At a time where alternative facts and fake news open doors to a parallel universe, where global labor markets are being disrupted by various flavors of travel bans to the United States, the specter of a wall being built at the US-Mexico border that costs more than the entire Space-X program, a reform of H1B visas that could likely dismantle the traditional outsourcing model, and a curious thing called Brexit that could change the global trade landscape forever, one might be forgiven for feeling slightly disoriented. Yes, people, we’ve arrived at a time where the very foundations for service delivery models across the industry are being put at risk, where there is no written rule book for how to get ahead of this. So what better time than to add a sprinkle RPA into this global potpourri of disruption? Maybe a food dose of process automation will give us all something to cling onto during these heady days?

Against this slightly perturbing background, what is the state of the RPA market, the emergence of the virtual workforce – and how will it affect the broader markets? Is RPA the silver bullet to overcome many of these issues and obstacles? Back in December, we already chartered the service provider capabilities around RPA. As a result, we not only got a strong endorsement for our findings, but stakeholders were asking us to provide a similar assessment for the RPA tool providers themselves. To get more clarity on these pressing issues, we have sent our automation overlord Dr Tom Reuner back into the RPA community to separate the wheat from the chaff… the bots from the clots.

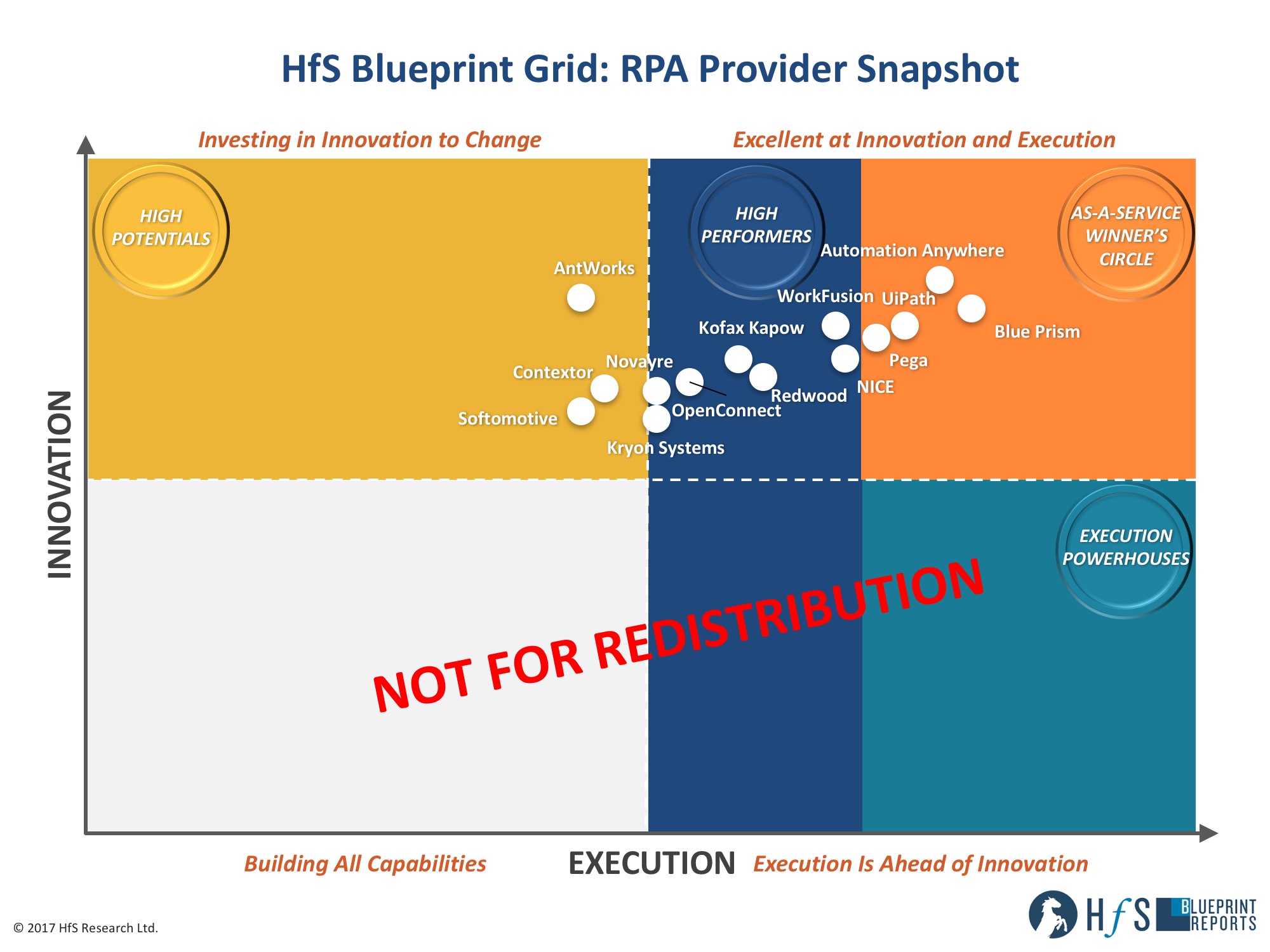

Based on his findings, Tom and I went into conclave, compared notes and war stories, as well as cranking the numbers for the evaluation. And finally, we have white smoke. Thus, we are pleased to share the new 2017 RPA Blueprint grid and the key findings with you.

Phil Fersht, CEO and Chief Analyst: Despite all the noise, many stakeholders still struggle to comprehend what RPA is all about. Tom, can you help these lost souls to get up to speed before we dive into the details?

Tom Reuner, SVP Intelligent Automation: I wish that would be so easy, Phil. Despite all the noise RPA is still an undefined market. To make matters worse, the IT juggernauts, the service providers, and management consultancies are only very gingerly educating the market. Two key reasons for that. On the one hand, it is still a nascent, albeit fast maturing market. On the other hand, it is a classic case of Innovators Dilemma: The large service providers still make more money with system integration and labor arbitrage. A cross-industry working group under the leadership of Lee Coulter and AJ Hanna from Ascension Health under the umbrella of the IEEE standards body, with the participation of the leading RPA tool providers and consultancies, is doing sterling work to drive a taxonomy and common understanding of the different building blocks of Intelligent Automation and thus also RPA. Yet, it will take considerable time until these suggested definitions will be adopted by the broader industry. The IEEE definitions of RPA are a useful reference point to describe the scope of this Blueprint evaluation: “Robotic Process Automation (autonomous)”: Preconfigured software instance that uses business rules and predefined activity choreography to complete the execution of a combination of processes, activities, transactions, and tasks in one or more unrelated software systems to deliver a result or service with human exception management.”

While nothing is defined in the context of automation, the common denominator of all the approaches to automation is decoupling routine service delivery from labor arbitrage. This is not only the common denominator but also the cause for the widespread disruption that we are expecting, largely on the supply side. But the providers are not always helping either. The biggest misconception and confusion is caused by the related proposition of desktop or Robotic Desktop Automation (RDA). It is here where there is so much smoke and mirrors in the industry. In simplistic terms, RDA has evolved from screen scraping in the front office where disparate sets of information were integrated to support call center agents. Thus, RDA is focused on quick deployments on desktop level, typically customer contact agents. In RDA, activities are being automated, while in RPA (back-office) processes are automated. On the danger of over-simplifying, in RDA the agents are passing on tasks to robots, while in RPA the robot passes on tasks to agents. And as we are on the topic of subterfuge, it is difficult to ascertain how much scripting and coding is actually needed to get solutions off the ground? Many contracts are largely a Managed Services agreement. This is confounding what automation and RPA should be all about, namely the decoupling of routine service delivery from labor arbitrage.

Phil: So, clear as mud. Against this background, what really is going on in the RPA community?

Tom: Well, yes. But I think the reason for so much smoke and mirror is that there is so much at stake. The large service providers fear an erosion of their profits, while the RPA providers have often banked their pension pots on the success of their companies. Looking at it from a more positive angle, most providers are evolving their offerings toward the notion of operational analytics and the broad bucket of cognitive. In particular, the integration of semi-structured content through Machine Learning or through partnerships with providers like Celaton or Loop AI who help to create patterns in unstructured environments.

Aligned with this maturation in the market, we see more funding coming through. The latest example is WorkFusion who raised $35m in January. However, the biggest shift in the market, underlining the increasing maturity, is the shift of mindset from RPA as a non-invasive turn-key solution that marked the early phase of market development to the notion of RPA as a conduit for transformational projects, looking at end-to-end processes rather as a short guarantor for cost takeout. And RPA as an enabler for transformational projects is the cornerstone for our evaluation of RPA providers.

Phil: So Tom, what was your methodology behind putting together the 2017 RPA Blueprint Snapshot?

Tom: Rather than taking a function and features centric evaluation that is more appropriate for software products, we are taking a market-led approach which we feel is more aligned with the need of buyers in the sourcing industry. The RPA Blueprint Snapshot is building on and expanding the discussions with stakeholders as well the research of HfS’ Intelligent Automation practice. Our Blueprints are based on multiple client interviews, interviews with advisors, service providers and internal analysts who have experience working with the RPA platforms. Our scoring system only allows for 10% of analyst judgment, where we made the case for your strong innovation. Our weightings are partially based on importance criteria we glean from our State of Industry survey with KPMG which covers over 450 major enterprises. As RPA is not yet commonly defined, we are taking a strong steer from the evolving RPA strategic partnerships of the leading system integrators and BPOs.

Against this background, and in addition to the above inputs, we have reached out to the RPA providers with an RFI set out to help us evaluate them against a set of criteria across both execution and innovation. As we have outlined above it is not an easy undertaking as there is so much smoke and mirror in the market. But given the strong endorsement for both our Intelligent Automation Blueprint and our RPA Premier League Table, we are confident that our approach is providing stakeholders with relevant information and guidance.

Phil: Not beating around the bush, who is standing out as RPA performer?

Tom: There are many ways to look at the RPA market given the caveats that we have called out. But painting with a broad brush, the companies in the Winner’s Circle – AutomationAnywhere, Blue Prism, UiPath, and Pega – are the providers of choice for the channel partners focusing on transforming back-office processes. Behind this leading group, the positioning is becoming decidedly more blurred. The best way to think about it is to be clear about the use cases and requirements to add more specific providers for tender or RFI. Be it WorkFusion for broad cognitive capabilities, NICE for front-office activities, Redwood for ERP-centric automation or OpenConnect for a focus on operational analytics. Almost below the radar, there are providers like Jidoka with core RPA capabilities who carved out a niche in the Spanish-speaking world. Similarly, Contextor who are evolving from an RDA position to broader RPA capabilities, have a strong position in the French market. Beyond a geographical focus providers like Kryon Systems or Softomotive have made significant progress evolving from attended to unattended scenarios, while KofaxKapow through acquisitions offers a broad portfolio from OCR capabilities to process analytics.

Drilling down into the specifics, the market is dominated by the “duopoly” of AutomationAnywhere and Blue Prism. AutomationAnywhere is strongest in F&A, offshore delivery centers, and the US market. Conversely, Blue Prism is leveraging the first mover advantage with strong partner relationships, having the strongest impact on industry specific services, headquartered CoEs and the UK market. Behind the two market leaders, UiPath is growing strongly as clients cite the effective partnership culture and attractive commercial terms. Thus, for mature clients, UiPath is increasingly seen as the third strategic option in multi- vendor environments next to AutomationAnywhere and Blue Prism. Adding to this mix, iPega is being credited for its the quick deployments as well as the integration of both RDA and RPA in attended or un-attended scenarios. At the same time, Pega offers broader functionality by extending bots to it BPM suite.

However, the biggest surprise in our evaluation was AntWorks that thus far have been below the radar of industry’s stakeholders. Their value proposition is about linking core RPA capabilities with machine reading including semi-structured content such as handwriting in forms as well as broader cognitive capabilities including pattern recognition, even in images. Furthermore, similar to providers like RAVN, AntWorks has Enterprise Search and Machine Learning functions to support extraction of data from legal documents. The combination of Computer Vision and pattern recognition allows AntWorks to provide one solution where many service providers have painstakingly integrated different tool sets. Even though around the broader cognitive capabilities, AntWorks is competing with IBM Watson, it goes without saying that AntWorks is still early on their journey and therefore needs to demonstrate client references to the broader market.

Phil: Despite the market being nascent, albeit maturing market, WorkFusion has announced a free RPA product. What do you think will be the impact?

Tom: When WorkFusion announced a free RPA product dubbed “RPA Express” back in December, many executives in the automation community went pale. In defiance, and sometimes confusion, executives were quick to suggest that WorkFusion does not have a “proper” enterprise grade RPA product. There are many different ways of looking at this announcement. First of all, credit where credit is due: WorkFusion has one of the best, if not the best, marketing programs in the Intelligent Automation community. And sometimes there is a hint of jealousy creeping in when we discuss WorkFusion with their peers. More pertinently to the RPA discussion, while WorkFusion might lack the enterprise-grade capabilities in core RPA that the providers in the Winners’ Circle have demonstrated, they have strong credentials in adjacent capabilities such as crowdsourcing, the integration of Machine Learning or enhancements to the RPA Object Library such as the capability to drag and drop entire processes (e.g., “KYC,” “corporate actions,” “OCR”). What is boils down to in the end is to get access to the table where the sourcing discussions and decisions on automation are being taken. WorkFusion has successfully demonstrated exactly that. Not having enterprise grade core RPA capabilities has thus far not harmed their revenue stream. Thus, the announcement might not disrupt the market, but it still might end up negatively impacting valuations of RPA providers as many look for an exit strategy.

Phil: Gazing into a crystal ball, what can we expect for 2017?

Tom: Phil, if I would have all the answers, I should probably change my job and could make a lot of money. But here are three scenarios that I am seeing for 2017:

- RPA will remain undefined. Over the next 12 months, the perception of RPA will remain blurred. RPA capabilities will fold into broad propositions such as Digital Workforces or Cognitive Automation. This is adding to the continuing confusion around RDA. Extending on that, in 18 months we won’t talk about RPA anymore. Most of the leading technology providers will have been acquired and RPA is a reality in the back-office.

- M&A through ISVs. Buyers will have to do scenario planning for acquisitions. While this might bring broader capabilities, licensing costs are likely to increase as well. Pega’s acquisition of OpenSpan is the template for such developments. Beyond the tool providers, the automation pure plays such as Symphony and GenFour are likely to be equally absorbed by larger consultancies.

- The emergence of an Automation Ecosystem: We already have seen the impact of Watson, as it is starting to evolve into an ecosystem. Suffice it to say, IBM could be the driving force to extend those capabilities, as we have argued some time ago. But it could equally be one of the tool providers significantly expanding its reach. As stated, we are seeing the providers in the Winner’s Circle moving toward the notion of orchestrating much broader automation capabilities. At the same time, we are seeing providers like Blue Prism and UiPath being deployed in IT-centric scenarios such as IT Help Desk and Application Management, pointing to a convergence of scenarios and tool sets.

HfS premium subscribers can access the RPA Blueprint Snapshot here.

Posted in : Cognitive Computing, intelligent-automation, Robotic Process Automation

A good representation of the current RPA vendors. Consistently starting to see BP, AA and UIPath out on top

Paul

Open era’s Federer, Nadal and Djokovic i.e. AA, BP and UIP

Tom, Phil – This is a fantastic look at the market place and, speaking for Pegasystems, we are delighted to be included as a leader. Your assessment of the market is most interesting; a moving target, with many ways to define and attack it. We like to look at it as another way to make the lives of our clients easier and add value for their customers. RPA can be seen as the first step to digital transformation across the enterprise and will allow enterprise to steal back both front and back time and put these resources into more meaningful activity that will make a positive impact on the bottom line. Our goal is to get ahead of the market and have a hand at shaping the accepted definition. Your research is really giving people something to think about!

Nice article, Thanks for providing this wonderful document.

Kryon Systems is catching up and being recognized by a handful of GSIs