labor-intensive services that charge for effort and software businesses that continue to monetize static licenses rather than business outcomes.

In other words, the traditional billable-hour model will shrink, and so will the bloated SaaS licensing model that has dominated enterprise software for the past two decades. That part of Wall Street’s bear case is not only credible, but it is also already starting to play out (see Exhibit 4).

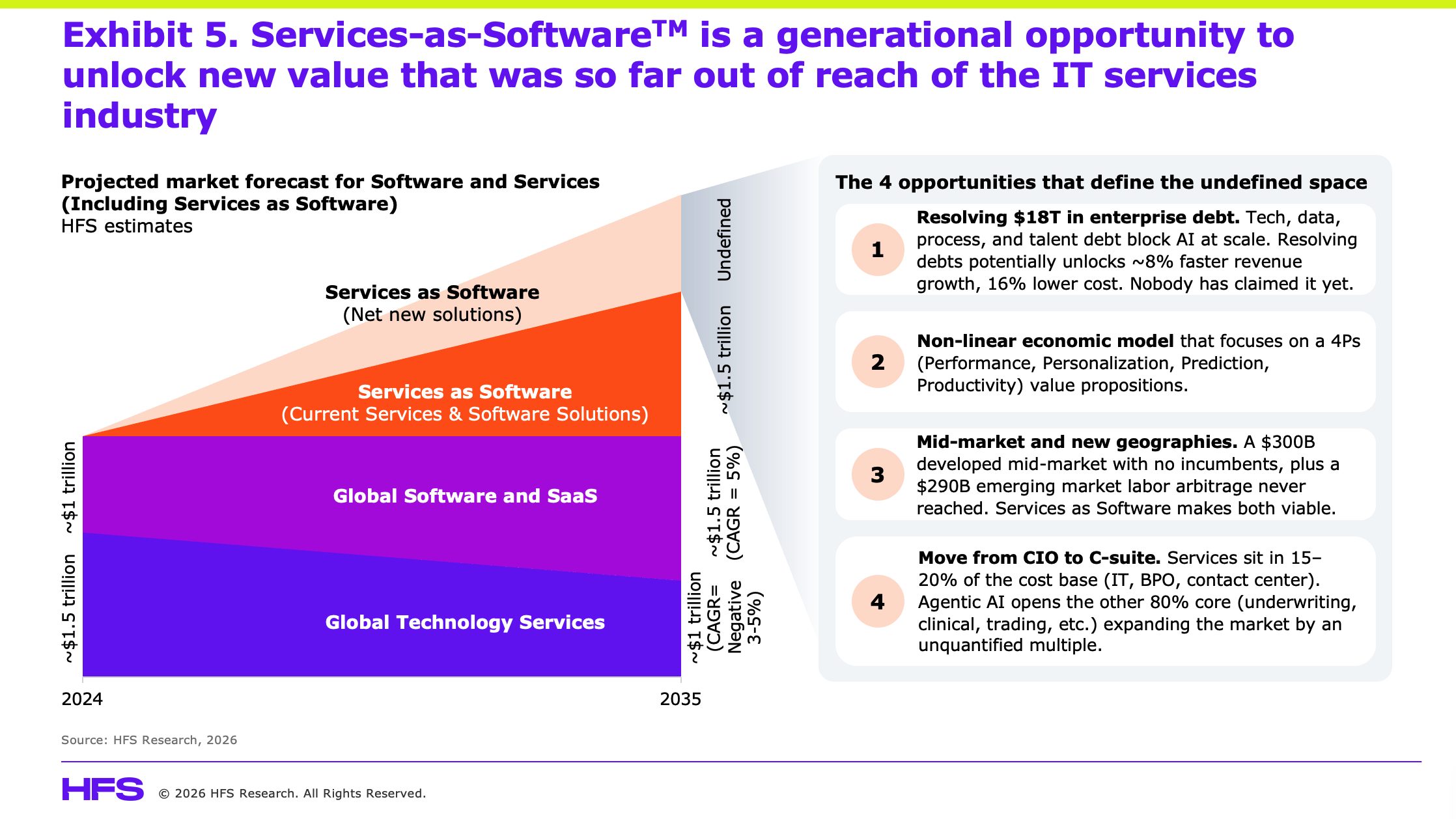

But that is only half the story. While Wall Street is focused on the value being destroyed in the traditional labor-based services model, it is largely ignoring a new triangle of value emerging above it. This is net new opportunity that the old headcount-driven model was never capable of capturing, and it falls into four distinct areas (see Exhibit 5).

- Resolving $18 trillion of enterprise debt. Technology debt, data debt, process debt and talent debt are the biggest obstacles preventing AI from scaling across the Global 2000. Traditional FTE-based delivery keeps those problems under control but rarely eliminates them. AI-native remediation changes the economics completely, allowing providers to remove debt rather than simply manage it. The firms that combine AI with deep client relationships, transformation expertise and privileged access to enterprise systems will be uniquely positioned to unlock this opportunity. For enterprises, the prize is significant, with the potential for around 8% faster revenue growth and a 16% reduction in operating costs. Remarkably, no provider has yet established a clear leadership position in this market.

- A non-linear economic model. For decades, IT services have priced effort by the hour, tying revenue directly to headcount. AI breaks that relationship because value no longer scales linearly with labor. The next generation of services will increasingly be priced around four sources of business value: Performance, Personalization, Prediction and Productivity. The providers that successfully monetize these four Ps instead of billable hours will build businesses with fundamentally different economics.

- The mid-market and emerging economies. Traditional delivery models made it uneconomic to serve companies with revenues between $100 million and $1 billion, leaving a vast addressable market largely untouched. Services-as-Software dramatically lowers the cost to serve, opening a developed-market opportunity worth roughly $300 billion across the US, Europe, Japan, South Korea and Australia. Beyond that lies an even larger opportunity across emerging markets, from regional banks in India to manufacturers in Vietnam and logistics providers in Brazil. AI agents do not require visas or large delivery centers, making markets commercially viable that labor arbitrage could never profitably reach. Together, these opportunities represent an additional addressable market approaching $290 billion.

- Expanding from the CIO to the C-suite. Most IT services firms have historically operated across only 15% to 20% of enterprise spending, concentrating on IT, business process services and customer operations. Agentic AI opens the remaining 80% by embedding intelligence directly into core business functions such as manufacturing, supply chains, underwriting, healthcare, finance and trading operations. That dramatically expands the addressable market beyond technology budgets into the heart of enterprise value creation.

The compression of the traditional market is real, but so is the expansion of the market that is replacing it. One opportunity is shrinking while another is only beginning to emerge, and the firms best positioned to capture that growth are the very ones Wall Street has decided to write off.

The Bottom-Line: AI and services need each other far more than Wall Street thinks

Wall Street has drawn a remarkably clear line between winners and losers, with AI-native companies representing the future and traditional IT services firms increasingly seen as part of the past. One side now commands price-to-sales multiples of 60x to 100x, while the other is steadily drifting towards 1x as investors bet that AI will replace the labor-intensive services model that has dominated enterprise technology for the last three decades.

The problem with that narrative is that it only works if enterprises can actually deploy AI at scale, and today they simply cannot. Until organizations resolve their technology, data, process, and talent debt, AI will remain trapped in pilots and proofs of concept rather than fundamentally changing how businesses operate, which means the AI balloon won’t burst because the models fail, but because enterprise adoption never catches up with the expectations already baked into today’s valuations.

This is precisely where Services-as-Software changes the equation, creating an entirely new category that sits between traditional services and enterprise software, blurring the distinction Wall Street still uses to justify a 60x multiple on one side and a 1x multiple on the other. Services firms are increasingly becoming software businesses, software companies are moving deeper into implementation and business transformation, and both are converging on the same outcome-based economic model, even if investors have yet to recognize it.

Ultimately, AI-native companies will have to come back to earth because their valuations depend on enterprise adoption that does not yet exist, while services firms have to convince investors they can escape the economics of selling labor and build businesses that scale through software, platforms and outcomes. Neither side gets where it wants to go without the other, and the companies that figure out how to combine AI innovation with enterprise transformation will define the next era of enterprise technology.

What should you do?

If you’re an enterprise leader…

- Treat enterprise debt as a board-level issue. Technology, data, process and talent debt are now strategic liabilities, not operational inconveniences. Measure them, prioritize them and fund their resolution with the same discipline you apply to capital investments.

- Stop celebrating pilots and start measuring business outcomes. If an AI initiative cannot demonstrate meaningful commercial impact within 90 days, question whether it deserves further investment. Every failed pilot delays the transformation you’re actually trying to achieve.

- Buy outcomes instead of effort. Whether you’re purchasing software, AI or services, the conversation should begin with business value, not licenses, tokens or full-time equivalents. If a supplier cannot explain how they improve your P&L, they are selling technology rather than transformation.

- Align your AI and services partners. The AI platform and the implementation partner are solving the same problem. If they are working independently, you will pay for the disconnect.

If you’re a services provider…

- Stop selling labor and start eliminating enterprise debt. Clients don’t need more people. They need measurable improvements in performance, productivity and business outcomes.

- Give investors a Services-as-Software story they can believe. Markets are no longer rewarding headcount growth. They are rewarding recurring platforms, proprietary IP and software-like economics. Show how your revenue mix is changing or accept that your valuation won’t.

- Take the conversation beyond the CIO. AI is no longer an IT discussion. It is an operating model discussion that belongs with the CEO, CFO and business leaders responsible for growth and profitability.

- Move aggressively into the mid-market. AI has fundamentally changed the economics of serving companies that were previously too small for global providers. This window will not remain open for long.

- Stop talking endlessly about AI and refocus on yourself as a foundation fixer with Services-as-Software. Clients already know AI matters. What they need is a partner that can fix the foundations preventing AI from delivering value. Become known for resolving enterprise debt through Services-as-Software, not for producing another AI presentation.

If you’re an AI-native company…

- Sell business outcomes, not tokens. Enterprises don’t want to buy compute. They want faster decisions, lower costs and new sources of growth. Your commercial model should reflect that.

- Get closer to implementation. A model working in a demo is very different from a model operating inside complex enterprise systems. The services firms understand those environments. Work with them rather than around them.

- Earn trust before expecting scale. Every enterprise deployment that delivers measurable value strengthens your long-term valuation far more than another funding round. Sustainable enterprise adoption will ultimately matter more than benchmark scores or headline valuations.

The future doesn’t belong exclusively to AI-native companies or to traditional services firms. It belongs to the organizations that combine the strengths of both. That is the real opportunity emerging from this market correction, and it is why Services-as-Software may prove to be the most important category the enterprise technology industry creates this decade.

Posted in : Agentic AI, AGI, AI layoffs, Artificial Intelligence, Economy