A lot has changed in the last year… especially when it comes to automation: it has now become the broadly-accepted efficiency tool for cost leverage with operations.

Every customer has RPA project managers and automation leads hungry for data, advice, and ideas. Every service provider has RPA embedded into their service delivery models, and every credible advisor has a practice that is working with multiple clients to make this happen. The Armageddon days of talking about robots taking our jobs are over – these are now the reality days where we can see exactly what’s going on with automation and AI, and accurately estimate how it’s going to impact the services industry in the next few years.

There will be impact, but it’s manageable provided we focus on new skills and value.

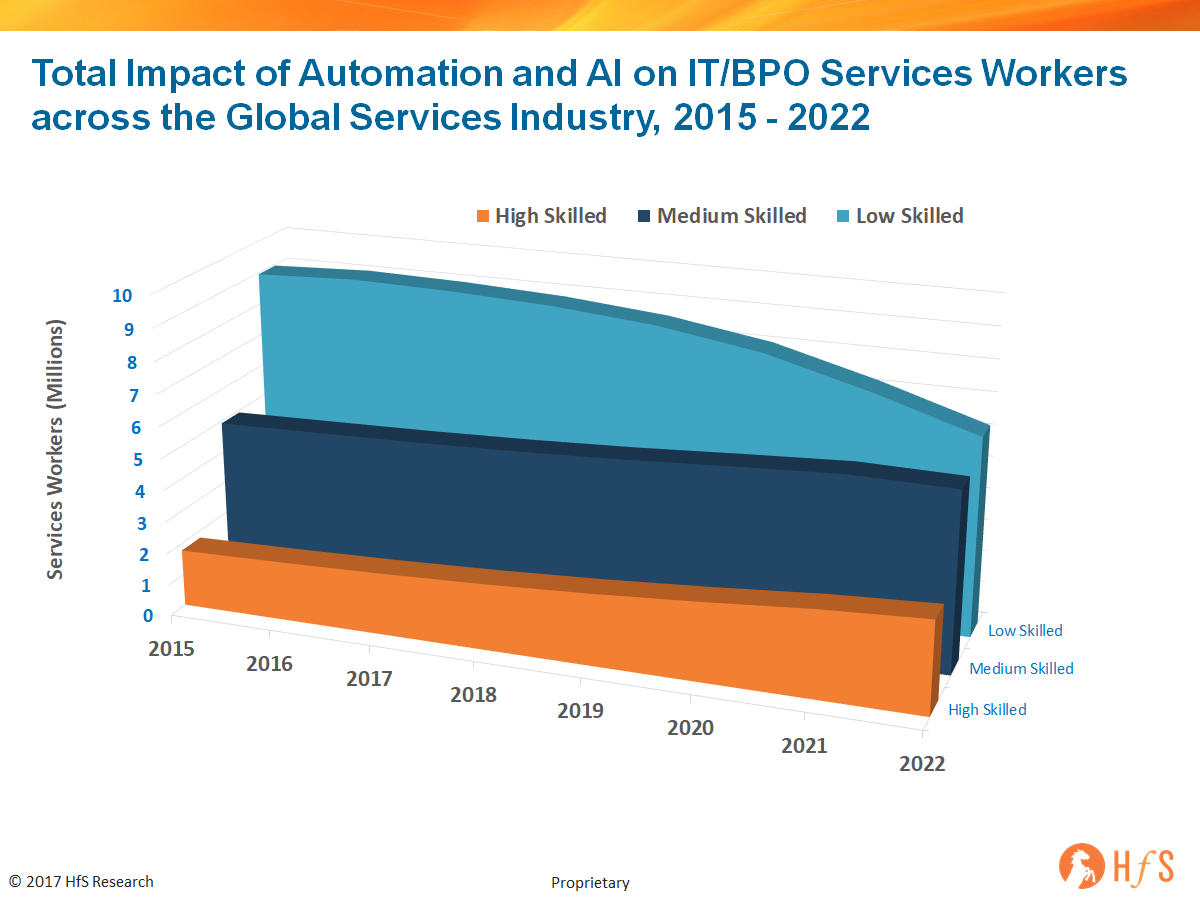

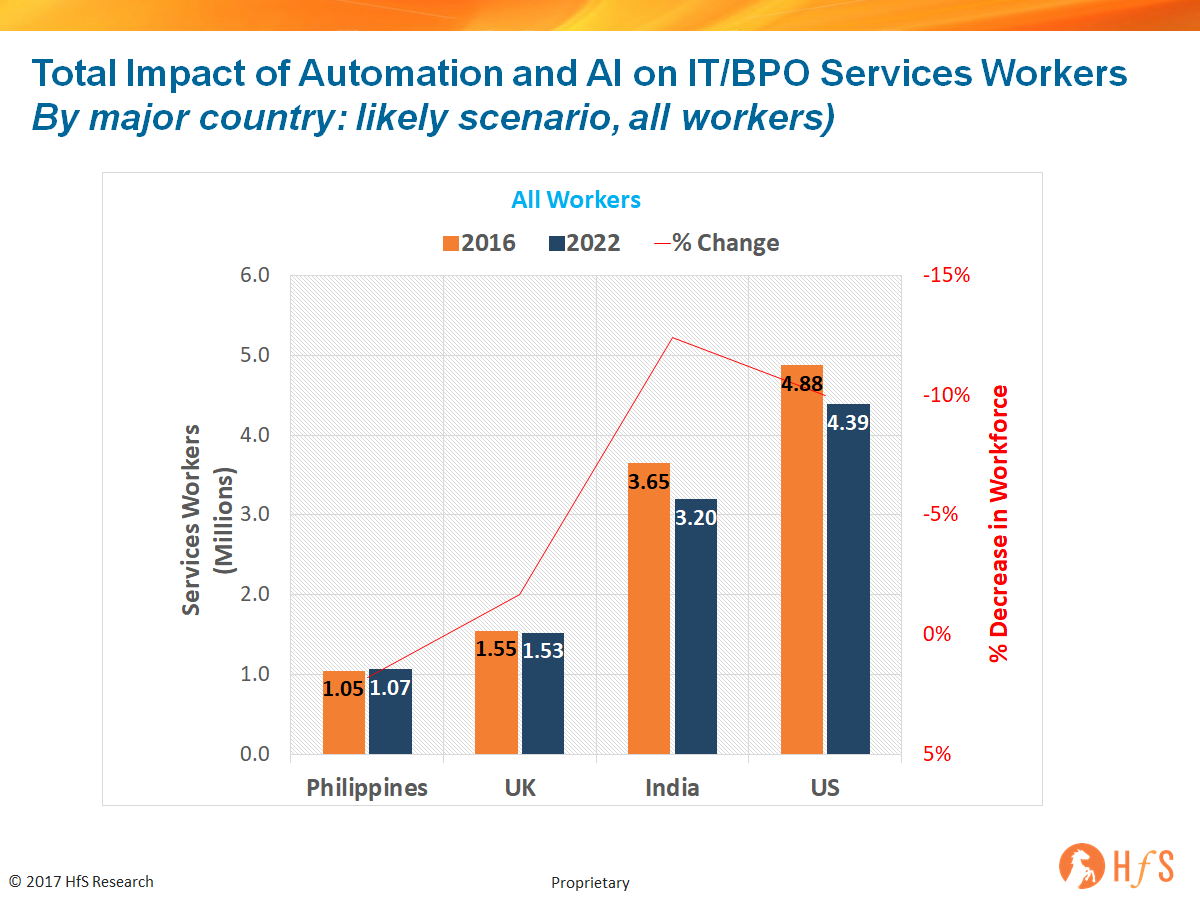

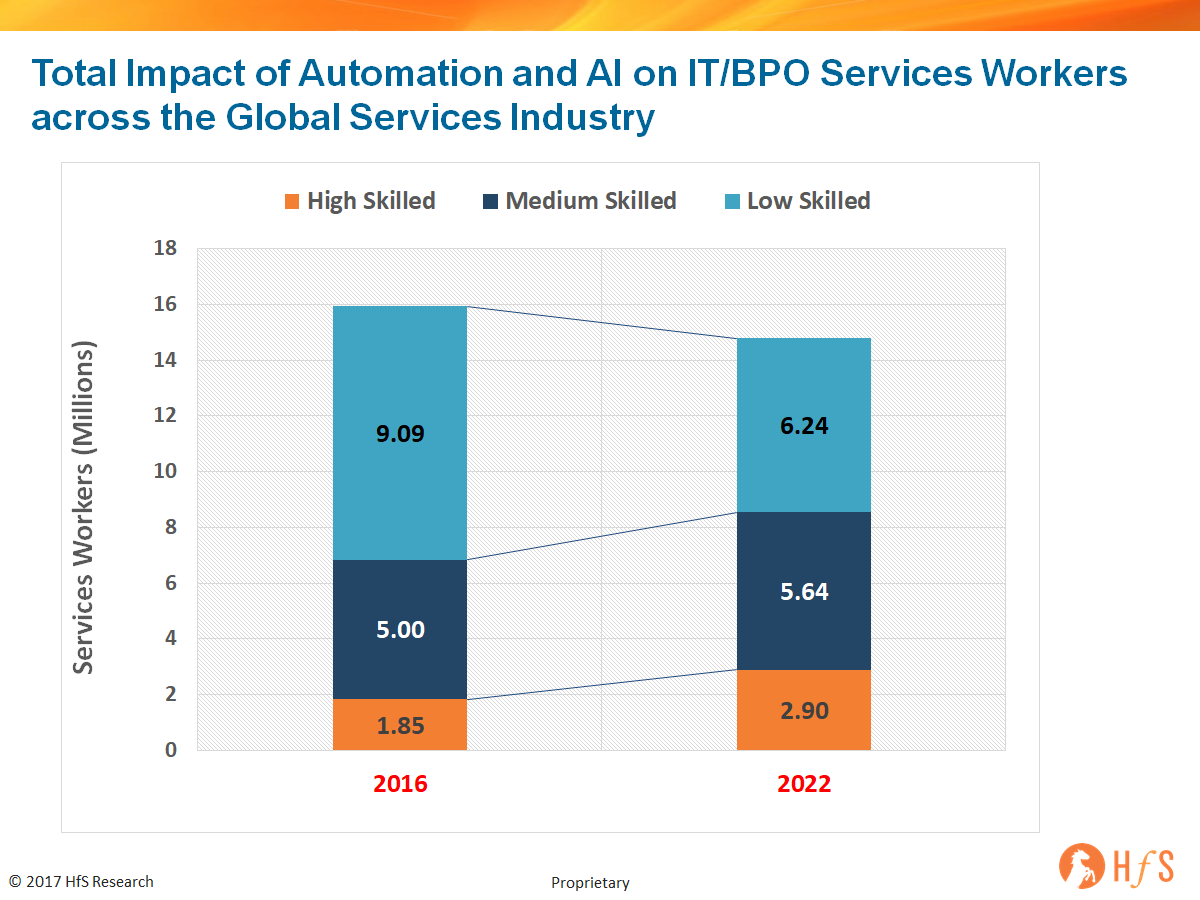

In short, the global IT and BPO services industry employs 16 million workers today. By 2022, our industry will employ 14.8 million – a likely decrease of 7.5%* in total workers (see our research methodology below). This isn’t devastating news – we’ll lose this many people through natural attrition, but what this data signifies is this industry is now delivering more for less because of advantages in automation and artificial intelligence. The new data also shows how job roles are evolving from low skilled workers conducting simple entry level, process driven tasks that require little abstract thinking or autonomy, to medium and high skilled workers undertaking more complicated tasks that require experience, expertise, abstract thinking, ability to manage machine-learning tools and autonomy.

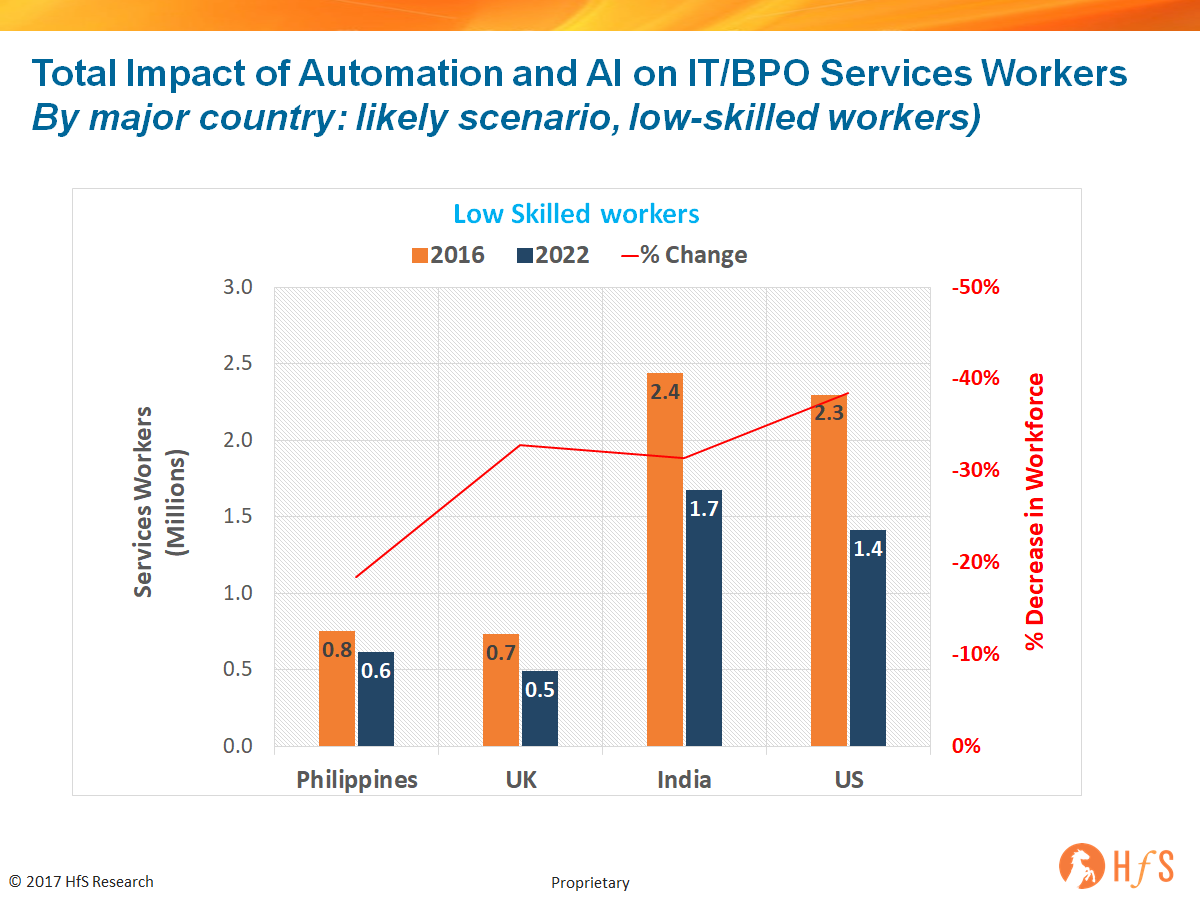

The low skill routine jobs are getting increasingly impacted, and our new demand data shows an acceleration in RPA tools (a 60% increase over the next year) where service providers are the largest adopters into their own service delivery organizations. We expect to see a more rapid impact on routine job roles which is most notable in 2022 as companies take time to build the impact of RPA into service contracts and figure out how to turn work elimination into hard savings than merely soft efficiency savings. With barely a 50% satisfaction level, this will take 4-5 years to see the real cost benefits in terms of job elimination. Most of the short-medium term benefits are being seen in increased efficiencies and more digital process workflows. All major service delivery locations are expected to be impacted at the low-end, but the higher the wage costs, the higher the expected role elimination (750,000 roles in India and a similar number in the US):

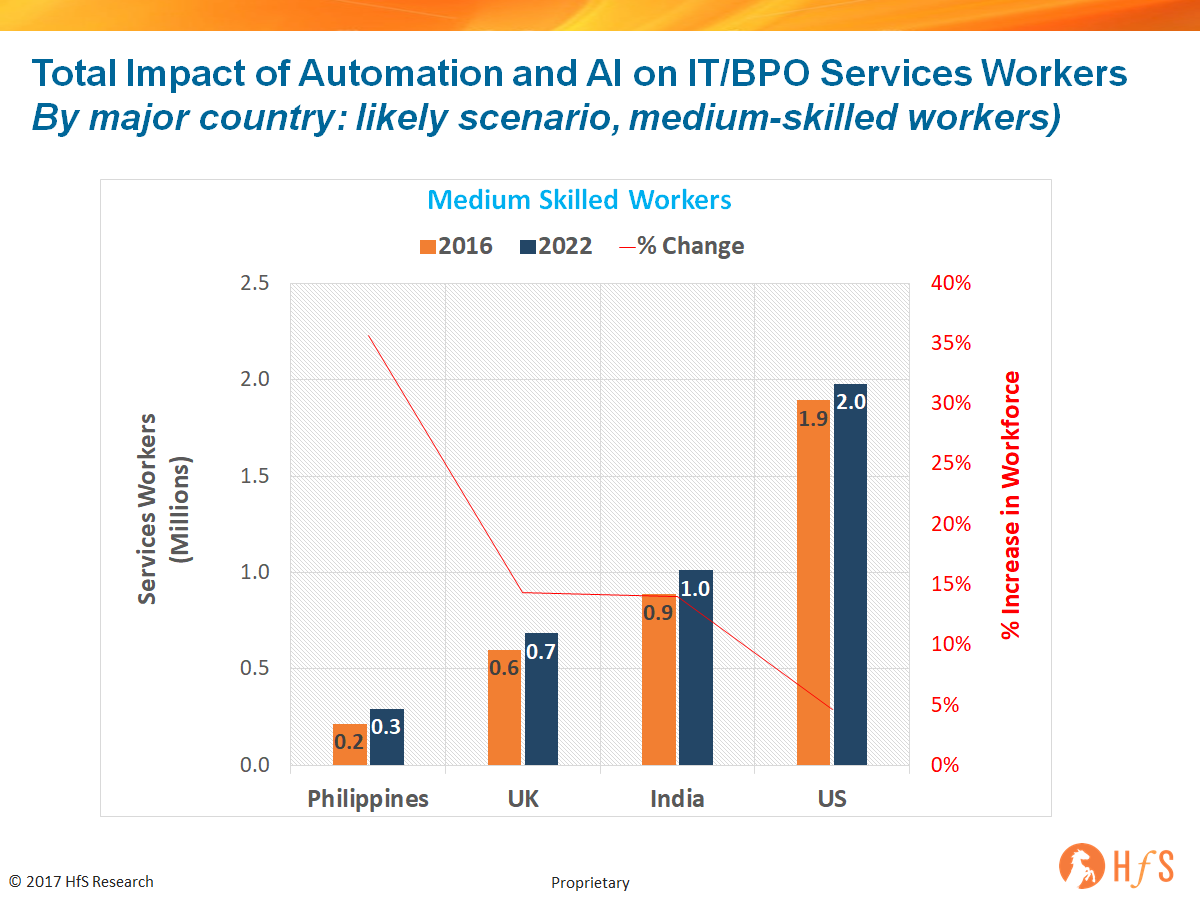

Medium skilled roles are picking up across the board, especially in roles that are customer/employee facing with the need for more customized support, the ability to handle basic customer and data queries, and more customized service work with virtual agent models in 2nd / 3rd tier escalations:

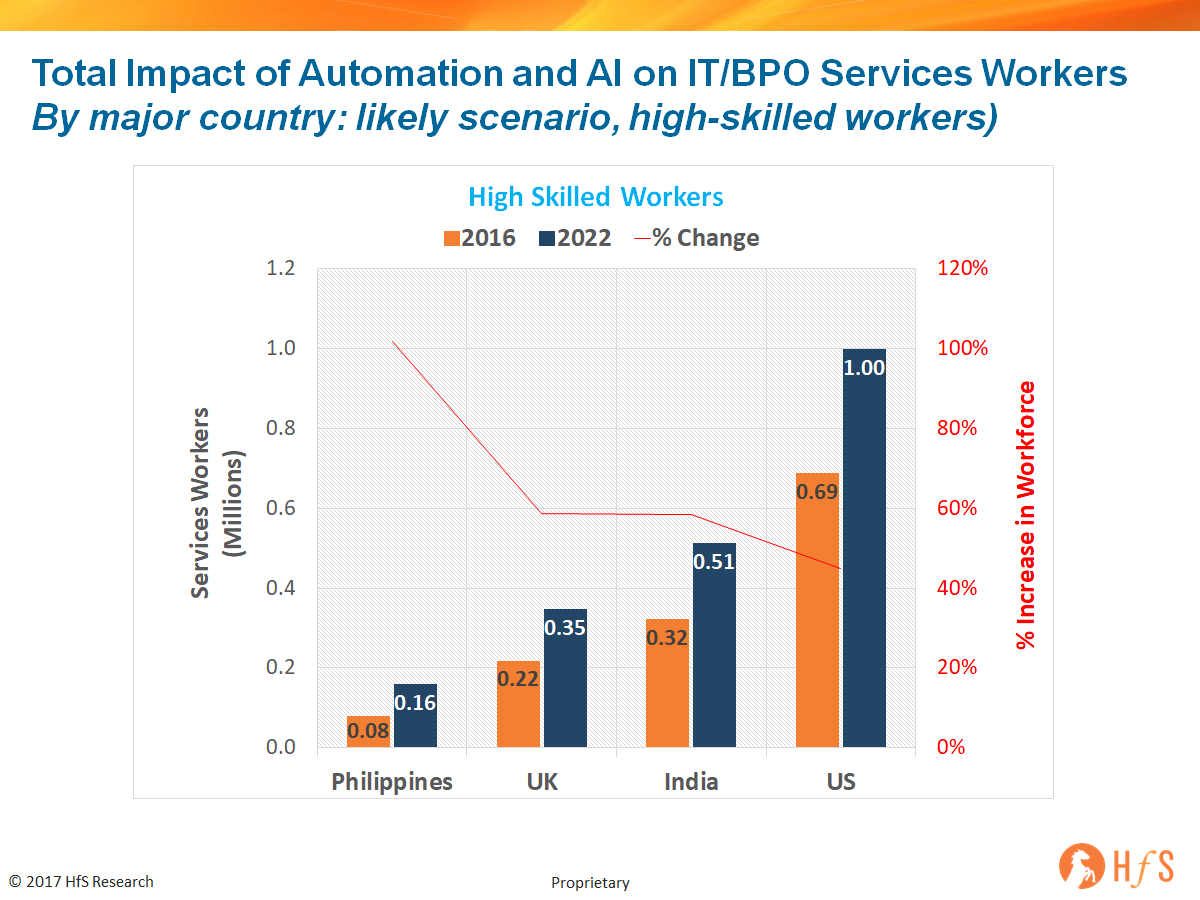

When we look into the high-end, this is where we see most positive impact, in terms of job creation:

As this data illustrates, the more we automate and digitize, and the more we adopt human + machine technologies, such as machine learning and cognitive solutions, the more we need people to developing skills in managing automated workflows, machine learning mechanisms, being able to interpret data, and service increasingly complex customer and employee needs. So when we take into account the total impact of automation and AI on services jobs, the impact is not nearly as severe as so many of the hypesters and fear-mongerers are prophesizing:

Philippines should actually increase its service delivery population due to its dominance in voice and capabilities to support increasingly complex and personalized customer models, the UK should be flat, especially with the challenges of Brexit and the slowdown in low cost worker immigration, while both India and the US will see a total worker reduction estimated at the 10% level between by 2022. You can view the total impact on the global services industry – a worker population decline of 7.5% here:

The Bottom-line: The rote jobs are going to be eroded, but there is time on our side to develop the new skills we need

The big narrative here isn’t about what’s going away, but more about what is emerging in its place. The next fives years we can manage, it’s the five after that when the impact on labor becomes much more challenging. Transaction roles at the bottom of the value chain have been under threat for many years now – with the impact of low cost location delivery and better technology. Now the emergence of RPA is eventually going to sound the death knell for most high-throughput, high-intensity jobs, as both service providers and enterprises master the ability to apply these technologies effectively. The good news is this takes time and there is no huge burning platform to do this overnight from most enterprises.

So our message to all stakeholders on operations and services is simply to get out of your comfort zones, accept that new skills are replacing old ones, and it’s critical we have a plan to train, develop and invest in changing what we have. I will leave you with six things to think about as you ponder your own value to this industry and your firm:

- Which customers have you delighted recently?

- What new relationships have you made that add value to our business?

- What work have you done that excited people inside and outside of the business?

- How are you helping energize your colleagues and exciting them with new ideas?

- How have you helped add value to new business wins?

- How have you contributed to new initiatives that improve productivity and effectiveness?

HfS subscribers can access the full report by clicking here

*Research Methodology

HfS has taken the following assumptions to form this size and forecast for the services industry:

A more aggressive uptake of RPA and Autonomic plus adoption of Cognitive in second half 2017

Leading stakeholders start to educate the market more realistically

The adoption of RPA, RDA, Cognitive Computing and AI reaches exponential growth

Visibility on impact through details in financial earnings calls and beyond

Stronger impact on supply-side, more marginal on buy-side

30% Reskilling to medium and high skilled jobs, with 2/3rd to medium and 1/3 to high

HfS bases its data findings on the following sources:

- HfS State of Automation survey (June 2017) covering the dynamics of 400 business operations and IT executives leading automation initiatives;

- Market expertise of the HfS analysts across RPA, AI, BPO, IT Services and key industries;

- Service provider interviews to understand their automation adoption across global delivery centers and emerging skills competencies with automation and AI solutions;

- Government data and data published by industry associations, such as NASSCOM, US Bureau of Labor Statistics, IBAP, OECD Employment and Labour Market Statistics and Office of National Statistics, which provide data on IT industries and education – including specific information about job creation and the impact of automation;

- HfS services contracts database, which provides analysis of service providers contracting activity;

- Qualitative interviews with service buyers across different industries and company sizes;

- Executive-level interviews with key independent advisors in the automation arena, such as KPMG, EY, Deloitte and Symphony Ventures to understand rate of adoption and other core issues related to automation and AI.

Posted in : Cognitive Computing, Robotic Process Automation

Great data. Can you shed light on the impact of AI and not just automation here?

Thanks

Very insightful data. Shows a realistic view of the impact of automation. Also agree with the bigger impact in 2022 – that timeframe feels right.

JS

@Adam – most customers are focused on getting RPA effective, with an eye on RDA and more digital automation cababilitles. However, our recent research into 400 major enteprises shows that 80% of them are pursuing AI as part of their automation agenda (directives from the C-Suite) and we expect far greater uptake of this in the medium term as automation matures. Hence, we see 2021-2022 as the years when the real adoption build up happens as clients genuinely have better governance and understand how to approach, staff and executive against the human-plus-machine models. The next five years are not too scary… it’s the five after that where we expect much more dramatic impact on operations,

PF

Phil and Jamie –

The most realistic view yet on the true impact. Well done

Very interesting data points. This indicates that the IT/BPO industry can been seen as an engine to create the ‘talent of the future’, since the industry will have ’embedded education’ as it shifts towards machine learning and cognitive solutions.

Really useful data, Phil. And I agree with the pace of the market you have reflected here. Automation is a long journey for clients, not an overnight once,

Alan

Great insights, Phil. What is your opinion on the growing need for “Content Creation” ? Look at the growing demand for “Content Writers” over the past two to three years on freelance sites & in the growth of the Media industry. Do you think that this large & rapidly expanding opportunity for Content Writers & related Digital Marketing professionals, will not be a part of the Outsourcing industry ? Will the new Media industry ( RR Donnelly , AC Nielsen etc) , successfully eating into the traditional Advertising Agency work for many years, not see competition from the IT&BPO players ?

There is a vast range of Content Creation which is being outsourced today. The “technical” content writing is effectively “research” work being outsourced & makes one wonder why the Analysts working in the BPO companies are ignoring it. As your 6 points to ponder over highlight, the Analysts working in an outsourcing company, will have to learn to work closely with their customers & have the ability to sell their analysis/research ( digitally) to their customer’s customers. Offshoring & large aggregation of such Content Creation work, will of course be a challenge & it reflects in the small size ( 10 to 20 employee, often lead by an ex-employee ) Content Creation Outsourcing companies which are being set up. Don’t you think the IT& BPO industry will also start competing with the New Media providers, over the next few years ?

Underlying the A.I. of today ( including Watson) is text ( word sequence) & digital image recognition ( also linked to word association). All of this drives up the need for more content, especially “curated content” i.e. researched & customized content. Surveys/Data & authentication of data is one part of it. The key piece which drives internet content of course is photos/images & that is going to be a key challenge for the IT/BPO players of today, making a foray into the Content creating space. Alliances/Acquisitions of photo-stock portals ( Alamy/ Shutter-Stock etc), may be a solution.

Your thoughts on such a convergence ….

Hi Phil,

Isnt it true that we are at the inception curve of the RPA wave ? Companies are still figuring out the “how” and it is just scratching the surface currently. It is also influenced by the current capability of the product tools; thereby limiting its scope to the simple tasks. This is very akin to the initial phase of the outsourcing journey.

Therefore, i concur that the real impact is still a few years out as technology and product tools become more advanced to slowly graduate towards higher skill jobs.

GREAT Insight data. Very useful updates and all IT companies to plan for alternative actions and skill upgrade to meet future trends.

Creating mid-to-high skilled job opportunities is one thing. Having enough mid to high skilled people to fill them is another.

This is the challenge… it’ll be a lot of retraining of existing people, and hiring of graduates with a very different approach

There is significant retraining effort that is required. A few companies have recognized this and have initiatives underway. Many others are yet to recognize the need to do this.

Phil,

Thanks for the analysis. I feel if the market understood this fully, we can anticipate many large transformation deals. As you very well know, automation done in pockets will not reap the desired outcome. It goes hand in hand with the technology & business transformation. It also gives the service provider the ability to transform their workforce and get ready over time , as per specific needs of their customers.

Partha

Looks like total spend will still increase steadily – As the addition to Mid-High skill workforce (and / or re-skilling) will incur more IT budget than the savings due to diminishing low-skill workforce… overall gain in investment fueling skill-upgrade and overall efficiency and throughput of the industry.

@Partha – the real area to watch here is how the providers build RPA into their delivery models, which is how most customers will ultimately benefit – services that are decreasing in cost, with the same KPIs (hopefully better as processes are more digitized). The more the focus shifts to outcomes, the more the onus will shift to the quality of talent to provide analytics and insights. As discussed, this is an evolution over time, but more like a 3-5 year shift, as opposed to a couple of decades (which was the first phase of moving from onshore to offshore).

PF

@Mandar – the demand for services is still increasing – the change is the way these services are being delivered to drive more savings over time and keep competitive with the decreasing prices. Hence the trend here is modest overall expenditure increase with a modest decrease in staff to deliver these services, underpinned by improvements in automation and quality of services dues to realigned talent. Some providers will up their game to deliver this effectively, others will struggle and wind up delivering the same old services with less people and for less profit. It’s going to be a painful squeeze for many firms as this industry matures,

PF

Nice one Phil. We are seeing that running Ops + RPA itself is creating a new kind of employee who has to work with automation, is comfortable managing BOTs as well as humans. This pivot isn’t that difficult and people at the associate/ Team Lead level are picking this up very quickly. On the nascent ML/AI part of the game, things are indeed much more difficult and we see a need to move to ops analyst kind of roles with an enhanced need for reskilling.